Concept explainers

Videos

Requirement – 1

To analyze: The given transaction, and explain their effect on the

Requirement – 1

Explanation of Solution

Accounting equation is an accounting tool expressed in the form of equation, by creating a relationship between the resources or assets of a company, and claims on the resources by the creditors and the owners. Accounting equation is expressed as shown below:

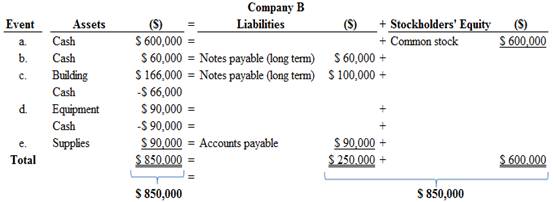

Accounting equation for each transaction is as follows:

Figure (1)

Figure (1)

Therefore, the total assets are equal to the liabilities and stockholder’s equity.

Requirement – 2

To record: The

Requirement – 2

Explanation of Solution

Journal:

Journal is the method of recording monetary business transactions in chronological order. It records the debit and credit aspects of each transaction to abide by the double-entry system.

Rules of Debit and Credit:

Following rules are followed for debiting and crediting different accounts while they occur in business transactions:

- Debit, all increase in assets, expenses and dividends, all decrease in liabilities, revenues and stockholders’ equities.

- Credit, all increase in liabilities, revenues, and stockholders’ equities, all decrease in assets, expenses.

Journal entries of Company B are as follows:

a. Issuance of common stock:

| Date | Accounts title and explanation | Ref. | Debit ($) | Credit ($) |

| Cash (+A) | 600,000 | |||

| Common stock (+SE) | 600,000 | |||

| (To record the issuance of common stock) |

Table (1)

- Cash is an assets account and it increased the value of asset by $600,000. Hence, debit the cash account for $600,000.

- Common stock is a component of stockholder’s equity and it increased the value of stockholder’s equity by $600,000, Hence, credit the common stock for $600,000.

b. Cash borrowed from bank (long term)

| Date | Accounts title and explanation | Ref. | Debit ($) | Credit ($) |

| Cash (+A) | 60,000 | |||

| Notes payable (+L) | 60,000 | |||

| (To record cash borrowed from bank) |

Table (2)

- Cash is an assets account and it increased the value of asset by $60,000. Hence, debit the cash account for $60,000.

- Notes payable is a liability account, and it increased the value of liabilities by $60,000. Hence, credit the notes payable for $60,000.

c. Building purchased on account and in cash:

| Date | Accounts title and explanation | Ref. | Debit ($) | Credit ($) |

| Building (+A) | 166,000 | |||

| Cash (-A) | 66,000 | |||

| Notes payable (+L) | 100,000 | |||

| (To record purchase of building on account and in cash) |

Table (3)

- Building is an assets account and it increased the value of asset by $166,000. Hence, debit the building account for $166,000.

- Cash is an assets account and it decreased the value of asset by $66,000. Hence, credit the cash account for $66,000.

- Notes payable is a liability account, and it increased the value of liabilities by $100,000. Hence, credit the notes payable for $100,000.

d. Equipment purchased:

| Date | Accounts title and explanation | Ref. | Debit ($) | Credit ($) |

| Equipment (+A) | 90,000 | |||

| Cash (-A) | 90,000 | |||

| (To record purchase of equipment in cash) |

Table (4)

- Equipment is an assets account and it increased the value of asset by $90,000. Hence, debit the equipment account for $90,000.

- Cash is an assets account and it decreased the value of asset by $90,000. Hence, credit the cash account for $90,000.

e. Purchase of supplies on account:

| Date | Accounts title and explanation | Ref. | Debit ($) | Credit ($) |

| Supplies (+A) | 90,000 | |||

| Accounts payable (+L) | 90,000 | |||

| (To record purchase of supplies on account) |

Table (5)

- Supplies are an assets account and it increased the value of asset by $90,000. Hence, debit the supplies account for $90,000.

- Accounts payable is a liability account and it increased the value of liability by $90,000. Hence, credit the liability account by $90,000.

Requirement – 3

To prepare: T-account for each account listed in the requirement 2.

Requirement – 3

Explanation of Solution

T-account:

T-account refers to an individual account, where the increasesor decreases in the value of specific asset, liability, stockholder’s equity, revenue, and expenditure items are recorded.

This account is referred to as the T-account, because the alignment of the components of the account resembles the capital letter ‘T’.’ An account consists of the three main components which are as follows:

- (a) The title of the account

- (b) The left or debit side

- (c) The right or credit side

T-accounts of Company B are as follows:

| Cash (A) | |||

| Beg. | 90,000 | ||

| (a) | 600,000 | 66,000 | (c) |

| (b) | 60,000 | 90,000 | (d) |

| End. | 594,000 | ||

| Supplies (A) | |||

| Beg. | 9,000 | ||

| (e) | 90,000 | ||

| End. | 99,000 | ||

| Equipment (A) | |||

| Beg. | 148,000 | ||

| (d) | 90,000 | ||

| End. | 238,000 | ||

| Buildings (A) | |||

| Beg. | 500,000 | ||

| (c) | 166,000 | ||

| End. | 666,000 | ||

| Land (A) | |||

| Beg. | 444,000 | ||

| End. | 444,000 | ||

| Accounts payable (L) | |||

| 50,000 | Beg. | ||

| 90,000 | (e) | ||

| 140,000 | End. | ||

| Note payable (L) | ||||

| 5,000 | Beg. | |||

| 60,000 | (b) | |||

| 100,000 | (c) | |||

| 165,000 | End. | |||

| Common stock (SE) | |||

| 170,000 | Beg. | ||

| 600,000 | (a) | ||

| 770,000 | End. | ||

| 966,000 | Beg. | ||

| 966,000 | End. | ||

Requirement – 4

To prepare: The

Requirement – 4

Explanation of Solution

Trial balance:

Trial balance is the summary of accounts, and their debit and credit balances at a given time. It is usually prepared at end of the accounting period. Debit balances are listed in left column and credit balances are listed in right column. The totals of debit and credit column should be equal. Trial balance is useful in the preparation of the financial statements.

Trial balance of Company B is as follows:

| Company B | ||

| Adjusted Trial Balance | ||

| At July, 31 | ||

| Accounts | Debit ($) | Credit ($) |

| Cash | 594,000 | |

| Supplies | 99,000 | |

| Equipment | 238,000 | |

| Building | 666,000 | |

| Land | 444,000 | |

| Accounts payable | 140,000 | |

| Notes payable | 165,000 | |

| Common stock | 770,000 | |

| Retained earnings | 966,000 | |

| Totals | $2,041,000 | $2,041,000 |

Table (6)

Therefore, the total of debit, and credit columns of trial balance is $2,041,000 and agree.

Requirement – 5

To prepare: The classified balance sheet of Company B at July 31.

Requirement – 5

Explanation of Solution

Classified balance sheet:

This is the financial statement of a company which shows the grouping of similar assets and liabilities under subheadings.

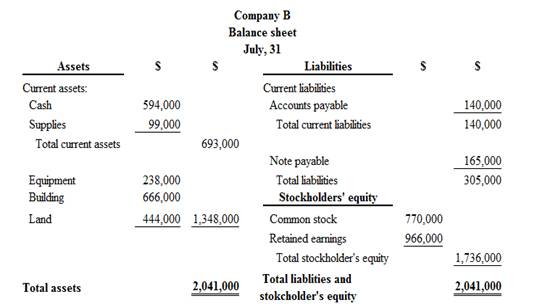

Classified balance sheet of Company B is as follows:

Figure (2)

Therefore, the total assets of Company B are$2,041,000, and the total liabilities and stockholders’ equity are $2,041,000.

Requirement – 6

Whether the assets amount of Company B is primarily come from liabilities or stockholders’ equity.

Requirement – 6

Explanation of Solution

The invested amount of assets are primarily come from stockholder’s’ equity of Company B, because the stockholder’s equity (common stock) financed $1,736,000 of the Company B’s total assets, and liabilities financed $305,000.

Want to see more full solutions like this?

Chapter 2 Solutions

FUND. OF FINANCIAL ACCT.-CONNECT ACCESS

- Transaction Analysis and Financial Statements Expert Consulting Services Inc. was organized on March 1 by two former college roommates. The corporation provides computer consulting services to small businesses. The following transactions occurred during the first month of operations: March 2: Received contributions of $20,000 from each of the two principal owners of the new business in exchange for shares of stock. March 7: Signed a two-year promissory note at the bank and received cash of $15,000. Interest, along with the $15,000, will be repaid at the end of the two years. March 12: Purchased $700 in miscellaneous supplies on account. The company has 30 days to pay for the supplies. March 19: Billed a client $4,000 for services rendered by Expert in helping to install a new computer system. The client is to pay 25% of the bill upon its receipt and the remaining balance within 30 days. March 20: Paid $1,300 bill from the local newspaper for advertising for the month of March. March 22: Received 25% of the amount billed to the client on March 19. March 26: Received cash of $2,800 for services provided in assisting a client in selecting software for its computer. March 29: Purchased a computer system for $8,000 in cash. March 30: Paid $3,300 of salaries and wages for March. March 31: Received and paid $1,400 in gas, electric, and water bills. Required Prepare a table to summarize the preceding transactions as they affect the accounting equation. Use the format in Exhibit 3-1. Identify each transaction with the date. Prepare an income statement for the month of March. Prepare a classified balance sheet at March 31. From reading the balance sheet you prepared in part (3), what events would you expect to take place in April? Explain your answer.arrow_forwardPrepare journal entries to record the following transactions. Create a T-account for Cash, post any entries that affect the account, and calculate the ending balance for the account. Assume a Cash beginning balance of $16,333. A. February 2, issued stock to shareholders, for cash, $25,000 B. March 10, paid cash to purchase equipment, $16,000arrow_forwardPrepare journal entries to record the following transactions that occurred in April: A. on first day of the month, issued common stock for cash, $15,000 B. on eighth day of month, purchased supplies, on account, $1,800 C. on twentieth day of month, billed customer for services provided, $950 D. on twenty-fifth day of month, paid salaries to employees, $2,000 E. on thirtieth day of month, paid for dividends to shareholders, $500arrow_forward

- Prepare journal entries to record the following transactions: A. December 1, collected balance due from customer account, $5,500 B. December 12, paid creditors for supplies purchased last month, $4,200 C. December 31, paid cash dividend to stockholders, $1,000arrow_forwardJournal entries and trial balance On August 1, 20Y7, Rafael Masey established Planet Realty, which completed the following transactions during the month: a. Rafael Masey transferred cash from a personal bank account to an account to be used for the business in exchange for common stock, 17,500. b. Purchased supplies on account, 2,300. c. Earned sales commissions, receiving cash, 13,300. d. Paid rent on office and equipment for the month, 3,000. e. Paid creditor on account, 1,150. f. Paid dividends, 1,800. g. Paid automobile expenses (including rental charge) for month, 1,500, and miscellaneous expenses, 400. h. Paid office salaries, 2,800. i. Determined that the cost of supplies used was 1,050. Instructions 1. Journalize entries for transactions (a) through (i), using the following account titles: Cash, Supplies, Accounts Payable, Common Stock, Dividends, Sales Commissions, Rent Expense, Office Salaries Expense, Automobile Expense, Supplies Expense, Miscellaneous Expense. Journal entry explanations may be omitted. 2. Prepare T accounts, using the account titles in (1). Post the journal entries to these accounts, placing the appropriate letter to the left of each amount to identify the transactions. Determine the account balances, after all posting is complete. Accounts containing only a single entry do not need a balance. 3. Prepare an unadjusted trial balance as of August 31, 20Y7. 4. Determine the following: a. Amount of total revenue recorded in the ledger. b. Amount of total expenses recorded in the ledger. c. Amount of net income for August. 5. Determine the increase or decrease in retained earnings for August.arrow_forwardDiscuss how each of the following transactions for Watson, International, will affect assets, liabilities, and stockholders equity, and prove the companys accounts will still be in balance. A. An investor invests an additional $25,000 into a company receiving stock in exchange. B. Services are performed for customers for a total of $4,500. Sixty percent was paid in cash, and the remaining customers asked to be billed. C. An electric bill was received for $35. Payment is due in thirty days. D. Part-time workers earned $750 and were paid. E. The electric bill in C is paid.arrow_forward

- Prepare journal entries to record the following transactions: A. October 9, issued common stock in exchange for building, $40,000 B. October 12, purchased supplies on account, $3,600 C. October 24, paid cash dividend to stockholders, $2,500arrow_forwardProvide journal entries to record each of the following transactions. For each, identify whether the transaction represents a source of cash (S), a use of cash (U), or neither (N). A. Paid $22,000 cash on bonds payable. B. Collected $12,600 cash for a note receivable. C. Declared a dividend to shareholders for $16,000, to be paid in the future. D. Paid $26,500 to suppliers for purchases on account. E. Purchased treasury stock for $18,000 cash.arrow_forwardJournal Entries, Trial Balance, and Financial Statements Neveranerror Inc. was organized on June 2 by a group of accountants to provide accounting and tax services to small businesses. The following transactions occurred during the first month of business: June 2: Received contributions of $10,000 from each of the three owners of the business in exchange for shares of stock. June 5: Purchased a computer system for $12,000. The agreement with the vendor requires a down payment of $2,500 with the balance due in 60 days. June 8: Signed a two-year promissory note at the bank and received cash of $20,000. June 15: Billed $12,350 to clients for the first half of June. Clients are billed twice a month for services performed during the month, and the bills are payable within ten days. June 17: Paid a $900 bill from the local newspaper for advertising for the month of June. June 23: Received the amounts billed to clients for services performed during the first half of the month. June 28: Received and paid gas, electric, and water bills. The total amount is $2,700. June 29: Received the landlords bill for $2,200 for rent on the office space that Neveranerror leases. The bill is payable by the 10th of the following month. June 30: Paid salaries and wages for June. The total amount is $5,670. June 30: Billed $18,400 to clients for the second half of June. June 30: Declared and paid dividends in the amount of $6,000. Required Prepare journal entries on the books of Neveranerror Inc. to record the transactions entered into during the month. Ignore depreciation expense and interest expense. Prepare a trial balance at June 30. Prepare the following financial statements: Income statement for the month of June Statement of retained earnings for the month of June Classified balance sheet at June 30 Assume that you have just graduated from college and have been approached to join this company as an accountant. From your reading of the financial statements for the first month, would you consider joining the company? Explain your answer. Limit your answer to financial considerations only.arrow_forward

- On July 1, K. Resser opened Ressers Business Services. Ressers accountant listed the following chart of accounts: The following transactions were completed during July: a. Resser deposited 25,000 in a bank account in the name of the business. b. Bought tables and chairs for cash, 725, Ck. No. 1200. c. Paid the rent for the current month, 1,750, Ck. No. 1201. d. Bought computers and copy machines from Ferber Equipment, 15,700, paying 4,000 in cash and placing the balance on account, Ck. No. 1202. e. Bought supplies on account from Wigginss Distributors, 535. f. Sold services for cash, 1,742. g. Bought insurance for one year, 1,375, Ck. No. 1203. h. Paid on account to Ferber Equipment, 700, Ck. No. 1204. i. Received and paid the electric bill, 438, Ck. No. 1205. j. Paid on account to Wigginss Distributors, 315, Ck. No. 1206. k. Sold services to customers for cash for the second half of the month, 820. l. Received and paid the bill for the business license, 75, Ck. No. 1207. m. Paid wages to an employee, 1,200, Ck. No. 1208. n. Resser withdrew cash for personal use, 700, Ck. No. 1209. Required 1. Record the owners name in the Capital and Drawing T accounts. 2. Correctly place the plus and minus signs for each T account and label the debit and credit sides of the accounts. 3. Record the transactions in the T accounts. Write the letter of each entry to identify the transaction. 4. Foot the T accounts and show the balances. 5. Prepare a trial balance as of July 31, 20--. 6. Prepare an income statement for July 31, 20--. 7. Prepare a statement of owners equity for July 31, 20--. 8. Prepare a balance sheet as of July 31, 20--. LO 1, 2, 3, 4, 5, 6arrow_forwardTransactions Interstate Delivery Service is owned and operated by Katie Wyer. The following selected transactions were completed by Interstate Delivery during May: 1. Received cash in exchange for common stock, 18,000. 2. Paid advertising expense, 4,850. 3. Purchased supplies on account, 2,100. 4. Billed customers for delivery services on account, 14,700. 5. Received cash from customers on account, 8,200. Indicate the effect of each transaction on the following accounting equation elements: Assets, Liabilities, Common Stock, Dividends, Revenue, and Expense. To illustrate, the answer to (1) follows: (1) Asset (Cash) increases by 18,000; Common Stock increases by 18,000.arrow_forwardDiscuss how each of the following transactions will affect assets, liabilities, and stockholders equity, and prove the companys accounts will still be in balance. A. A company purchased $450 worth of office supplies on credit. B. The company parking lot was plowed after a blizzard. A check for $75 was given to the plow truck operator. C. $250 was paid on account. D. A customer paid $350 on account. E. Provided services for a customer, $500. The customer asked to be billed.arrow_forward

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning

Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning, College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub

College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning

Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning