Videos

FISH & CHIPS INC, PART I

LEASE ANALYSIS Martha Millon,

If the computer is purchased, a maintenance contract must be obtained at a cost of $25,000, payable at the beginning of each year. After 4 years, the computer will be sold. Millon′s best estimate of its residual value at that time is $125,000. Because technology is changing rapidly however, the residual value is uncertain.

As an alternative. National Leasing is willing to write a 4-year lease on the computer, including maintenance, for payments of $340,000 at the beginning of each year. Fish 4c Chips′s marginal federal-plus-state tax rate is 40%. Help Millon conduct her analysis by answering the following questions.

a. 1. Why is leasing sometimes referred to as "off-balance-sheet" financing?

2. What is the difference between a capital lease and an operating lease?

3. What effect does leasing have on a firm′s capital structure?

b. 1. What is Fish & Chips's present value cost of owning the computer? (Hint: Set up a table whose bottom line is a “time line" that shows the cash flows over the period t = 0 to t = 4. Then find the PV of these cash flows, or the PV cost of owning.)

2. Explain the rationale for the discount rate you used to find the PV.

c. 1. What is Fish & Chips′s present value cost of leasing the computer? (Hint: Again, construct a time line.)

2. What is the net advantage to leasing? Does your analysis indicate that the firm should buy or lease the computer? Explain.

d. Now assume that Millon believes that the computer′s residual value could be as low as $0 or as high as $250,000, but she stands by $125,000 as her expected value. She concludes that the residual value is riskier than the other cash flows in the analysis, and she wants to incorporate this differential risk into her analysis. Describe how this can be accomplished. What effect will it have on the lease decision?

e. Millon knows that her firm has been considering moving its headquarters to a new location, and she is concerned that these plans may come to fruition prior to the expiration of the lease. If the move occurs, the company would obtain new computers; hence, Millon would like to include a cancellation clause in the lease contract. What effect would a cancellation clause have on the risk of the lease?

a.1.

To discuss: The reason why leasing is referred as an off-balance-sheet financing.

Introduction:

Off-balance sheet financing is a type of financing where the firm does not include a liability on its balance sheet. This is an accounting term and has impact on firm’s debt level and liabilities.

Explanation of Solution

The reason why leasing is referred as an off-balance-sheet financing is as follows:

At the time when an asset is purchased, this asset will be exhibited on the left-hand side balance sheet’s left hand side and has to offset equity or debt on the balance sheet’s right-hand side. However, when an asset is leased and the lease is not segregated into a capital lease, then it will not be exhibited straightly on the balance sheet. This will only be reported in the footnotes of the financial statement of the company. Therefore, this is the main reason for a leasing, which is being termed as off-balance sheet financing.

a.2

To discuss: The difference between the operating and capital lease.

Introduction:

Capital lease is termed as contract wherein lesser agrees to transfer ownership right to leasee once the completion of lease time. It is a long term lease contracts. There are also termed as finance lease.

Operating lease is a lease on assets, which is not fully amortized in the non-cancelable period. It is considered as a short term lease.

Explanation of Solution

Capital leases are distinguished from operating leases in three factors which are as follows:

- Capital lease does not gives maintenance services.

- Capital lease are not cancelable

- It is fully amortized

a.3.

To discuss: The effect that leasing has on the capital structure of the firm.

Explanation of Solution

The effect that leasing has on the capital structure of the firm is as follows:

Leasing is one substitute for debt financing. The lease payments are considered as a contractual obligation between the corresponding parties. The firm would face bankruptcy when the lease payment is not paid time. As a result the leasing uses up a firm’s debt capacity.

For instance, the F Company’s optimal capital structure comprise of 50 percent of equity and 50 percent debt. At the time when the company leases half of its assets, then the reaming half of asset will be financed by the common equity.

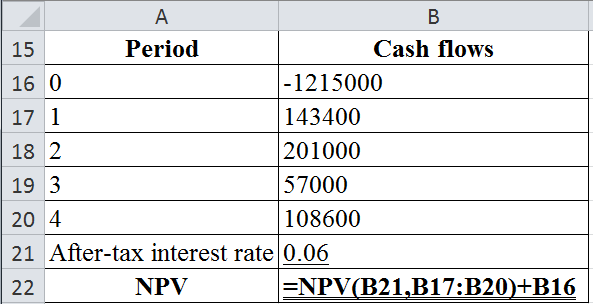

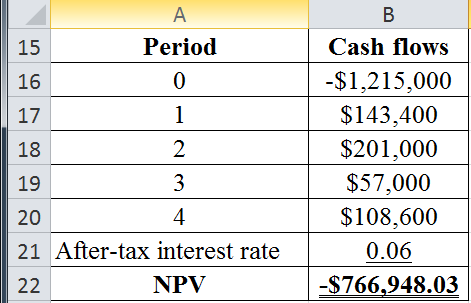

b.1.

To determine: The present value cost of owing the computer.

Explanation of Solution

Given information:

F Company has decided to purchase a new computer system on lease. The cost of computer is $1,200,000 and company can provide a term loan for the total amount of 10%. This loan is amortized over the 4-years life of the computer. The MACRS rates are 30 percent, 45 percent, 15 percent, and 7 percent. The maintenance cost of the computer will be $25,000 which is payable in the beginning of every year.

The computer will be sold after 4-years period and its residual value is $125,000. The national leasing is willing to offer 4-years lease on the computer including maintenance for payment of $340,000 and tax rate is 40 percent.

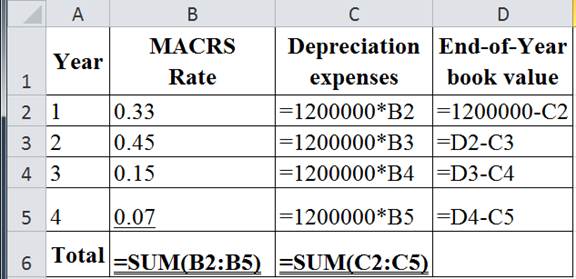

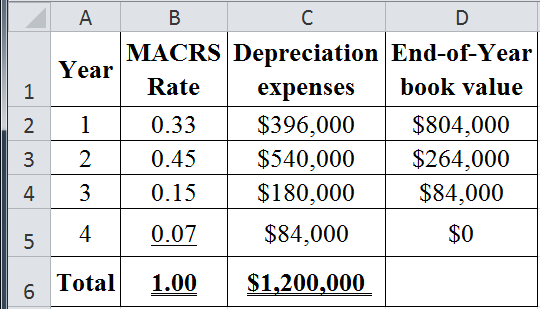

Construct a depreciation schedule in order to determine the cost of owing:

The below table show the Excel formula to compute the depreciation expenses and end-of-year book value:

The table below shows the calculated value of depreciation expenses and end-of-year book value:

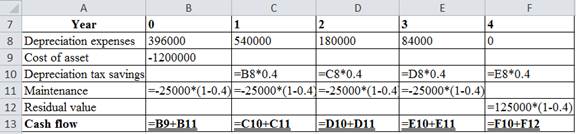

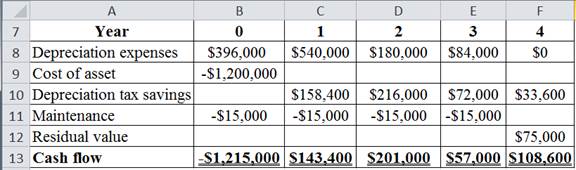

The table below shows the Excel formula to compute the cash flow:

The table below shows the calculated value of cash flows:

Compute the after-tax interest rate:

Hence, the after-tax interest rate is 0.06.

Compute the present value of the cost of owing:

The table below shows the Excel Formula to compute the present value of the cost of owing:

The table below shows the calculated value of present value of the cost of owing:

The present value of the cost of owing is −$766,948.03.

b.2.

To discuss: The rationale for the discount rate that is utilised to determine the present value.

Explanation of Solution

The rationale for the discount rate that is used to determine the present value is as follows:

The discount rate used to find the present value depends on the riskless of the cash flows stream and even the level of interest rate. The cost of owing cash flows without including the residual value is fixed by means of the contract. As a result, it is not very risky. However, they have almost the similar risk as the company’s debt flows that are also contractual in nature.

