Concept explainers

Videos

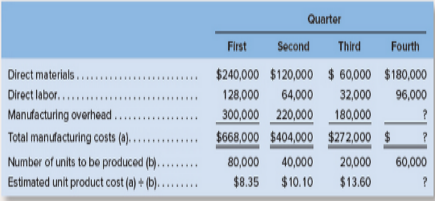

Varying Plantwide Predetermined Overhead Rates

Kingsport Containers Company makes a single product that is subject to wide seasonal variations in demand. The company uses a job-ordercosting system and computes pIantwide predeterminedoverhead rates on a quarterly basis using the number of units to be produced as theallocation base. Its estimated costs, by quarter, for the coming year are given below:

Management finds the variation in quarterly unit product costs to be confusing and difficult to work with.It has been suggested that theproblem lies with manufacturing overhead because it is the largest element of total

Required:

1. Assuming the estimated variable manufacturing overhead cost per unit is $2.00, what must be the estimated total fixed manufacturing overhead cost per quarter?

2. Assuming the assumptions about cost behavior from the first three quarters hold constant what is the estimated unit product cost for thefourth quarter?

3. 1iat is causing the estimated unit product cost to fluctuate from one quarter to the next?

4. How would you recommend stabilizing the company’s unit product cost? Support your answer with computations.

Want to see the full answer?

Check out a sample textbook solution

Chapter 2 Solutions

EBK INTRODUCTION TO MANAGERIAL ACCOUNTI

- Kingsport Containers Company makes a single product with wide seasonal variations in demand. The company uses a job-order costing system and computes plantwide predetermined overhead rates on a quarterly basis using the number of units to be produ as the allocation base. Its estimated costs, by quarter, for the coming year are given below: Direct materials Direct labor Manufacturing overhead Total manufacturing costs (a) Number of units to be produced (b) Estimated unit product cost (a) + (b) Quarter First $ 280,000 160,000 220,000 Second $ 140,000 80,000 196,000 $ 660,000 $ 416,000 120,000 $ 5.50 60,000 $ 6.93 Third $ 70,000 40,000 184,000 $ 294,000 30,000 $9.80 Fourth $ 210,000 120,000 ? $? 90,000 $? Management finds the variation in quarterly unit product costs to be confusing. Accordingly, you have been asked to find a more appropriate way of applying manufacturing overhead cost to units of product. Required: 1. Assuming the estimated variable manufacturing overhead cost per unit…arrow_forwardKingsport Containers Company makes a single product with wide seasonal variations in demand. The company uses a job-order costing system and computes plantwide predetermined overhead rates on a quarterly basis using the number of units to be produced as the allocation base. Its estimated costs, by quarter, for the coming year are given below: Direct materials Direct labor Manufacturing overhead Total manufacturing costs (a) Number of units to be produced (b) Estimated unit product cost (a) (b) First $ 240,000 80,000 230,000 $ 550,000 80,000 $6.88 Quarter Second $ 120,000 40,000 206,000 $366,000 40,000 $ 9.15 Third $ 60,000 20,000 194,000 $274,000 20,000 $ 13.70 Fourth $ 180,000 60,000 ? $ ? 60,000 $ ? Management finds the variation in quarterly unit product costs to be confusing. Accordingly, you have been asked to find a more appropriate way of applying manufacturing overhead cost to units of product. Required: 1. Assuming the estimated variable manufacturing overhead cost per unit is…arrow_forwardThe management of Garn Corporation would like to investigate the possibility of basing its predetermined overhead rate on activity at capacity rather than on the estimated activity for the coming year. The Corporation's controller has provided an example to illustrate how this new system would work. In this example, the allocation base is machine-hours and the estimated activity for the upcoming year is 59,400 machine-hours. Capacity is 78,400 machine-hours. All of the manufacturing overhead is fixed and is $3,136,000 per year within the range of 59,400 to 78,400 machine-hours. If the Corporation bases its predetermined overhead rate on capacity but the actual level of activity for the year turns out to be 59,900 machine-hours, the cost of unused capacity shown on the income statement prepared for internal management purposes would be closest to: Multiple Choice $26.177 $766,177 $740,000 $26,397arrow_forward

- wrong answer. from 1 to 4. Kingsport Containers Companymakes a single product with wide seasonal variations indemand. The company uses a job - order costing system andcomputes plantwide predetermined overhead rates on aquarterly basis using the number of units to be produced asthe allocation base. Its estimated costs, by quarter, for thecoming year are given below: Management finds thevariation in quarterly unit product costs to be confusing.Accordingly, you have been asked to find a more appropriateway of applying manufacturing overhead cost to units ofproduct. Required: Assuming the estimated variablemanufacturing overhead cost per unit is $0.40, what must bethe estimated total fixed manufacturing overhead cost perquarter? Assuming the assumptions about cost behavior from the first three quarters hold constant, what is the estimated unit product cost for the fourth quarter? What is causing the estimated unit product cost to fluctuate from one quarter to the next? Assuming the company…arrow_forwardThe management of Krach Corporation would like to investigate the possibility of basing its predetermined overhead rate on activity at capacity. The company's controller has provided an example to illustrate how this new system would work. In this example, the allocation base is machine-hours and the estimated amount of the allocation base for the upcoming year is 23,000 machine-hours. Capacity is 27,000 machine-hours and the actual level of activity for the year is assumed to be 13,500 machine-hours. All of the manufacturing overhead is fixed and both the estimated amount at the beginning of the year and the actual amount at the end of the year are assumed to be $78,300 per year. For simplicity, it is assumed that this is the estimated manufacturing overhead for the year as well as the manufacturing overhead at capacity. It is further assumed that this is also the actual amount of manufacturing overhead for the year. If the company bases its predetermined overhead rate on capacity,…arrow_forwardThe management of Garn Corporation would like to investigate the possibility of basing its predetermined overhead rate on activity at capacity rather than on the estimated activity for the coming year. The Corporation's controller has provided an example to illustrate how this new system would work. In this example, the allocation base is machine-hours and the estimated activity for the upcoming year is 69,000 machine-hours. Capacity is 85,000 machine-hours. AlIl of the manufacturing overhead is fixed and is $4,105,500 per year within the range of 69,000 to 85,000 machine-hours. If the Corporation bases its predetermined overhead rate on capacity but the actual level of activity for the year turns out to be 69,700 machine-hours, the cost of unused capacity shown on the income statement prepared for internal management purposes would be closest to: Multiple Choice $772,800 $780,640 $738,990 $41,650arrow_forward

- Cost Classification and Behaviour—Spark Electrical Company Spark Electrical Company manufactures electrical components. Plant management has experienced difficulties with fluctuating monthly overhead costs. Management wants to be able to estimate overhead costs to plan its operations and financial needs. A trade association publication reports that for companies manufacturing electrical components, overhead tends to vary with machine hours. Monthly data was gathered on machine hours and overhead costs for the past two years. There were no major changes in operations over this period of time. The raw data is: Month Number Machine Hours Overhead Costs ($) 1 20,000 84,000 2 25,000 99,000 3 22,000 89,500 4 23,000 90,000 5 20,000 81,500 6 19,000 75,500 7 14,000 70,500 8 10,000 64,500 9 12,000 69,000 10 17,000 75,000 11 16,000 71,500 12 19,000 78,000 13 21,000 86,000 14 24,000 93,000 15 23,000 93,000 16 22,000 87,000 17 20,000 80,000…arrow_forwardThe management of Hartman Company is trying to determine the amount of each of two products to produce over the coming planning period. The following information concerns labor availability, labor utilization, and product profitability: a. Develop a linear programming model of the Hartman Company problem. Solve the model to determine the optimal production quantities of products 1 and 2. b. In computing the profit contribution per unit, management does not deduct labor costs because they are considered fixed for the upcoming planning period. However, suppose that overtime can be scheduled in some of the departments. Which departments would you recommend scheduling for overtime? How much would you be willing to pay per hour of overtime in each department? c. Suppose that 10, 6, and 8 hours of overtime may be scheduled in departments A, B, and C, respectively. The cost per hour of overtime is 18 in department A, 22.50 in department B, and 12 in department C. Formulate a linear programming model that can be used to determine the optimal production quantities if overtime is made available. What are the optimal production quantities, and what is the revised total contribution to profit? How much overtime do you recommend using in each department? What is the increase in the total contribution to profit if overtime is used?arrow_forwardYoung Company is beginning operations and is considering three alternatives to allocate manufacturing overhead to individual units produced. Young can use a plantwide rate, departmental rates, or activity-based costing. Young will produce many types of products in its single plant, and not all products will be processed through all departments. In which one of the following independent situations would reported net income for the first year be the same regardless of which overhead allocation method had been selected? a. All production costs approach those costs that were budgeted. b. The sales mix does not vary from the mix that was budgeted. c. All manufacturing overhead is a fixed cost. d. All ending inventory balances are zero.arrow_forward

- Variable and Fixed Costs What follows are a number of resources that are used by a manufacturer of futons. Assume that the output measure or cost driver is the number of futons produced. All direct labor is paid on an hourly basis, and hours worked can be easily changed by management. All other factory workers are salaried. a. Power to operate a drill (to drill holes in the wooden frames of the futons) b. Cloth to cover the futon mattress c. Salary of the factory receptionist d. Cost of food and decorations for the annual Fourth of July party for all factory employees e. Fuel for a forklift used to move materials in a factory f. Depreciation on the factory g. Depreciation on a forklift used to move partially completed goods h. Wages paid to workers who assemble the futon frame i. Wages paid to workers who maintain the factory equipment j. Cloth rags used to wipe the excess stain off the wooden frames Required: Classify the resource costs as variable or fixed.arrow_forwardMiller Minerals Co. manufactures a product that requires the use of a considerable amount of natural gas to heat it to a desired temperature. The process requires a constant level of heat, so the furnaces are maintained at a set temperature for 24 hours a day. Although units are not continuously processed, management desires that the variable cost be charged directly to the product and the fixed cost to the factory overhead. The following data have been collected for the year: Required: 1. Separate the variable and fixed elements, using the high-low method. 2. Determine the variable cost to be charged to the product for the year. (Hint: First determine the number of annual units produced.) 3. Determine the fixed cost to be charged to factory overhead for the year.arrow_forwardIdentify cost graphs The following cost graphs illustrate various types of cost behavior: For each of the following costs, identify the cost graph that best illustrates its cost behavior as the number of units produced increases: A. Total direct materials cost B. Electricity costs of 1,000 per month plus 0.10 per kilowatt-hour C. Per-unit cost of straight-line depreciation on factory equipment D. Salary of quality control supervisor, 20,000 per month E. Per-unit direct labor costarrow_forward

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Essentials of Business Analytics (MindTap Course ...StatisticsISBN:9781305627734Author:Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. AndersonPublisher:Cengage Learning

Essentials of Business Analytics (MindTap Course ...StatisticsISBN:9781305627734Author:Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. AndersonPublisher:Cengage Learning Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning