Videos

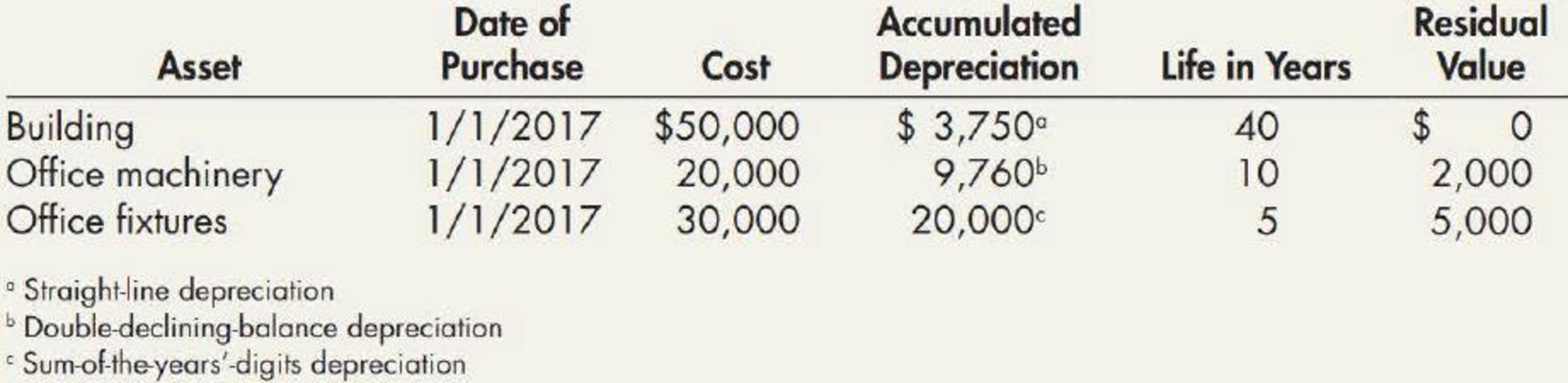

On December 31, 2019, Vail Company owned the following assets:

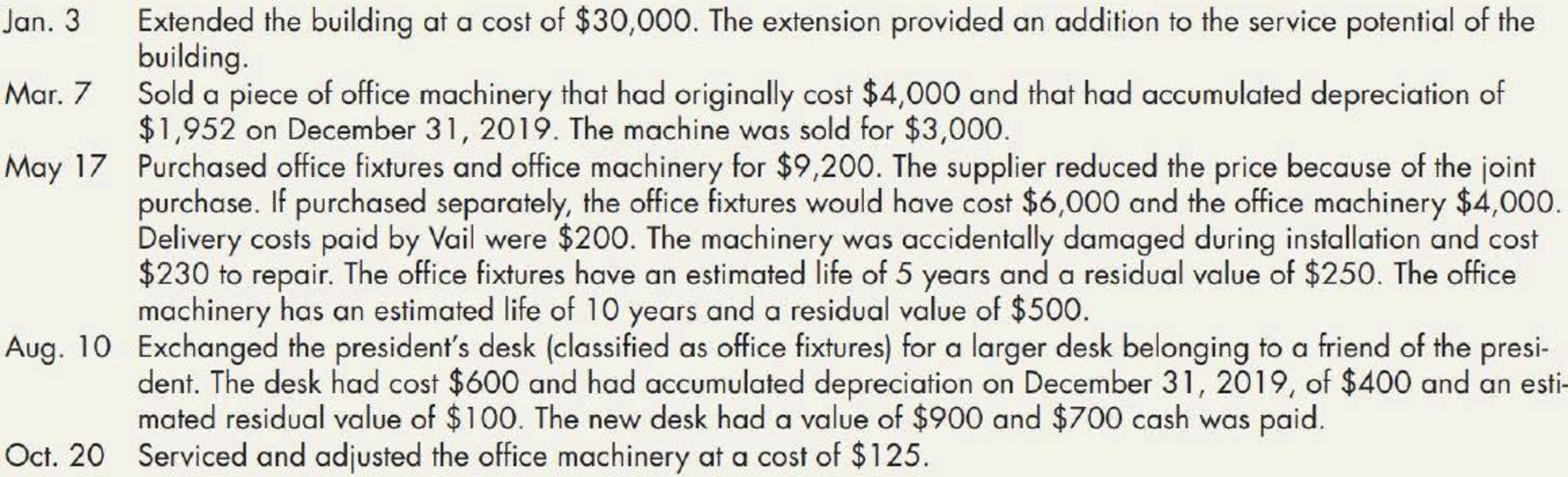

Vail computes depreciation and amortization expense to the nearest whole year. During 2020, Vail engaged in the following transactions:

Required:

- 1. Check the accuracy of the

accumulated depreciation balances at December 31, 2019. Round to the nearest whole dollar in all requirements. - 2. Prepare

journal entries to record the preceding events in 2020, as well as the year-end recording of depreciation expense. - 3. Prepare an Accumulated Depreciation account for each category of assets, enter the beginning balance,

post the journal entries from Requirement 2, and compute the ending balance.

1.

Calculate the accumulated depreciation balance at December 31, 2019 for the given assets, and check it’s ‘accuracy.

Explanation of Solution

Depreciation expense: Depreciation expense is a non-cash expense, which is recorded on the income statement reflecting the consumption of economic benefits of long-term asset on account of its wear and tear or obsolesces.

Straight-line depreciation method: The depreciation method which assumes that the consumption of economic benefits of long-term asset could be distributed equally throughout the useful life of the asset is referred to as straight-line method.

Sum-of- the-years’ digits method: Sum-of-the years’ digits method determines the depreciation by multiplying the depreciable base and declining fraction.

Double-declining-balance method: The depreciation method which assumes that the consumption of economic benefits of long-term asset is high in the early years but gradually declines towards the end of its useful life is referred to as double-declining-balance method.

Calculate the accumulated depreciation balance at December 31, 2019 for the given assets, and cross check its’ accuracy as follows:

Building:

Office machinery:

| Year | Beginning book value (A) |

Depreciation rate (2) (B) | Depreciation expense |

Ending book value |

| 2017 | 20,000 | 20% | 4,000 | 16,000 |

| 2018 | 16,000 | 20% | 3,200 | 12,800 |

| 2019 | 12,800 | 20% | 2,560 | 10,240 |

| Total | 9,760 |

Table (1)

Note: Ending book value of the prior year is considered as the beginning book value of current year.

Office fixtures:

| Year | Depreciation base (3) (A) |

Faction (4) (B) | Depreciation expense |

Ending book value |

| 2017 | 25,000 | 8,333 | 21,667 | |

| 2018 | 25,000 | 6,667 | 15,000 | |

| 2019 | 25,000 | 5,000 | 10,000 | |

| Total | 20,000 |

Table (2)

Working note (1):

Calculate the annual depreciation expense of building.

Working note (2):

Compute the straight line rate:

Useful life = 10 years

Working note (3):

Calculate the depreciable base of office fixtures.

Working note (4):

Calculate the denominator of the fraction for sum-of-the-year’s digit.

2.

Prepare necessary journal entries for the given transaction for 2020.

Explanation of Solution

Prepare necessary journal entries for the given transaction for 2020 as follows:

| Date | Account Title & Explanation | Debit ($) |

Credit ($) |

| January 3, 2020 | Building | 30,000 | |

| Cash | 30,000 | ||

| (To record the purchase of building for cash) | |||

| March 8, 2020 | Cash | 3,000 | |

| Accumulate depreciation-Office machinery | 1,952 | ||

| Office machinery | 4,000 | ||

| Gain on disposal of office machinery (5) | 952 | ||

| (To record a piece of office machinery sold during the year) | |||

| May 17, 2020 | Office fixtures (6) | 5,640 | |

| Office machinery (6) | 3,760 | ||

| Repair expense | 230 | ||

| Cash | 9,630 | ||

| (To record office fixtures and machinery purchased during the year) | |||

| August 10, 2020 | Depreciation expense (7) | 67 | |

| Accumulated depreciation-Office fixtures | 67 | ||

| (To record the depreciation expense incurred for office fixtures) | |||

| August 10, 2020 | Office fixtures | 900 | |

| Accumulated depreciation-Office fixtures (7) | 467 | ||

| Cash | 700 | ||

| Office fixtures | 600 | ||

| Gain on disposal of office fixtures (8) | 67 | ||

| (To record the office fixtures exchanged during the year ) | |||

| October 20, 2020 | Repair expense | 125 | |

| Cash | 125 | ||

| (To record the repair expense incurred during the year) | |||

| December 31, 2020 | Depreciation expense – Building (9) | 2,061 | |

| Depreciation expense - Office machinery (14) | 2,390 | ||

| Depreciation expense - Office fixtures (17) | 5,064 | ||

| Accumulated depreciation-Building | 2,061 | ||

| Accumulated depreciation-Office machinery | 2,390 | ||

| Accumulated depreciation-Office fixtures | 5,064 | ||

| (To record the depreciation expense of assets incurred at the end of the accounting year) |

Table (3)

Working note (5):

Calculate the gain on disposal of office machinery.

Working note (6):

Calculate the cost of office fixtures and office machinery.

| Particulars | Appraisal value (A) | Total appraisal value (B) |

Proportion | Total purchase cost (D) |

Cost ($) |

| Office fixtures | $6,000 | $10,000 | 60% |

$9,400 | $5,640 |

| Office machinery | $4,000 | 10,000 | 40% | $9,400 | $3,760 |

| Total | $10,000 | 100% | $9,400 |

Table (4)

Working note (7):

Calculate the depreciation expense of desk.

| Year | Depreciation base |

Faction (4) (B) | Depreciation expense |

| 2017 | 500 | 167 | |

| 2018 | 500 | 133 | |

| 2019 | 500 | 100 | |

| 2020 | 500 | 67 | |

| Total | 467 |

Table (5)

Working note (8):

Calculate the gain on disposal of desk.

Working note (9):

Calculate the depreciation expense of building at the end of the year 2020.

Working note (10):

Calculate the remaining office machinery at 2020.

Working note (11):

Calculate the depreciation expense of office machinery at the end of the year 2020.

Working note (12):

Calculate the depreciation expense for remaining office machinery under double declining balance method.

Working note (13):

Calculate depreciation expense of office machinery purchased during 2020 under double declining balance method.

Working note (14):

Calculate total depreciation expense of office machinery at 2020.

Working note (15):

Calculate the depreciation expense of remaining office fixtures under the sum of the year’s digit method.

Working note (16):

Calculate the depreciation expense of new office fixtures under the sum of the year’s digit method.

Working note (17):

Calculate the total depreciation expense for office fixtures.

3.

Prepare T-account for the accumulated depreciation, and calculate the ending balance of accumulated depreciation for the given assets.

Explanation of Solution

Prepare T-account for the accumulated depreciation, and calculate the ending balance of accumulated depreciation as follows:

| Accumulated depreciation - Building | |||

| December 31, 2019 | 3,750 | ||

| December 31, 2019 | $2,061 | ||

| Clos. Bal. | $5,811 | ||

| Accumulated depreciation – Office machinery | |||

| July 3, 2020 | $1,952 | December 31, 2019 | 9,760 |

| December 31, 2019 | $2,390 | ||

| Clos. Bal. | $10,198 | ||

| Accumulated depreciation – Office mixtures | |||

| October 8, 2020 | 467 | December 31, 2019 | $20,000 |

| October 8, 2020 | $67 | ||

| December 31, 2019 | $5,064 | ||

| Clos. Bal. | $24,664 | ||

Want to see more full solutions like this?

Chapter 11 Solutions

EBK INTERMEDIATE ACCOUNTING: REPORTING

- Soon after December 31, 2019, the auditor requested a depreciation schedule for trucks of Jarrett Trucking Company, showing the additions, retirements, depreciation, and other data affecting the income of the company in the 4-year period 2016 to 2019, inclusive. The following data were in the Trucks account as of January 1, 2016: The Accumulated DepreciationTrucks account, previously adjusted to January 1,2016, and duly entered in the ledger, had a balance on that date of 16,460. This amount represented the straight-line depreciation on the four trucks from the respective dates of purchase, based on a 5-year life and no residual value. No debits had been made to this account prior to January 1, 2016. Transactions between January 1,2017, and December 31, 2019, and their record in the ledger were as follows: 1. July 1, 2016: Truck no. 1 was sold for 1,000 cash. The entry was a debit to Cash and a credit to Trucks, 1,000. 2. January 1, 2017: Truck no. 3 was traded for a larger one (no. 5) with a 5-year life. The agreed purchase price was 12,000. Jarrett paid the other company 1,780 cash on the transaction. The entry was a debit to Trucks, 1,780, and a credit to Cash, 1,780. 3. July 1, 2018: Truck no. 4 was damaged in a wreck to such an extent that it was sold as junk for 50 cash. Jarrett received 950 from the insurance company. The entry made by the bookkeeper was a debit to Cash, 1,000, and credits to Miscellaneous Revenue, 50, and Trucks, 950, 4. July 1, 2018: A new truck (no. 6) was acquired for 20,000 cash and debited at that amount to the Trucks account. The truck has a 5-year life. Entries for depreciation had been made at the close of each year as follows: 2016, 8,840; 2017, 5,436; 2018, 4,896; 2019, 4,356. Required: 1. Next Level For each of the 4 years, calculate separately the increase or decrease in earnings arising from the companys errors in determining or entering depreciation or in recording transactions affecting trucks. 2. Prove your work by one compound journal entry as of December 31, 2019; the adjustment of the Trucks account is to reflect the correct balances, assuming that the books have not been closed for 2019.arrow_forwardKoolman Construction Company began work on a contract in 2019. The contract price is 3,000,000, and the company determined that its performance obligation was satisfied over time. Other information relating to the contract is as follows: Required: 1. Compute the gross profit or loss recognized in 2019 and 2020. 2. Prepare the appropriate sections of the income statement and ending balance sheet for each year.arrow_forwardVaughn Corporation owns machinery that cost $26,000 when purchased on July 1, 2021. Depreciation has been recorded at a rate of $3,120 per year, resulting in a balance in accumulated depreciation of $10,920 at December 31, 2025. The machinery is sold on September 1, 2026, for $6,760. Prepare journal entries to (a) update depreciation for 2026 and (b) record the sale. (Credit account titles are automatically indented when amount is entered. Do not indent manually. If no entry is required, select "No Entry" for the account titles and enter O for the amounts. List all debit entries before credit entries.) No. Account Titles and Explanation (a) (b) Debit Creditarrow_forward

- Astro Company sold equipment on July 1, 2021 for $75,000. The equipment had cost $210,000 and had $120,000 of accumulated depreciation as of January 1, 2021. The equipment is being annually depreciated at an amount of $24,000. Required: Prepare the necessary journal entries to: A. Update the depreciation for the equipment. B. Record the sale of the equipment.arrow_forwardMarigold Company owns equipment that cost $79,000 when purchased on January 1, 2019. It has been depreciated using the straight-line method based on an estimated salvage value of $7,900 and an estimated useful life of 5 years. Depreciation expense adjustments are recognized annually. Instructions: Prepare Marigold Company's journal entries to record the sale of the equipment in these four independent situations. Update depreciation on assets disposed of at time of sale. (Credit account titles are automatically indented when the amount is entered. Do not indent manually. List all debit entries before credit entries. If no entry is required, select "No Entry" for the account titles and enter o for the amounts.) (a) (b) (c) (d) (e) (A) SR. Account Titles and Explanation (a) (b) Sold for $45,000 on January 1, 2022. Sold for $45,000 on April 1, 2022. Sold for $17,000 on January 1, 2022. Sold for $17,000 on September 1, 2022 Repeat (a), assuming Marigold uses double-declining balance…arrow_forwardMBS Inc. acquires a building on February 1, 2019 at a cost of P5,500,000. The building has an estimated useful life of 40 years and an estimated salvage value of P500,000. a. Prepare the following: i. journal entry to record the purchase of building. ii. Adjusting entry on December 31 assuming the company prepares its financial statements on this date. b. Determine the following (show solution): i. amount of expense to be recognized for 2019 ii. book value of the building as of December 31, 2019.arrow_forward

- MBS Inc. acquires a building on February 1, 2019 at a cost of P5,500,000. The building has an estimated useful life of 40 years and an estimated salvage value of P500,000. Required: a. Prepare the following: i. journal entry to record the purchase of building. ii. Adjusting entry on December 31 assuming the company prepares its financial statements on this date. b. Determine the following (show solution): i. amount of expense to be recognized for 2019 ii. book value of the building as of December 31, 2019.arrow_forwardAccounting Prepare all necessary journal entries for 2020, 2021, and 2022 related to each of the following scenarics: Astrom Ltd. purchased a piece of equipment on January 1, 2020, for $49.200. At the time, management determined that the equipment would have a 4-year useful life and a residual value of $4,800. Astrom uses the straight-line depreciation method for its equipment, and the company has a December 31 year end. (Credit account titles are automatically indented when the amount is entered. Do not indent manually. If no entry is required, select "No Entry" for the account titles and enter 0 for the amounts. Date Account Titles and Explanation Debit Credit Astrom Ltd. purchased a piece of equipment on January 1, 2020, for $49,200. At the time, management determined that the equipment would have a 4-year useful life and a residual value of $4,800. Astrom uses the double-diminishing-balance depreciation method for its equipment, and the company has a December 31 year end. (Credit…arrow_forwardmark Inc. purchased a machinery on January 1, 2020, at a cost of P1,250,000. It is being depreciated using the straight-line method over its projected useful life of 8 years. On December 31, 2021, the asset’s fair value was P1,125,000. Accordingly, an entry was made on that date to recognize the revaluation surplus. Revaluation is recorded maintaining the proportionate relationship between the asset account and accumulated depreciation. It is the company policy to transfer a portion of revaluation surplus to retained earnings every period. What is the amount of revaluation surplus reported in equity on December 31, 2022?arrow_forward

- Cake, Inc. purchased a machinery on January 1, 2020, at a cost of P1,250,000. It is being depreciated using the straight-line method over its projected useful life of 8 years. On December 31, 2021, the asset's fair value was P1,125,000. Accordingly, an entry was made on that date to recognize the revaluation surplus. Revaluation is recorded maintaining the proportionate relationship between the asset account and accumulated depreciation. It is the company policy to transfer a portion of revaluation surplus to retained earnings every period. What is the amount of revaluation surplus reported in equity on December 31, 2022?*arrow_forwardOn January 4, 2019, Columbus Company purchased new equipment for $693,000 that had a useful life of four years and a salvage value of $53,000. Required: Prepare a schedule showing the annual depreciation and end-of-year accumulated depreciation for the first three years of the asset's life under the straight-line method, the sum-of-the-years'-digits method, and the double-declining-balance method. Analyze: If the double-declining balance method is used to compute depreciation, what would be the book value of the asset at the end of 2020? Complete this question by entering your answers in the tabs below. Straight Line Sum of Year Digits Year 2019 2020 2021 Double Declining Prepare a schedule showing the annual depreciation and end-of-year accumulated depreciation for the first three years of the asset's life under the straight-line method. Acquisition Cost Analyze STRAIGHT-LINE METHOD Salvage Value Useful Life years years years Annual Depreciation Accumulated Depreciationarrow_forwardWildhorse Company owns equipment that cost $121,000 when purchased on January 1, 2019. It has been depreciated using the straight-line method based on an estimated salvage value of $12,100 and an estimated useful life of 5 years. Depreciation expense adjustments are recognized annually. Instructions: Prepare Wildhorse Company's journal entries to record the sale of the equipment in these four independent situations. Update depreciation on assets disposed of at time of sale. (Credit account titles are automatically indented when the amount is entered. Do not indent manually. List all debit entries before credit entries. If no entry is required, select "No Entry" for the account titles and enter O for the amounts.) (a) Sold for $73,000 on January 1, 2022. (b) Sold for $73,000 on April 1, 2022. (c) Sold for $25,500 on January 1, 2022. (d) Sold for $25,500 on September 1, 2022. (e) Repeat (a), assuming Wildhorse uses double-declining balance depreciation. (f) Repeat (c), assuming Wildhorse…arrow_forward

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning