Intermediate Accounting

9th Edition

ISBN: 9781259722660

Author: J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher: McGraw-Hill Education

expand_more

expand_more

format_list_bulleted

Concept explainers

Videos

Textbook Question

Chapter 19, Problem 19.10P

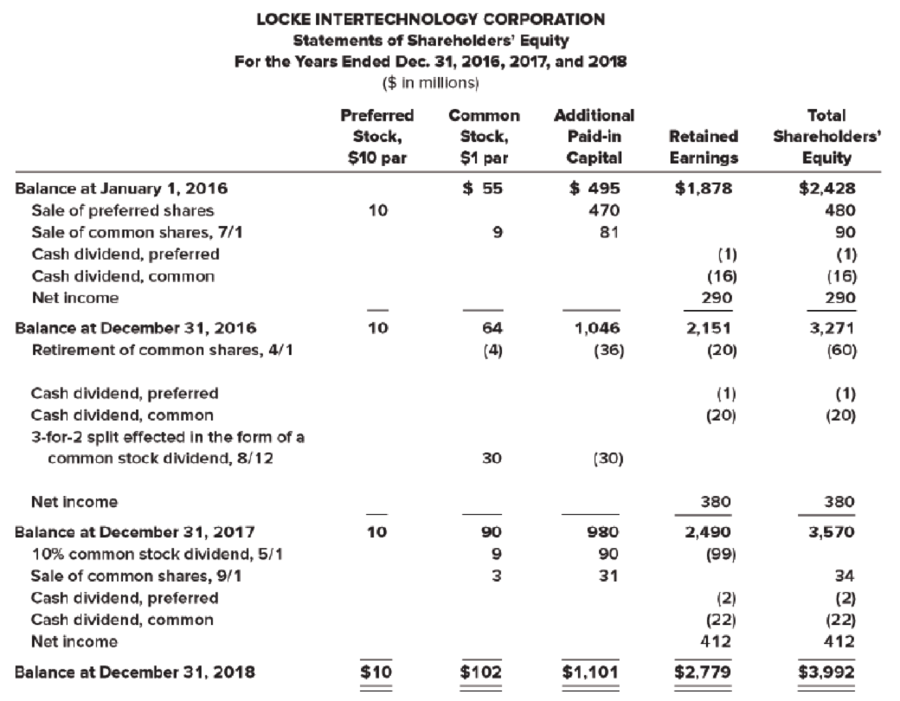

EPS from statement of shareholders’ equity

• LO19–4 through LO19–6

Comparative Statements of Shareholders’ Equity for Locke Intertechnology Corporation were reported as follows for the fiscal years ending December 31, 2016, 2017, and 2018.

Required:

Infer from the statements the events and transactions that affected Locke Intertechnology Corporation’s shareholders’ equity and compute earnings per share as it would have appeared on the income statements for the years ended December 31, 2016, 2017, and 2018. No potential common shares were outstanding during any of the periods shown.

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Students have asked these similar questions

Question 68

Using Financial Statements for 2018-2019. Net book value per share of common stock for 2019 is $17.46.

N4

Refer to the Real Life Case of Chapter 19. Use financial statements (page 51) of Microsoft's 10-K for the fiscal year ended June 30 , 2019 (Source: SEC Edgar). The basic EPS of Microsoft for year 2019 is

$5.11

, weighted average shares outstanding is 7,673 million shares, and share price is

$134

. If the company had pre-announced and used all funds in its share repurchase program of

$40

billion on June 30 , 2019, what would Microsoft's basic EPS have been for fiscal year 2019? a.

$3.29

b.

$5.06

c.

$2.13

d.

$5.32

e.

$5.11

Question 80

Using Financial Statements for 2018-2019. Net book value per share of common stock for 2018 is $18.46.

TRUE OR FALSE?

Chapter 19 Solutions

Intermediate Accounting

Ch. 19 - Prob. 19.1QCh. 19 - Prob. 19.2QCh. 19 - The Tax Code differentiates between qualified...Ch. 19 - Stock option (and other share-based) plans often...Ch. 19 - What is a simple capital structure? How is EPS...Ch. 19 - Prob. 19.6QCh. 19 - Blake Distributors had 100,000 common shares...Ch. 19 - Why are preferred dividends deducted from net...Ch. 19 - Prob. 19.9QCh. 19 - The treasury stock method is used to incorporate...

Ch. 19 - The potentially dilutive effect of convertible...Ch. 19 - How is the potentially dilutive effect of...Ch. 19 - Prob. 19.13QCh. 19 - If stock options and restricted stock are...Ch. 19 - Wiseman Electronics has an agreement with certain...Ch. 19 - Prob. 19.16QCh. 19 - When the income statement includes discontinued...Ch. 19 - Prob. 19.18QCh. 19 - Prob. 19.19QCh. 19 - (Based on Appendix B) LTV Corporation grants SARs...Ch. 19 - Prob. 19.1BECh. 19 - Prob. 19.2BECh. 19 - Stock options LO192 Under its executive stock...Ch. 19 - Prob. 19.4BECh. 19 - Prob. 19.5BECh. 19 - Prob. 19.6BECh. 19 - Prob. 19.7BECh. 19 - Prob. 19.8BECh. 19 - Prob. 19.9BECh. 19 - Performance-based options LO192 Refer to the...Ch. 19 - Prob. 19.11BECh. 19 - Prob. 19.12BECh. 19 - EPS; nonconvertible preferred shares LO197 At...Ch. 19 - Prob. 19.14BECh. 19 - Prob. 19.15BECh. 19 - Prob. 19.16BECh. 19 - Prob. 19.1ECh. 19 - Prob. 19.2ECh. 19 - Prob. 19.3ECh. 19 - Prob. 19.4ECh. 19 - Prob. 19.5ECh. 19 - Prob. 19.6ECh. 19 - Prob. 19.7ECh. 19 - Prob. 19.8ECh. 19 - Prob. 19.9ECh. 19 - Prob. 19.10ECh. 19 - Prob. 19.11ECh. 19 - EPS; shares issued; stock dividend LO195, LO196...Ch. 19 - Prob. 19.13ECh. 19 - EPS; stock dividend; nonconvertible preferred...Ch. 19 - EPS; net loss; nonconvertible preferred stock;...Ch. 19 - EPS; stock dividend; nonconvertible preferred...Ch. 19 - Prob. 19.17ECh. 19 - EPS; stock dividend; nonconvertible preferred...Ch. 19 - EPS; stock dividend; nonconvertible preferred...Ch. 19 - EPS; shares issued; stock options LO196 through...Ch. 19 - EPS; convertible preferred stock; convertible...Ch. 19 - Prob. 19.22ECh. 19 - Prob. 19.23ECh. 19 - Prob. 19.24ECh. 19 - Prob. 19.25ECh. 19 - EPS; concepts; terminology LO195 through LO1913...Ch. 19 - FASB codification research LO192 The FASB...Ch. 19 - Prob. 19.28ECh. 19 - Prob. 19.29ECh. 19 - Prob. 19.30ECh. 19 - Restricted stock units; cash settlement Appendix...Ch. 19 - Stock options; forfeiture; exercise LO192 On...Ch. 19 - Stock options; graded vesting LO192 January 1,...Ch. 19 - Stock options; graded vesting; measurement using a...Ch. 19 - Stock options; graded vesting; IFRS LO192, LO1914...Ch. 19 - Prob. 19.5PCh. 19 - Prob. 19.6PCh. 19 - Prob. 19.7PCh. 19 - Prob. 19.8PCh. 19 - EPS from statement of retained earnings LO194...Ch. 19 - EPS from statement of shareholders equity LO194...Ch. 19 - EPS; non convertible preferred stock; treasury...Ch. 19 - EPS; non convertible preferred stock; treasury...Ch. 19 - EPS; non convertible preferred stock; treasury...Ch. 19 - EPS; convertible preferred stock; convertible...Ch. 19 - EPS; antidilution LO194 through LO1910, LO1913...Ch. 19 - EPS; convertible bonds; treasury shares LO194...Ch. 19 - Prob. 19.17PCh. 19 - Prob. 19.18PCh. 19 - EPS; options; restricted stock; additional...Ch. 19 - Prob. 19.1BYPCh. 19 - Communication Case 192 Stock options; basic...Ch. 19 - Prob. 19.3BYPCh. 19 - Real World Case 195 Share-based plans; Walmart ...Ch. 19 - Prob. 19.6BYPCh. 19 - Prob. 19.7BYPCh. 19 - Analysis Case 198 EPS concepts LO194 through...Ch. 19 - Prob. 19.9BYPCh. 19 - Prob. 19.10BYPCh. 19 - Communication Case 1911 Dilution LO199 I thought...Ch. 19 - Real World Case 1912 Reporting EPS; discontinued...Ch. 19 - Analysis Case 1913 Analyzing financial statements;...Ch. 19 - Analysis Case 1915 Kelloggs EPS; PE ratio;...Ch. 19 - Prob. 19.16BYPCh. 19 - Prob. 1CCTCCh. 19 - Air FranceKLM Case IFRS LO199 Air FranceKLM (AF),...

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Statement of stockholders' equity The stockholders' equity T accounts of I-Cards Inc. for the fiscal year ended December 31, 20Y9, are as follows. Prepare a statement of stockholders' equity for the year ended December 31, 20Y9.arrow_forwardNineteen measures of solvency and profitability The comparative financial statements of Bettancort Inc. are as follows. The market price of Bettancort Inc. common stock was 71.25 on December 31, 2016. Bettancort Inc. Comparative Retained Earnings Statement For the Years Ended December 31, 2016 and 2015 2016 2015 Retained earnings. January 1......................................... 2,655,000 2,400,000 Add net income for year............................................. 300,000 280,000 Total............................................................... 2,955,000 2,680,000 Deduct dividends: On preferred stock................................................ 15,000 15,000 On common stock................................................. 10,000 10,000 Total........................................................... 25,000 25,000 Retained earnings. December 31..................................... 2,930,000 2,655,000 Bettancort Inc. Comparative Retained Earnings Statement For the Years Ended December 31, 2016 and 2015 2016 2015 Sales...................... 1,200,000 1,000,000 Cost of goods sold............ 500,000 475,000 Gross profit............... 700,000 525,000 Selling expenses.......... 240,000 200,000 Administrative expenses...... 180,000 150,000 Total operating expenses.. 420,000 350,000 Income from operations.. 280,000 175,000 Other income............. 166,000 225,000 446,000 400,000 Other expense (Interest)... 66,000 60,000 Income before income tax 380,000 340,000 Income tax expense....... 80,000 60,000 Net income............... 300,000 280,000 Bettancort Inc. Comparative Retained Earnings Statement For the Years Ended December 31, 2016 and 2015 Dec.31, 2016 Dec. 31, 2015 Assets Current Assets: Cash.................................... 450,000 400,000 Marketable securities.................... 300,000 260,000 Accounts receivable (net)................. 130,000 110,000 Inventories.............................. 67,000 58,000 Prepaid expenses........................ 153,000 139,000 Total current assets..................... 1,100,000 967,000 Long-term investments.................... 2,350,000 2,200,000 Property, plant and equipment (net)....... 1,320,000 1,118,000 Total assets............................... 4,770,000 4,355,000 Liabilities Current liabilities.......................... 440,000 400,000 Long-term liabilities: Mortgage note payable, 8.8%, due 2021... 100,000 0 Bonds payable, 9%, due 2017............. 1,000,000 1,000,000 Total long term liabilities............... 1,100,000 1,000,000 Total liabilities............................ 1,540,000 1,400,000 Stockholders' equity Preferred stock 0.90, 10 par.. 200,000 200,000 Common stock. 5 par..................... 100,000 100,000 Retained earnings......................... 2,930,000 2,665,000 Total stockholders equity............... 3,230,000 2,955,000 Total liabilities and stockholders' equity..... 4,770,000 4,355,000 Instructions Determine the following measures for 2016, rounding to one decimal place: 1. Working capital 2. Current ratio 3. Quick ratio 4. Accounts receivable turnover 5. Number of days' sales in receivables 6. Inventory turnover 7. Number of days' sales in inventory 8. Ratio of fixed assets to long-term liabilities 9. Ratio of liabilities to stockholders equity 10. Number of times interest charges are earned 11. Number of times preferred dividends are earned 12. Ratio of sales to assets 13. Rate earned on total assets 14. Rate earned on stockholders' equity 15. Rate earned on common stockholders' equity 16. Earnings per share on common stock 17. Price-earnings ratio 18. Dividends per share of common stock 19. Dividend yieldarrow_forwardMeasures of liquidity, solvency, and profitability The comparative financial statements of Marshall Inc. are as follows. The market price of Marshall common stock was 82.60 on December 31, 20Y2. Marshall Inc. Comparative Retained Earnings Statement For the Years Ended December 31,20Y2 and 20Y1 20Y2 20Y1 Retained earnings, January 1 3,704,000 3,264,000 Net income 600,000 550,000 Total 4,304,000 3,814,000 Dividends: On preferred stock 10,000 10,000 On common stock 100,000 100,000 Total dividends 110,000 110,000 Retained earnings, December 31 4,194,000 3,704,000 Sales 10,850,000 10,000,000 Cost of goods sold 6,000,000 5,450,000 Gross profit 4,850,000 4,550,000 Selling expenses 2,170,000 2,000,000 Administrative expenses 1,627,500 1,500,000 Total operating expenses 3,797,500 3,500,000 Income from operations 1,052,500 1,050,000 Other income 99,500 20,000 1,152,000 1,070,000 Other expense (interest) 132,000 120,000 Income before income tax 1,020,000 950,000 Income tax expense 420,000 400,000 Net income 600,000 550,000 Marshall Inc. Comparative Balance Sheet December 31,20Y2 and 20Y1 20Y2 20Y1 Assets Current assets: Cash 1,050,000 950,000 Marketable securities 301,000 420,000 Accounts receivable (net) 585,000 500,000 Inventories 420,000 380,000 Prepaid expenses 108,000 20,000 Total current assets 2,464,000 2,270,000 Long-term investments 800,000 800,000 Property, plant, and equipment (net) 5,760,000 5,184,000 Total assets 9,024,000 8,254,000 Liabilities Current liabilities 880,000 800,000 Long-term liabilities: Mortgage note payable. 6% 200,000 0 Bonds payable. 4%, 3,000,000 3,000,000 Total long term liabilities 3,200,000 3,000,000 Total liabilities 4,080,000 3,800,000 Stockholders' Equity Preferred 4% stock, 5 par 250,000 250,000 Common stock. 5 par 500,000 500,000 Retained earnings 4,194,000 3,704,000 Total stockholders' equity 4,944,000 4,454,000 Total liabilities and stockholders' equity 9,024,000 8,254,000 Instructions Determine the following measures for 20Y2 (round to one decimal place, including percentages, except for per-share amounts): 1. Working capital 2. Current ratio 3. Quick ratio 4. Accounts receivable turnover 5. Number of days' sales in receivables 6. Inventory turnover 7. Number of days' sales in inventory 8. Ratio of fixed assets to long-term liabilities 9. Ratio of liabilities to stockholders' equity 10. Times interest earned 11. Asset turnover 12. Return on total assets 13. Return on stockholders' equity 14. Return on common stockholders' equity 15. Earnings per share on common stock 16. Price-earnings ratio 17. Dividends per share of common stock 18. Dividend yieldarrow_forward

- Statement of stockholders equity The stockholders equity T accounts of I-Cards Inc. for the fiscal year ended December 31, 2016, are as follows. Prepare a statement of stockholders equity for the fiscal year ended December 31, 2016.arrow_forwardQuestion 67 Using Financial Statements for 2018-2019. The amount of shares of common stock for 2019 is 307,082. TRUE OR FALSE?arrow_forwardChapter 11 Comprehensive Problem – CP11-11 The following note appeared on the balance sheet of Sabre Rigging Limited: As of December 31, 2019, dividends on the cumulative preferred stock were in arrears for three years to the extent of $15 per stock or $15,000 in total. Required: 1.Does the amount of the arrears appears as a liability on the December31, 2019 balance sheet? Explain your answer. Why might the dividends be in arrears? The comptroller of Sabre Rigging projects net income for the2020 fiscal year of $35,000. When the company last paid dividends, the directors allocated 50 per cent of current year’s net income for dividends. If dividends on shares of preferred stock are resumed at the end of 2020 and the established policy of 50 per cent is continued, how much will be available for dividends to the common stockholders if the profit projection is realized?arrow_forward

- Q21 Significant influence is normally presumed to exist if the investor owns at least a certain percentage of the investee company's ordinary shares. This percentage is_____. Select one: a. 10% b. 51% c. 20% d. 50%arrow_forwardProblem 6 (Adapted)Anna company presented the following account balances in the shareholders’ equity section for the year ended December 31, 2018: Preference share capital, 12% P50 par, P3,000,000, Ordinary share capital, P100 par, P6,000,000 and deficit, (P1,350,000). No dividends have been paid on the preference share since 2016. Determine the book value per share under the following conditions:a. Preference share is preferred as to assetsb. Preference share is preferred as to dividendarrow_forwardRequirements: 10. How much is the consolidated liabilities on December 31, 2x19?11. How much is the consolidated stockholder’s equity on December 31, 2x19?arrow_forward

- Requirements:10. How much is the consolidated liabilities on December 31, 2x19?11. How much is the consolidated stockholder’s equity on December 31, 2x19?arrow_forwardQuestion 39 Company X ows 10,000,000 shares of voting common stock of a foreign entity that it accounts for using the equity method of accounting. The 10,000,0000 shares constitute 40% of the oustanding shares of voting common stock of the foreign entity. The foreign entity has its own functional currency, which is differenet than Company X's reporting currency.. The cumulative translation adjustment as of December 31, 2020 in Company X's consolidated financial statements relating ot this investee is $ 1.5 million debit balance. Subequent to year-end, Company X sells 2,000,000 of the shares held in this foreign entity to outside investors. As a result of this transaction, Company X now owns 32% of the foreign entity's' voting common stock and continues to apply the equity method. What is the impact of this sale transaction on Company X's cumulative translation adjustment account? There is no impact $480,000 debit $480,000 credit $300,000…arrow_forwardQ 30 Question 30 An unrealized loss on available-for-sale securities is … Select one: a. reported under Other Expenses and Losses in the income statement. b. deducted from the cost of the investment. c. reported as a separate component of stockholders equity. d. closed-out at the end of the accounting period.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Accounting (Text Only)AccountingISBN:9781285743615Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Accounting (Text Only)AccountingISBN:9781285743615Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Corporate Financial AccountingAccountingISBN:9781337398169Author:Carl Warren, Jeff JonesPublisher:Cengage Learning

Corporate Financial AccountingAccountingISBN:9781337398169Author:Carl Warren, Jeff JonesPublisher:Cengage Learning Corporate Financial AccountingAccountingISBN:9781305653535Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Corporate Financial AccountingAccountingISBN:9781305653535Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Financial & Managerial AccountingAccountingISBN:9781337119207Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial & Managerial AccountingAccountingISBN:9781337119207Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Financial & Managerial AccountingAccountingISBN:9781285866307Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial & Managerial AccountingAccountingISBN:9781285866307Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Accounting (Text Only)

Accounting

ISBN:9781285743615

Author:Carl Warren, James M. Reeve, Jonathan Duchac

Publisher:Cengage Learning

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Corporate Financial Accounting

Accounting

ISBN:9781337398169

Author:Carl Warren, Jeff Jones

Publisher:Cengage Learning

Corporate Financial Accounting

Accounting

ISBN:9781305653535

Author:Carl Warren, James M. Reeve, Jonathan Duchac

Publisher:Cengage Learning

Financial & Managerial Accounting

Accounting

ISBN:9781337119207

Author:Carl Warren, James M. Reeve, Jonathan Duchac

Publisher:Cengage Learning

Financial & Managerial Accounting

Accounting

ISBN:9781285866307

Author:Carl Warren, James M. Reeve, Jonathan Duchac

Publisher:Cengage Learning

The KEY to Understanding Financial Statements; Author: Accounting Stuff;https://www.youtube.com/watch?v=_F6a0ddbjtI;License: Standard Youtube License