Videos

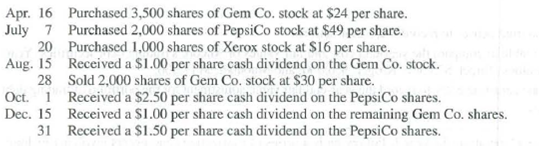

Rose Company had no short-term investments prior to this year. It had the following transactions this year involving short-term stock investments with insignificant influence.

Required

- 1. Prepare

journal entries to record the preceding transactions and events. - 2. Prepare a table to compare the year-end cost and fair values of Rose’s short-term stock investments. The year-end fair values per share are Gem Co., $26; PepsiCo, $46; and Xerox, $13.

- 3. Prepare an

adjusting entry to record the year-end fair value adjustment for the portfolio of short-term stock investments.

Analysis Component

- 4. Explain the

balance sheet presentation of the fair value adjustment for Rose's short-term investments. - 5. How do these short-term stock investments affect Rose’s (a) income statement for this year and (b) the equity section of its balance sheet at this year-end?

1.

Prepare the journal entries to record the given transactions.

Explanation of Solution

Journal entry:

Journal entry is a set of economic events which can be measured in monetary terms. These are recorded chronologically and systematically.

Prepare the journal entries to record the given transactions as follows:

| Date | Account Titles and Description | Post Ref. | Debit ($) | Credit ($) |

| April 16, | Stock Investments in company G (1) | 84,000 | ||

| Cash | 84,000 | |||

| (To record the Purchase of 4,000 shares of Company G in cash) | ||||

| July 7, | Stock Investments in Company P (2) | 98,000 | ||

| Cash | 98,000 | |||

| (To record 2,000 shares of company P purchased in cash) | ||||

| July 20, | Stock Investments in company X (3) | 16,000 | ||

| Cash | 16,000 | |||

| (To record 1,000 shares of Company X purchased in cash) | ||||

| August 15, | Cash | 3,500 | ||

| Dividend Revenue (4) | 3,500 | |||

| (To record dividend revenue received in cash) | ||||

| August 28, | Cash (5) | 60,000 | ||

| Stock Investments in Company G (6) | 48,000 | |||

| Gain on Sale of Stock Investments (7) | 12,000 | |||

| (To record sales made 2,000 shares at the rate of $30 per share) | ||||

| October 1, | Cash | 5,000 | ||

| Dividend Revenue (8) | 5,000 | |||

| (To record dividend revenue received in cash) | ||||

| December 1, | Cash | 1,500 | ||

| Dividend Revenue (9) | 1,500 | |||

| (To record dividend revenue received in cash) | ||||

| December 31, | Cash | 3,000 | ||

| Dividend Revenue (10) | 3,000 | |||

| (To record dividend revenue received in cash) |

Table (1)

Working note:

Calculate the purchased value of stock investment (Company G)

Calculate the purchased value of stock investment (Company P)

Calculate the purchased value of stock investment (Company X)

Calculate the dividend revenue received from Company G

Calculate the value of cash received from the sale of stock investment (Company G stocks)

Calculate the purchase value of long-term investment for 2,000 shares of Company G

Calculate the gain (loss) from sale of stock investment.

Calculate the dividend revenue received from Company P

Calculate the dividend revenue received from Company G

Calculate the dividend revenue received from Company X

2.

Prepare a table to compare the year-end cost and fair value of Company R’s stock investments in available-for sale securities.

Explanation of Solution

Prepare a table to compare the year-end cost and fair value of Company R’s stock investments in available-for sale securities as follows:

| Name of the company | Cost of short-term investment | Fair value of short-term investment | Unrealized gain or (loss) |

| Company G | $36,000 (12) | $39,000 (13) | |

| Company P | $98,00 (2) | $92,000 (14) | |

| Company X | $16,000 (3) | $13,000 (15) | |

| Totals | $150,000 | $144,000 | $(6,000) (15) |

Table (2)

Working note:

Calculate the cost of stock investment of Company G

Calculate the fair value of stock investment of Company G

Calculate the fair value of stock investment of Company P

Calculate the fair value of stock investment of Company X

Calculate the value of unrealized gain or loss

3.

Prepare an adjusting entry, if necessary, to record the year-end fair value adjustment for the portfolio of stock investments in available-for-sale securities.

Explanation of Solution

Adjusting entries:

Adjusting entries refers to the entries that are made at the end of an accounting period in accordance with revenue recognition principle, and expenses recognition principle. The purpose of adjusting entries is to adjust the revenue, and expenses during the period in which they actually occurs.

Prepare an adjusting entry, if necessary, to record the year-end fair value adjustment for the portfolio of stock investments in available-for-sale securities as follows:

Adjusting entry for unrealized loss:

| Date | Account Titles and Description | Post Ref. | Debit ($) | Credit ($) |

| December, 31 | Unrealized loss - Equity | 6,000 | ||

| Fair value adjustment | 6,000 | |||

| (To record the adjustment entry for unrealized loss at the end of the accounting year ) |

Table (3)

- Unrealized Loss–Equity is an adjustment account to report the investment at fair market value. Since loss has occurred while adjusting; therefore, debit the unrealized Gain or Loss–Equity account with $6,000.

- Fair Value Adjustment is a contra-asset account. The account shows a credit balance since the market price has decreased (loss); therefore, credit the fair value adjustment with $6,000.

4.

Explain the manner in which the fair value adjustment of Company R’s stock investment is presented in the balance sheet.

Explanation of Solution

Explain the manner in which the fair value adjustment of Company R’s stock investment is presented in the balance sheet as follows:

Cost of stock investment in available-for-sale securities of $150,000 is reported in the assets side of the balance sheet and unrealized loss of $6,000 is subtracted from the cost of investment for the fair value adjustment. Net fair value of $144,000

5.

Explain the manner in which the stock investments affect company R’s

- a. Income statement for the year, and

- b. The equity section of the balance sheet at year ended.

Explanation of Solution

Explain the manner in which the stock investments affect company R’s income statement for the year, and the equity section of the balance sheet at year ended as follows:

(a) Income statement:

- Unrealized loss-Interest Revenue, $6,000

- Dividend Revenue, $13,000 (17)

- Gain on Sale of Stock Investments, $12,000

- Net effect on income is $19,000

(b) Equity section of Balance sheet:

- Increase to equity from the $19,000 increase in income

Working note:

Calculate the value of total dividend revenue received:

Want to see more full solutions like this?

Chapter 15 Solutions

Principles of Financial Accounting.

- Assume that Lily Corporation has outstanding 1,500 shares of 150 par callable preferred stock that were issued at 175 per share, and that no dividends are in arrears. If the call price is 185 per share, what journal entry will Lily make to record the recall of these shares?arrow_forwardVictoria Company has investments in marketable securities classified as trading and available-for-sale. At the beginning of the year, the aggregate market value of each portfolio exceeded its amortized cost. During the year, Victoria sold some securities from each portfolio. At the end of the year, the aggregate amortized cost of each portfolio exceeded its market value. Victoria also has investments in bonds classified as held-to-maturity, all of which were purchased for face value. During the year, some of these bonds held by Victoria were called prior to their maturity by the bond issuer. Three months before the end of the year, additional similar bonds were purchased for face value plus 2 months accrued interest. Required: 1. Explain how Victoria accounts for: a. sale of securities from each portfolio b. each equity securities portfolio at year-end 2. Explain how Victoria accounts for the disposition prior to their maturity of the long-term bonds called by their issuer. 3. Explain how Victoria reports the purchase of the additional similar bonds at the date of the acquisition.arrow_forwardDuring Year 2, Copernicus Corporation held a portfolio of available-for-sale securities having a cost of $183,300. There were no purchases or sales of investments during the year. The market values at the beginning and end of the year were $216,300 and $174,100, respectively. The net income for Year 2 was $168,600, and no dividends were paid during the year. The Stockholders' Equity section of the balance sheet was as follows on December 31, Year 1: Copernicus CorporationStockholders' EquityDecember 31, Year 1 Common stock $38,000 Paid-in capital in excess of par 290,000 Retained earnings 381,300 Unrealized gain on available-for-sale investments 33,000 Total stockholders’ equity $742,300 Prepare the Stockholders' Equity section of the balance sheet for December 31, Year 2.arrow_forward

- Carlsville Company began operations in the current year and had no prior stock investments. The following transactions are from its short-term stock investments with insignificant influence. Prepare journal entries to record these transactions. On December 31, prepare the adjusting entry to record the fair value adjustment for the portfolio of stock investments. July 22 Purchased 1,600 shares of Hunt Corp. at $30 per share. Sep. 5 Received a $2 cash dividend for each share of Hunt Corp. Sep. 27 Purchased 3,400 shares of HCA at $34 per share. Oct. 3 Sold 1,600 shares of Hunt at $25 per share. Oct. 30 Purchased 1,200 shares of Black & Decker at $50 per share. Dec. 17 Received a $3 cash dividend for each share of Black & Decker. Dec. 31 Fair value of the short-term stock investments is $180,000.arrow_forwardDuring the month, Blue, Inc. purchased 1,050 shares for $7.00 per share and classified them as trading investments. At the end of the month, the price of the securities was $11.25 per share. What adjusting entry, if any, will Blue, Inc. record when it closes its books at the end of the month to reflect this change in value?ᐧ a Dr. Valuation Allowance for Trading Investments $11,812.50 Cr. Unrealized Gain on Trading Investments $11,812.50 b Dr. Unrealized Loss on Trading Investment $4,462.50 Cr. Valuation Allowance for Trading Investments $4,462.50 c Dr. Valuation Allowance for Trading Investments $4,462.50 Cr. Unrealized Gain on Trading Investments $4,462.50 Because the trading investments were not sold during the month, no adjusting entry is required. d Dr. Valuation Allowance for Trading Investments $4,462.50 Cr. Realized Gain on Trading Investments $4,462.50arrow_forwardA company issues 10,000 shares of its own $10 par value common stock to the public for $19 per share. Later, 1, 000 of these shares are bought for $21 per share as treasury stock. Which of the Losses on the resale of these shares would impact reported net income for the year although gains would not The par value method and the cost method have the same total impact on stockholders equity Because this is a stock transaction, retained earnings cannot be affected by a re - issuance of these sharesarrow_forward

- Conroy Financial paid $530,000 for a 20% investment in the common stock ofMaverick, Inc. For the first year, Maverick reported net income of $270,000, and at year-enddeclared and paid cash dividends of $115,000. On the balance-sheet date, the fair value of Conroy’s investment in Maverick stock was $410,000.Requirements1. Which method is appropriate for Conroy to use in its accounting for its investment inMaverick? Why?2. Show everything that Conroy would report for the investment and any investment revenuein its year-end financial statements.arrow_forwardOn October 17, 2021, LILAC Corporation exchanged 20,000 shares of its ₱200 par value stock for land. A few months ago, the land was appraised by an independent appraiser at ₱5,000,000. The land had an initial cost of ₱4,500,000. LILAC is currently trading at the stock exchange at ₱300. How much should be credited to Share Premium upon the issuance of the shares? Choose answer, either a or b. Show solution in good accounting form. a.) ₱ - 0 - b. ) ₱ 2,000,000arrow_forwardLexington Co. has the following securities outstanding on December 31, 2017 (its first year of operations). Cost Fair Value Greenspan Corp. stock $20,000 $19,000 Summerset Company stock 9,500 8,800 Tinkers Company stock 20,000 20,600 $49,500 $48,400 During 2018, Summerset Company stock was sold for $9,200, the difference between the $9,200 and the “fair value” of $8,800 being recorded as a “Gain on Sale of Investments.” The market price of the stock on December 31, 2018, was Greenspan Corp. stock $19,900; Tinkers Company stock $20,500.Instructions(a) What justification is there for valuing equity securities at fair value and reporting the unrealized gain or loss as part of net income?(b) How should Lexington Co. report this information in its financial statements at December 31, 2017? Explain.(c) Did Lexington Co. properly account for the sale of the Summerset Company stock? Explain.(d) Are there any additional entries necessary for Lexington Co. at December 31,…arrow_forward

- Brad Dolan, a stockholder of Rhode Corporation, has asked you, the firm's accountant, to explain why his stock warrants were not included in diluted EPS. In order to explain this situation, you must briefly explain what dilutive securities are, why they are included in the EPS calculation, and why some securities are antidilutive and thus not included in this calculation. Rhode Corporation earned $228,000 during the period, when it had an average of 100,000 shares of common stock outstanding. The common stock sold at an average market price of $25 per share during the period. Also outstanding were 30,000 warrants that could be exercised to purchase one share of common stock at $30 per warrant. Instructions Write Mr. Dolan a 1–1.5-page letter explaining why the warrants are not included in the calculation.arrow_forwardSmith Corporation had 30,000 shares of common stock outstanding during the year. In addition, there were compensatory share options to purchase 3,000 shares of common stock at $20 a share outstanding the entire year. The average market price for the common stock during the year was $36 a share. The unrecognized compensation cost (net of tax) relating to these options was $4 a share. What is the denominator to compute the diluted earnings per share? Group of answer choices 31,333 31,000 33,000 None of the above 31,667arrow_forwardRose Company had no short-term investments prior to this yearIt had the following transactions this year involving short- term stock Investments with insignificant influence. April 16 Purchased 6,000 shares of Gem Company stock at $25.75 per share. July 7 Purchased 3,000 shares of PepsiCo stock at $46.00 per share. July 20 Purchased 1,500 shares of Xerox stock at $19.00 per share. August 15 Received a 8.95 per share cash dividend on the Gem Company stock. August 28 Sold 3,000 shares of Company stock at $32.50 per share. October 1 Received a $2.00 per share cash dividend on the PepsiCo shares. December 15 Received a $1.10 per share cash dividend on the remaining Gem Company shares. December 31 Received a $1.30 per share cash dividend on the PepsiCo shares. The year-end fair values per share are Gem Company$28.00 PepsiCo, 43.25and Xerox, $16.00 Required: Prepare journal entries to record the preceding transactions and events.arrow_forward

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning