Concept explainers

Videos

ATC 6-2 Group Assignment Relevance and cost behavior

Maccoa Soft, a division of Zayer Software Company, produces and distributes an automated payroll software system. A contribution margin format income statement for Maccoa Soft for the past year follows:

| Revenue (12,000 units × $1,200) | $14,400,000 |

| Unit-level variable costs | |

| Product materials cost (12,000 × $60) | (720,000) |

| Installation labor cost (12,000 × $200) | (2,400,000) |

| Manufacturing overhead (12,000 × $2) | (24,000) |

| Shipping and handling (12,000 × $25) | (300,000) |

| Sales commissions (12,000 × $300) | (3,600,000) |

| Nonmanufacturing miscellaneous costs (12,000 × $5) | (60,000) |

| Contribution margin (12,000 × $608) | 7,296,000 |

| Fixed costs | |

| Research and development | (2,700,000) |

| Legal fees to ensure product protection | (780,000) |

| Advertising costs | (1,200,000) |

| Rental |

(600,000) |

| (300,000) | |

| Other manufacturing costs (salaries, utilities, etc.) | (744,000) |

| Division-level facility sustaining costs | (1,730,000) |

| Allocated companywide facility-level costs | (1,650,000) |

| Net loss | $ (2,408,000) |

- a. Divide the class into groups and then organize the groups into three sections. Assign Task 1 to the first section, Task 2 to the second section, and Task 3 to the third section. Each task should be considered independently of the others.

Group Tasks

- (1) Assume that Maccoa has excess capacity. The sales staff has identified a large franchise company with 200 outlets that is interested in Maccoa’s software system but is willing to pay only $800 for each system. Ignoring qualitative considerations, should Maccoa accept the special order?

- (2) Maccoa has the opportunity to purchase a comparable payroll system from a competing vendor for $600 per system. Ignoring qualitative considerations, should Maccoa outsource producing the software? Maccoa would continue to sell and install the software if the manufacturing activities were outsourced.

- (3) Given that Maccoa is generating a loss, should Zayer eliminate it? Would your answer change if Maccoa could increase sales by 1,000 units?

- b. Have a representative from each section explain its respective conclusions. Discuss the following:

- (1) Representatives from Section 1 should respond to the following: The analysis related to the special order (Task 1) suggests that all variable costs are always relevant. Is this conclusion valid? Explain your answer.

- (2) Representatives from Section 2 should respond to the following: With respect to the outsourcing decision, identify a relevant fixed cost and a nonrelevant fixed cost. Discuss the criteria for determining whether a cost is or is not relevant.

- (3) Representatives from Section 3 should respond to the following: Why did the segment elimination decision change when the volume of production and sales increased?

a1.

Whether Division MS should accept the special order by ignoring the qualitative considerations.

Explanation of Solution

Variable cost: It is also called as production costs that change in extent to the measure of goods that are manufactured. In other words, for each product that is manufactured, variable costs increment by a similar amount.

Opportunity cost: Opportunity cost is the forfeit of certain benefits such as cost savings, incomes, which is surrendered by not picking an option. Opportunity costs are applicable in decisions where the acknowledgment of one option disqualifies the likelihood of selecting different alternatives.

Determine the unit-level incremental costs

Therefore the unit-level incremental cost is $592.

From the result obtained above, the fixed costs are irrelevant since they will continue the similar irrespective of whether the special order is accepted. The total unit-level incremental costs that will be incurred if the special order is accepted will be $592. Because the incremental cost per unit of $592 is less than the incremental income of $800 per unit, hence the special order should be accepted.

Therefore the special order should be accepted.

a2.

Whether Division MS should outsource producing the software by ignoring the qualitative considerations.

Explanation of Solution

Determine the total avoidable costs

Therefore the total avoidable cost is $5,568,000.

Determine the total avoidable cost per unit

Therefore the avoidable cost per unit is $464.

From the result obtained above, the total avoidable expense per unit is $464. Since the avoidable cost is less than the value required to buy of $600, Division MS would be in an ideal situation to keep on producing the software.

Therefore Division MS should produce the software.

a3.

Whether Company Z should eliminate Division MS.

Explanation of Solution

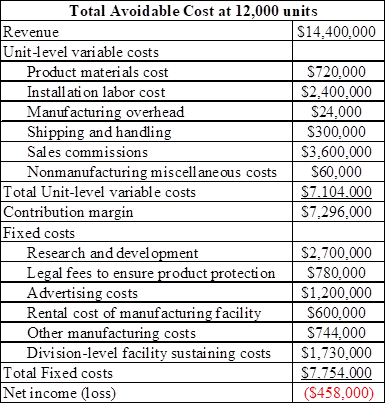

Determine the total avoidable costs at 12,000 units

If the division is eliminated, all expenses with the exception of the assigned companywide facility level expense and the depreciation on manufacturing the equipment or the sunk cost could be avoided.

Table (1)

(Refer excel for workings)

Therefore the total avoidable cost at 12,000 units is -$458,000.

From the result obtained above, the avoidable costs surpass the incremental revenue, the division must be eliminated.

Therefore Division MS should be eliminated.

Whether the answer changes if the sales increase by 1,000 units.

Explanation of Solution

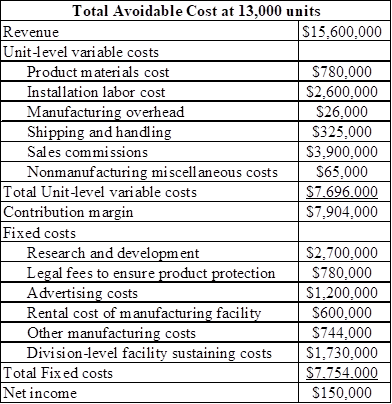

Determine the total avoidable costs at 13,000 units

The additional selling units of 1,000 units would build add up to the total sales of 13,000 units.

Table (2)

(Refer excel for workings)

Therefore the total avoidable cost at 13,000 units is $150,000.

From the result obtained above, At a sales volume level of 13,000 units, the division must not be eliminated.

Therefore Division MS should not be eliminated.

b1.

Whether the conclusion is valid.

Explanation of Solution

The reason on whether the conclusion is valid is as follows:

All the variable costs are not constantly relevant. For instance, assume that the special order customer move towards the organization openly, in this way eliminating the requirement to pay sales commissions. Under these conditions the sales commissions would not be relevant to a choice with respect to whether the special order should be accepted. The variable costs can be either relevant or irrelevant contingent upon the specific conditions related with the special decision.

b2.

The criteria for determining whether a cost is relevant or not relevant.

Explanation of Solution

The criteria for determining whether a cost is relevant or not relevant are as follows:

The research and development expenditures are applicable on the grounds that they are not incurred if the item is outsourced. The advertising costs are not relevant since they are important to advance the item irrespective of whether it is produced or outsourced. In other words, the costs must vary between the choices and be future arranged.

b3.

The reason on the segment elimination decision changes when the volume of production and sales increased.

Explanation of Solution

The reason on the segment elimination decision changes when the volume of production and sales increased are as follows:

Increases in volume influence the total contribution margin to increment. In like manner, additional margin is accessible to take care of fixed costs or to add to the productivity.

Want to see more full solutions like this?

Chapter 13 Solutions

SURVEY OF ACCOUNTING-ACCESS

- Activity-based and department rate product costing and product cost distortions Black and Blue Sports Inc. manufactures two products: snowboards and skis. The factory overhead incurred is as follows: Indirect labor 507,000 Cutting Department 156,000 Finishing Department 192,000 Total 855,000 The activity hase associated with the two production departments is direct labor hours. The indirect labor can be assigned to two different activities as follows: Activity Budgeted Activity Cost Activity Base Production control 237,000 Number of production runs Materials handling 270,000 Number of moves Total 507,000 The activity-base usage quantities and units produced for the two products follow: Number o Production Runs Number of Moves Direct Labor HoursCutting Direct Labor HoursFinishing Units Produced Snowboards 430 5,000 4,000 2,000 6,000 Skis _70 2,500 2,000 4,000 6,000 Total 500 7,500 6,000 6,000 12,000 Instructions 1. Determine the factory overhead rates under the multiple production department rate method. Assume that indirect labor is associated with the production departments, so that the total factory overhead is 315,000 and 540,000 for the Cutting and finishing departments, respectively. 2. Determine the total and per-unit factory overhead costs allocated to each product, using the multiple production department overhead rates in (1). 3. Determine the activity rates, assuming that the indirect labor is associated with activities rather than with the production departments. 4. Determine the total and per-unit cost assigned to each product under activity-based costing. 5. Explain the difference in the per-unit overhead allocated to each product under the multiple production department factory overhead rate and activity-based costing methods.arrow_forwardCommunication The controller of New Wave Sounds Inc. prepared the following product profitability report for management, using activity-based costing methods for allocating both the factory overhead and the marketing expenses. As such, the controller has confidence in the accuracy of this report. Home Theater Speakers Wireless Speakers Wireless Headphones Total Sales 1,500,000 1,200,000 900,000 3,600,000 Cost of goods sold 1,050,000 720,000 810,000 2,580,000 Gross profit 450,000 480,000 90,000 1,020,000 Marketing expenses 600,000 120,000 72,000 792,000 Income from operations (150,000) 360,000 18,000 228,000 In addition, the controller interviewed the vice president of marketing, who provided the following insight into the company's three products: The home theater speakers are an older product that is highly recognized in the marketplace. The wireless speakers are a new product that was just recently bunched. The wireless headphones are a new technology that has no competition in the marketplace, and it is hoped that they will become an important future addition to the companys product portfolio. Initial indications are that the product is well received by customers. The controller believes that the manufacturing costs for all three products are in line with expectations. Based on the information provided: 1. Calculate the ratio of gross profit to sales and the ratio of income from operations to sales for each product. 2. Write a brief (one page) memo using the product profitability report and the calculations in (1) to make recommendations to management with respect to strategies for the three products.arrow_forwardConstruct and interpret a product profitability report, allocating selling and administrative expenses Naper Inc. manufactures power equipment. Naper has two primary productsgenerators and air compressors. The following report was prepared by the controller for Napers senior marketing management for the year ended December 31: Generators Air Compressors Total Revenue 4,200,000 3,000,000 7,200,000 Cost of goods sold 2,940,000 2,100,000 5,040,000 Gross profit 1,260,000 900,000 2,160,000 Selling and administrative expenses 610,000 Income from operations 1,550,000 The marketing management team was concerned that the selling and administrative expenses were not traced to the products. Marketing management believed that some products consumed larger amounts of selling and administrative expense than did other products. To verify this, the controller was asked to prepare a complete product profitability report, using activity-based costing. The controller determined that selling and administrative expenses consisted of two activities: sales order processing and post-sale customer service. The controller was able to determine the activity base and activity rate for each activity, as follows: Activity Activity Base Activity Rate Sales order processing Sales orders 65 per sales order Post-sale customer service Service requests 200 per customer service request The controller determined the following activity-base usage information about each product: Generators Air Compressors Number of sales orders 3,000 4,000 Number of service requests 225 550 A. Determine the activity cost of each product for sales order processing and post-sale customer service activities. B. Use the information in (A) to prepare a complete product profitability report dated for the year ended December 31. Compute the gross profit to sales and the income from operations to sales percentages for each product. (Round to two decimal places.) C. Interpret the product profitability report. How should management respond to the report?arrow_forward

- Activity-based department rate product costing and product cost distortions Big Sound Inc. manufactures two products: receivers and loud-speakers. The factory overhead incurred is as follows: Indirect labor 400,400 Cutting Department 198,800 Finishing Department 114,800 Total 714,000 The activity base associated with the two production departments is direct labor hours. The indirect labor can be assigned to two different activities as follows: Activity Budgeted Activity Cost Activity Base Setup 138,600 Number of setup Quality Control 261,800 Number of inspections Total 400,400 The activity-base usage quantities and units produced for the two products follow: Number o Setup Number of Inspections Direct Labor HoursSubassembly Direct Labor HoursFinal Assembly Units Produced Snowboards 430 5,000 4,000 2,000 6,000 Skis _70 2,500 2,000 4,000 6,000 Total 500 7,500 6,000 6,000 12,000 Instructions 1. Determine the factory overhead rates under the multiple production department rate method. Assume that indirect labor is associated with the production departments, so that the total factory overhead is 5420,000 and 294,000 for the Subassembly and Final Assembly departments, respectively. 2. Determine the total and per-unit factory overhead costs allocated to each product, using the multiple production department overhead rates in (1). 3. Determine the activity rates, assuming that the indirect labor is associated with activities rather than with the production departments. 4. Determine the total and per-unit cost assigned to each product under activity-based costing. 5. Explain the difference in the per-unit overhead allocated to each product under the multiple production department factory overhead rate and activity-based costing methods.arrow_forwardActivity-based and department rate product costing and product cost distortions Black and Blue Sports Inc. manufactures two products: snowboards and skis. The factory overhead incurred is as follows: Indirect labor 507,000 Cutting Department 156,000 Finishing Department 192,000 Total 855,000 The activity hase associated with the two production departments is direct labor hours. The indirect labor can be assigned to two different activities as follows: Activity Budgeted Activity Cost Activity Base Production control 237,000 Number of production runs Materials handling 270,000 Number of moves Total 507,000 The activity-base usage quantities and units produced for the two products follow: Number o Production Runs Number of Moves Direct Labor HoursCutting Direct Labor HoursFinishing Units Produced Snowboards 430 5,000 4,000 2,000 6,000 Skis _70 2,500 2,000 4,000 6,000 Total 500 7,500 6,000 6,000 12,000 Instructions 1. Determine the factory overhead rates under the multiple production department rate method. Assume that indirect labor is associated with the production departments, so that the total factory overhead is 315,000 and 540,000 for the Cutting and finishing departments, respectively. 2. Determine the total and per-unit factory overhead costs allocated to each product, using the multiple production department overhead rates in (1). 3. Determine the activity rates, assuming that the indirect labor is associated with activities rather than with the production departments. 4. Determine the total and per-unit cost assigned to each product under activity-based costing. 5. Explain the difference in the per-unit overhead allocated to each product under the multiple production department factory overhead rate and activity-based costing methods.arrow_forwardActivity-based department rate product costing and product cost distortions Big Sound Inc. manufactures two products: receivers and loud-speakers. The factory overhead incurred is as follows: Indirect labor 400,400 Cutting Department 198,800 Finishing Department 114,800 Total 714,000 The activity base associated with the two production departments is direct labor hours. The indirect labor can be assigned to two different activities as follows: Activity Budgeted Activity Cost Activity Base Setup 138,600 Number of setup Quality Control 261,800 Number of inspections Total 400,400 The activity-base usage quantities and units produced for the two products follow: Number o Setup Number of Inspections Direct Labor HoursSubassembly Direct Labor HoursFinal Assembly Units Produced Snowboards 430 5,000 4,000 2,000 6,000 Skis _70 2,500 2,000 4,000 6,000 Total 500 7,500 6,000 6,000 12,000 Instructions 1. Determine the factory overhead rates under the multiple production department rate method. Assume that indirect labor is associated with the production departments, so that the total factory overhead is 5420,000 and 294,000 for the Subassembly and Final Assembly departments, respectively. 2. Determine the total and per-unit factory overhead costs allocated to each product, using the multiple production department overhead rates in (1). 3. Determine the activity rates, assuming that the indirect labor is associated with activities rather than with the production departments. 4. Determine the total and per-unit cost assigned to each product under activity-based costing. 5. Explain the difference in the per-unit overhead allocated to each product under the multiple production department factory overhead rate and activity-based costing methods.arrow_forward

Survey of Accounting (Accounting I)AccountingISBN:9781305961883Author:Carl WarrenPublisher:Cengage Learning

Survey of Accounting (Accounting I)AccountingISBN:9781305961883Author:Carl WarrenPublisher:Cengage Learning Financial & Managerial AccountingAccountingISBN:9781337119207Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial & Managerial AccountingAccountingISBN:9781337119207Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Financial & Managerial AccountingAccountingISBN:9781285866307Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial & Managerial AccountingAccountingISBN:9781285866307Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning