1. a.

Prepare the

1. a.

Explanation of Solution

Investment: It refers to the process of using the currently held excess cash to earn profitable returns in future. The investments can be made in equity securities such as shares or debt securities such as bonds.

Available for sale securities: these are the securities which are not intended to be sold in the near future and there is no intension to hold the securities till their maturity.

Prepare the journal entries to record the investment in shares transactions, using fair value method, and classify the securities as available-for-sale securities.

Record the purchase of Company G’s shares on January 1, 2015.

Step 1: Determine the number of shares purchased.

Corporation S purchased 20% shares of Company G for

Step 2: Record the entry.

| Date | Account Title and Explanation | Debit | Credit |

| January 1, 2015 | Investment in Available-for-sale Securities | $160,000 | |

| Cash | $160,000 | ||

| (To record the purchase of 20% shares of Company G) |

Table (1)

Record the dividend income received on December 31, 2015.

Corporation S received

| Date | Account Title and Explanation | Debit | Credit |

| December 31, 2015 | Cash | $6,000 | |

| Dividend income | $6,000 | ||

| (To record the amount of dividend income received from investment) |

Table (2)

Record the unrealized gain or loss on available-for-sale securities, as on December 31, 2015.

Step 1: Determine the amount of unrealized holding loss or gain.

Step 2: Record the

| Date | Account Title and Explanation | Debit | Credit |

| December 31, 2015 | Unrealized holding gain or loss: Available-for-sale securities | $8,000 | |

|

Allowance for change in fair value of investment | $8,000 | ||

| (To record the unrealized holding loss on investment) |

Table (3)

Record the dividend income received on December 31, 2016.

Corporation S received

| Date | Account Title and Explanation | Debit | Credit |

| December 31, 2016 | Cash | $7,000 | |

| Dividend income | $7,000 | ||

| (To record the amount of dividend income received from investment) |

Table (4)

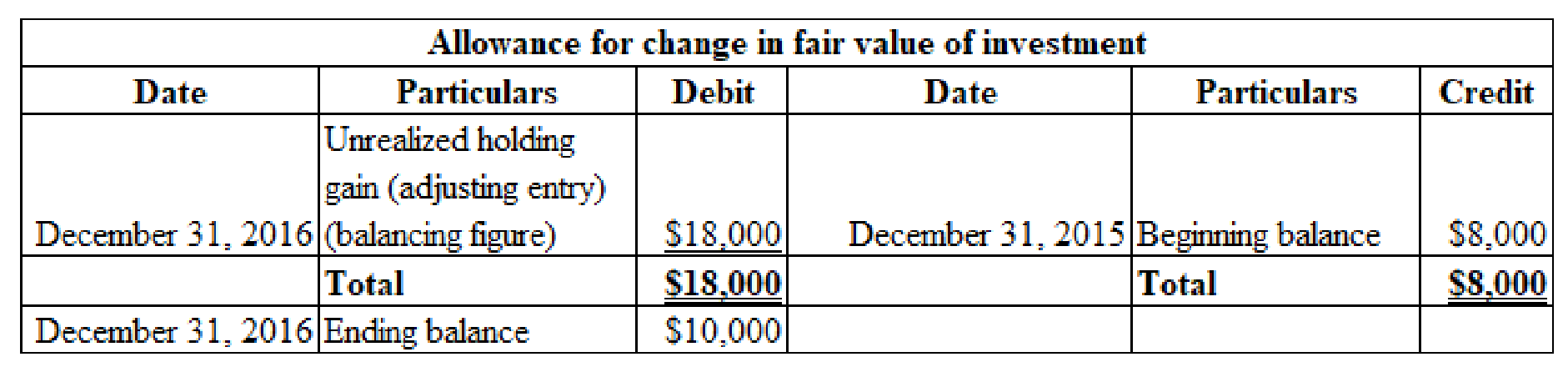

Record the unrealized gain or loss on available-for-sale securities, as on December 31, 2016.

Step 1: Determine the amount of unrealized holding loss or gain.

Step 2: Determine the amount of allowance to be adjusted to have $10,000 debit balance in allowance account at the end of the year 2016, using T-account.

Credit balance in allowance account on December 31, 2015 is $8,000.

Table (5)

Step 3: Record the adjusting entry.

| Date | Account Title and Explanation | Debit | Credit |

| December 31, 2016 | Allowance for change in fair value of investment | $18,000 | |

|

Unrealized holding gain or loss: Available-for-sale securities | $18,000 | ||

| (To adjust the unrealized holding gain on investment) |

Table (6)

Note:

Under the fair value method of recording the investment, no entry is required for recording the investee company’s net income.

1. b.

Prepare the journal entries to record the investment in shares transactions, using equity method.

1. b.

Explanation of Solution

Record the purchase of Company G’s 20% outstanding common stock:

| Date | Account Title and Explanation | Debit | Credit |

| January 1, 2015 | Investment in Stock: Company G | $160,000 | |

| Cash | $160,000 | ||

| (To record the purchase of 20% shares of Company G) |

Table (7)

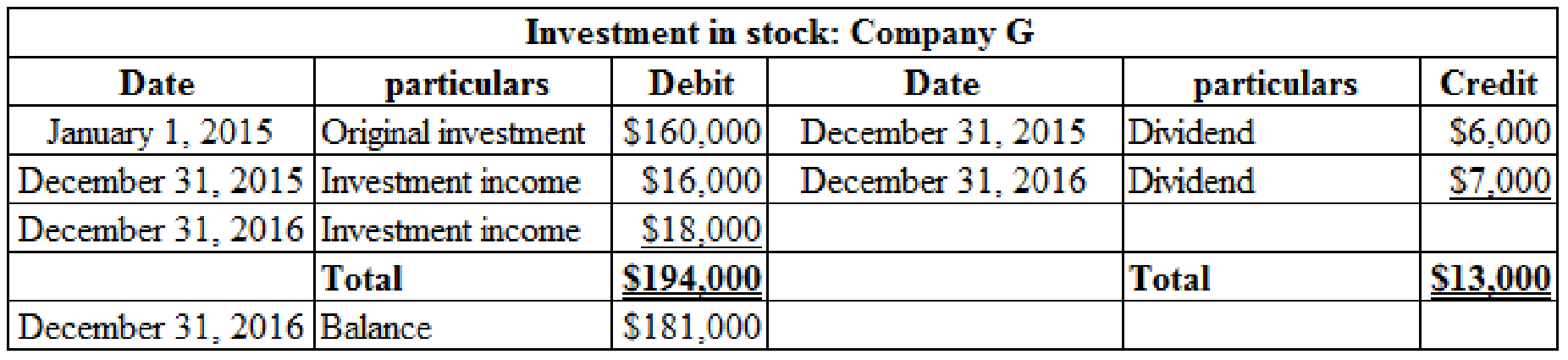

Record the income from investment.

Step 1: Determine the amount of investment income.

Step 2: Record the entry.

| Date | Account Title and Explanation | Debit | Credit |

| December 31, 2015 | Investment in Stock: Company G | $16,000 | |

| Investment income | $16,000 | ||

| (To record the income earned from investment) |

Table (8)

Record the receipt of dividend.

Step 1: Determine the amount of cash received as dividend.

Step 2: Record the entry.

| Date | Account Title and Explanation | Debit | Credit |

| December 31, 2015 | Cash | $6,000 | |

| Investment in Stock: Company G | $6,000 | ||

| (To record the receipt of cash dividend) |

Table (9)

Record the income from investment.

Step 1: Determine the amount of investment income.

Step 2: Record the entry.

| Date | Account Title and Explanation | Debit | Credit |

| December 31, 2016 | Investment in Stock: Company G | $18,000 | |

| Investment income | $18,000 | ||

| (To record the income earned from investment) |

Table (10)

Record the receipt of dividend.

Step 1: Determine the amount of cash received as dividend.

Step 2: Record the entry.

| Date | Account Title and Explanation | Debit | Credit |

| December 31, 2016 | Cash | $7,000 | |

| Investment in Stock: Company G | $7,000 | ||

| (To record the receipt of cash dividend) |

Table (11)

Note: Under the equity method of recording the investment, no entry is required for recording the increase in the investee company’s market value.

2. a.

Prepare the journal entries to record the sale of 10,000 of Company G’s shares, using fair value method, and classify the securities as available-for-sale securities.

2. a.

Explanation of Solution

Record the sale of 10,000 shares of Company G for $4.25 per share on January 4, 2017, under fair value method.

Corporation S sold Company G’s shares and received cash of $42,500

Determine the cost of investment in available-for-sale securities sold on January 4, 2017.

Record the entry.

| Date | Account Title and Explanation | Debit | Credit |

| January 4, 2017 | Cash | $42,500 | |

|

Investment in Available-for-sale Securities | $40,000 | ||

|

Gain on sale of Available-for-sale Securities | $2,500 | ||

| (To record the gain on sale of available-for-sale of securities) |

Table (12)

On January 4, 2017, reverse the unrealized gain that had accumulated at the end of December 31, 2016 for 10,000 numbers of shares sold.

The previously recorded $10,000 unrealized gain and allowance for 40,000 shares should be reversed as follows for 10,000 shares sold

| Date | Account Title and Explanation | Debit | Credit |

| January 4, 2017 | Unrealized holding gain or loss: Available-for-sale securities | $2,500 | |

|

Allowance for change in fair value of investment | $2,500 | ||

| (To reverse the allowance and the unrealized gain on holding the Securities of 10,000 shares) |

Table (13)

2. b.

Prepare the journal entries to record the sale of 10,000 of Company G’s shares, using equity method.

2. b.

Explanation of Solution

Record the sale of 10,000 shares of Company G for $4.25 per share on January 4, 2017, under equity method.

Determine the balance in Corporation S’s investment account on January 4, 2017.

Table (14)

Record the realized gain or loss from sale of 10,000 shares of Company G.

| Date | Account Title and Explanation | Debit | Credit |

| January 4, 2017 | Cash | $42,500 | |

| Loss on sale of equity investment | $2,750 | ||

| Investment in Stock: Company G | $45,250 | ||

| (To record the loss on sale of investment) |

Table (15)

Want to see more full solutions like this?

Chapter 13 Solutions

Bundle: Intermediate Accounting: Reporting And Analysis, 2017 Update, Loose-leaf Version, 2nd + Lms Integrated Cengagenowv2, 2 Terms Printed Access Card

- Parilo Company acquired 170,000 of Makofske Co., 5% bonds on May 1, 2016, at their face amount. Interest is paid semiannually on May 1 and November 1. On November 1, 2016, Parilo Company sold 50,000 of the bonds for 96. Journalize entries to record the following: a. The initial acquisition of the bonds on May 1. b. The semiannual interest received on November 1. c. The sale of the bonds on November 1. d. The accrual of 1,000 interest on December 31, 2016.arrow_forwardOBrien Industries Inc. is a book publisher. The comparative unclassified balance sheets for December 31, 2017 and 2016 follow. Selected missing balances are shown by letters. Note 1. Investments are classified as available for sale. The investments at cost and fair value on December 31, 2016, are as follows: Note 2. The investment in Jolly Roger Co. stock is an equity method investment representing 30% of the outstanding shares of Jolly Roger Co. The following selected investment transactions occurred during 2017: May 5. Purchased 3,080 shares of Gozar Inc. at 30 per share including brokerage commission. Gozar Inc. is classified as an available-for-sale security. Oct. 1. Purchased 40,000 of Nightline Co. 6%, 10-year bonds at 100. The bonds are classified as available for sale. The bonds pay interest on October 1 and April 1. 9. Dividends of 12,500 are received on the Jolly Roger Co. investment. Dec. 31. Jolly Roger Co. reported a total net income of 112,000 for 2017. OBrien Industries Inc. recorded equity earnings for its share of Jolly Roger Co. net income. 31. Accrued three months of interest on the Nightline bonds. 31. Adjusted the available-for-sale investment portfolio to fair value, using the following fair value per-share amounts: 31. Closed the OBrien Industries Inc. net income of 146,230. OBrien Industries Inc. paid no dividends during the year. Instructions Determine the missing letters in the unclassified balance sheet. Provide appropriate supporting calculations.arrow_forward

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning

Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning