Videos

(a)

Record the journal entries and

(a)

Explanation of Solution

Accounting Cycle: The accounting cycle refers to the entire process of recording the accounting transactions of an organization and then processing them. The accounting cycle starts when a transaction takes places and it ends at the time when these transactions are recorded in the financial statements of the company.

The following are the rules of debit and credit:

- Increase in assets and expenses accounts are debited. Decrease in liabilities and

stockholders’ equity accounts are debited. - Increase in liabilities, revenues, and stockholders’ equity accounts are credited. Decreases in all asset accounts are credited.

Prepare the journal entries for Incorporation C during 2017:

| Date | Account Title and Description | Post Ref. |

Debit ($) |

Credit ($) |

| February 1 | Cash | 13,000 | ||

| Common Stock | 7,500 (1) | |||

| Paid-in-Capital in Excess of par value – Common Stock | 5,500 (2) | |||

| (To record the issuance of common stock) | ||||

| February 1 | Cash | 8,000 | ||

| Notes payable | 8,000 | |||

| (To record the issuance of notes payable.) | ||||

| February 1 | Equipment | 9,020 | ||

| Cash | 9,020 | |||

| (To record the purchase of equipment) | ||||

| February 1 | Utility Expense | 220 | ||

| Cash | 220 | |||

| (To record the payment of utility expense) | ||||

| February 3 | Supplies | 980 | ||

| Accounts Payable | 980 | |||

| (To record the purchase of supplies on account) | ||||

| February 5 | Prepaid insurance | 2,460 | ||

| Cash | 2,460 | |||

| (To record the payment of insurance in advance) | ||||

| February 5 | Cash | 3,950 | ||

| Loss on Disposal of Plant Assets | 250 (3) | |||

| Equipment | 4,200 | |||

| (To record the cash received for sale of equipment) | ||||

| February 16 | 3,900 | |||

| Service Revenue | 3,900 | |||

| (To record the service revenue) | ||||

| February 17 | Cash | 540 | ||

| Unearned Service Revenue | 540 | |||

| (To record the unearned service revenue) | ||||

| February 18 | Accounts Payable | 300 | ||

| Cash | 300 | |||

| (To record the payment for accounts payable) | ||||

| February 20 | 900 (4) | |||

| Cash | 900 | |||

| (To record the purchase of treasury stock) | ||||

| February 23 | Accounts Receivable | 4,300 | ||

| Service Revenue | 4,300 | |||

| (To record the service revenue) | ||||

| February 24 | Salaries and Wages Expense | 3,840 (5) | ||

| Cash | 3,840 | |||

| (To record the payment of utility expense) | ||||

| Date | Account Title and Description | Post Ref. |

Debit ($) |

Credit ($) |

| February 25 | Cash | 2,500 | ||

| Accounts Receivable | 2,500 | |||

| (To record the cash received for accounts receivable) | ||||

| February 27 | Prepaid Expense | 220 | ||

| Cash | 220 | |||

| (To record the payment of prepaid expense) | ||||

| February 28 | Dividends | 940 (6) | ||

| Cash | 940 | |||

| (To record the payment of dividends) |

Table (1)

Working Note 1: Calculate the amount of common stock.

Total number of share issued = 5,000

Price per share = $1.5

Working Note 2: Calculate the amount of paid-in capital.

Common stock = $7,500 (1)

Cash received for common stock = $13,000

Working Note 3: Calculate the loss on disposal of plant asset.

Equipment cost = $4,200

Cash received from sale of equipment = $3,950

Working Note 4: Calculate the amount of treasury stock.

Number of shares purchased = 300

Price per share = $3

Working Note 5: Calculate the salaries and wages expense.

Per week wages = $480

Number of employees = 4

Number of weeks = 2

Working Note 6: Calculate the amount of dividends payable.

Dividend per share (common stock) = $0.20

Common stock outstanding = 4,700 (5,000 - 300)

(d)

Record the adjusting entries of Incorporation C during 2017.

(d)

Explanation of Solution

Adjusting entries are the journal entries that are recorded at an end of an accounting period. It adjusts the income and expense account to comply with the accrual based accounting. This accounting system states that the revenues should be recognized when it is earned, and the expenses should be recognized when it is incurred, irrespective to cash received or paid for it.

Journalize the adjusting entries.

| Date | Accounts title and Description | Post Ref. | Debit ($) | Credit ($) |

| February 28 | Accounts Receivable | 3,800 | ||

| Service Revenue | 3,800 | |||

| (To record the adjustment of service revenue) | ||||

| February 28 | Allowance for doubtful accounts | 200 | ||

| Accounts receivable | 200 | |||

| (To record the adjustment of account receivables) | ||||

| February 28 | 479 | |||

| Allowance for doubtful accounts | 479 | |||

| (To record the adjustment of bad debt expense) | ||||

| February 28 | 90 (7) | |||

| | 90 | |||

| (To record the adjustment of depreciation expense) | ||||

| February 28 | Insurance expense | 820 (8) | ||

| Prepaid insurance | 820 | |||

| (To record the adjustment of insurance expense) | ||||

| February 28 | Supplies expense | 580 (9) | ||

| Supplies | 580 | |||

| (To record the adjustment of supplies expense) | ||||

| February 28 | Unearned service revenue | 135 (10) | ||

| Service revenue | 135 | |||

| (To record the adjustment of service revenue) | ||||

| February 28 | Salaries and wages expense | 1,920 (11) | ||

| Salaries and wages payable | 1,920 | |||

| (To record the adjustment of salaries and wages expense) | ||||

| February 28 | Interest expense | 40 (12) | ||

| Interest payable | 40 | |||

| (To record the adjustment of interest expense) | ||||

| February 28 | Income tax expense | 779 (13) | ||

| Income tax payable | 779 | |||

| (To record the adjustment of income tax expense) |

Table (2)

Working Note 7: Calculate the amount of depreciation expense.

Equipment value = $4,820

Salvage value = $500

Life of building = 4 years

Working Note 8: Calculate the amount of insurance expense.

Insurance coverage per year = $9,840

Working Note 9: Calculate the amount of supplies expense.

Purchase = $980

Ending balance = $400

Working Note 10: Calculate the amount of service revenue adjusted.

Services collected in advance for 4 weeks = $540

Weeks adjusted for unearned service revenue = 1

Working Note 11: Calculate the amount of salaries and wages expense.

Wages per week = $480

Wages accrue for weeks = 1 weeks

Number of employees = 4

Working Note 12: Calculate the amount of interest expense.

Amount of notes payable = $8,000

Percentage of interest = 6%

Working Note 13: Calculate the income tax expense.

Net income before tax = $3,896 (Refer Table 34)

Income tax rate = 20%

(b) and (e)

Post the above journal entries and adjusting entries to T-accounts of Incorporation C.

(b) and (e)

Explanation of Solution

T Accounts: T- accounts are prepared for all the business transactions. First, journal entries are passed and then transferred to the respective ledger accounts where they are recorded, and summarized in either side of the ‘T’ format. It is divided into two parts by a vertical line, that is, the left side and the right side. The left side of the T-account is known as the debit side, and the right side of the T-account is known as the credit side. The account name appears on the top of the T-account.

The following are the T-accounts.

Cash Account:

| Cash Account | |||||

| Date | Particulars | Debit ($) | Date | Particulars | Credit ($) |

| Common stock | 7,500 | Equipment | 9,020 | ||

| Paid-in capital in Excess of par value – Common stock | 5,500 | Utilities expense | 220 | ||

| Notes Payable | 8,000 | Prepaid insurance | 2,460 | ||

| Equipment | 3,950 | Accounts payable | 300 | ||

| Unearned service revenue | 540 | Treasury stock | 900 | ||

| Accounts receivable | 2,500 | Salaries and wages payable | 3,840 | ||

| Prepaid expense | 220 | ||||

| Dividends | 940 | ||||

| Ending Balance | 10,090 | ||||

| Total | 27,990 | Total | 27,990 | ||

Table (3)

Accounts Receivable Account:

| Accounts Receivable Account | |||||

| Date | Particulars |

Debit ($) | Date | Particulars |

Credit ($) |

| Sales Revenue | 3,900 | Cash | 2,500 | ||

| Sales Revenue | 4,300 | Ending Balance | 5,700 | ||

| Total | 8,200 | Total | 8,200 | ||

| Opening Balance | 5,700 | Adjustment | 200 | ||

| Adjustment | 3,800 | Ending Balance | 9,300 | ||

| Total | 9,500 | Total | 9,500 | ||

Table (4)

Allowance for Doubtful Accounts:

| Allowance for doubtful Accounts | |||||

| Date | Particulars |

Debit ($) | Date | Particulars |

Credit ($) |

| Adjustment | 200 | Adjustment | 479 | ||

| Ending Balance | 279 | ||||

| Total | 479 | Total | 479 | ||

Table (5)

Supplies Account:

| Supplies Account | |||||

| Date | Particulars |

Debit ($) | Date | Particulars | Credit ($) |

| Accounts Payable | 980 | Ending Balance | 980 | ||

| Total | 980 | Total | 980 | ||

| Opening Balance | 980 | Adjustment | 580 | ||

| Ending Balance | 400 | ||||

| Total | 980 | Total | 980 | ||

Table (6)

Prepaid Insurance Account:

| Prepaid Insurance Account | |||||

| Date | Particulars |

Debit ($) | Date | Particulars | Credit ($) |

| Cash | 2,460 | Ending Balance | 2,460 | ||

| Total | 2,460 | Total | 2,460 | ||

| Opening Balance | 2,460 | Adjustment | 820 | ||

| Ending Balance | 1,640 | ||||

| Total | 2,460 | Total | 2,460 | ||

Table (7)

Prepaid Expenses Account:

| Prepaid Expenses Account | |||||

| Date | Particulars |

Debit ($) | Date | Particulars | Credit ($) |

| Cash | 220 | Ending Balance | 220 | ||

| Total | 220 | Total | 220 | ||

Table (8)

Equipment Account:

| Equipment Account | |||||

| Date | Particulars |

Debit ($) | Date | Particulars | Credit ($) |

| Cash | 9,020 | Cash | 3,950 | ||

| Loss on disposal | 250 | ||||

| Ending Balance | 4,820 | ||||

| Total | 9,020 | Total | 9,020 | ||

Table (9)

Accumulated Depreciation - Equipment Account:

| Accumulated Depreciation - Equipment Account | |||||

| Date | Particulars |

Debit ($) | Date | Particulars | Credit ($) |

| Ending Balance | 90 | Adjustment | 90 | ||

| Total | 90 | Total | 90 | ||

Table (10)

Accounts Payable Account:

| Accounts Payable Account | |||||

| Date | Particulars |

Debit ($) | Date | Particulars | Credit ($) |

| Cash | 300 | Supplies | 980 | ||

| Ending Balance | 680 | ||||

| Total | 980 | Total | 980 | ||

Table (11)

Notes Payable Account:

| Notes Payable Account | |||||

| Date | Particulars |

Debit ($) | Date | Particulars | Credit ($) |

| Ending Balance | 8,000 | Cash | 8,000 | ||

| Total | 8,000 | Total | 8,000 | ||

Table (12)

Salaries and Wages Payable Account:

| Salaries and Wages Payable Account | |||||

| Date | Particulars |

Debit ($) | Date | Particulars | Credit ($) |

| Ending Balance | 1,920 | Adjustment | 1,920 | ||

| Total | 1,920 | Total | 1,920 | ||

Table (13)

Interest Payable Account:

| Interest Payable Account | |||||

| Date | Particulars |

Debit ($) | Date | Particulars | Credit ($) |

| Ending Balance | 40 | Adjustment | 40 | ||

| Total | 40 | Total | 40 | ||

Table (14)

Income Tax Payable Account:

| Income Tax Payable Account | |||||

| Date | Particulars |

Debit ($) | Date | Particulars | Credit ($) |

| Ending Balance | 779 | Adjustment | 779 | ||

| Total | 779 | Total | 779 | ||

Table (15)

Unearned Service Revenue Account:

| Unearned Service Revenue Account | |||||

| Date | Particulars |

Debit ($) | Date | Particulars | Credit ($) |

| Ending Balance | 540 | Cash | 540 | ||

| Total | 540 | Total | 540 | ||

| Adjustment | 135 | Opening balance | 540 | ||

| Ending Balance | 405 | ||||

| Total | 540 | Total | 540 | ||

Table (16)

Common Stock Account:

| Common Stock Account | |||||

| Date | Particulars |

Debit ($) | Date | Particulars | Credit ($) |

| Ending Balance | 7,500 | Cash | 7,500 | ||

| Total | 7,500 | Total | 7,500 | ||

Table (17)

Paid-In Capital in Excess of Par Value - Common Stock Account:

| Paid-In Capital in Excess of Par Value - Common Stock Account | |||||

| Date | Particulars |

Debit ($) | Date | Particulars | Credit ($) |

| Ending Balance | 5,500 | Cash | 5,500 | ||

| Total | 5,500 | Total | 5,500 | ||

Table (18)

Dividends Account:

| Dividends Account | |||||

| Date | Particulars |

Debit ($) | Date | Particulars | Credit ($) |

| Cash | 940 | Ending Balance | 940 | ||

| Total | 940 | Total | 940 | ||

Table (19)

Treasury Stock Account:

| Treasury Stock Account | |||||

| Date | Particulars |

Debit ($) | Date | Particulars | Credit ($) |

| Cash | 900 | Ending Balance | 900 | ||

| Total | 900 | Total | 900 | ||

Table (20)

Retained Earnings Account:

| Retained Earnings Account | |||||

| Date | Particulars | Debit ($) | Date | Particulars | Credit ($) |

| Dividends | 940 | Income Summary | 3,117 | ||

| Ending Balance | 2,177 | ||||

| Total | 3,117 | Total | 3,117 | ||

Table (21)

Income Summary Account:

| Income Summary Account | |||||

| Date | Particulars | Debit ($) | Date | Particulars | Credit ($) |

| Bad debt expense | 479 | Service Revenue | 12,135 | ||

| Depreciation expense | 90 | ||||

| Insurance expense | 820 | ||||

| Supplies expense | 580 | ||||

| Salaries and wages expense | 5,760 | ||||

| Interest expense | 40 | ||||

| Utilities expense | 220 | ||||

| Loss on disposal of assets | 250 | ||||

| Income tax expense | 779 | ||||

| Retained earnings | 3117 | ||||

| Total | 12,135 | Total | 12,135 | ||

Table (22)

Service Revenue Account:

| Service Revenue Account | |||||

| Date | Particulars |

Debit ($) | Date | Particulars |

Credit ($) |

| Ending Balance | 8,200 | Accounts receivable | 3,900 | ||

| Accounts receivable | 4,300 | ||||

| Total | 8,200 | Total | 8,200 | ||

| Ending Balance | 12,135 | Opening balance | 8,200 | ||

| Adjustment | 3,800 | ||||

| Adjustment | 135 | ||||

| Total | 12,135 | Total | 12,135 | ||

Table (23)

Utilities Expense Account:

| Utilities Expense Account | |||||

| Date | Particulars |

Debit ($) | Date | Particulars |

Credit ($) |

| Cash | 220 | Ending Balance | 220 | ||

| Total | 220 | Total | 220 | ||

Table (24)

Salaries and Wages Expense Account:

| Salaries and Wages Expense Account | |||||

| Date | Particulars |

Debit ($) | Date | Particulars |

Credit ($) |

| Cash | 3,840 | Ending Balance | 3,840 | ||

| Total | 3,840 | Total | 3,840 | ||

| Opening balance | 3,840 | Ending balance | 5,760 | ||

| Adjustment | 1,920 | ||||

| Total | 5,760 | Total | 5,780 | ||

Table (25)

Insurance Expense Account:

| Insurance Expense Account | |||||

| Date | Particulars |

Debit ($) | Date | Particulars |

Credit ($) |

| Adjustment | 820 | Ending Balance | 820 | ||

| Total | 820 | Total | 820 | ||

Table (26)

Depreciation Expense Account:

| Depreciation Expense Account | |||||

| Date | Particulars |

Debit ($) | Date | Particulars |

Credit ($) |

| Adjustment | 90 | Ending Balance | 90 | ||

| Total | 90 | Total | 90 | ||

Table (27)

Bad Debt Expense Account:

| Bad Debt Expense Account | |||||

| Date | Particulars |

Debit ($) | Date | Particulars |

Credit ($) |

| Adjustment | 479 | Ending Balance | 479 | ||

| Total | 479 | Total | 479 | ||

Table (28)

Supplies Expense Account:

| Supplies Expense Account | |||||

| Date | Particulars |

Debit ($) | Date | Particulars |

Credit ($) |

| Adjustment | 580 | Ending Balance | 580 | ||

| Total | 580 | Total | 580 | ||

Table (29)

Interest Expense Account:

| Interest Expense Account | |||||

| Date | Particulars |

Debit ($) | Date | Particulars |

Credit ($) |

| Adjustment | 40 | Ending Balance | 40 | ||

| Total | 40 | Total | 40 | ||

Table (30)

Loss on Disposal of Plant Assets Expense Account:

| Loss on Disposal of Plant Assets Expense Account | |||||

| Date | Particulars |

Debit ($) | Date | Particulars |

Credit ($) |

| Cash | 250 | Ending Balance | 250 | ||

| Total | 250 | Total | 250 | ||

Table (31)

Income Tax Expense Account:

| Income Tax Expense Account | |||||

| Date | Particulars |

Debit ($) | Date | Particulars |

Credit ($) |

| Adjustment | 779 | Ending Balance | 779 | ||

| Total | 779 | Total | 779 | ||

Table (32)

(c) and (f)

