Videos

a.

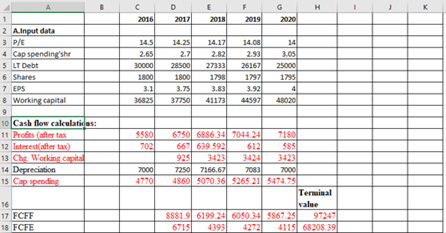

To calculate:The intrinsic value when GE’s P/E ratio starting in 2020 will be 16.

Introduction:

Unlevered Beta: This is also called as asset beta. It is one of the risk measurement unit which is used to compare the risk of company that doesnot have any debts with that of risk of the markets. In other words, risk of the company without dedts and risk of the market is compared.

a.

Answer to Problem 16PS

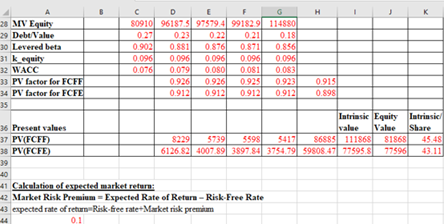

The intrinsic value when P/E ratio in the year 2020 is 16 will be $111868 and of FCFE will be $77595.80.

Explanation of Solution

Given information:

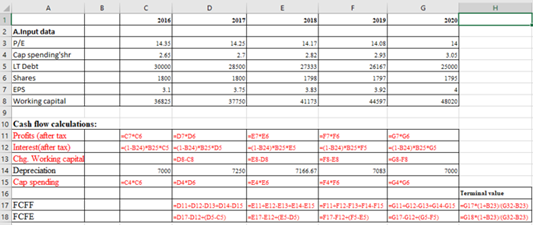

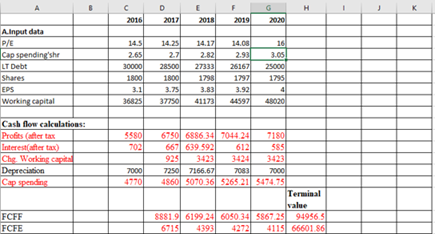

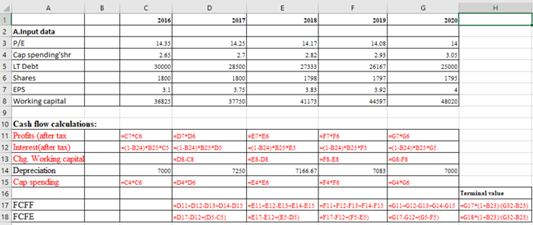

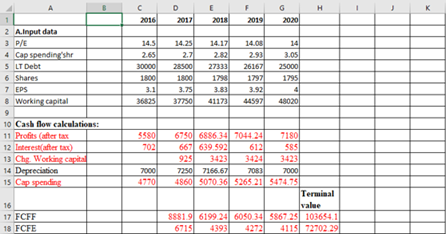

Spreadsheet 18.2 −

| 2016 | 2017 | 2018 | 2019 | 2020 | ||

| A.Input data | ||||||

| P/E | 14.35 | 14.25 | 14.17 | 14.08 | 14 | |

| Cap spending'shr | 2.65 | 2.7 | 2.82 | 2.93 | 3.05 | |

| LT Debt | 30000 | 28500 | 27333 | 26167 | 25000 | |

| Shares | 1800 | 1800 | 1798 | 1797 | 1795 | |

| EPS | 3.1 | 3.75 | 3.83 | 3.92 | 4 | |

| Working capital | 36825 | 37750 | 41173 | 44597 | 48020 | |

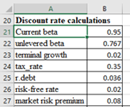

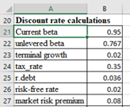

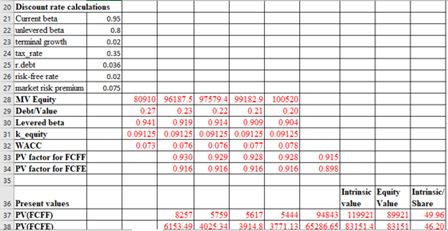

| Discount rate calculations | ||||||

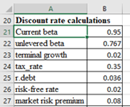

| Current beta | 0.95 | |||||

| unlevered beta | 0.767 | |||||

| terminal growth | 0.02 | |||||

| tax_rate | 0.35 | |||||

| r.debt | 0.036 | |||||

| risk-free rate | 0.02 | |||||

| market risk premium | 0.08 |

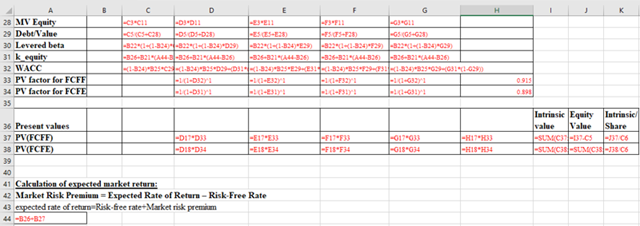

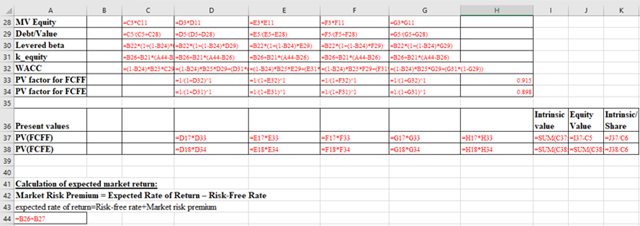

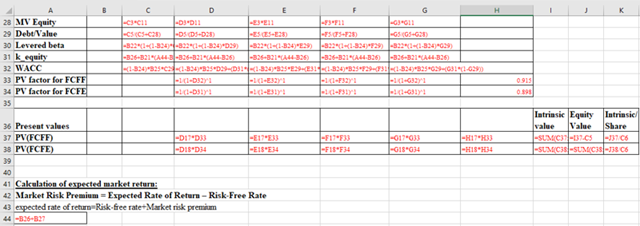

The formulas to be entered in the cells are as follows:

After inputing the required value in the cell related to G3, we get the following values.

Therefore the intrinsic value when P/E ratio in the year 2020 is 16 will be $111868 and of FCFE will be $77595.80

b.

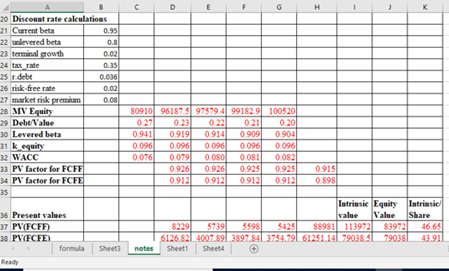

To calculate: The intrinsic value when GE’s unlevered beta is 0.80.

Introduction:

Unlevered Beta: This is also called as asset beta. It is one of the risk measurement unit which is used to compare the risk of company that doesnot have any debts with that of risk of the markets. In other words, risk of the company without dedts and risk of the market is compared.

b.

Answer to Problem 16PS

The intrinsic value of FCFF is $113972 and FCFE is $79038.50.

Explanation of Solution

Given information:

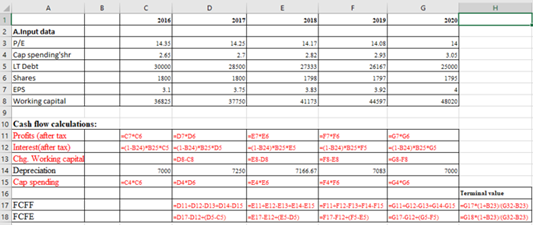

Spreadsheet 18.2 − Free cash flow model

| 2016 | 2017 | 2018 | 2019 | 2020 | ||

| A.Input data | ||||||

| P/E | 14.35 | 14.25 | 14.17 | 14.08 | 14 | |

| Cap spending'shr | 2.65 | 2.7 | 2.82 | 2.93 | 3.05 | |

| LT Debt | 30000 | 28500 | 27333 | 26167 | 25000 | |

| Shares | 1800 | 1800 | 1798 | 1797 | 1795 | |

| EPS | 3.1 | 3.75 | 3.83 | 3.92 | 4 | |

| Working capital | 36825 | 37750 | 41173 | 44597 | 48020 | |

| Discount rate calculations | ||||||

| Current beta | 0.95 | |||||

| unlevered beta | 0.767 | |||||

| terminal growth | 0.02 | |||||

| tax_rate | 0.35 | |||||

| r.debt | 0.036 | |||||

| risk-free rate | 0.02 | |||||

| market risk premium | 0.08 |

The formulas to be entered in the cells are as follows:

We need to change the vaue of unlevered beta from 0.767 to 0.80. After inputing the required value in the cell related to B22, we get the following values.

Therefore, the intrinsic value of FCFF is $113972 and FCFE is $79038.50.

c.

To calculate: Intrinsic value when the market risk premium is 7.5%

Introduction:

Unlevered Beta: This is also called as asset beta. It is one of the risk measurement unit which is used to compare the risk of company that doesnot have any debts with that of risk of the markets. In other words, risk of the company without dedts and risk of the market is compared.

c.

Answer to Problem 16PS

The intrinsic value of FCFF will be$ 119921 and for FCFE it will be $83151.40.

Explanation of Solution

Given information:

Spreadsheet 18.2 − Free cash flow model

| 2016 | 2017 | 2018 | 2019 | 2020 | ||

| A.Input data | ||||||

| P/E | 14.35 | 14.25 | 14.17 | 14.08 | 14 | |

| Cap spending'shr | 2.65 | 2.7 | 2.82 | 2.93 | 3.05 | |

| LT Debt | 30000 | 28500 | 27333 | 26167 | 25000 | |

| Shares | 1800 | 1800 | 1798 | 1797 | 1795 | |

| EPS | 3.1 | 3.75 | 3.83 | 3.92 | 4 | |

| Working capital | 36825 | 37750 | 41173 | 44597 | 48020 | |

| Discount rate calculations | ||||||

| Current beta | 0.95 | |||||

| unlevered beta | 0.767 | |||||

| terminal growth | 0.02 | |||||

| tax_rate | 0.35 | |||||

| r.debt | 0.036 | |||||

| risk-free rate | 0.02 | |||||

| market risk premium | 0.08 |

The formulas to be entered in the cells are as follows:

We need to change the vaue of unlevered beta from 0.08 to 0.075. After inputing the required value in the cell related to B27, we get the following values.

Therefore the intrinsic value of FCFE will be$ 119921 and for FCFE it will be $83151.40.

Want to see more full solutions like this?

Chapter 18 Solutions

INVESTMENTS-LOOSELEAF

- An analyst has modeled the stock of a company using the Fama-French three-factor model. The market return is 10%, the return on the SMB portfolio (rSMB) is 3.2%, and the return on the HML portfolio (rHML) is 4.8%. If ai = 0, bi = 1.2, ci = 20.4, and di = 1.3, what is the stock’s predicted return?arrow_forwardAssume that you’ve just inherited $500,000 and have decided to invest a big chunk of it ($350,000, to be exact) in common stocks. Your objective is to build up as much capital as you can over the next 15 to 20 years, and you’re willing to tolerate a “good deal’’ of risk. What types of stocks (blue chips, income stocks, and so on) do you think you’d be most interested in, and why? Select at least three types of stocks and briefly explain the rationale for selecting each. Would your selections change if you were dealing with a smaller amount of money—say, only $50,000? What if you were a more risk-averse investor?arrow_forwardMarket equity beta measures the covariability of a firms returns with all shares traded on the market (in excess of the risk-free interest rate). We refer to the degree of covariability as systematic risk. The market prices securities so that the expected returns should compensate the investor for the systematic risk of a particular stock. Stocks carrying a market equity beta of 1.20 should generate a higher return than stocks carrying a market equity beta of 0.90. Nonsystematic risk is any source of risk that does not affect the covariability of a firms returns with the market. Some writers refer to nonsystematic risk as firm-specific risk. Why is the characterization of nonsystematic risk as firm-specific risk a misnomer?arrow_forward

- Calculate the required rate of return for the Wagner Assets Management Group, which holds 4 stocks. The market's required rate of return is 17.0%, the risk-free rate is 7.0%, and the Fund's assets are as follows: Stock Investment Beta A $200,000 1.50 B 300,000 −0.50 C 500,000 1.25 D 1,000,000 0.75 Select the correct answerarrow_forwardPART A,B and C are completed. need help in D and E. TIA Unique vs. Market Risk. The figure below shows plots of monthly rates of return on three stocks versus the stock market index. The beta and standard deviation of each stock is given besides its plot. A. Which stock is riskiest to a diversified investor? B. Which stock is riskiest to an undiversified investor who puts all her funds in one of these stocks? C. Consider a portfolio with equal investments in each stock. What would this portfolio’s beta have been? D. Consider a well-diversified portfolio made up of stocks with the same beta as Exxon. What are the beta and standard deviation of this portfolio’s return? The standard deviation of the market portfolio’s return is 20 percent. E. What is the expected rate of return on each stock? Use the capital asset pricing model with a market risk premium of 8 percent. The risk-free rate of interest is 4 percent.arrow_forwardThe following graph plots the current security market line (SML) and indicates the return that investors require from holding stock from Happy Corp. (HC). Based on the graph, complete the table that follows: 00.51.01.52.020.016.012.08.04.00REQUIRED RATE OF RETURN (Percent)RISK (Beta)Return on HC's Stock CAPM Elements Value Risk-free rate (rRFrRF) Market risk premium (RPMRPM) Happy Corp. stock’s beta Required rate of return on Happy Corp. stock An analyst believes that inflation is going to increase by 2.0% over the next year, while the market risk premium will be unchanged. The analyst uses the Capital Asset Pricing Model (CAPM). The following graph plots the current SML. Calculate Happy Corp.’s new required return. Then, on the graph, use the green points (rectangle symbols) to plot the new SML suggested by this analyst’s prediction. Happy Corp.’s new required rate of return is . Tool tip: Mouse over the points on…arrow_forward

- The financial controller is considering the use of the Capital Asset Pricing Model as a surrogate discount factor. The risk-free rate is 5 percent. The information in the table below has been used by company management in calculating the stock beta value which is 1.151and the expected return on the stock which is 12.5%.Year Stock Market Index share Price2011 2000 $15.002012 2400 $25.002013 2900 $33.002014 3500 $40.002015 4200 $45.002016 5000 $55.002017 5900 $62.002018 6000 $68.002019 6100 $74.002020 6200 $80.002021 6300 $83.33e) Calculate the CAPMf) Explain why this figure may differ from that calculated…arrow_forward5 ABL shares are currently trading at a price of $30, while HHT shares are trading at a price of $37.98. The risk-free rate is 1.24% per year. Using the information above, perform each of the following tasks: c) Compute the Delta (number of shares) that if you also short a call on HHT will create a risk-free portfolio. Assume the call is European and that the strike-price is $34.7517 d) Using the information above, compute the risk-neutral probability of HHT shares increasing 10% if the time-step to the next node is 1 year. f) Find the Black-Scholes price of the call on ABL with a strike price of $29.19 if there is 6 months until the call expires and the annual standard deviation of the stock price is 20%.arrow_forwardThe Angelina Corporation’s common stock has a beta of 1.6. If the risk-free rate is 4.7 percent and the expected return on the market is 13 percent, what is the company’s cost of equity capital? (Do not round intermediate calculations and enter your answer as a percent rounded to 2 decimal places, e.g., 32.16.) Cost of equity capital: _______?arrow_forward

- Express Steel Corporation wishes to calculate its cost of common stock equity, by using the capital asset pricing model (CAPM). The firm’s investment advisors and its own analysts indicate that the risk-free rate equals 9,1%; the firm’s beta equals 0,75; and the market return equals 16%. Please estimate the cost of common stock equity by using CAPM.arrow_forwardYou are facing three stock investment alternatives, Stock A, Stock B and Stock C. Given the following information, please indicate which stock is (are) overvalued, which stock is (are) undervalued, and which stock is (are) correctly priced based on the required returns calculation using the Capital Asset Pricing Model (CAPM or Security Market Line=SML). The risk free rate is 3% and the risk premium for the market index return is 5%. Please Show Work Expected Stocks Returns BETA A 14% 1.2 B 8% 0.67 C 20% 2.5arrow_forwardYour broker has recommended that you purchase stock in Alacan, Inc. She estimates that the 1-year target price is $76.00, and Alacan consistently pays an annual dividend of $17.00. Analysts estimate that the stock has a beta of 0.91. The current risk-free rate is 2.70% and the market risk premium (RM - RF) is 9.50%. Assuming that CAPM holds, what is the intrinsic value of this stock?arrow_forward

EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT

EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning

Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning Pfin (with Mindtap, 1 Term Printed Access Card) (...FinanceISBN:9780357033609Author:Randall Billingsley, Lawrence J. Gitman, Michael D. JoehnkPublisher:Cengage Learning

Pfin (with Mindtap, 1 Term Printed Access Card) (...FinanceISBN:9780357033609Author:Randall Billingsley, Lawrence J. Gitman, Michael D. JoehnkPublisher:Cengage Learning Financial Reporting, Financial Statement Analysis...FinanceISBN:9781285190907Author:James M. Wahlen, Stephen P. Baginski, Mark BradshawPublisher:Cengage Learning

Financial Reporting, Financial Statement Analysis...FinanceISBN:9781285190907Author:James M. Wahlen, Stephen P. Baginski, Mark BradshawPublisher:Cengage Learning