Concept explainers

Videos

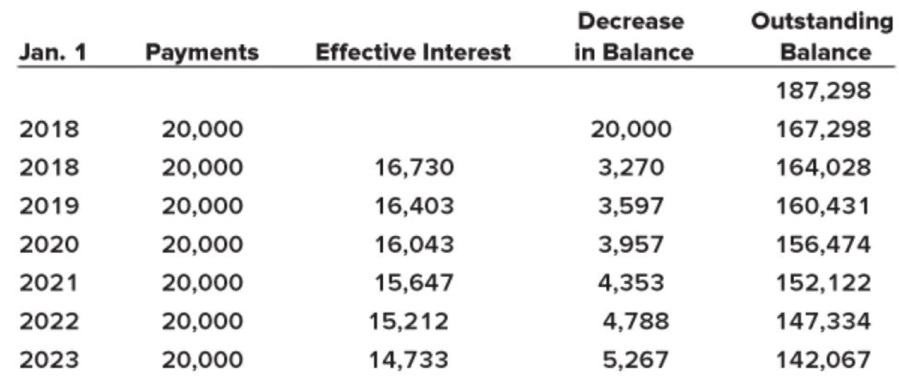

Lease amortization schedule

• LO15–2

On January 1, 2018, Majestic Mantles leased a lathe from Equipment Leasing under a finance lease. Lease payments are made annually. Title does not transfer to the lessee and there is no purchase option or guarantee of a residual value by Majestic. Portions of the Equipment Leasing’s lease amortization schedule appear below:

Required:

1. What is Majestic’s lease liability at the beginning of the lease (after the first payment)?

2. What amount would Majestic record as a right-of-use asset?

3. What is the lease term in years?

4. What is the effective annual interest rate?

5. What is the total amount of lease payments?

6. What is the total effective interest expense recorded over the term of the lease?

Want to see the full answer?

Check out a sample textbook solution

Chapter 15 Solutions

INTERMEDIATE ACCOUNTING(LL)-W/CONNECT

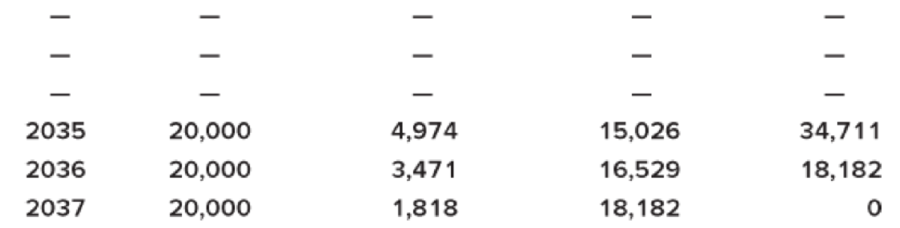

- PROBLEM NO. 3 Assume that DBP Leasing Corp. and Minasugbo Inc. sign a lease contract effective on January 1, 2019 where DBP Leasing leases to Minasugbo a bulldozer. The terms and provisions of the lease contract and other pertinent date are as follows: • The term of the lease is five years. The lease agreement is non-cancelable, requiring equal rental payments of P20,711.11 at the beginning of each year (annuity-due basis). The bulldozer has a fair value at the commencement of the lease of P100,000, an estimated economic life of five years, and a guaranteed residual value of P5,000. (Minasugbo expects that it is probable that the expected value of the residual value at the end of the lease will be greater than the guaranteed amount of P5,000.) The lease contains no renewal options. The bulldozer reverts to DBP Leasing at the termination of the lease. Minasugbo's incremental borrowing rate is 5 percent per year. • Minasugbo depreciates its equipment on a straight-line basis. DBP Leasing…arrow_forwardEP#5 On January 1, 2021, Yancey, Inc. signs a 10-year noncancelable lease agreement to lease a storage building from Holt Warehouse Company. Collectibility of lease payments is reasonably predictable and no important uncertainties surround the amount of costs yet to be incurred by the lessor. The following information pertains to this lease agreement.(a) The agreement requires equal rental payments at the beginning each year.(b) The fair value of the building on January 1, 2021 is $6,000,000; however, the book value to Holt is $4,950,000.(c) The building has an estimated economic life of 10 years, with no residual value. Yancey depreciates similar buildings using the straight-line method.(d) At the termination of the lease, the title to the building will be transferred to the lessee.(e) Yancey’s incremental borrowing rate is 11% per year. Holt Warehouse Co. set the annual rental to insure a 10% rate of return. The implicit rate of the lessor is known by Yancey, Inc.(f) The yearly…arrow_forwardOn January 1, 2024, National Insulation Corporation (NIC) leased equipment from United Leasing under a finance lease. Lease payments are made annually. Title does not transfer to the lessee and there is no purchase option or guarantee of a residual value by NIC. Portions of the United Leasing’s lease amortization schedule appear below: January 1 Payments Effective Interest Decrease in Balance Outstanding Balance 2024 $ 244,813 2024 $ 27,000 $ 27,000 $ 217,813 2025 $ 27,000 $ 23,959 $ 3,041 $ 214,772 2026 $ 27,000 $ 23,625 $ 3,375 $ 211,397 2027 $ 27,000 $ 23,254 $ 3,746 $ 207,651 2028 $ 27,000 $ 22,842 $ 4,158 $ 203,493 2029 $ 27,000 $ 22,384 $ 4,616 $ 198,877 — — — — — — — — — — — — — — — 2041 $ 27,000 $ 10,852 $ 16,148 $ 82,505 2042 $ 27,000 $ 9,076 $ 17,924 $ 64,581 2043 $ 27,000 $ 7,104 $ 19,896 $ 44,685 2044 $ 49,600 $ 4,915 $ 44,685 $ 0 What is the asset’s residual value expected at the end of the lease term? What is the effective…arrow_forward

- (Leases) 6 Exercise 15-5 (Static) Sales-type lease; lessor; balance sheet and income statement effects [LO15-3] On June 30, 2021, Georgia-Atlantic, Inc. leased warehouse equipment from Bullders, Inc. The lease agreement calls for Georgia- Atlantic to make semiannual lease payments of $562,907 over a three-year lease term (also the asset's useful life), payable each June 30 and December 31, with the first payment at June 30, 2021. Georgia-Atlantic's incremental borrowing rate is 10%, the same rate Builders used to calculate lease payment amounts. Builders manufactured the equipment at a cost of $2.5 million. (FV of $1, PV of $1, FVA of $1, PVA of $1, FVAD of $1 and PVAD of $1) (Use appropriate factor(s) from the tables provided.) Required: 1. Determine the price at which Builders is "selling" the equipment (present value of the lease payments) at June 30, 2021. 2. What amount related to the lease would Builders report in its balance sheet at December 31, 2021 (ignore taxes)? 3. What…arrow_forwardOn January 1, 2024, National Insulation Corporation (NIC) leased equipment from United Leasing under a finance lease. Lease payments are made annually. Title does not transfer to the lessee and there is no purchase option or guarantee of a residual value by NIC. Portions of the United Leasing’s lease amortization schedule appear below: January 1 Payments Effective Interest Decrease in Balance Outstanding Balance 2024 $ 244,813 2024 $ 27,000 $ 27,000 $ 217,813 2025 $ 27,000 $ 23,959 $ 3,041 $ 214,772 2026 $ 27,000 $ 23,625 $ 3,375 $ 211,397 2027 $ 27,000 $ 23,254 $ 3,746 $ 207,651 2028 $ 27,000 $ 22,842 $ 4,158 $ 203,493 2029 $ 27,000 $ 22,384 $ 4,616 $ 198,877 — — — — — — — — — — — — — — — 2041 $ 27,000 $ 10,852 $ 16,148 $ 82,505 2042 $ 27,000 $ 9,076 $ 17,924 $ 64,581 2043 $ 27,000 $ 7,104 $ 19,896 $ 44,685 2044 $ 49,600 $ 4,915 $ 44,685 $ 0 What is the lease term in years? 20 years What is the asset’s residual value expected at the end…arrow_forwardThe details of the equipment lease agreement that Taj Corp. (lessee) recently entered into with Stanger Leasing (lessor) are: Commencement date: January 1, 2019. ■ Term of lease: 12 months. Payments: $1,000 per month first due at the commencement date. Other: Title does not transfer and the lease does not include any renewal or purchase options. Interest rate implicit in the lease: Lessee not able to readily determine. Incremental borrowing rate: 9% per annum (0.75% per month). Estimated useful life of equipment: 8 years. Depreciation method: Straight-line. Year end: December 31. Assume that Taj Corp. does not elect to expense leases of a short-term nature. Prepare the journal entry for January 31, 2019.arrow_forward

- Question 1 (theory) What was the major change in accounting for leases introduced by new accounting standard AASB16/IFRS16? Why was such a change launched by the professional standard setting bodies to abandon AASB117/IAS17? Question 2 On 1 July 2020, Sherlock Ltd leased a processing plant to Holmes Ltd. The plant was purchased by Sherlock Ltd on 1 July 2020 for its fair value of $467 112. The lease agreement contained the following provisions: Lease term 3 years Economic terms of the plant 5 years Annual rental payments, in arrears (commencing 30?6/2021) $150,000 Residual value at the end of lease term $90,000 Residual guaranteed by lessee $60,000 Interest rate implicit in lease 7% The lease is cancellable only with the permission of the lessor Holmes Ltd intends to return the processing plant to Sherlock Ltd at the end of the lease term. The lease has been classified as a finance lease by Sherlock Ltd. Required: Prepare: (a) the…arrow_forwardSales-Type Lease with Guaranteed Residual Value Calder Company, the lessor, enters into a lease with Darwin Company, the lessee, to provide heavy equipment beginning January 1, 2017. The lease is appropriately classified as a sales-type lease. The lease terms, provisions, and related events are as follows: The lease is noncancelable, has a term of 8 years, and has no renewal or bargain purchase option. The annual rentals are 65,000, payable at the end of each year. The interest rate implicit in the lease is 15%. Darwin agrees to pay all executory costs directly to a third party. The cost of the equipment is 280,000. The fair value of the equipment to Calder is 308,021.03. Calder incurs no material initial direct costs. Calder expects that it will be able to collect all lease payments. Calder estimates that the fair value at the end of the lease term will be 50,000 and that the economic life the equipment is 9 years. This residual value is guaranteed by Darwin. The following present value factors are relevant: PV of an ordinary annuity n = 8, i = 15% = 4.487322 PV n = 8, i = 15% = 0.326902 PV n = 1, i = 15% = 0.869565 Required: 1. Determine the proper classification of the lease. 2. Prepare a table summarizing the lease receipts and interest income earned by Calder for this lease. 3. Prepare journal entries for Calder for the years 2019, 2020, and 2021. 4. Next Level Prepare partial balance sheets for December 31, 2019, and December 31, 2020, showing how the accounts should be reported. Use the present value of next years payment approach to classify the lease receivable as current and noncurrent. 5. Next Level Prepare partial balance sheets for December 31, 2019, and December 31, 2020, showing how the accounts should be reported. Use the change in present value approach to classify the lease receivable as current and noncurrent.arrow_forwardLessee Accounting Issues Sax Company signs a lease agreement dated January 1, 2019, that provides for it to lease computers from Appleton Company beginning January 1, 2019. The lease terms, provisions, and related events are as follows: 1. The lease term is 5 years. The lease is noncancelable and requires equal rental payments to be made at the end of each year. The computers are not specialized for Sax. 2. The computers have an estimated life of 5 years, a fair value of 300,000, and a zero estimated residual value. 3. Sax agrees to pay all executory costs directly to a third party. 4. The lease contains no renewal or bargain purchase options. 5. The annual payment is set by Appleton at 83,222.92 to earn a rate of return of 12% on its net investment. Sax is aware of this rate. Saxs incremental borrowing rate is 10%. 6. Sax uses the straight-line method to record depreciation on similar equipment. Required: 1. Next Level Examine and evaluate each capitalization criteria and determine what type of lease this is for Sax. 2. Calculate the amount of the asset and liability of Sax at the inception of the lease (round to the nearest dollar). 3. Prepare a table summarizing the lease payments and interest expense. 4. Prepare journal entries for Sax for the years 2019 and 2020.arrow_forward

- Lessor Accounting with Guaranteed Residual Value Use the information for Edom Company in E20-8, except that the residual value was guaranteed by Davis Company (the lessee). Required: 1. Assuming that the lease is a sales-type lease, calculate the selling price. 2. Prepare a table summarizing the lease receipts and interest income earned by Edom. 3. Prepare journal entries for Edom tor the years 2019 and 2020.arrow_forwardLeased Assets Koffman and Sons signed a four-year lease for a forklift on January 1, 2016. Annual lease payments of $1,510, based on an interest rate of 8%, are to be made every December 31, beginning with December 31, 2016. Required Assume that the lease is treated as an operating lease. Will the value of the forklift appear on Koffmans balance sheet? What account will indicate that lease payments have been made? Assume that the lease is treated as a capital lease. Prepare any journal entries needed when the lease is signed. Explain why the value of the leased asset is not recorded at $6,040 (1,5104). Prepare the journal entry to record the first lease payment on December 31, 2016. Calculate the amount of depreciation expense for the year 2016. At what amount would the lease obligation be presented on the balance sheet as of December 31, 2016?arrow_forwardLessee Accounting with Payments Made at Beginning of Year Adden Company signs a lease agreement dated January 1, 2019, that provides for it to lease non-specialized heavy equipment from Scott Rental Company beginning January 1, 2019. The lease terms, provisions, and related events are as follows: 1. The lease term is 4 years. The lease is noncancelable and requires annual rental payments of 20,000 to be paid in advance at the beginning of each year. 2. The cost, and also fair value, of the heavy equipment to Scott at the inception of the lease is 68,036.62. The equipment has an estimated life of 4 years and has a zero estimated residual value at the end of this time. 3. Adden agrees to pay all executory costs directly to a third party. 4. The lease contains no renewal or bargain purchase options. 5. Scotts interest rate implicit in the lease is 12%. Adden is aware of this rate, which is equal to its borrowing rate. 6. Adden uses the straight-line method to record depreciation on similar equipment. 7. Executory costs paid at the end of the year by Adden are: Required: 1. Next Level Determine what type of lease this is for Adden. 2. Prepare a table summarizing the lease payments and interest expense for Adden. 3. Prepare journal entries for Adden for the years 2019 and 2020.arrow_forward

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning

Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning