Videos

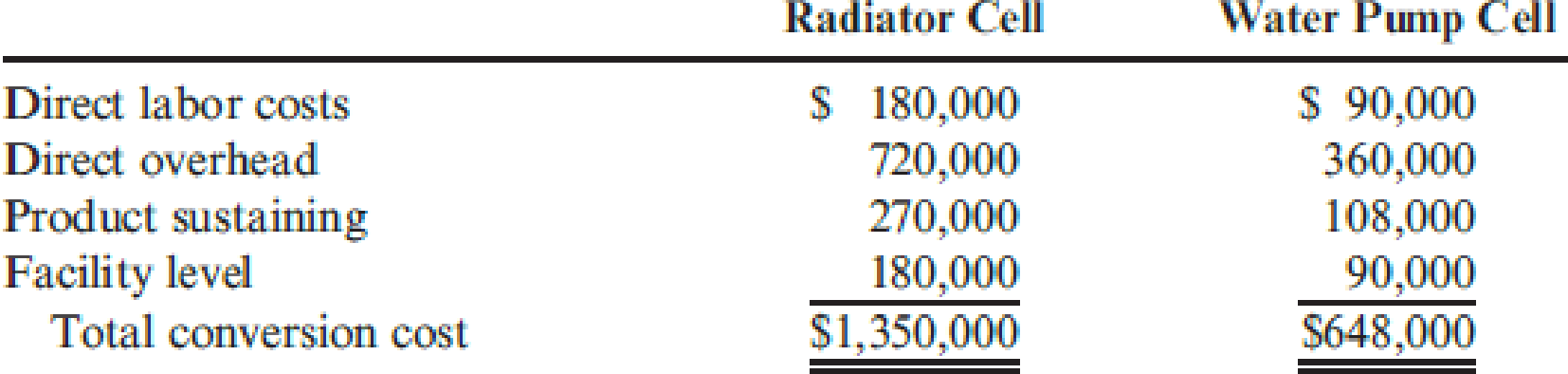

Southward Company has implemented a JIT flexible manufacturing system. John Richins, controller of the company, has decided to reduce the accounting requirements given the expectation of lower inventories. For one thing, he has decided to treat direct labor cost as a part of overhead and to discontinue the detailed direct labor accounting of the past. The company has created two manufacturing cells, each capable of producing a family of products: the radiator cell and the water pump cell. The output of both cells is sold to a sister division and to customers who use the radiators and water pumps for repair activity. Product-level overhead costs outside the cells are assigned to each cell using appropriate drivers. Facility-level costs are allocated to each cell on the basis of square footage. The budgeted direct labor and overhead costs are as follows:

The predetermined conversion cost rate is based on available production hours in each cell. The radiator cell has 45,000 hours available for production, and the water pump cell has 27,000 hours. Conversion costs are applied to the units produced by multiplying the conversion rate by the actual time required to produce the units. The radiator cell produced 81,000 units, taking 0.5 hour to produce one unit of product (on average). The water pump cell produced 90,000 units, taking 0.25 hour to produce one unit of product (on average).

Other actual results for the year are as follows:

All units produced were sold. Any conversion cost variance is closed to Cost of Goods Sold.

Required:

- 1. Calculate the predetermined conversion cost rates for each cell.

- 2. Prepare

journal entries using backflush accounting. Assume two trigger points, with completion of goods as the second trigger point. - 3. Repeat Requirement 2, assuming that the second trigger point is the sale of the goods.

- 4. Explain why there is no need to have a work-in-process inventory account.

- 5. Two variants of backflush costing were presented in which each used two trigger points, with the second trigger point differing. Suppose that the only trigger point for recognizing

manufacturing costs occurs when the goods are sold. How would the entries be listed here? When would this backflush variant be considered appropriate?

Want to see the full answer?

Check out a sample textbook solution

Chapter 11 Solutions

EBK CORNERSTONES OF COST MANAGEMENT

- Larsen, Inc., produces two types of electronic parts and has provided the following data: There are four activities: machining, setting up, testing, and purchasing. Required: 1. Calculate the activity consumption ratios for each product. 2. Calculate the consumption ratios for the plantwide rate (direct labor hours). When compared with the activity ratios, what can you say about the relative accuracy of a plantwide rate? Which product is undercosted? 3. What if the machine hours were used for the plantwide rate? Would this remove the cost distortion of a plantwide rate?arrow_forwardArklan Production is upgrading its manufacturing process from a manual process to a highly automated system. Management believes that the new system will result in greater efficiencies and a better finished product. Arklan is also working on a plan to downsize staff after the implementation of the new system. Arklan has used a traditional absorption costing system to calculate unit product costs for external financial reporting. In the past, Arklan has allocated its manufacturing overhead costs using a predetermined plant-wide overhead rate based on direct labor hours. The controller realizes that the new system may require changing the overhead allocation process. Management plans to take the opportunity to reconsider other improvements to the costing system. Identify and explain three benefits of using departmental overhead rates to allocate overhead costs. Explain the difference between absorption costing and variable costing. Identify which is more suitable for internal…arrow_forwardAsbury Coffee Enterprises (ACE) manufactures two models of coffee grinders: Personal and Commercial. The Personal grinders have a smaller capacity and are less durable than the Commercial grinders. ACE only recently began producing the Commercial model. Since the introduction of the new product, profits have been steadily declining, although sales have been increasing. The management at ACE believes that the problem might be in how the accounting system allocates costs to products. The current system at ACE allocates manufacturing overhead to products based on direct labor costs. For the most recent year, which is representative, manufacturing overhead totaled $2,037,000 based on production of 30,000 Personal grinders and 10,000 Commercial grinders. Direct costs were as follows: Personal Commercial Total Direct materials $ 1,445,000 $ 620,000 $ 2,065,000 Direct labor 1,030,000 667,500 1,697,500 Management has determined that overhead costs are caused by three cost…arrow_forward

- Asbury Coffee Enterprises (ACE) manufactures two models of coffee grinders: Personal and Commercial. The Personal grinders have a smaller capacity and are less durable than the Commercial grinders. ACE only recently began producing the Commercial model. Since the introduction of the new product, profits have been steadily declining, although sales have been increasing. The management at ACE believes that the problem might be in how the accounting system allocates costs to products. The current system at ACE allocates manufacturing overhead to products based on direct labor costs. For the most recent year, which is representative, manufacturing overhead totaled $2,023,500 based on production of 30,000 Personal grinders and 10,000 Commercial grinders. Direct costs were as follows: Personal Commercial Total Direct materials $ 1,444,200 $ 609,750 $ 2,053,950 Direct labor 1,029,000 657,250 1,686,250 Management has determined that overhead costs are caused by three cost…arrow_forwardAsbury Coffee Enterprises (ACE) manufactures two models of coffee grinders: Personal and Commercial. The Personal grinders have a smaller capacity and are less durable than the Commercial grinders. ACE only recently began producing the Commercial model. Since the introduction of the new product, profits have been steadily declining, although sales have been increasing. The management at ACE believes that the problem might be in how the accounting system allocates costs to products. The current system at ACE allocates manufacturing overhead to products based on direct labor costs. For the most recent year, which is representative, manufacturing overhead totaled $1,902,000 based on production of 30,000 Personal grinders and 10,000 Commercial grinders. Direct costs were as follows: Direct materials Direct labor Personal $ 1,437,000 1,020,000 Commercial $ 517,500 565,000 Total $ 1,954,500 1,585,000 Management has determined that overhead costs are caused by three cost drivers. These…arrow_forwardAsbury Coffee Enterprises (ACE) manufactures two models of coffee grinders. Personal and Commercial. The Personal grinders have a smaller capacity and are less durable than the Commercial grinders. ACE only recently began producing the Commercial model. Since the introduction of the new product, profits have been steadily declining, although sales have been increasing. The management at ACE believes that the problem might be in how the accounting system allocates costs to products. The current system at ACE allocates manufacturing overhead to products based on direct labor costs. For the most recent year, which is representative, manufacturing overhead totaled $1,929,000 based on production of 30,000 Personal grinders and 10,000 Commercial grinders. Direct costs were as follows: Direct materials Direct labor Cost Driver Number of production runs Quality tests performed Shipping orders processed Total overhead Management has determined that overhead costs are caused by three cost…arrow_forward

- Utica Manufacturing (UM) was recently acquired by MegaMachines, Inc. (MM), and organized as a separate division within the company. Most manufacturing plants at MM use an ABC system, but UM has always used a traditional product costing system. Bob Miller, the plant controller at UM, has decided to experiment with ABC and has asked you to help develop a simple ABC system that would help him decide if it was useful. The controller’s staff has identified costs for the first month in the four overhead cost pools along with appropriate cost drivers for each pool. Cost Pools Costs Activity Drivers Incoming inspection $ 154,000 Direct material cost Production 1,430,000 Machine-hours Machine setup 792,000 Setups Shipping 484,000 Units shipped The company manufactures two basic products with model numbers 308 and 510. The following are data for production for the first month as part of MM. Products 308 510 Total direct material…arrow_forwardMozaic Inc. has decided to introduce a new product, which can be manufactured by either a computer-assisted manufacturing system (CAM) or a labor-intensive production system (LIP). The manufacturing method will not affect the quality of the product. The estimated manufacturing costs by the two methods are as follows: CAM System LIP System Direct Material $5.00 $5.60 Direct Labor (DLH) 0.5 DLH x $12 $6.00 0.8 DLH x $9 $7.20 Variable Overhead 0.5 DLH x $6 $3.00 0.8 DLH x $6 $4.80 Fixed Overhead* $2,440,000 $1,320,000 * These costs are directly traceable to the new product line. They would not be incurred if the new product were not produced. The company's marketing research department has recommended an introductory unit sales price of $30. Selling expenses are estimated to be $500,000 annually plus $2 for each unit sold. (Ignore income taxes.) Required: 1. Calculate the estimated break-even point in annual unit sales of the new product if the company uses the (a) computer-assisted…arrow_forwardUtica Manufacturing (UM) was recently acquired by MegaMachines, Inc. (MM). and organized as a separate division within the company. Most manufacturing plants at MM use an ABC system, but UM has always used a traditional product costing system. Bob Miller, the plant controller at UM, has decided to experiment with ABC and has asked you to help develop a simple ABC system that would help him decide if it was useful. The controller's staff has identified costs for the first month in the four overhead cost pools along with appropriate cost drivers for each pool. Activity Drivers Direct material cost Costs 154, 000 1,600, 900 900, 000 450, 000 Cost Pools Incoming inspection Production Machine-hours Machine setup Shipping Setups Units shipped The company manufactures two basic products with model numbers 308 and 510. The following are data for production for the first month as part of MM. Products 308 510 $ 45,000 $173,800 50,000 $ 32,000 $283,809 118,800 Total direct material costs Total…arrow_forward

- Maglie Company manufactures two video game consoles: handheld and home. The handheld consoles are smaller and less expensive than the home consoles. The company only recently began producing the home model. Since the introduction of the new product, profits have been steadily declining. Management believes that the accounting system is not accurately allocating costs to products, particularly because sales of the new product have been increasing. Management has asked you to investigate the cost allocation problem. You find that manufacturing overhead is currently assigned to products based on their direct labor costs. For your investigation, you have data from last year. Manufacturing overhead was $1,262,000 based on production of 320,000 handheld consoles and 114,000 home consoles. Direct labor and direct materials costs were as follows. Handheld Home Total Direct labor $1,192,500 $385,000 $1,577,500 Materials 780,000 711,000 1,491,000 Management has determined that…arrow_forwardMaglie Company manufactures two video game consoles: handheld and home. The handheld consoles are smaller and less expensive than the home consoles. The company only recently began producing the home model. Since the introduction of the new product, profits have been steadily declining. Management believes that the accounting system is not accurately allocating costs to products, particularly because sales of the new product have been increasing. Management has asked you to investigate the cost allocation problem. You find that manufacturing overhead is currently assigned to products based on their direct labor costs. For your investigation, you have data form last year. Manufacturing overhead was $1,432,000 based on production of 290,000 handheld consoles and 108,000 home consoles. Direct labor and direct materials costs were as follows. Handheld Home Total Direct labor…arrow_forwardMaglie Company manufactures two video game consoles: handheld and home. The handheld consoles are smaller and less expensive than the home consoles. The company only recently began producing the home model. Since the introduction of the new product, profits have been steadily declining. Management believes that the accounting system is not accurately allocating costs to products, particularly because sales of the new product have been increasing. Management has asked you to investigate the cost allocation problem. You find that manufacturing overhead is currently assigned to products based on their direct labor costs. For your investigation, you have data from last year. Manufacturing overhead was $1,320,000 based on production of 300,000 handheld consoles and 105,000 home consoles. Direct labor and direct materials costs were as follows. Handheld Home Total Direct labor $ 1,250,000 $ 400,000 $ 1,650,000 Materials $ 720,000 $ 657,000 $…arrow_forward

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning