INTERMEDIATE ACCOUNTING(LL)-W/2 ACCESS

9th Edition

ISBN: 9781260180657

Author: SPICELAND

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Concept explainers

Videos

Textbook Question

Chapter 16, Problem 16.27E

• LO16–8

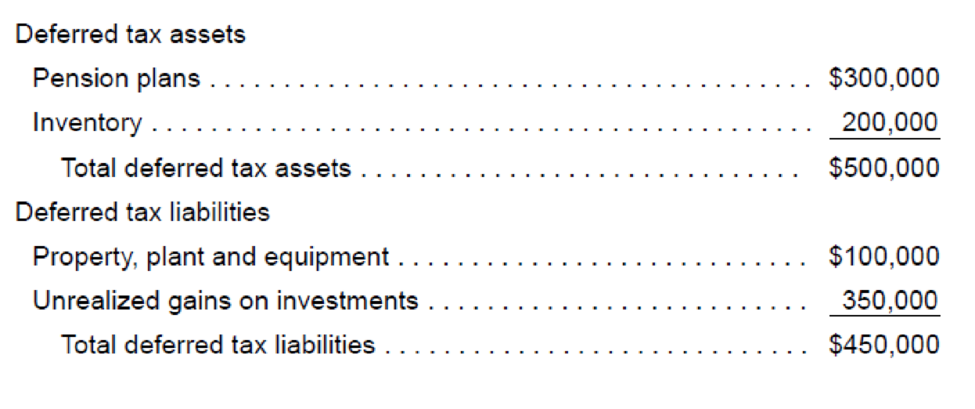

As of December 31, 2016, Lange Company has the following

Required:

1. Assume that all of Lange’s deferred tax assets and liabilities are in the same tax jurisdiction. How would

2. Assume that the deferred tax effects of Lange’s pension plans and unrealized gains on investments occurred in a different tax jurisdiction from Lange’s other deferred tax effects. How would deferred taxes be shown on Lange’s balance sheet?

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Students have asked these similar questions

Question 1

What is the main principle of tax-effect accounting as outlined in AASB 112/IAS 12?

Answer:

XX

Question 2

How are the current and future tax consequences of transactions accounted for?

Answer:

XX

Question 3

What is an ‘exempt income’ and how does it affect the calculation or recovery of carry‐forward tax losses?

Answer:

XX

Question 4

Calculation of Current Tax Liability (CTL)

SydMel Ltd commences operations on 1 July 2020. One year later, on 30 June 2021, the entity prepares its first statement of comprehensive income and its first statement of financial position. The statements are prepared before considering taxation. The following information is available.

Statement of Profit or Loss and other Comprehensive Income

For the year ended 30 June 2021

Gross Profit

$510,000

Salaries expenses

(210,000)

Rent expense

(52,000)

Long service leave expenses

(50,000)

Depreciation expense - Plant

(30,000)

Bad debt expense

(19,000)…

Question 7

For each of the following items, indicate whether it would generate a permanent or temporary tax

difference:

Use of different depreciation methods for financial reporting and

tax reporting purposes

The incurrence of fines for late tax payments

The payment of monies as prepayment for services to be received

in future periods (prepaid asset)

The receipt of non-taxable interest

The recognition of warranty expense using the allowance method

[Select]

[Select]

[Select]

[Select]

[Select]

Problem 16-9 (Algo) Determine deferred tax assets and liabilities from book-tax differences; financial

statement effects [LO16-2, 16-3]

Corning-Howell reported taxable income in 2024 of $200 million. At December 31, 2024, the reported amount of some assets and

liabilities in the financial statements differed from their tax bases as indicated below:

Assets

Current

Net accounts receivable

Prepaid insurance

Prepaid advertising

Noncurrent

Investments in equity securities (fair value) *

Buildings and equipment (net)

Liabilities

Current

Deferred subscription revenue

Long-term

Liability-compensated future absences

Gains and losses taxable when investments are sold.

Carrying Amount

Tax Basis

$ 88 million

$ 92 million

100 million

0

84 million

84 million

0

440 million

360 million

92 million

0

674 million

0

The total deferred tax asset and deferred tax liability amounts at January 1, 2024, were $196.25 million and $25 million, respectively.

The enacted tax rate is 25% each year.

Required:

1.…

Chapter 16 Solutions

INTERMEDIATE ACCOUNTING(LL)-W/2 ACCESS

Ch. 16 - Prob. 16.1QCh. 16 - A deferred tax liability (or asset) is described...Ch. 16 - Prob. 16.3QCh. 16 - Prob. 16.4QCh. 16 - Temporary differences result in future taxable or...Ch. 16 - Identify three examples of differences with no...Ch. 16 - The income tax rate for Hudson Refinery has been...Ch. 16 - Suppose a tax reform bill is enacted that causes...Ch. 16 - A net operating loss occurs when tax-deductible...Ch. 16 - Prob. 16.10Q

Ch. 16 - Additional disclosures are required pertaining to...Ch. 16 - Additional disclosures are required pertaining to...Ch. 16 - Prob. 16.13QCh. 16 - Prob. 16.14QCh. 16 - IFRS and U.S. GAAP follow similar approaches to...Ch. 16 - Temporary difference LO161 A company reports...Ch. 16 - Prob. 16.2BECh. 16 - Temporary difference LO162 A company reports...Ch. 16 - Prob. 16.4BECh. 16 - Temporary difference; income tax payable given ...Ch. 16 - Valuation allowance LO162, LO163 At the end of...Ch. 16 - Valuation allowance LO162, LO163 VeriFone Systems...Ch. 16 - Temporary and permanent differences; determine...Ch. 16 - Calculate taxable income LO161, LO164 Shannon...Ch. 16 - Multiple tax rates LO165 J-Matt, Inc., had pretax...Ch. 16 - Change in tax rate LO165 Superior Developers...Ch. 16 - Net operating loss carryforward LO167 During its...Ch. 16 - Net operating loss carryback LO167 AirParts...Ch. 16 - Tax uncertainty LO169 First Bank has some...Ch. 16 - Intraperiod tax allocation LO1610 Southeast...Ch. 16 - Temporary difference; taxable income given LO161...Ch. 16 - Prob. 16.2ECh. 16 - Prob. 16.3ECh. 16 - Prob. 16.4ECh. 16 - Prob. 16.5ECh. 16 - Prob. 16.6ECh. 16 - Identify future taxable amounts and future...Ch. 16 - Calculate income tax amounts under various...Ch. 16 - Determine taxable income LO161, LO162 Eight...Ch. 16 - Prob. 16.10ECh. 16 - Deferred tax asset; income tax payable given;...Ch. 16 - Prob. 16.12ECh. 16 - Prob. 16.13ECh. 16 - Multiple differences LO164, LO166 For the year...Ch. 16 - Multiple t ax rates LO162, LO165 Allmond...Ch. 16 - Prob. 16.16ECh. 16 - Deferred taxes; change in tax rates LO161, LO165...Ch. 16 - Multiple temporary differences; record income...Ch. 16 - Multiple temporary differences; record income...Ch. 16 - Net operating loss carryforward LO167 During...Ch. 16 - Net operating loss carryback LO167 Wynn Sheet...Ch. 16 - Net operating loss carryback and carryforward ...Ch. 16 - Identifying income tax deferrals LO161, LO162,...Ch. 16 - Multiple temporary differences; balance sheet...Ch. 16 - Multiple tax rates LO161, LO164, LO165 Case...Ch. 16 - Prob. 16.26ECh. 16 - Balance sheet classification LO168 As of December...Ch. 16 - Concepts; terminology LO161 through LO168 Listed...Ch. 16 - Tax credit; uncertainty regarding sustainability ...Ch. 16 - Intraperiod tax allocation LO1610 The following...Ch. 16 - FASB codification research LO165, LO168, LO1610...Ch. 16 - Prob. 16.1PCh. 16 - Prob. 16.2PCh. 16 - Prob. 16.3PCh. 16 - Prob. 16.4PCh. 16 - Change in tax rate; record taxes for four years ...Ch. 16 - Multiple differences; temporary difference yet to...Ch. 16 - Multiple differences; calculate taxable income;...Ch. 16 - Multiple differences; taxable income given; two...Ch. 16 - Determine deferred tax assets and liabilities ...Ch. 16 - Prob. 16.10PCh. 16 - Prob. 16.11PCh. 16 - Prob. 16.12PCh. 16 - Prob. 16.13PCh. 16 - Prob. 16.1BYPCh. 16 - Prob. 16.2BYPCh. 16 - Integrating Case 163 Tax effects of accounting...Ch. 16 - Communication Case 164 Deferred taxes; changing...Ch. 16 - Prob. 16.5BYPCh. 16 - Research Case 166 Researching the way tax...Ch. 16 - Analysis Case 167 Reporting deferred taxes; Ford...Ch. 16 - Prob. 16.8BYPCh. 16 - Judgment Case 169 Analyzing the effect of deferred...Ch. 16 - Prob. 16.12BYPCh. 16 - Target Case LO16-1, LO16-2, LO16-4, LO16-8,...Ch. 16 - Prob. 1CCIFRS

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- 1 contiune Listed below are items that are commonly accounted for differently for financial reporting purposes than they are for tax purposes.For each item below, indicate whether it involves: 1. A temporary difference that will result in future deductible amounts and, therefore, will usually give rise to a deferred income tax asset. 2. A temporary difference that will result in future taxable amounts and, therefore, will usually give rise to a deferred income tax liability. 3. A permanent difference. (e) Installment sales of investments are accounted for by the accrual method for financial reporting purposes and the installment method for tax purposes.(f) For some assets, straight-line depreciation is used for both financial reporting purposes and tax purposes, but the assets’ lives are shorter for tax purposes.(g)…arrow_forwardQuestion 11: Which statement regarding the calculation of taxes is accurate? Answer: A. O For simplicity, taxable income for local, state, and federal income tax withholdings has been standardized. B. O All taxes are calculated based on net pay. C. O Because retirement plans are exempt from federal income tax, you add the contributed amount before calculating the employee's federal withholding. D. O Taxes may be calculated based on an amount lower than gross pay, and not all taxes are calculated based on the same amount. Question 12: Which of these is a credit reduction state/territory? Question 15: Union dues are considered a deduction. Answer: Answer: A. A. O Connecticut O cafeteria B. O Ohio B. O insurance C. O Virginia C. O mandatory D. O U.S. Virgin Islands D. O voluntary Question 14: Alejandra owns and operates an appliance store where employees clock in and out for each shift. Per the FLSA, Alejandra rounds employee time worked to the nearest 15-minute increment. On Tuesday this…arrow_forwardWhich of the following statements concerning the classification of deferred tax assets and liabilities is true? Multiple Choice A deferred tax asset is classified as noncurrent only if the company expects the future tax benefit to be received more than 12 months from the balance sheet date. All deferred tax assets and liabilities are treated as noncurrent. A deferred tax asset related to a bad debt reserve is classified as current if the related accounts receivable is classified as a current asset. A deferred tax asset related to inventory capitalization is classified as noncurrent only if the company uses a FIFO accounting method and the inventory to which the deferred tax asset relates will not be treated as sold within 12 months from the balance sheet date.arrow_forward

- Question 11: Which statement regarding the calculation of taxes is accurate? Answer: A. O For simplicity, taxable income for local, state, and federal income tax withholdings has been standardized. В. O All taxes are calculated based on net pay. С. O Because retirement plans are exempt from federal income tax, you add the contributed amount before calculating the employee's federal withholding. D. O Taxes may be calculated based on an amount lower than gross pay, and not all taxes are calculated based on the same amount. Question 12: Which of these is a credit reduction state/territory? Question 15: Union dues are considered a deduction. Answer: Answer: A. O Connecticut A. O cafeteria В. O Ohio В. O insurance C. O Virginia O mandatory С. D. O U.S. Virgin Islands D. O voluntary Question 14: Alejandra owns and operates an appliance store where employees clock in and out for each shift. Per the FLSA, Alejandra rounds employee time worked to the nearest 15-minute increment. On Tuesday this…arrow_forwardQ.1.1 The government announced a change to the tax law which will have a significanteffect on the value of current tax expense that the company will pay in future years. For each of the events described above, discuss whether an adjusting or non‐adjusting eventoccurred. In order to get the mark allocated you will need to justify why you believe the event is either an adjusting or non‐adjusting event.Where the events are adjusting, describe the adjustment that must be made as well as theamount and where the events are non‐adjusting, discuss whether any disclosure needs to bemade in the notes to the financial statements. Justify your answers.arrow_forward1continue.. Listed below are items that are commonly accounted for differently for financial reporting purposes than they are for tax purposes.For each item below, indicate whether it involves: 1. A temporary difference that will result in future deductible amounts and, therefore, will usually give rise to a deferred income tax asset. 2. A temporary difference that will result in future taxable amounts and, therefore, will usually give rise to a deferred income tax liability. 3. A permanent difference. (e) Installment sales of investments are accounted for by the accrual method for financial reporting purposes and the installment method for tax purposes. (f) For some assets, straight-line depreciation is used for both financial reporting purposes and tax purposes, but the assets’ lives are shorter for tax purposes. (g)…arrow_forward

- Deferred Tax Assets. Components of the deferred tax asset of Biosante Pharmaceuticals, Inc., are shown in Exhibit 2.14. The company had no deferred tax liabilities. REQUIRED a. At the end of 2008, the largest deferred tax asset is for net operating loss carryforwards. (Net operating loss carryforwards [also referred to as tax loss carryforwards] are amounts reported as taxable losses on tax filings. Because the tax authorities generally do not pay corporations for incurring losses, companies are allowed to carry forward taxable losses to future years to offset taxable income. These future tax benefits give rise to deferred tax assets.) As of the end of 2008, what is the dollar amount of the companys net operating loss carryforwards? What is the dollar amount of the deferred tax asset for the net operating loss carryforwards? Describe how these two amounts are related. b. Biosante has gross deferred tax assets of 28,946,363. However, the net deferred tax assets balance is zero. Explain. c. The valuation allowance for the deferred tax asset increased from 21,818,084 to 28,946,363 between 2007 and 2008. How did this change affect the company's net income?arrow_forwardQuestion 2: Which of the following is an accurate statement about SUTA tax? Answer: A. O Every state designates a taxable earnings threshold below which SUTA tax is not levied. O SUTA tax paid by an employer is typically less than FUTA tax paid for the same period. В. C. SUTA tax rates differ from one employer to another but do not change from year to year. D. The SUTA tax rate is based on the number of layoffs that an employer has experienced.arrow_forwardUnless a company has a legal right of set-off, IAS 12 Income Taxes, requires disclosure of all of the following information for deferred tax in the statement of financial position: I The amount of deferred tax assets recognised II The amount of the deferred tax liabilities recognised III The net amount of the deferred tax assets and liabilities recognised IV The amount of the deferred tax asset relating to tax losses a. I, II and III only b. III and IV only c. I, II and IV only d. IV onlyarrow_forward

- Listed below are items that are treated differently for accounting purposes than they are for tax purposes. Indicate whether the items are permanent differences or temporary differences. For temporary differences, indicate whether they will create deferred tax assets or deferred tax liabilities. 1. Investments accounted for by the equity method (ignore dividends received deduction). 2. Advance rental receipts. 3. Fine for polluting. 4. Estimated future warranty costs. 5. Excess…arrow_forwardWhen income tax expense differs from income taxes currently payable on taxable income companies recognize deferred tax assets and deferred tax liabilities. What type of event would create a deferred tax asset and deferred tax liability? Please provide numerical examples. Discuss the two principal reasons income before taxes for financial reporting differs from taxable income. Please provide an argument over the life of the assets deferred liabilities and deferred assets cancel each other out. Use minimum two in text citation that must match peer reviewed referencesarrow_forwardExercise 16-10 (Algo) Calculate income tax amounts under various circumstances; financial statement effects [LO16-2, 16-3] Four independent situations are described below. Each involves future deductible amounts and/or future taxable amounts produced by temporary differences: ($ in thousands) Taxable income Future deductible amounts Future taxable amounts. Balance(s) at beginning of the year: Deferred tax asset Deferred tax liability The enacted tax rate is 25%. Required: Situation 1 2 3 4 $ 112 $ 244 $ 252 $ 344 16 20 20 16 16 56 2 16 8 2 For each situation, determine the following: Note: Enter your answers in thousands rounded to one decimal place (i.e. 1,200 should be entered as 1.2). Negative amounts should be indicated by a minus sign. Leave no cell blank, enter "O" wherever applicable. a. Income tax payable currently. b. Deferred tax asset-ending balance. c. Deferred tax asset-change. d. Deferred tax liability-ending balance. e. Deferred tax liability change. f. Income tax…arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Financial Reporting, Financial Statement Analysis...FinanceISBN:9781285190907Author:James M. Wahlen, Stephen P. Baginski, Mark BradshawPublisher:Cengage Learning

Financial Reporting, Financial Statement Analysis...FinanceISBN:9781285190907Author:James M. Wahlen, Stephen P. Baginski, Mark BradshawPublisher:Cengage Learning Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning

Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning

Financial Reporting, Financial Statement Analysis...

Finance

ISBN:9781285190907

Author:James M. Wahlen, Stephen P. Baginski, Mark Bradshaw

Publisher:Cengage Learning

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:9781337788281

Author:James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:Cengage Learning

Financial Accounting: The Impact on Decision Make...

Accounting

ISBN:9781305654174

Author:Gary A. Porter, Curtis L. Norton

Publisher:Cengage Learning

Chapter 19 Accounting for Income Taxes Part 1; Author: Vicki Stewart;https://www.youtube.com/watch?v=FMjwcdZhLoE;License: Standard Youtube License