Concept explainers

Videos

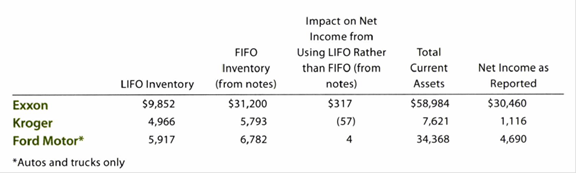

Under U.S. GAAP, LIFO is an acceptable inventory method. Financial statement information for three companies that use LIFO follows. All table numbers are in millions of dollars.

Assume these companies adopted IFRS, and thus were required to use FIFO, rather than LIFO.

a. Prepare a table with the following columns:

(1) Difference between FIFO and LIFO

(2) Revised IFRS net income using FIFO.

(3) Difference between FIFO and LIFO inventory valuation as a percent of total current assets.

(4) Revised IFRS net income as a percent of the reported net income.

b. Complete the table for the three companies.

c. For which company would a change to IFRS for inventory valuation have the largest percentage impact on total current assets (Col. 3)?

d. For which company would a change to IFRS for inventory valuation have the largest percentage impact on net income (Col. 4)?

e. Why might Kroger have a negative impact on net income from using LIFO, while the other two companies have a positive impact on net income from using LIFO?

(a)

International Financial Reporting Standards (IFRS): IFRS are a set of international accounting standards which are framed, approved, and published by International Accounting Standards Board (IASB) for the preparation and disclosure of international financial reports.

Generally Accepted Accounting Principles (GAAP): These are the guidelines necessary to create accounting principles for the implementation of financial information reporting in the Country U.

First-in-First-Out(FIFO): In this method, items purchased initially are sold first. So, the value of the ending inventory consists the recent cost for the remaining unsold items.

Last-in-First-Out(LIFO): In this method, items purchased recently are sold first. So, the value of the ending inventory consists the initial cost for the remaining unsold items.

To draft: A table with the columns given in the problem

Explanation of Solution

Table is prepared as follows (amounts in millions of dollars):

| FIFO less LIFO | IFRS Net Income | |||

| Company E | ||||

| Company K | ||||

| Company F |

Table (1)

(b)

To complete: The table prepared in Part (a)

Explanation of Solution

Complete the table as follows (amounts in millions of dollars):

| FIFO less LIFO | IFRS Net Income | |||

| Company E | $21,348 | $30,143 | ||

| Company K | 827 | 1,173 | ||

| Company F | 865 | 4,686 |

Table (2)

Working Notes:

Compute FIFO less LIFO (amounts in millions of dollars).

| FIFO | LIFO | FIFO less LIFO | |

| Company E | $31,200 | $9,852 | $21,348 |

| Company K | 5,793 | 4,966 | 827 |

| Company F | 6,782 | 5,917 | 865 |

Table (3)

Deduct the LIFO value from FIFO value to get FIFO less LIFO.

Compute IFRS net income (amounts in millions of dollars).

| Net Income as Reported | Impact on Net Income From Using LIFO Rather Than FIFO | IFRS Net Income | |

| Company E | $30,460 | $317 | $30,143 |

| Company K | 1,116 | (57) | 1,173 |

| Company F | 4,690 | 4 | 4,686 |

Table (4)

Deduct the impact on net income value from net income reported value to get IFRS net income.

Compute FIFO less LIFO divided by total current assets (amounts in millions of dollars).

| FIFO less LIFO | Total Current Assets | ||

| Company E | $21,348 | $58,984 | 36% |

| Company K | 827 | 7,621 | 11% |

| Company F | 865 | 34,368 | 3% |

Table (5)

Divide FIFO less LIFO value by total current assets value to get the value in last column. Refer to Table (3) for value and computation of FIFO less LIFO value.

Compute IFRS net come divided by reported net income(amounts in millions of dollars).

| IFRS Net Income | Net Income as Reported | ||

| Company E | $30,143 | $30,460 | 99% |

| Company K | 1,173 | 1,116 | 105% |

| Company F | 4,686 | 4,690 | 100% |

Table (6)

Divide IFRS net income value by reported net income value to get the value in last column. Refer to Table (4) for value and computation of IFRS net income value.

(c)

To indicate: The company which would have the highest impact on total current assets due to change in inventory valuation method, if the company uses IFRS instead of GAAP

Answer to Problem 3IFRS

If the inventory valuation method is changed to reflect the use of IFRS, Company E would have greatest impact on total current assets.

Explanation of Solution

Refer to Table (5) for value and computation of impact of change in inventory valuation method on total current assets.

(d)

To indicate: The company which would have the highest impact on net income due to change in inventory valuation method, if the company uses IFRS instead of GAAP

Answer to Problem 3IFRS

If the inventory valuation method is changed to reflect the use of IFRS, Company K would have greatest impact on net income.

Explanation of Solution

Refer to Table (6) for value and computation of impact of change in inventory valuation method on net income.

(e)

To discuss: The reasons for negative impact on net income if LIFO is used rather than FIFO

Explanation of Solution

During inflation, the inventory purchased last will have higher price than the inventory purchased first. Thus, under LIFO method, the inventory purchased last with higher price will be sold first, thereby increasing the cost of goods sold. Increase in cost of goods sold decreases the net income.

Want to see more full solutions like this?

Chapter 15FSI Solutions

Bundle: Accounting, Chapters 1-13, 26th + Working Papers, Chapters 1-17 For Warren/reeve/duchac's Accounting, 26th And Financial Accounting, 14th + ... For Warren/reeve/duchac's Accounting, 26th

- Below is the net income of New Girl Instrument AG, a private company, computed under the two inventory methods using a periodic system. FIFO Average-Cost 2017 $26,000 $23,000 2018 30,000 25,000 2019 29,000 27,000 2020 34,000 30,000 (ignore tax considerations) Required: a. Assume that in 2020 New Girl decided to change from the FIFO method to the average-cost method of pricing inventories. Prepare the journal entry necessary for the change that took place during 2020, and show net income reported for 2017, 2018, 2019, and 2020. b. Assume that in 2020 New Girl, which had been using the average-cost method since beginning operations in 2017, changed to the FIFO method of pricing inventories. Prepare the journal entry necessary to record the change in 2020, and show net income reported for 2017, 2018, 2019, and 2020.arrow_forwardIn 2022, Kimberly Corporation changed its method of inventory pricing from LIFO to FIFO. Net income computed on a LIFO as compared to a FIFO basis for the four years involved is: (Ignore income taxes.) LIFO FIFO 2019 $78,600 $87,400 2020 84,000 88,900 2021 86,800 90,600 2022 92,800 92,200 (a)Indicate the net income that would be shown on comparative financial statements issued at 12/31/22 for each of the four years, assuming that the company changed to the FIFO method in 2022. Net Income 2019 $ 2020 $ 2021 $ 2022 $arrow_forwardWhen following U.S. GAAP, the lower-of-cost-or-market rule for inventory requires a firm to report ________. Group of answer choices the inventory at cost if the market value of inventory is higher than its cost basis the inventory at the higher amount of cost or market on the balance sheet the difference between the cost basis and the market-based measure of inventory as a gain on the income statement the inventory at cost if the market value of inventory is lower than its cost basisarrow_forward

- Required:a. Complete a subsidiary ledger record for the computer using each of the three inventory valuation methods listed below 1. Average cost.2. FIFO.3. LIFO. Your inventory records should show both purchases of this product, the sale on Mar 31, and the balance on hand on Mar 31, 2020. b. Which of the three cost flow assumptions will result in reporting the lowest net income for the current year? Explainarrow_forwardColonial Corporation uses the retail method to value its inventory. The following information is available for the year: Beginning inventory Purchases Freight-in Net markups Net markdowns Net sales Beginning inventory Purchases Freight-in Net markups Required: Determine ending inventory and cost of goods sold by applying the conventional retail method using the information provided. Note: Round ratio calculation to 2 decimal places (i.e., 0.1234 should be entered as 12.34%.). Enter amounts to be deducted with a minus sign. Net markdowns Goods available for sale Cost-to-retail percentage Net sales Cost $ 190,000 600,000 8,000 Estimated ending inventory at retail Estimated ending inventory at cost Estimated cost of goods sold Retail $ 280,000 840,000 $ 20,000 4,000 800,000 Cost 190,000 $ 600,000 8,000 798,000 $ Retail 280,000 840,000 20,000 1,140,000 (4,000) 1,136,000 79,520 1,056,480 Cost-to-Retail Ratio 70.00 %arrow_forwardCarey Company adheres to U.S. GAAP, whereas Jonathan Company adheres to IFRS. Itis least likely that:A. Carey has reversed an inventory write-down.B. Jonathan has reversed an inventory write-down.C. Jonathan and Carey both use the FIFO inventory accounting method.arrow_forward

- Under the last-in, first-out (LIFO) inventory valuation method, a price index for inventory must be established for tax purposes. The quantity weights are based on year-ending inventory levels. Unit Price ($) Ending Inventory Ending Product Beginning A 500 0.15 0.19 B 50 1.40 1.80 100 4.50 4.20 D 40 12.00 13.40 Use the beginning-of-the-year price per unit as the base-period price and develop a weighted aggregate index for the total inventory value at the end of the year. (Round your answer to the nearest integer.) I = What type of weighted aggregate price index must be developed for the LIFO inventory valuation? O Laspeyres Index O Paasche indexarrow_forwardDuring 2010, Orca Corp. decided to change from the FIFO method of inventory valuation to the weighted-average method. Inventory balances under each method were as follows:FIFO Weighted-averageJanuary 1, 2010 71,000 77,000December 31, 2010 79,000 83,000Orca’s income tax rate is 30%. In its 2010 financial statements, what amount should Orca report as the cumulative effect of this accounting change?a.2,800b.4,000c.4,200d.6,000arrow_forwardThe following information for Tuell Company is available: 1. Assume Tuell uses the LIFO cost flow assumption. what is the correct inventory value in each of the preceding situations under U.S. GAAP? 2. Assume Tuell Uses the average cost inventorγcost flow asstrmption. what is the correct inventory value in each of the preceding situations under U .S. GAAP? 3. Assume that Tuell uses the average cost inventory cost flow assumption. What is the correct inventor)' value rn each of the preceding situations if Tuell uses IFRS?arrow_forward

- At the end of the Year 2 accounting period, DeYoung Company determined that the market value of its inventory was $79,800. The historical cost of this inventory was $81,400. DeFazio uses the perpetual inventory method. Assuming the amount is immaterial, how will the necessary write-down to reduce the inventory to the lower-of-cost-or-market affect the company's financial statements? Multiple Choice O O Decrease total assets, gross margin, and net income Increase total assets and net income Decrease total assets and gross margin Decrease total assets and net incomearrow_forwardOn January 1, 2020, Bonanza Wholesalers Inc. adopted the dollar-value LIFO inventory method for income tax and external financial reporting purposes. However, Bonanza continued to use the FIFO inventory method for internal accounting and management purposes. In applying the LIFO method, Bonanza uses internal conversion price indexes and the multiple pools approach under which substantially identical inventory items are grouped into LIFO inventory pools. The following data were available for inventory pool no. 1, which comprises products A and B, for the 2 years following the adoption of LIFO. FIFO Basis per Records Units Unit Cost Total Cost Inventory, 1/1/20 Product A 10,000 $30 $300,000 Product B 9,000 25 225,000 $525,000 Inventory, 12/31/20 Product A 17,000 36 $612,000 Product B 9,000 26 234,000 $846,000 Inventory, 12/31/21 Product A 13,000 40 $520,000 Product B 10,000 32 320,000 $840,000…arrow_forwardBelow is the net income of New Girl Instrument AG, a private company, computed under the two inventory methods using a periodic system. FIFO P26,000 30,000 29,000 34,000 (Ignore tax considerations.) Average Cost P23,000 25,000 27,000 30.000 2017 2018 2019 2020 Required a. Assume that in 2020 New Girl decided to change from the FIFO method to the average-cost method of pricing inventories. Prepare the journal entry necessary for the change that took place during 2020, and show net income reported for 2017, 2018, 2019, and 2020.arrow_forward

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning