Concept explainers

Videos

FIFO method (continuation of 17-36).

- 1. Do Problem 17-36 using the FIFO method of

process costing . Explain any difference between the cost per equivalent unit in the assembly department under the weighted-average method and the FIFO method. - 2. Should Hoffman’s managers choose the weighted-average method or the FIFO method? Explain briefly.

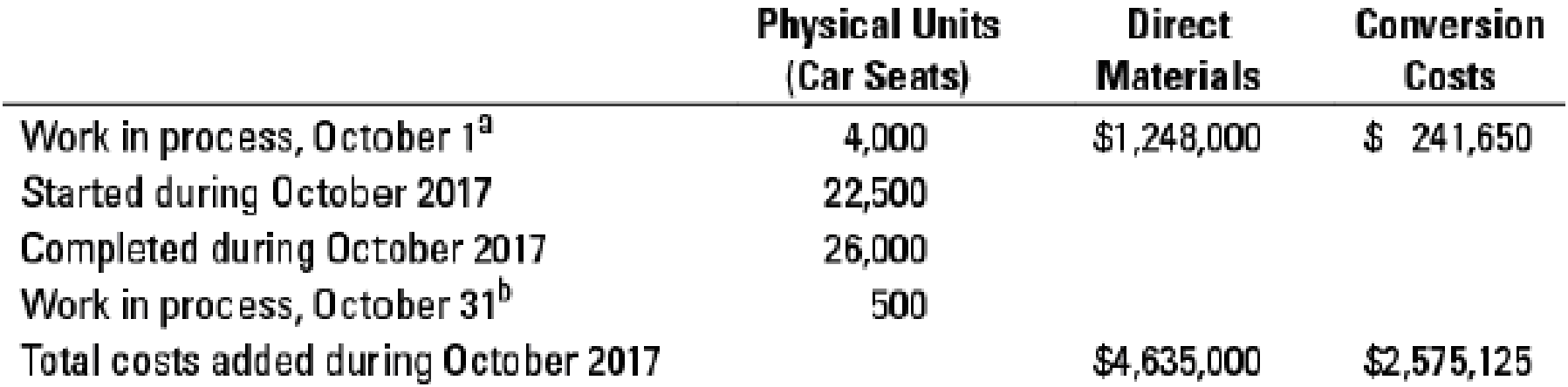

17-36 Weighted-average method. Hoffman Company manufactures car seats in its Boise plant. Each car seat passes through the assembly department and the testing department. This problem focuses on the assembly department. The process-costing system at Hoffman Company has a single direct-cost category (direct materials) and a single indirect-cost category (conversion costs). Direct materials are added at the beginning of the process. Conversion costs are added evenly during the process. When the assembly department finishes work on each car seat, it is immediately transferred to testing.

Hoffman Company uses the weighted-average method of process costing. Data for the assembly department for October 2017 are as follows:

a Degree of completion: direct materials, ?%; conversion costs, 45%.

b Degree of completion: direct materials, ?%; conversion costs, 65%.

- 1. For each cost category, compute equivalent units in the assembly department. Show physical units in the first column of your schedule.

Required

- 2. What issues should the manager focus on when reviewing the equivalent-unit calculations?

- 3. For each cost category, summarize total assembly department costs for October 2017 and calculate the cost per equivalent unit.

- 4. Assign costs to units completed and transferred out and to units in ending work in process.

Learn your wayIncludes step-by-step video

Chapter 17 Solutions

Horngren's Cost Accounting: A Managerial Emphasis (16th Edition)

Additional Business Textbook Solutions

Financial Accounting (11th Edition)

Horngren's Accounting (11th Edition)

Financial Accounting, Student Value Edition (4th Edition)

Principles of Accounting Volume 2

Intermediate Accounting (2nd Edition)

Horngren's Financial & Managerial Accounting, The Managerial Chapters (6th Edition)

- Friedman Company uses JIT manufacturing. There are several manufacturing cells set up within one of its factories. One of the cells makes stands for flat-screen televisions. The cost of production for the month of April is given below. During May, 30,000 stands were produced and sold. Required: 1. Explain why process costing can be used for computing the cost of production for the stands. 2. Calculate the cost per unit for a stand. 3. Explain how activity-based costing can be used to determine the overhead assigned to the cell.arrow_forwardThe current cost accounting system charges overhead to products based on machine-hours. What unit product costs will be reported for the two products if the current cost system continues to be used? (Round intermediate calculations and "Per unit cost" answers to 2 decimal places.) 308 510 Total cost Per unit cost A consulting firm has recommended using an activity-based costing system, with the activities based on the cost pools identified by the cost accountant. What are the cost driver rates for the four cost pools identified by the cost accountant? (Round your answers to 2 decimal places.) Incoming inspection % of material dollars Production per machine-hour Machine setup per setup Shipping per unit What unit product costs will be reported for the two products if the ABC system suggested by the cost accountant’s classification of…arrow_forwardSubject: Cost Accounting Give what is required of the problem. What is the answer to numbers 1, 2, 3 and 4?arrow_forward

- Using the information calculate the following,1. The manufacturing costs per unit and the total manufacturing costs, if all the overhead costs are absorbed on a machine hour basis.2. The overheads costs per unit using the ABC systemarrow_forwardPlease answer allarrow_forwardplease give answer step by steparrow_forward

- Anita Corporation Berhad uses the following activity rates from its activity-based costing to assign overhead costs to products. Activity Cost Pools Activity Rate (USD) Setting up batches 86.50 per batch Assembling products 4.63 per assembly hour Processing customer orders 52.16 per customer order Data concerning two products appear below: Product JJ Product SS Number of batches 34 43 Number of assembly hours 105 812 Number of customer orders 17 32 How much overhead cost would be assigned to Product JJ using the company's activity-based costing system? How much overhead cost would be assigned to Product SS using the company's activity-based costing system?arrow_forwardDoles Corporation uses the following activity rates from its activity-based costing to assign overhead costs to products. Activity Cost Pools Setting up batches Processing customer orders Assembling products Activity Rate Number of batches Number of customer orders Number of assembly hours Required: $66.52 per batch $23.58 per customer order $10.71 per assembly hour Data concerning two products appear below: Product K52W Product X94T 65 45 418 How much overhead cost would be assigned to each of the two products using the company's activity-based costing system? Product K52W Total overhead cost: ? 52 30 161 Product X94T ?arrow_forward1. Calculate the overhead rate based on the traditional overhead allocation method using direct labour hours as the base. 2. Calculate the total overhead applied to order no. 147 using the traditional overhead rate calculated in question 3.1 above. 3. Using activity based costing (ABC), calculate the overhead rate for the following activity: Purchasing. That is, what is the overhead rate per purchase order?arrow_forward

- Desjariais Corporation uses the following activity rates from its activity-based costing to assign overhead costs to products. Activity Coat Pools Setting up batches Assembling products Processing customer orders. Data concerning two products appear below: Number of batches Number of assembly hours. Number of customer orders a. Product S96U b. Product QO6F Overhead cost Activity Rate $ 123.70 per batch $ 7.32 per assembly hour $ 59.76 per customer order Product S960 36 192 23 Required: a. How much overhead cost would be assigned to Product S96U using the company's activity-based costing system? b. How much overhead cost would be assigned to Product Q06F using the company's activity-based costing system? Note: Do not round intermediate calculations. Round your final answers to 2 decimal places. Product 006F 45 870 42arrow_forwardWhat are the Costs per unit of Alfa and Beta under traditional and ABC costing systems? What would be the prices of Alpha and Beta traditional and ABC costing systems? Compare the costs and prices calculated in the two systems. Please write down the calculation process!thanks!!!arrow_forwardHoffman Company manufactures car seats in its Boise plant. Each car seat passes through the assembly department and the testing department. This problem focuses on the assembly department. (Click the icon to view information about Hoffman Company's process-costing system.) Data for the assembly department for October 2017 are as follows: 2(Click the icon to view the assembly department data.) 3(Click the icon to view the total costs to account for.) *(Click the icon to view the total costs accounted for.) 1 Read the requirement. Prepare a set of summarized journal entries for all October 2017 transactions affecting Work in Process-Assembly. (Record debits first, then credits. Exclude explanations from any journal entries.) Begin by recording the purchase and use of direct materials. Journal Entry Accounts Debit Credit JE 1 (1) (2) (3) (4) Record the conversion costs. Journal Entry Accounts Debit Credit JE 2 (5) (6) (7) (8) Prepare a journal entry to transfer out the cost of goods…arrow_forward

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning