Concept explainers

Videos

Varying Plantwide Predetermined

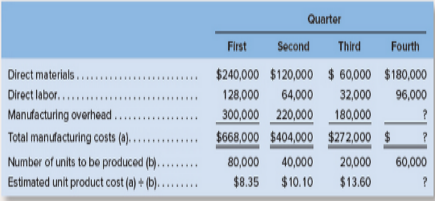

Kingsport Containers Company makes a single product that is subject to wide seasonal variations in demand. The company uses a job-ordercosting system and computes pIantwide predeterminedoverhead rates on a quarterly basis using the number of units to be produced as theallocation base. Its estimated costs, by quarter, for the coming year are given below:

Management finds the variation in quarterly unit product costs to be confusing and difficult to work with.It has been suggested that theproblem lies with manufacturing overhead because it is the largest element of total

Required:

1. Assuming the estimated variable manufacturing overhead cost per unit is $2.00, what must be the estimated total fixed manufacturing overhead cost per quarter?

2. Assuming the assumptions about cost behavior from the first three quarters hold constant what is the estimated unit product cost for thefourth quarter?

3. 1iat is causing the estimated unit product cost to fluctuate from one quarter to the next?

4. How would you recommend stabilizing the company’s unit product cost? Support your answer with computations.

Want to see the full answer?

Check out a sample textbook solution

Chapter 2 Solutions

BREWER ND LL INTRO MGRL ACTG CON+ AC

- A. Use the high-low method to estimate the fixed and variable portions of overhead costs based on machine hours. B. Managers expect the plant to operate at a monthly average of 7,500 machine-hours next year. What are the estimated monthly overhead costs, assuming no inflation?arrow_forwardThe management of Hartman Company is trying to determine the amount of each of two products to produce over the coming planning period. The following information concerns labor availability, labor utilization, and product profitability: a. Develop a linear programming model of the Hartman Company problem. Solve the model to determine the optimal production quantities of products 1 and 2. b. In computing the profit contribution per unit, management does not deduct labor costs because they are considered fixed for the upcoming planning period. However, suppose that overtime can be scheduled in some of the departments. Which departments would you recommend scheduling for overtime? How much would you be willing to pay per hour of overtime in each department? c. Suppose that 10, 6, and 8 hours of overtime may be scheduled in departments A, B, and C, respectively. The cost per hour of overtime is 18 in department A, 22.50 in department B, and 12 in department C. Formulate a linear programming model that can be used to determine the optimal production quantities if overtime is made available. What are the optimal production quantities, and what is the revised total contribution to profit? How much overtime do you recommend using in each department? What is the increase in the total contribution to profit if overtime is used?arrow_forwardYoung Company is beginning operations and is considering three alternatives to allocate manufacturing overhead to individual units produced. Young can use a plantwide rate, departmental rates, or activity-based costing. Young will produce many types of products in its single plant, and not all products will be processed through all departments. In which one of the following independent situations would reported net income for the first year be the same regardless of which overhead allocation method had been selected? a. All production costs approach those costs that were budgeted. b. The sales mix does not vary from the mix that was budgeted. c. All manufacturing overhead is a fixed cost. d. All ending inventory balances are zero.arrow_forward

- Miller Minerals Co. manufactures a product that requires the use of a considerable amount of natural gas to heat it to a desired temperature. The process requires a constant level of heat, so the furnaces are maintained at a set temperature for 24 hours a day. Although units are not continuously processed, management desires that the variable cost be charged directly to the product and the fixed cost to the factory overhead. The following data have been collected for the year: Required: 1. Separate the variable and fixed elements, using the high-low method. 2. Determine the variable cost to be charged to the product for the year. (Hint: First determine the number of annual units produced.) 3. Determine the fixed cost to be charged to factory overhead for the year.arrow_forwardVariable and Fixed Costs What follows are a number of resources that are used by a manufacturer of futons. Assume that the output measure or cost driver is the number of futons produced. All direct labor is paid on an hourly basis, and hours worked can be easily changed by management. All other factory workers are salaried. a. Power to operate a drill (to drill holes in the wooden frames of the futons) b. Cloth to cover the futon mattress c. Salary of the factory receptionist d. Cost of food and decorations for the annual Fourth of July party for all factory employees e. Fuel for a forklift used to move materials in a factory f. Depreciation on the factory g. Depreciation on a forklift used to move partially completed goods h. Wages paid to workers who assemble the futon frame i. Wages paid to workers who maintain the factory equipment j. Cloth rags used to wipe the excess stain off the wooden frames Required: Classify the resource costs as variable or fixed.arrow_forwardIdentify cost graphs The following cost graphs illustrate various types of cost behavior: For each of the following costs, identify the cost graph that best illustrates its cost behavior as the number of units produced increases: A. Total direct materials cost B. Electricity costs of 1,000 per month plus 0.10 per kilowatt-hour C. Per-unit cost of straight-line depreciation on factory equipment D. Salary of quality control supervisor, 20,000 per month E. Per-unit direct labor costarrow_forward

- Grand Canyon Manufacturing Inc. produces and sells a product with a price of 100 per unit. The following cost data have been prepared for its estimated upper and lower limits of activity: Overhead: Selling and administrative expenses: Required: 1. Classify each cost element as either variable, fixed, or semi-variable. (Hint: Recall that variable expenses must go up in direct proportion to changes in the volume of activity.) 2. Calculate the break-even point in units and dollars. (Hint: First use the high-low method illustrated in Chapter 4 to separate costs into their fixed and variable components.) 3. Prepare a break-even chart. 4. Prepare a contribution income statement, similar in format to the statement appearing on page 540, assuming sales of 5,000 units. 5. Recompute the break-even point in units, assuming that variable costs increase by 20% and fixed costs are reduced by 50,000.arrow_forwardBolger and Co. manufactures large gaskets for the turbine industry. Bolgers per-unit sales price and variable costs for the current year are as follows: Bolgers total fixed costs aggregate to 360,000. Bolgers labor agreement is expiring at the end of the year, and management is concerned about the effects of a new labor agreement on its break-even point in units. The controller performed a sensitivity analysis to ascertain the estimated effect of a 10-per-unit direct labor increase and a 10,000 reduction in fixed costs. Based on these data, the break-even point would: a. decrease by 1,000 units. b. decrease by 125 units. c. increase by 375 units. d. increase by 500 units.arrow_forwardA company’s current cost information relating to its production is shown in the table below: Per Unit Sales price $ 43 Direct material $ 7 Direct labor $ 6 Variable overhead $ 4 Fixed overhead $ 4 The company has been approached by a customer with a request for a 200-unit special order. What is the minimum per unit sales price that management would accept for this order, assuming the company has sufficient excess capacity?arrow_forward

- The management of Gregory Corporation believes that the inspection cost is a mixed cost that depends on units produced. The high- low method is used to estimate the variable and fixed components of this cost. The total inspection costs at Gregory's factory are listed below. Month Units Produced Inspection Cost January 990 $21,730 February 985 $21,645 March 807 $18,619 April 650 $15,950 May 760 $17,820 June 870 $19,690 July 8OS S18,585 August 810 SI8,670 September 700 $16,800arrow_forwardCurrent Attempt in Progress In Robert's manufacturing plant, the estimated monthly overhead cost function is provided in the Y = m(X) + b format: Total monthly overhead costs = $1.15(number of machine hours) + $6,500. Given this cost function, specify (a) the variable cost, (b) the fixed cost, (c) the cost driver, and (d) whether these monthly overhead costs are considered variable, fixed, or mixed in total. (Round variable cost to 2 decimal places, e.g. 15.25.) Variable cost Fixed cost Cost driver Cost type $ $arrow_forwardThe management of Gregory Corporation believes that the inspection cost is a mixed cost that depends on units produced. The high- low method is used to estimate the variable and fixed components of this cost. The total inspection costs at Gregory's factory are listed below. Month Units Produced Inspection Cost January 990 S21,730 February 985 $21,645 March 807 SIR619 April 650 SI5,950 May 760 $17,820 June 870 S19,690 July 805 SI8,585 August 810 SIRA0 September 700 S16,300 5. What is the variable cost per unit? * $8.50 per unit $17.00 per unit $21.95 per unit $22.98 per unit None of the abovearrow_forward

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Essentials of Business Analytics (MindTap Course ...StatisticsISBN:9781305627734Author:Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. AndersonPublisher:Cengage Learning

Essentials of Business Analytics (MindTap Course ...StatisticsISBN:9781305627734Author:Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. AndersonPublisher:Cengage Learning Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning