Concept explainers

Videos

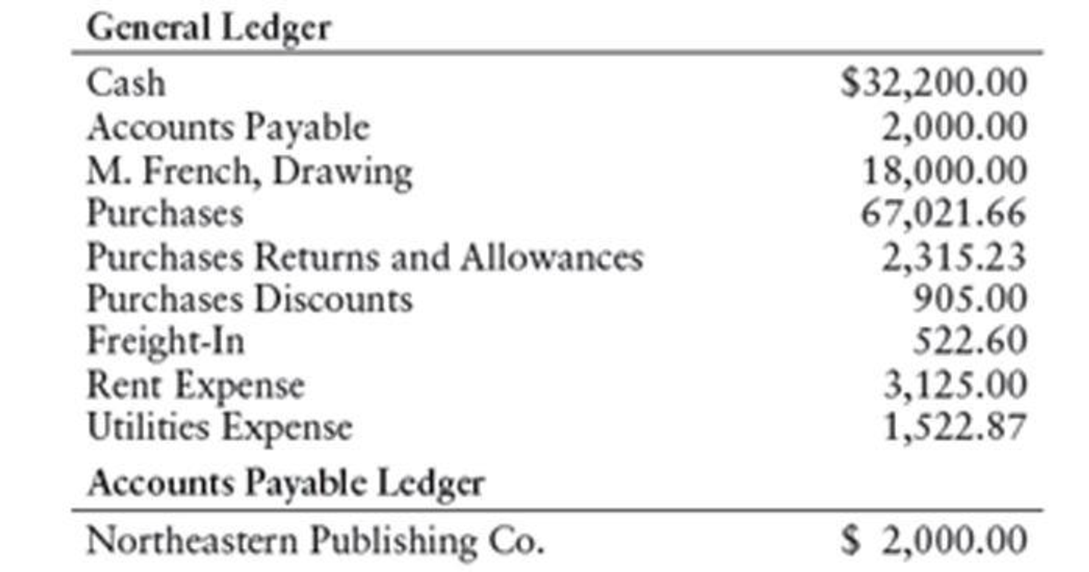

Michelle French owns and operates Books and More, a retail book store. Selected account balances on June 1 are as follows:

The following purchases and cash payments transactions took place during the month of June:

June 1 Purchased books on account from Irving Publishing Company, $2,100. Invoice No. 101, terms 2/10, n/30, FOB destination.

2 Issued Cheek No. 300 to Northeastern Publishing Co. for goods purchased on May 23, terms 2/10, n/30, $1,960 (the $2,000 invoice amount less the 2% discount).

3 Purchased books on account from Broadway Publishing, Inc., $2,880. Invoice No. 711, less a 20% trade discount, and invoice terms of 3/10, n/30, FOB shipping point.

3 Issued Cheek No. 301 to Mayday Shipping for delivery from Broadway Publishing, Inc., $250.

4 Issued Cheek No. 302 for June rent, $625.

8 Purchased books on account from Northeastern Publishing Co., $5,825. Invoice No. 268, terms 2/com, n/60, FOB destination.

10 Received a credit memo from Irving Publishing Company, $550. Books had been returned because the covers were on upside down.

13 Issued Check No. 304 to Broadway Publishing, Inc., for the purchase made on June 3. (Check No. 303 was voided because an error was made in preparing it.)

28 Made the following purchases:

30 Issued Cheek No. 305 to Taylor County Utility Co. for June utilities, $325.

30 French withdrew cash for personal use, $4,500. Issued Check No. 306.

30 Issued Cheek No. 307 to Irving Publishing Company for purchase made on June 1 less returns made on June 10.

30 Issued Check No. 308 to Northeastern Publishing Co. for purchase made on June 8.

30 Issued Check No. 309 for books purchased at an auction, $1,328.

REQUIRED

- 1. Enter the transactions in a general journal (start with page 16).

- 2. Post from the journal to the general ledger accounts and the accounts payable ledger. Use general ledger account numbers as indicated in the chapter.

- 3. Prepare a schedule of accounts payable.

- 4. If merchandise inventory was $35,523 on January 1 and $42,100 as of June 30, prepare the cost of goods sold section of the income statement for the six months ended June 30,20--.

1.

Journalize the purchases and cash payment transactions for the month of June.

Explanation of Solution

Journal entry: Journal entry is a set of economic events which can be measured in monetary terms. These are recorded chronologically and systematically.

Debit and credit rules:

- ■ Debit an increase in asset account, increase in expense account, decrease in liability account, and decrease in stockholders’ equity accounts.

- ■ Credit decrease in asset account, increase in revenue account, increase in liability account, and increase in stockholders’ equity accounts.

Journalize the purchases and cash payment transactions for the month of June.

Transaction on June 1:

| Page: 16 | ||||||

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| June | 1 | Purchases | 501 | 2,100 | ||

| Accounts Payable, Company IP | 202/✓ | 2,100 | ||||

| (Record purchases made on account) | ||||||

Table (1)

Description:

- ■ Purchases is an expense account which records the cost of inventory purchased. An increase in expense reduces the equity value, and a decrease in equity is debited.

- ■ Accounts Payable, Company IP is a liability account. Since the payable increased, the liability increased, and an increase in liability is credited.

Transaction on June 2:

| Page: 16 | ||||||

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | ||

| June | 2 | Accounts Payable, Corporation NP | 202/✓ | 2,000 | ||

| Cash | 101 | 1,960 | ||||

| Purchases Discounts | 501.2 | 40 | ||||

| (Record cash paid for purchases on account) | ||||||

Table (2)

Description:

- ■ Accounts Payable, Corporation NP is a liability account. Since the payable decreased, the liability decreased, and a decrease in liability is debited.

- ■ Cash is an asset account. Since cash is paid, asset account decreased, and a decrease in asset is credited.

- ■ Purchases Discounts is a contra-purchases or contra-costs account, and contra-purchases accounts increase the equity value, and an increase in equity is credited.

Working Note 1:

Compute purchases discount value.

Working Note 2:

Compute amount of cash paid (Refer to Working Note 2 for purchase discount value).

Transaction on June 3:

| Page: 16 | ||||||

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| June | 3 | Purchases | 501 | 2,304 | ||

| Accounts Payable, Incorporation BP | 202/✓ | 2,304 | ||||

| (Record purchases made on account) | ||||||

Table (3)

Description:

- ■ Purchases is an expense account which records the cost of inventory purchased. An increase in expense reduces the equity value, and a decrease in equity is debited.

- ■ Accounts Payable, Incorporation BP is a liability account. Since the payable increased, the liability increased, and an increase in liability is credited.

Working Note 3:

Compute the purchase invoice value.

Transaction on June 3:

| Page: 16 | ||||||

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| June | 3 | Freight-In | 502 | 250 | ||

| Cash | 101 | 250 | ||||

| (Record payment of freight charges) | ||||||

Table (4)

Description:

- ■ Freight-In is an expense account. An increase in expense reduces the equity value, and a decrease in equity is debited.

- ■ Cash is an asset account. Since cash is paid, asset account decreased, and a decrease in asset is credited.

Transaction on June 4:

| Page: 16 | ||||||

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| June | 4 | Rent Expense | 521 | 625 | ||

| Cash | 101 | 625 | ||||

| (Record payment of rent expense) | ||||||

Table (5)

Description:

- ■ Rent Expense is an expense account. An increase in expense reduces the equity value, and a decrease in equity is debited.

- ■ Cash is an asset account. Since cash is paid, asset account decreased, and a decrease in asset is credited.

Transaction on June 8:

| Page: 16 | ||||||

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| June | 8 | Purchases | 501 | 5,825 | ||

| Accounts Payable, Corporation NP | 202/✓ | 5,825 | ||||

| (Record purchases made on account) | ||||||

Table (6)

Description:

- ■ Purchases is an expense account which records the cost of inventory purchased. An increase in expense reduces the equity value, and a decrease in equity is debited.

- ■ Accounts Payable, Corporation NP is a liability account. Since the payable increased, the liability increased, and an increase in liability is credited.

Transaction on June 10:

| Page: 16 | ||||||

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| June | 10 | Accounts Payable, Company IP | 202/✓ | 550 | ||

| Purchases Returns and Allowances | 501.1 | 550 | ||||

| (Record merchandise returned) | ||||||

Table (7)

Description:

- ■ Accounts Payable, Company IP is a liability account. Since inventory is returned, amount to be paid has decreased, liability account is decreased, and a decrease in liability is debited.

- ■ Purchases Returns and Allowances is a contra-cost account, and contra-cost accounts increase the equity value, and an increase in equity is credited.

Transaction on June 13:

| Page: 16 | ||||||

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | ||

| June | 13 | Accounts Payable, Incorporation BP | 202/✓ | 2,304.00 | ||

| Cash | 101 | 2,234.88 | ||||

| Purchases Discounts | 501.2 | 69.12 | ||||

| (Record cash paid for purchases on account) | ||||||

Table (8)

Description:

- ■ Accounts Payable, Incorporation BP is a liability account. Since the payable decreased, the liability decreased, and a decrease in liability is debited.

- ■ Cash is an asset account. Since cash is paid, asset account decreased, and a decrease in asset is credited.

- ■ Purchases Discounts is a contra-purchases or contra-costs account, and contra-purchases accounts increase the equity value, and an increase in equity is credited.

Working Note 4:

Compute purchases discount value (Refer to Working Note 3 for value of purchases).

Working Note 5:

Compute amount of cash paid (Refer to Working Note 4 for purchase discount value).

Transaction on June 28:

| Page: 16 | ||||||

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| June | 28 | Purchases | 501 | 2,350 | ||

| Accounts Payable, Incorporation BP | 202/✓ | 2,350 | ||||

| (Record purchases made on account) | ||||||

Table (9)

Description:

- ■ Purchases is an expense account which records the cost of inventory purchased. An increase in expense reduces the equity value, and a decrease in equity is debited.

- ■ Accounts Payable, Incorporation BP is a liability account. Since the payable increased, the liability increased, and an increase in liability is credited.

Transaction on June 28:

| Page: 16 | ||||||

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| June | 28 | Purchases | 501 | 4,200 | ||

| Accounts Payable, Corporation NP | 202/✓ | 4,200 | ||||

| (Record purchases made on account) | ||||||

Table (10)

Description:

- ■ Purchases is an expense account which records the cost of inventory purchased. An increase in expense reduces the equity value, and a decrease in equity is debited.

- ■ Accounts Payable, Corporation NP is a liability account. Since the payable increased, the liability increased, and an increase in liability is credited.

Transaction on June 28:

| Page: 16 | ||||||

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| June | 28 | Purchases | 501 | 3,450 | ||

| Accounts Payable, Corporation RP | 202/✓ | 3,450 | ||||

| (Record purchases made on account) | ||||||

Table (11)

Description:

- ■ Purchases is an expense account which records the cost of inventory purchased. An increase in expense reduces the equity value, and a decrease in equity is debited.

- ■ Accounts Payable, Corporation RP is a liability account. Since the payable increased, the liability increased, and an increase in liability is credited.

Transaction on June 30:

| Page: 16 | ||||||

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| June | 30 | Utilities Expense | 533 | 325 | ||

| Cash | 101 | 325 | ||||

| (Record payment of utilities expense) | ||||||

Table (12)

Description:

- ■ Utilities Expense is an expense account. An increase in expense reduces the equity value, and a decrease in equity is debited.

- ■ Cash is an asset account. Since cash is paid, asset account decreased, and a decrease in asset is credited.

Transaction on June 30:

| Page: 16 | ||||||

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| June | 30 | F, Drawing | 533 | 4,500 | ||

| Cash | 101 | 4,500 | ||||

| (Record withdrawal for personal use) | ||||||

Table (13)

Description:

- ■ F, Drawings is a contra-capital account. Contra-capital accounts have a normal debit balance, hence the account is debited.

- ■ Cash is an asset account. Since cash is paid, asset account decreased, and a decrease in asset is credited.

Transaction on June 30:

| Page: 16 | ||||||

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | ||

| June | 30 | Accounts Payable, Company IP | 202/✓ | 1,550 | ||

| Cash | 101 | 1,550 | ||||

| (Record cash paid for purchases on account) | ||||||

Table (14)

Description:

- ■ Accounts Payable, Company IP is a liability account. Since the payable decreased, the liability decreased, and a decrease in liability is debited.

- ■ Cash is an asset account. Since cash is paid, asset account decreased, and a decrease in asset is credited.

Working Note 6:

Compute amount of cash paid.

Transaction on June 30:

| Page: 16 | ||||||

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | ||

| June | 30 | Accounts Payable, Corporation NP | 202/✓ | 5,825.00 | ||

| Cash | 101 | 5,708.50 | ||||

| Purchases Discounts | 501.2 | 116.50 | ||||

| (Record cash paid for purchases on account) | ||||||

Table (15)

Description:

- ■ Accounts Payable, Corporation NP is a liability account. Since the payable decreased, the liability decreased, and a decrease in liability is debited.

- ■ Cash is an asset account. Since cash is paid, asset account decreased, and a decrease in asset is credited.

- ■ Purchases Discounts is a contra-purchases or contra-costs account, and contra-purchases accounts increase the equity value, and an increase in equity is credited.

Working Note 7:

Compute purchases discount value.

Working Note 8:

Compute amount of cash paid (Refer to Working Note 7 for purchase discount value).

Transaction on June 30:

| Page: 16 | ||||||

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| June | 30 | Purchases | 501 | 1,328 | ||

| Cash | 101 | 1,328 | ||||

| (Record purchase of inventory) | ||||||

Table (16)

Description:

- ■ Purchases is an expense account which records the cost of inventory purchased. An increase in expense reduces the equity value, and a decrease in equity is debited.

- ■ Cash is an asset account. Since cash is paid, asset account decreased, and a decrease in asset is credited.

2.

Post the given transactions into the accounts of the general ledger, and the suppliers account in accounts payable ledger.

Explanation of Solution

Posting transactions: The process of transferring the journalized transactions into the accounts of the ledger is known as posting the transactions.

Post the given transactions into the accounts of the general ledger.

| ACCOUNT Cash ACCOUNT NO. 101 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| June | 1 | Balance | ✓ | 32,200.00 | |||

| 2 | J16 | 1,960.00 | 30,240.00 | ||||

| 3 | J16 | 250.00 | 29,990.00 | ||||

| 4 | J16 | 625.00 | 29,365.00 | ||||

| 13 | J16 | 2,234.88 | 27,130.12 | ||||

| 30 | J16 | 325.00 | 26,805.12 | ||||

| 30 | J16 | 4,500.00 | 22,305.12 | ||||

| 30 | J16 | 1,550.00 | 20,755.12 | ||||

| 30 | J16 | 5708.50 | 15,046.62 | ||||

| 30 | J16 | 1,328.00 | 13,718.62 | ||||

Table (17)

| ACCOUNT Accounts Payable ACCOUNT NO. 202 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| June | 1 | Balance | ✓ | 2,000 | |||

| 1 | J16 | 2,100 | 4,100 | ||||

| 2 | J16 | 2,000 | 2,100 | ||||

| 3 | J16 | 2,304 | 4,404 | ||||

| 8 | J16 | 5,825 | 10,229 | ||||

| 10 | J16 | 550 | 9,679 | ||||

| 13 | J16 | 2,304 | 7,375 | ||||

| 28 | J16 | 2,350 | 9,725 | ||||

| 28 | J16 | 4,200 | 13,925 | ||||

| 28 | J16 | 3,450 | 17,375 | ||||

| 30 | J16 | 1,550 | 15,825 | ||||

| 30 | J16 | 5,825 | 10,000 | ||||

Table (18)

| ACCOUNT Purchases ACCOUNT NO. 501 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| June | 1 | Balance | ✓ | 67,021.66 | |||

| 1 | J16 | 2,100.00 | 69,121.66 | ||||

| 3 | J16 | 2,304.00 | 71,425.66 | ||||

| 8 | J16 | 5,825.00 | 77,250.66 | ||||

| 28 | J16 | 2,350.00 | 79,600.66 | ||||

| 28 | J16 | 4,200.00 | 83,800.66 | ||||

| 28 | J16 | 3,450.00 | 87,250.66 | ||||

| 30 | J16 | 1,328.00 | 88,578.66 | ||||

Table (19)

| ACCOUNT Purchases Returns and Allowances ACCOUNT NO. 501.1 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| June | 1 | Balance | ✓ | 2,315.23 | |||

| 10 | J16 | 550.00 | 2,865.23 | ||||

Table (20)

| ACCOUNT Purchases Discounts ACCOUNT NO. 501.2 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| June | 1 | Balance | ✓ | 905.00 | |||

| 2 | J16 | 40.00 | 945.0 | ||||

| 13 | J16 | 69.12 | 1,014.12 | ||||

| 30 | J16 | 116.50 | 1,130.62 | ||||

Table (21)

| ACCOUNT Freight-In ACCOUNT NO. 502 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| June | 1 | Balance | ✓ | 522.60 | |||

| 3 | J16 | 250.00 | 772.60 | ||||

Table (22)

| ACCOUNT Rent Expense ACCOUNT NO. 521 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| June | 1 | Balance | ✓ | 3,125.00 | |||

| 4 | J16 | 625.00 | 3,750.00 | ||||

Table (23)

| ACCOUNT Utilities Expense ACCOUNT NO. 533 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| June | 1 | Balance | ✓ | 1,522.87 | |||

| J16 | 325.00 | 1,847.87 | |||||

Table (24)

| ACCOUNT F, Drawings ACCOUNT NO. 312 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| June | 1 | Balance | ✓ | 18,000 | |||

| J16 | 4,500 | 22,500 | |||||

Table (25)

Post the accounts payable balances of the suppliers to the supplier accounts in the accounts payable ledger.

| NAME Incorporation BP | ||||||

| ADDRESS | ||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance ($) | |

| June | 3 | J16 | 2,304 | 2,304 | ||

| 13 | J16 | 2,304 | 0 | |||

| 28 | J16 | 2,350 | 2,350 | |||

Table (26)

| NAME Company IP | ||||||

| ADDRESS | ||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance ($) | |

| June | 1 | J16 | 2,100 | 2,100 | ||

| 10 | J16 | 550 | 1,550 | |||

| 30 | J16 | 1,550 | 0 | |||

Table (27)

| NAME Corporation NP | ||||||

| ADDRESS | ||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance ($) | |

| June | 1 | Balance | ✓ | 2,000 | ||

| 2 | J16 | 2,000 | 0 | |||

| 8 | J16 | 5,825 | 5,825 | |||

| 28 | J16 | 4,200 | 10,025 | |||

| 30 | J16 | 5,825 | 4,200 | |||

Table (28)

| NAME Corporation RP | ||||||

| ADDRESS | ||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance ($) | |

| June | 28 | J16 | 3,450 | 3,450 | ||

Table (29)

3.

Prepare accounts payable schedule for Company BM as at June 30.

Explanation of Solution

Schedule of accounts payable: This is the schedule which is prepared to verify that the total balances of all the suppliers in the accounts payable ledger, equals the balance of Accounts Payable in the general ledger.

Prepare accounts payable schedule for Company BM as at June 30 (Refer to Requirement (2) for all the values and computations of the balances of the customers).

| Company BM | |

| Schedule of Accounts Payable | |

| June 30 | |

| Incorporation BP | $2,350 |

| Corporation NP | 4,200 |

| Corporation RP | 3,450 |

| Total | $10,000 |

Table (30)

Thus, the schedule of accounts payable of Company BM shows a balance of $10,000, as of June 30.

4.

Prepare the cost of goods sold section of income statement for Company BM.

Explanation of Solution

Cost of goods sold: Cost of goods sold is the total of all the expenses incurred by a company to sell the goods during the given period.

Formula to compute cost of goods sold:

| Details | Amount ($) | Amount ($) | Amount ($) |

| Merchandise inventory, January 1 | $XXX | ||

| Purchases | $XXX | ||

| Less: Purchase returns and allowances | $XXX | ||

| Less: Purchases discounts | XXX | XXX | |

| Net purchases | XXX | ||

| Add: Freight-in | XXX | ||

| Cost of goods purchased | XXX | ||

| Goods available for sale | XXX | ||

| Less: Merchandise inventory, December 31 | XXX | ||

| Cost of goods sold | $XXX |

Table (31)

Prepare the cost of goods sold section of income statement for Company BM (Refer to Requirement (2) for all the values and computations of the ledger balances).

| Details | Amount ($) | Amount ($) | Amount ($) |

| Merchandise inventory, January 1 | $35,523.00 | ||

| Purchases | $88,578.66 | ||

| Less: Purchase returns and allowances | $2,865.23 | ||

| Less: Purchases discounts | 1,130.62 | 3,995.85 | |

| Net purchases | 84,582.81 | ||

| Add: Freight-in | 772.60 | ||

| Cost of goods purchased | 85,355.41 | ||

| Goods available for sale | 120,878.41 | ||

| Less: Merchandise inventory, June 30 | 42,100.00 | ||

| Cost of goods sold | $78,778.41 |

Table (32)

Thus, the cost of goods sold of income statement for Company BM is $78,778.41.

Want to see more full solutions like this?

Chapter 11 Solutions

College Accounting, Chapters 1-9 (New in Accounting from Heintz and Parry)

- Guardian Services Inc. had the following transactions during the month of April: a. Record the June purchase transactions for Guardian Services Inc. in the following purchases journal format: b. What is the total amount posted to the accounts payable and office supplies accounts from the purchases journal for April? c. What is the April 30 balance of the Officemate Inc. creditor account assuming a zero balance on April 1?arrow_forwardHappy Tails Inc. has a September 1, 20Y4, accounts payable balance of 620, which consists of 320 due Labradore Inc. and 300 due Meow Mart Inc. Transactions related to purchases and cash payments completed by Happy Tails Inc. during the month of September 20Y4 are as follows: a. Prepare a purchases journal and a cash payments journal to record these transactions. The forms of the journals are similar to those used in the text. Place a check mark () in the Post. Ref. column to indicate when the accounts payable subsidiary ledger should be posted. Happy Tails Inc. uses the following accounts: b. Prepare a listing of accounts payable creditor balances on September 30, 20Y4. Verify that the total of the accounts payable creditor balances equals the balance of the accounts payable controlling account on September 30, 20Y4. c. Why does Happy Tails Inc. use a subsidiary ledger for accounts payable?arrow_forwardThe following transactions were completed by Nelsons Boutique, a retailer, during July. Terms of sales on account are 2/10, n/30, FOB shipping point. July 3Received cash from J. Smith in payment of June 29 invoice of 350, less cash discount. 6Issued Ck. No. 1718, 742.50, to Designer, Inc., for invoice. no. 2256, recorded previously for 750, less cash discount of 7.50. July 9Sold merchandise in the amount of 250 on a credit card. Sales tax on this sale is 6%. The credit card fee the bank deducted for this transaction is 5. 10Issued Ck. No. 1719, 764.40, to Smart Style, Inc., for invoice no. 1825, recorded previously on account for 780. A trade discount of 25% was applied at the time of purchase, and Smart Style, Inc.s credit terms are 2/10, n/30. 12Received 180 cash in payment of June 20 invoice from R. Matthews. No cash discount applied. 18Received 1,575 cash in payment of a 1,500 note receivable and interest of 75. 21Voided Ck. No. 1720 due to error. 25Received and paid utility bill, 152; Ck. No. 1721, payable to City Utilities Company. 31Paid wages recorded previously for the month, 2,586, Ck. No. 1722. Required 1. Journalize the transactions for July in the cash receipts journal, the general journal (for the transaction on July 9th), or the cash payments journal as appropriate. Assume the periodic inventory method is used. 2. If you are using Working Papers, total and rule the journals. Prove the equality of debit and credit totals.arrow_forward

- The following transactions were completed by Nelsons Hardware, a retailer, during September. Terms on sales on account are 1/10, n/30, FOB shipping point. Sept. 4Received cash from M. Alex in payment of August 25 invoice of 275, less cash discount. 7Issued Ck. No. 8175, 915.75, to Top Tools, Inc., for invoice. no. 2256, recorded previously for 925, less cash discount of 9.25. 10Sold merchandise in the amount of 175 on a credit card. Sales tax on this sale is 8%. The credit card fee the bank deducted for this transaction is 5. 11Issued Ck. No. 8176, 653.40, to Snap Tools, Inc. for invoice no. 726, recorded previously on account for 660. A trade discount of 15% was applied at the time of purchase, and Snap Tools, Inc.s credit terms are 1/10, n/45. 15Received 95 cash in payment of August 20 invoice from N. Johnson. No cash discount applied. 19Received 1,165 cash in payment of a 1,100 note receivable and interest of 65. 22Voided Ck. No. 8177 due to error. 26Received and paid telephone bill, 62; Ck. No. 8178, payable to Southern Telephone Company. 30Paid wages recorded previously for the month, 3,266, Ck. No. 8179. Required 1. Journalize the transactions for September in the cash receipts journal, the general journal (for the transaction on Sept. 10th), or the cash payments journal as appropriate. Assume the periodic inventory method is used. 2. If you are using Working Papers, total and rule the journals. Prove the equality of debit and credit totals.arrow_forwardGomez Company sells electrical supplies on a wholesale basis. The balances of the accounts as of April 1 have been recorded in the general ledger in your Working Papers and CengageNow. The following transactions took place during April of this year: Apr. 1 Sold merchandise on account to Myers Company, invoice no. 761, 570.40. 5 Sold merchandise on account to L. R. Foster Company, invoice no. 762, 486.10. 6 Issued credit memo no. 50 to Myers Company for merchandise returned, 40.70. 10 Sold merchandise on account to Diaz Hardware, invoice no. 763, 293.35. 14 Sold merchandise on account to Brooks and Bennett, invoice no. 764, 640.16. 17 Sold merchandise on account to Powell and Reyes, invoice no. 765, 582.12. 21 Issued credit memo no. 51 to Brooks and Bennett for merchandise returned, 68.44. 24 Sold merchandise on account to Ortiz Company, invoice no. 766, 652.87. 26 Sold merchandise on account to Diaz Hardware, invoice no. 767, 832.19. 30 Issued credit memo no. 52 to Diaz Hardware for damage to merchandise, 98.50. Required 1. Record these sales of merchandise on account in the sales journal. If using Working Papers, use page 39. Record the sales returns and allowances in the general journal. If using Working Papers, use page 74. 2. Immediately after recording each transaction, post to the accounts receivable ledger. 3. Post the amounts from the general journal daily. Post the sales journal amount as a total at the end of the month: Accounts Receivable 113, Sales 411, Sales Returns and Allowances 412. 4. Prepare a schedule of accounts receivable. Compare the balance of the Accounts Receivable controlling account with the total of the schedule of accounts receivable.arrow_forwardReview the following transactions and prepare any necessary journal entries for Tolbert Enterprises. A. On April 7, Tolbert Enterprises contracts with a supplier to purchase 300 water bottles for their merchandise inventory, on credit, for $10 each. Credit terms are 2/10, n/60 from the invoice date of April 7. B. On April 15, Tolbert pays the amount due in cash to the supplier.arrow_forward

- SALES TRANSACTIONS J. K. Bijan owns a retail business and made the following sales on account during the month of August 20--. There is a 6% sales tax on all sales. REQUIRED 1. Record the transactions starting on page 15 of a general journal. 2. Post from the journal to the general ledger and accounts receivable ledger accounts. Use account numbers as shown in the chapter.arrow_forwardOn March 24, MS Companys Accounts Receivable consisted of the following customer balances: S. Burton 310 A. Tangier 240 J. Holmes 504 F. Fullman 110 P. Molty 90 During the following week, MS made a sale of 104 to Molty and collected cash on account of 207 from Burton and 360 from Holmes. Prepare a schedule of accounts receivable for MS at March 31, 20--.arrow_forwardSALES TRANSACTIONS T. M. Maxwell owns a retail business and made the following sales on account during the month of July 20--. There is a 5% sales tax on all sales. REQUIRED 1. Record the transactions starting on page 15 of a general journal. 2. Post from the journal to the general ledger and accounts receivable ledger accounts. Use account numbers as shown in the chapter.arrow_forward

- Aviles Corporation engaged in the following transactions during June. DATE. TRANSACTIONS June 4, 20X1. Purchased merchandise on account from Eliassen Company; Invoice 100 for 1,145; terms n/30. June 15,20X1. Recorded purchases for cash, 1,630. June 30, 20X1. Paid amount due to Eliassen Company for the purchase on June 4. Required: Record these transactions in a general journal. View transaction list Journal entry worksheet < 1 2 Date June 04, 20X1 Note: Enter debits before credits. 3 Purchased merchandise on account from Eliassen Company; Invoice 100 for $1,145; terms n/30. Record entry Show Transcribed Text 3 General Journal Clear entry c Date. General Journal. Debit. Credit June 04, 20X1 Debit Credit View general journal Journal entry worksheet Purchased merchandise on account from Eliassen Company; Invoice 100 for 1,145; terms n/30arrow_forwardGomez Company sells electrical supplies on a wholesale basis. The balances of the accounts as of April 1 have been recorded in the general ledger in your working papers and CengageNow. The following transactions took place during April of this year: Apr. 1 Sold merchandise on account to Myers Company, invoice no. 761, $570.40. Apr. 5 Sold merchandise on account to L.R. Foster, invoice no. 762, $486.10. Apr. 6 Issued credit memo no. 50 to Myers Company for merchandise returned, $40.70. Apr. 10 Sold merchandise on account to Diaz Hardware, invoice no. 763, $293,35. Apr. 14 Sold merchandise on account to Brooks and Bennett, invoice no. 764, $640.16. Apr. 17 Sold merchandise on account to Powell and Reyes, invoice no. 765, $582.12. Apr. 21 Issued credit memo no. 51 to Brooks and Bennett for merchandise returned, $68.44. Apr. 24 Sold merchandise on account to Ortiz Company, invoice no. 766, $652.87. Apr. 26 Sold merchandise on account to Diaz Hardware, invoice no. 767, $832.19. Apr. 30…arrow_forwardPurchases and Cash Payments Journals Transactions related to purchases and cash payments completed by Wisk Away Cleaning Services Inc. during the month of May 20Y5 are as follows: May 1. Issued Check No. 57 to Bio Safe Supplies Inc. in payment of account, $360. 3. Purchased cleaning supplies on account from Brite N' Shine Products Inc., $220. 8. Issued Check No. 58 to purchase equipment from Carson Equipment Sales, $3,680. 12. Purchased cleaning supplies on account from Porter Products Inc., $310. 15. Issued Check No. 59 to Bowman Electrical Service in payment of account, $180. 18. Purchased supplies on account from Bio Safe Supplies Inc., $410. 20. Purchased electrical repair services from Bowman Electrical Service on account, $150. 26. Issued Check No. 60 to Brite N’ Shine Products Inc. in payment of May 3 invoice. 31. Issued Check No. 61 in payment of salaries, $7,050. Wisk Away Cleaning Services Inc. uses the following accounts: Cash 11…arrow_forward

College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub

College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,