The leasing process use debt capacity, so the similar impact on the financial risk such as debt financing. Therefore, the appropriate interest rate is the cost of debt of the F Company since the flows are after-tax flows. In this case, the F Company’s before-tax debt cost is 10 percent and tax rate is 40 percent. Therefore, the after-tax cost of debt will be 6 percent

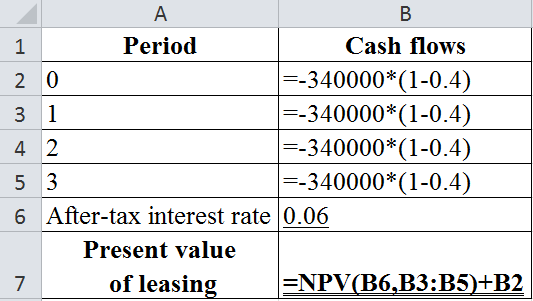

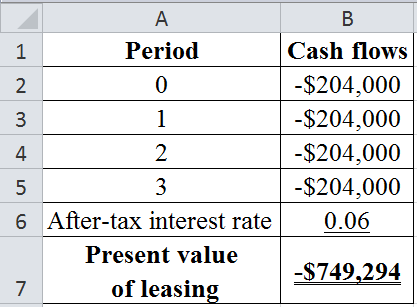

c.1.

To determine: The present value cost of leasing the computer.

Explanation of Solution

Given information:

F Company has decided to purchase a new computer system on lease. The cost of computer is $1,200,000 and company can give a term loan for the total amount of 10%. This loan is amortized for the 4-years life of the computer. The MACRS rates are 30 percent, 45 percent, 15 percent, and 7 percent. The maintenance cost of the computer will be $25,000 which is payable in the beginning of every year.

The computer will be sold after 4-years period and its residual value is $125,000. The national leasing is wishing to offer 4-years lease on the computer including maintenance for payment of $340,000 and tax rate is 40 percent.

Compute the present value of leasing:

The table below shows the Excel formula to compute the present value of leasing:

The table below shows the calculated value of present value of leasing:

Hence, the present value of leasing is −$749,294.

c.2.

To determine: The net advantage to leasing and whether the analysis indicates that the firm must purchase or lease the computer.

Explanation of Solution

Given information:

F Company has decided to purchase a new computer system on lease. The cost of computer is $1,200,000 and company can give a term loan for the total amount of 10 %. This loan is amortized for the 4-years life of the computer. The MACRS rates are 30 percent, 45 percent, 15 percent, and 7 percent. The maintenance cost of the computer will be $25,000 which is payable in the starting of every year.

The computer will be sold after 4-years period and its residual value is $125,000. The national leasing is ready to offer 4-years lease on the computer including maintenance for payment of $340,000 and tax rate is 40 percent.

The formula to calculate the net advantage to leasing is as follows:

Calculate the net advantage to leasing:

Hence the net advantage to leasing is $17,654.03. Here, the net advantage to leasing has a positive value. The cost of owing outweighs the cost of leasing. Therefore, the F Company can lease the computer system than buying it.

d.

To discuss: The way for accomplishing the task and effect that will have on the leasing decision.

Explanation of Solution

The way for accomplishing the task and effect that will have on the leasing decision is as follow:

The rate utilized to discount the residual value cash flow must be raised in order to account for an increased risk. This can result to a lower present value. As a result, the lower present value can leads to a greater cost of owing because the residual value is an inflow. Therefore, the higher risk of the residual value can result in the greater cost of owing and even the leasing becomes much attractive in this stage.

The asset owner bears the residual value risk, so the leasing passes the risk to the lessor. Here, the lessor identifies this risk factor, so the assets with highly uncertain residual value can carry maximum lease payments as compared to the assets with relatively certain residual values.

e.

To discuss: The effect of a cancellation clause has on the risk of the lease.

Explanation of Solution

The effect of a cancellation clause has on the risk of the lease is as follows:

The cancelation clause will lower the risk of the lease for the F Company (lessee). It is because the company is not being obligated to make the payments on lease in all terms. Here, the company can terminate the lease when it does not need a computer or wants to change into a more technological advanced system. On the other hand, a cancellation clause can make the contract more risky for the lessor. As a result, the lessor will not only bear the residual value risk but also the uncertainty of when the contract would be cancelled.

The lessor must increase the annual lease payment to account for extra risks. Moreover, the lessor must include clauses that will prohibit cancellation for some period or impose a penalty charges for cancellation, which might reduce on the cancellation of the lease over time.

Want to see more full solutions like this?

Chapter 20 Solutions

Bundle: Fundamentals Of Financial Management, Loose-leaf Version, 15th + Mindtapv2.0 Finance, 1 Term (6 Months) Printed Access Card

- Lease versus Buy Consider the data in Problem 19-1. Assume that RCs tax rate is 40% and that the equipments depreciation would be 100 per year. If the company leased the asset on a 2-year lease, the payment would be 110 at the beginning of each year. If RC borrowed and bought, the bank would charge 10% interest on the loan. In either case, the equipment is worth nothing after 2 years and will be discarded. Should RC lease or buy the equipment?arrow_forwardOwens Company leased equipment for 4 years at 50,000 a year with an option to renew the lease for 6 years at 2,000 per month or to purchase the equipment for 25,000 (a price considerably less than the expected fair value) after the initial lease term of 4 years. Why would this lease qualify as a finance lease?arrow_forwardUse the information in RE20-6. However, assume that there is no bargain purchase option and that Montevallo guarantees the 20,000 estimated residual value at the end of the 10-year lease. Montevallo estimates that it is probable that it will have to pay 15,000 cash due to the residual value guarantee. Calculate the present value of the lease payments. Round your answer to the nearest dollar.arrow_forward

- Big Sky Mining Company must install 1.5 million of new machinery in its Nevada mine. It can obtain a bank loan for 100% of the purchase price, or it can lease the machinery. Assume that the following facts apply. (1) The machinery falls into the MACRS 3-year class. (2) Under either the lease or the purchase, Big Sky must pay for insurance, property taxes, and maintenance. (3) The firms tax rate is 25%. (4) The loan would have an interest rate of 15%. It would be nonamortizing, with only interest paid at the end of each year for four years and the principal repaid at Year 4. (5) The lease terms call for 400,000 payments at the end of each of the next 4 years. (6) Big Sky Mining has no use for the machine beyond the expiration of the lease, and the machine has an estimated residual value of 250,000 at the end of the 4th year. a. What is the cost of owning? b. What is the cost of leasing? c. What is the NAL of the lease?arrow_forwardReynolds Construction (RC) needs a piece of equipment that costs 200. RC can either lease the equipment or borrow 200 from a local bank and buy the equipment. Reynoldss balance sheet prior to the acquisition of the equipment is as follows: a. (1) What is RCs current debt ratio? (2) What would be the companys debt ratio if it purchased the equipment? (3) What would be the debt ratio if the equipment were leased and the lease not capitalized? (4) What would be the debt ratio if the equipment were leased and the lease were capitalized? Assume that the present value of the lease payments is equal to the cost of the equipment. b. Would the companys financial risk be different under the leasing and purchasing alternatives?arrow_forwardDifferential analysis for a lease or sell decision Burlington Construction Company is considering selling excess machinery with a book value of 115,000 (original cost of 275,000 less accumulated depreciation of 160,000) for 90,000, less a 6% brokerage commission. Alternatively, the machinery can be leased for a total of 100,000, for four years, after which it is expected to have no residual value. During the period of the lease, Burlington Construction Companys costs of repairs, insurance, and property tax expenses are expected to be 9,000. a. Prepare a differential analysis dated January 15 to determine whether Burlington Construction Company should lease (Alternative 1) or sell (Alternative 2) the machinery. b. On the basis of the data presented, would it be advisable to lease or sell the machinery? Explain.arrow_forward

- Grummet Company is acquiring a new wood lathe with a cash purchase price of $80,000. The Wood Master Industries (the manufacturer) has agreed to accept $23,500 at the end of each of the next 4 years. Based on this deal, how much interest will Grummet pay over the life of the loan? A. $94,000 B. $80,000 C. $23,500 D. $14,000arrow_forwardLease versus purchase Northwest Lumber Company needs to expand its facilities. To do so, the firm must acquire a machine costing $80,000. The machine can be leased or purchased. The firm is in the 21% tax bracket, and its after-tax cost of debt is 9%. The terms of the lease and purchase plans are as follows: Lease The leasing arrangement requires end-of-year payments of $19,800 over 5 years. All maintenance costs will be paid by the lessor; insurance and other costs will be borne by the lessee. The lessee will exercise its option to purchase the asset for $24,000 at termination of the lease. Purchase If the firm purchases the machine, its cost of $80,000 will be financed with a 5-year, 14% loan requiring equal end-of-year payments of $23,302. The machine will be depreciated under MACRS using a 5-year recovery period. (See Table 2 for the applicable depreciation percentages.) The firm will pay $2,000 per year for a service contract that covers all maintenance costs; insurance and other…arrow_forward

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781285867977Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781285867977Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT

EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT

Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning

Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning