Concept explainers

Videos

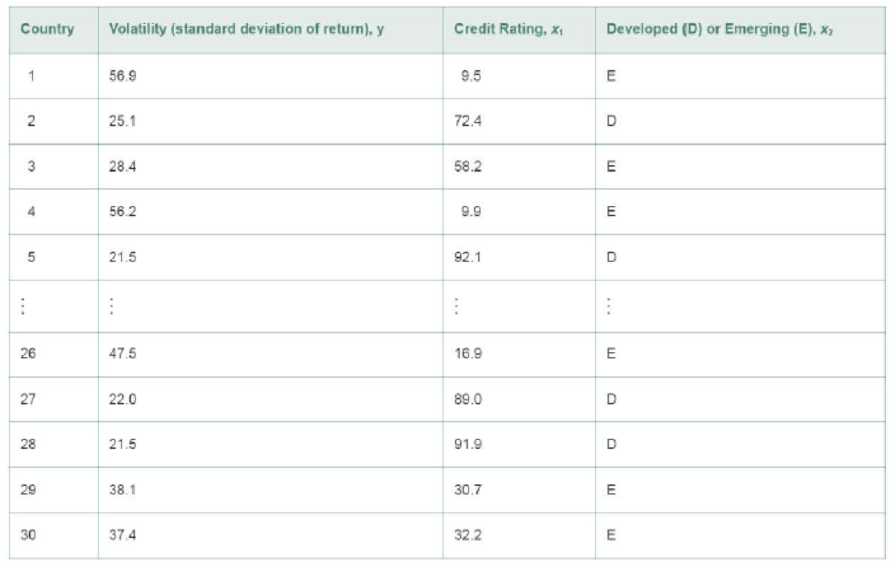

Volatility of foreign stocks. The relationship between country credit ratings and the volatility of the countries’ stock markets was examined in the Journal of Portfolio Management (Spring 1996). The researchers point out that this volatility can be explained by two factors: the countries’ credit ratings and whether the countries in question have developed or emerging markets. Data on the volatility (measured as the standard deviation of stock returns), credit rating (measured as a percentage), and market type (developed or emerging) for a sample of 30 fictitious countries are saved in the file. (Selected observations are shown in the table below.)

- a. Write a model that describes the relationship between volatility (y) and credit rating (x1) as two nonparallel lines, one for each type of market. Specify the dummy variable coding scheme you use.

- b. Plot volatility y against credit rating x1 for all the developed markets in the sample. On the same graph, plot y against x1 for all emerging markets in the sample. Does it appear that the model specified in part a is appropriate? Explain.

- c. Fit the model, part a. to the data using a statistical software package. Report the least squares prediction equation for each of the two types of markets.

- d. Plot the two prediction equations of part c on a

scatterplot of the data. - e. is there evidence to conclude that the slope of the linear relationship between volatility y and credit rating x1 depends on market type? Test using α=.01.

Want to see the full answer?

Check out a sample textbook solution

Chapter 12 Solutions

Statistics for Business and Economics Plus MyLab Statistics with Pearson eText -- Title-Specific Access Card Package (13th Edition)

Glencoe Algebra 1, Student Edition, 9780079039897...AlgebraISBN:9780079039897Author:CarterPublisher:McGraw Hill

Glencoe Algebra 1, Student Edition, 9780079039897...AlgebraISBN:9780079039897Author:CarterPublisher:McGraw Hill