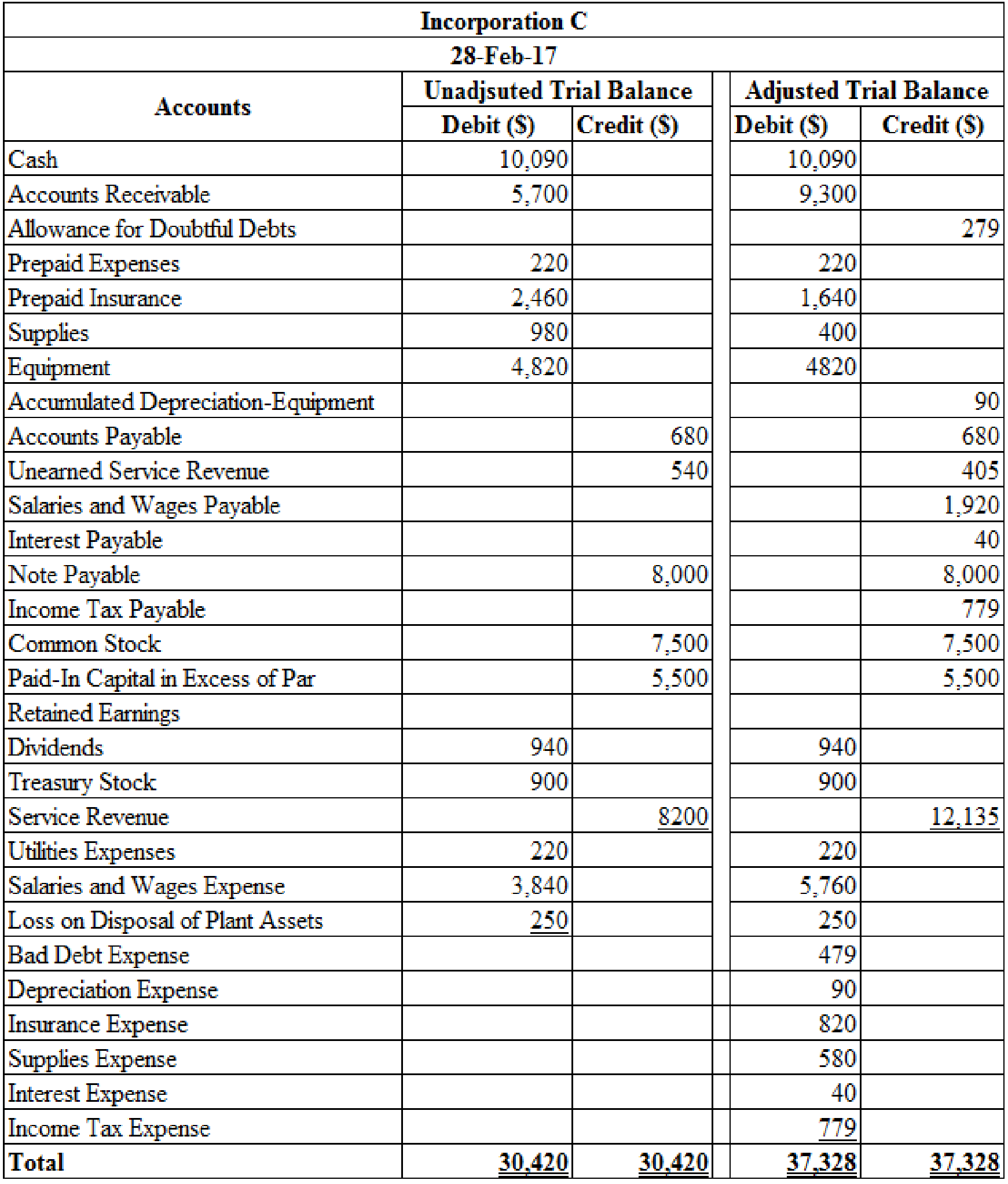

Prepare trial balance for Incorporation C as on February 28, 2017.

(c) and (f)

Answer to Problem 11.2CACR

Trial balance: This is a statement prepared to show all the year-end account balances of a business. The balances are shown in separate columns as debit and credit. Trial balance is made to check whether books of accounts of the business are arithmetically accurate.

The following is the adjusted trial balance of Incorporation C as on February 28, 2017.

Table (33)

Explanation of Solution

The trial balance as shown in Table (33) is prepared after placing the journal entries and adjusting entries to the ledger account. It will show the ending balance of all the accounts. Here, the total debit balance is matched with the credit balance.

(g)

Prepare the income statement, retained earnings statement, and balance sheet of Incorporation C for the year ended February 28, 2017.

(g)

Explanation of Solution

Prepare the income statement of Incorporation C.

Income statement: This is a financial statement that shows the net income earned or net loss suffered by a company through reporting all the revenues earned and expenses incurred by the company over a specific period of time. An income statement is also known as an operations statement, an earnings statement, a revenue statement, or a profit and loss statement. The net income is the excess of revenue over expenses.

| Incorporation C | ||

| Income Statement | ||

| For the Year Ended February 28, 2017 | ||

| Particulars | Amount ($) | Amount ($) |

| Service revenue | 12,135 | |

| Operating expenses | ||

| Salaries and wages expenses | 5,760 | |

| Utilities expense | 220 | |

| Bad debt expense | 479 | |

| Depreciation expense | 90 | |

| Insurance expense | 820 | |

| Supplies expense | 580 | |

| Total operating expenses | (7,949) | |

| Income from Operations | 4,186 | |

| Loss on disposal of plant assets | 250 | |

| Interest expense | 40 | (290) |

| Income before income taxes | 3,896 | |

| Income tax expense | 779 | |

| Net income | 3,117 | |

Table (34)

Prepare a retained earnings statement of Incorporation C for the year ended February 28, 2017.

Retained Earnings Statement is one of the financial statement, which shows the amount of the net income retained by a company at a particular point of time for reinvestment and used to pay its debts and obligations. It shows the amount of earnings that is not paid as dividends to the shareholders.

| Incorporation C | |

| Retained Earnings Statement | |

| For the Year Ended February 28, 2017 | |

| Details | Amount ($) |

| Beginning Balance of Retained earnings | 0 |

| Add: Net Income for the year | 3,117 |

| Total Retained Earnings | 3,117 |

| Less: Dividends | (940) |

| Ending balance of Retained Earnings | 2,177 |

Table (35)

Prepare the balance sheet of Incorporation C for the year ended February 28, 2017.

The balance sheet: This is a financial statement that shows the assets, liabilities, and stockholders’ equity of a company at a particular point of time. It reveals the financial health of a company. Thus, this statement is also called as the Statement of Financial Position. It helps the users to know about the creditworthiness of a company as to whether the Incorporation C has enough assets to pay off its liabilities.

| Incorporation C | ||||

| Balance Sheet | ||||

| As of February 28, 2017 | ||||

| Assets | Amount ($) | Amount ($) | Amount ($) | Amount ($) |

| Current assets | ||||

| Cash | $10,090 | |||

| Accounts receivable | $9,300 | |||

| Less: Allowance for doubt. accounts | 279 | 9,021 | ||

| Prepaid expenses | 220 | |||

| Prepaid insurance | 1,640 | |||

| Supplies | 400 | |||

| Total current assets | 21,371 | |||

| Property, plant and equipment | ||||

| Equipment | 4,820 | |||

| Less: Accumulated depreciation-equipment | 90 | 4,730 | ||

| Total Assets | $26,101 | |||

| Liabilities and Stockholders’ Equity | ||||

| Current liabilities | ||||

| Accounts payable | $680 | |||

| Unearned service revenue | 405 | |||

| Salaries and wages payable | 1,920 | |||

| Income tax payable | 779 | |||

| Interest payable | 40 | |||

| Total current liabilities | $3,824 | |||

| Note payable, 6% due 2/1/2019 | 8,000 | |||

| Total Liabilities | 11,824 | |||

| Stockholders' Equity | ||||

| Common stock, $1.50 par | $7,500 | |||

| Paid-in capital in excess of par | 5,500 | 13,000 | ||

| Retained earnings | 2,177 | 15,177 | ||

| Less: Treasury stock at cost | 900 | |||

| Total stockholders' equity | 14,277 | |||

| Total Liabilities and Stockholders' equity | $26,101 | |||

Table (36)

(h)

Record the closing entries of Incorporation C for the month February.

(h)

Explanation of Solution

Closing entries: These refer to the journal entries that are recorded at the end of an each accounting period. It closes all revenue accounts earned, and all expenses account incurred during the current accounting year to the income summary account.

Record the closing entry of revenue.

| Date | Accounts and Description | Post Ref |

Debit ($) |

Credit ($) |

| February 28 | Service Revenue | 12,135 | ||

| Income Summary | 12,135 | |||

| (To close the revenues.) |

Table (37)

Description:

- Service revenue is revenue and it increases the value of equity. To close the revenue account it should be debited. Therefore, debit service revenue account by $12,135.

- Income Summary is a component of equity and it increases by $12,135. Therefore, credit income summary account by $12,135.

Record the closing entries of expenses and other debit accounts.

| Date | Accounts and Description | Post Ref |

Debit ($) |

Credit ($) |

| February 28 | Income Summary | 9,018 | ||

| Bad Debt Expense | 479 | |||

| Depreciation Expense | 90 | |||

| Insurance Expense | 820 | |||

| Supplies Expense | 580 | |||

| Salaries and Wages Expense | 5,760 | |||

| Interest Expense | 40 | |||

| Utilities Expense | 220 | |||

| Loss on Disposal of Plant Assets | 250 | |||

| Income Tax Expense | 779 | |||

| (To close expenses and other debit accounts) |

Table (38)

Description:

- Income summary is a component of equity and it decreases by $9,018. Therefore, debit income summary account by $9,018.

- Bad debt expense, Depreciation expense, Insurance expense, Supplies Expense, Salaries and wages expense, Interest expense, Utilities expense, Loss on disposal of plant assets, and Income tax expense accounts are closed by transferring their amount to Income Summary account. Therefore, credit all these expense with their respective amounts.

Record the closing entry of income summary account.

| Date | Accounts and Description | Post Ref |

Debit ($) |

Credit ($) |

| February 28 | Income Summary | 3,117 | ||

| Retained Earnings | 3,117 | |||

| (To close income summary account) |

Table (39)

Description:

- Income summary is a component of equity and it decreases by $3,117. Therefore, debit income summary account by $3,117.

- Retained earnings are component of equity and it increases by $3,117. Therefore, credit retained earnings account by $3,117.

Record the closing entry for dividends.

| Date | Accounts and Description | Post Ref | Debit ($) | Credit ($) |

| February 28 | Retained Earnings | 940 | ||

| Dividends | 940 | |||

| (To close the dividends account to retained earnings account) |

Table (40)

Description:

- Retained Earnings amount is decreased because the dividends are transferred and deducted from retained earnings. Therefore, debit retained earnings account with $940.

- Dividends have a debit balance and are transferred to retained earnings account. Therefore, credit dividends account with $940.

Want to see more full solutions like this?

Chapter 11 Solutions

FINANCIAL ACCT.:TOOLS...(LL)-W/ACCESS

- During 2012, Ponce Towers issued 30,000 additional shares of common stock on June 1 and 24,000 on November 1. The company earned 602,000 from continuing operations and 28,000 from another segment of the business that was discontinued during the year. Use your completed worksheet to prepare a computation of earnings per share for 2012. Erase any data in the Data Section that are not required for 2012. Save the solution for 2012 as EPS3 and print the results.arrow_forwardPonce Towers, Inc., had 50,000 shares of common stock and 10,000 shares of 100 par value, 8% preferred stock outstanding on January 1, 2011. Each share of preferred stock is convertible into four shares of common stock. The stock has not been converted. During the year, Ponce Towers issued additional shares of common stock as follows: For 2011, Ponce Towers, Inc., had income from continuing operations of 545,000 and a 72,000 loss from discontinued operations (net of tax). As vice president of finance for the firm, you have been asked to calculate earnings per share for 2011. The worksheet EPS has been provided to assist you.arrow_forwardBastion Corporation earned net income of $200,000 this year. The company began the year with 10,000 shares of common stock and issued 5,000 more on April 1. They issued $7,500 in preferred dividends for the year. What is the EPS for the year for Bastion?arrow_forward

- Longmont Corporation earned net income of $90,000 this year. The company began the year with 600 shares of common stock and issued 500 more on April 1. They issued $5,000 in preferred dividends for the year. What is the numerator of the EPS calculation for Longmont?arrow_forwardSelected transactions completed by Equinox Products Inc. during the fiscal year ended December 31, 2016, were as follows: a. Issued 15,000 shares of 0 par common stock at 0, receiving cash. b. Issued 4,000 shares of 80 par preferred 5% stock at 100, receiving cash. c. Issued 500,000 of 10-year, 5% bonds at 104, with interest payable semiannually. d. Declared a quarterly dividend of 0.50 per share on common stock and 1.00 per share on preferred stock. On the date of record, 100,000 shares of common stock were outstanding, no treasury shares were held, and 20,000 shares of preferred stock were outstanding. e. Paid the cash dividends declared in (d). f. Purchased 7,500 shares of Solstice Corp. at 40 per share, plus a 150 brokerage commission. The investment is classified as an available-for-sale investment. g. Purchased 8,000 shares of treasury common stock at 33 per share. h. Purchased 40,000 shares of Pinkberry Co. stock directly from the founders for 24 per share. Pinkberry has 125,000 shares issued and outstanding. Equinox Products Inc. treated the investment as an equity method investment. i. Declared a 1.00 quarterly cash dividend per share on preferred stock. On the date of record, 20,000 shares of preferred stock had been issued. j. Paid the cash dividends to the preferred stockholders. k. Received 27,500 dividend from Pinkberry Co. investment in (h). l. Purchased 90,000 of Dream Inc. 10-year, 5% bonds, directly from the issuing company, at their face amount plus accrued interest of 375. The bonds are classified as a held- to-maturitv long-term investment. m. Sold, at 38 per share, 2,600 shares of treasury common stock purchased in (g). n. Received a dividend of 0.60 per share from the Solstice Corp. investment in (f). o. Sold 1,000 shares of Solstice Corp. at 545, including commission. p. Recorded the payment of semiannual interest on the bonds issued in (c) and the amortization of the premium for six months. The amortization is determined using the straight-line method, q. Accrued interest for three months on the Dream Inc. bonds purchased in (1). r. Pinkberry Co. recorded total earnings of 240,000. Equinox Products recorded equity earnings for its share of Pinkberry Co. net income. s. The fair value for Solstice Corp. stock was 39.02 per share on December 31, 2016. The investment is adjusted to fair value, using a valuation allowance account. Assume Valuation Allowance for Available-for-Sale Investments had a beginning balance of zero. Instructions Journalize the selected transactions. After all of the transactions for the year ended December 31, 2016, had been posted [including the transactions recorded in part (1) and all adjusting entries], the data that follows were taken from the records of Equinox Products Inc. a. Prepare a multiple-step income statement for the year ended December 31, 2016, concluding with earnings per share. In computing earnings per share, assume that the average number of common shares outstanding was 100,000 and preferred dividends were 100,000. (Round earnings per share to the nearest cent.) b. Prepare a retained earnings statement for the year ended December 31, 2016. c. Prepare a balance sheet in report form as of December 31, 2016. Income statement data: Advertising expense 150,000 Cost of merchandise sold 3,700,000 Delivery expense 30,000 Depreciation expense -office buildings and equipment 30,000 Depreciation expensestore buildings and equipment 100,000 Dividend revenue 4,500 Gain on sale of investment 4,980 Income from Pinkberry Co. investment 76,800 Income tax expense 140,500 Interest expense 21,000 Interest revenue 2,720 Miscellaneous administrative expense 7.500 Miscellaneous selling expense 14,000 Office rent expense 50,000 Office salaries expense 170,000 Office supplies expense 10,000 Sales 5,254,000 Sales commissions 185,000 Sales salaries expense 385,000 Store supplies expense 21,000 Retained earnings and balance sheet data: Accounts payable 194,300 Accounts receivable 545,000 Accumulated depreciationoffice buildings and equipment 1,580,000 Accumulated depreciationstore buildings and equipment 4,126,000 Allowance for doubtful accounts 8,450 Available for sale investments (at cost) 260,130 Bonds payable. 5%. due 2024 500,000 Cash 246,000 Common stock, 20 par (400,000 shares authorized; 100,000 shares issued. 94,600 outstanding) 2,000,000 Dividends: Cash dividends for common stock 155,120 Cash dividends for preferred stock 100,000 Goodwill 500,000 Income tax payable 44,000 Interest receivable 1,125 Investment in Pinkberry Co. stock (equity method) 1,009,300 Investment in Dream Inc. bonds (long term) 90,000 Merchandise inventory [December 31, 2016). at lower of cost (FIFO) or market 778,000 Office buildings and equipment 4.320,000 Paid-in capital from sale of treasury stock 13,000 Excess of issue price over parcommon stock 886,800 Excess of issue price over parpreferred stock 150,000 Preferred 5% stock. 80 par (30,000 shares authorized; 20,000 shares issued] 1,600,000 Premium on bonds payable 19,000 Prepaid expenses 27,400 Retained earnings, January 1, 2016 9,319,725 Store buildings and equipment 12,560,000 Treasury stock (5,400 shares of common stock at cost of 33 per share) 178,200 Unrealized gain (loss) on available for sale investments (6,500) Valuation allowance for available for sale investments (6,500)arrow_forwardSelected transactions completed by Equinox Products Inc. during the fiscal year ended December 31, 2016, were as follows: a. Issued 15,000 shares of 20 par common stock at 30, receiving cash. b. Issued 4,000 shares of 80 par preferred 5% stock at 100, receiving cash. c. Issued 500,000 of 10-year, 5% bonds at 104, with interest payable semiannually. d. Declared a quarterly dividend of 0.50 per share on common stock and 1.00 per share on preferred stock. On the date of record, 100,000 shares of common stock were outstanding, no treasury shares were held, and 20,000 shares of preferred stock were outstanding. e. Paid the cash dividends declared in (d). f. Purchased 7,500 shares of Solstice Corp. at 40 per share, plus a 150 brokerage commission. The investment is classified as an available-for-sale investment. g. Purchased 8,000 shares of treasury common stock at 33 per share. h. Purchased 40,000 shares of Pinkberry Co. stock directly from the founders for 24 per share. Pinkberry has 125,000 shares issued and outstanding. Equinox Products Inc. treated the investment as an equity method investment. i. Declared a 1.00 quarterly cash dividend per share on preferred stock. On the date of record, 20,000 shares of preferred stock had been issued. j. Paid the cash dividends to the preferred stockholders. k. Received 27,500 dividend from Pinkberry Co. investment in (h). l. Purchased 90,000 of Dream Inc. 10-year, 5% bonds, directly from the issuing company, at their face amount plus accrued interest of 375. The bonds are classified as a heldtomaturity long-term investment. m. Sold, at 38 per share, 2,600 shares of treasury common stock purchased in (g). n. Received a dividend of 0.60 per share from the Solstice Corp. investment in (f). o. Sold 1,000 shares of Solstice Corp. at 45, including commission. p. Recorded the payment of semiannual interest on the bonds issued in (c) and the amortization of the premium for six months. The amortization is determined using the straight-line method. q. Accrued interest for three months on the Dream Inc. bonds purchased in (l). r. Pinkberry Co. recorded total earnings of 240,000. Equinox Products recorded equity earnings for its share of Pinkberry Co. net income. s. The fair value for Solstice Corp. stock was 39.02 per share on December 31, 2016. The investment is adjusted to fair value, using a valuation allowance account. Assume Valuation Allowance for Available-for-Sale Investments had a beginning balance of zero. Instructions 1. Journalize the selected transactions. 2. After all of the transactions for the year ended December 31, 2016, had been posted [including the transactions recorded in part (1) and all adjusting entries], the data that follows were taken from the records of Equinox Products Inc. a. Prepare a multiple-step income statement for the year ended December 31, 2016, concluding with earnings per share. In computing earnings per share, assume that the average number of common shares outstanding was 100,000 and preferred dividends were 100,000. (Round earnings per share to the nearest cent.) b. Prepare a retained earnings statement for the year ended December 31, 2016. c. Prepare a balance sheet in report form as of December 31, 2016.arrow_forward

- Nutritious Pet Food Companys board of directors declares a cash dividend of $1.00 per common share on November 12. On this date, the company has issued 12,000 shares but 2,000 shares are held as treasury shares. The company pays the dividend on December 14. What is the journal entry to record the payment of the dividend?arrow_forwardSpring Company is authorized to issue 500,000 shares of $2 par value common stock. In its first year, the company has the following transactions: Journalize the transactions and calculate how many shares of stock are outstanding at August 3.arrow_forwardPonce Towers, Inc., had 50,000 shares of common stock and 10,000 shares of 100 par value, 8% preferred stock outstanding on January 1, 2011. Each share of preferred stock is convertible into four shares of common stock. The stock has not been converted. During the year, Ponce Towers issued additional shares of common stock as follows: For 2011, Ponce Towers, Inc., had income from continuing operations of 545,000 and a 72,000 loss from discontinued operations (net of tax). Open the file EPS from the website for this book at cengagebrain.com. Enter all input items (AF) in the appropriate cells in the Data Section. Enter all formulas in the appropriate cells in the Answer Section. Enter your name in cell A1. Save the completed file as EPS2. Print the worksheet when done. Also print your formulas. Check figure: Basic earnings per share from continuing operations (cell D29), 5.94.arrow_forward

- James Incorporated is authorized to issue 5,000,000 shares of $1 par value common stock. In its second year of business, the company has the following transactions: Journalize the transactions.arrow_forwardJames Corporation earned net income of $90,000 this year. The company began the year with 600 shares of common stock and issued 500 more on April 1. They issued $5,000 in preferred dividends for the year. What is the EPS for the year for James (rounded to the nearest dollar)?arrow_forwardFortuna Company is authorized to issue 1,000,000 shares of $1 par value common stock. In its first year, the company has the following transactions: Journalize the transactions and calculate how many shares of stock are outstanding at August 3.arrow_forward

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning

Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT

EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College Financial & Managerial AccountingAccountingISBN:9781285866307Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial & Managerial AccountingAccountingISBN:9781285866307Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning