Concept explainers

Videos

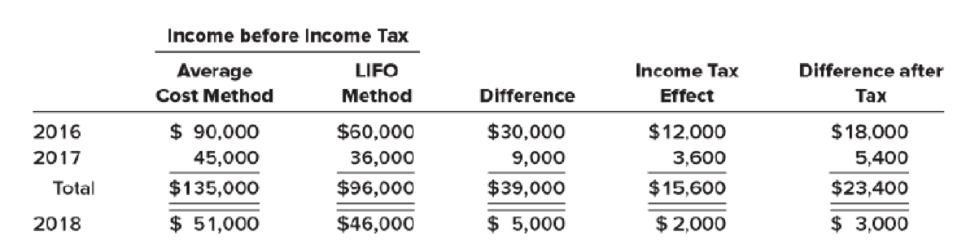

P 20-2

Change in principle; change in method of accounting for long-term construction

• LO20–2

The Pyramid Company has used the LIFO method of accounting for inventory during its first two years of operation, 2016 and 2017. At the beginning of 2018, Pyramid decided to change to the average cost method for both tax and financial reporting purposes. The following table presents information concerning the change for 2016–2018. The income tax rate for all years is 40%.

Pyramid issued 50,000 $1 par, common shares for $230,000 when the business began, and there have been no changes in paid-in capital since then. Dividends were not paid the first year, but $10,000 cash dividends were paid in both 2017 and 2018.

Required:

- 1. Prepare the

journal entry to record the change in accounting principle. - 2. Prepare the 2018–2017 comparative income statements beginning with income before income taxes.

- 3. Prepare the 2018–2017 comparative statements of shareholders’ equity. [Hint: The 2016 statements reported

retained earnings of $36,000. This is $60,000 − ($60,000 × 40%).]

Want to see the full answer?

Check out a sample textbook solution

Chapter 20 Solutions

INTERMEDIATE ACCOUNTING(LL)-W/2 ACCESS

- Exercise 16-23 (Algo) Net operating loss carryforward; financial statement effects [LO16-7] During 2024, its first year of operations, Baginski Steel Corporation reported a net operating loss of $444,000 for financial reporting and tax purposes. The enacted tax rate is 25%. Required: 1. Prepare the journal entry to recognize the income tax benefit of the net operating loss. Assume the weight of available evidence suggests that future taxable income will be sufficient to benefit from future deductible amounts arising from the net operating loss carryforward. 2. Show the lower portion of the 2024 income statement that reports the income tax benefit of the net operating loss.arrow_forward46 tax pharrow_forwardajt.1arrow_forward

- 6arrow_forwardProblem 16-6 (IAA) Complex Company reported the following information relating to income before tax for accounting purposes: 2021 2022 2023 2024 Income tax rate In 2021, the entity recognized doubtful accounts of P100,000. The doubtful accounts were considered worthless or uncollectible in 2022. 2,000,000 3,000,000 4,000,000 5,000,000 25% Analysis of the tax and book records disclosed P120,000 in unearned rent income on December 31, 2021 that had been recognized as taxable income in 2021 when the cash was received. Also on December 31, 2021, estimated warranty cost of P300,000 had been recognized as expense on the books in 2021 when the product sales were made but is not deductible for tax purposes until paid. The unearned rent income on December 31, 2021 was realized and the actual warranty payments were made in the following years: Rent income per book Actual warranty payments 40,000 40,000 40,000 2022' 2023 2024 20,000 80,000 200,000 Required: 1. Prepare journal entries for 2021,…arrow_forwardQUESTION 12 Annual data for ABC Corporation appear below, in millions of US dollars: 2016 2017 2018 2019 Sales Revenue 126.1 131.3 144.5 150.4 Cost of Goods Sold 45.3 50.8 54.6 55.3 Operating Income Ending Inventory 18.8 21.1 20.9 23.3 9.6 10.2 10.8 9.6 Ending Accounts Payable 10.2 8.8 9.5 10.2 Calculate ABC's inventory turnover ratio for 2017. Round your answer to 1 decimal place (xx.x).arrow_forward

- E 18-1 Comprehensive The following is from the 2018 annual report of Kaufman Chemicals, Inc.: Statements of Comprehensive Income Years Ended December 31 income • LO18-2 2018 2017 2016 Net income $856 $766 $594 Other comprehensive income: Change in net unrealized gains on investments, net of tax of $22, ($14), and $15 in 2018, 2017, and 2016, respectively 34 (21) 23 Other (2) $888 (1) $744 $618 Total comprehensive income Kaufman reports accumulated other comprehensive income in its balance sheet as a component of shareholders equity as follows: ($ in millions) 2018 2017 Shareholders' equity: Common stock 355 355 Additional paid-in capital Retained earnings Accumulated other comprehensive income 8,567 6,544 8,567 5,988 107 75 Total shareholders'equity $15,573 $14,985 Required: 1. What is comprehensive income and how does it differ from net income? 2. How is comprehensive income reported in a balance sheet? 3. Why is Kaufman's 2018 balance sheet amount different from the 2018 amount…arrow_forwardExercise 19-21 The pretax financial income (or loss) figures for Kingbird Company are as follows. 74,000 (50,000) (40,000) 113,000 99,000 2017 2018 2019 2020 2021 Pretax financial income (or loss) and taxable income (loss) were the same for all years involved. Assume a 25% tax rate for 2017 and a 20% tax rate for the remaining years. Prepare the journal entries for the years 2017 to 2021 to record income tax expense and the effects of the net operating loss carryforwards. All income and losses relate to normal operations. (In recording the benefits of a loss carryforward, assume that no valuation account is deemed necessary.) (Credit account titles are automatically indented when amount is entered. Do not indent manually. If no entry is required, select "No Entry" for the account titles and enter 0 for the amounts.) Account Titles and Explanation Debit Credit 2017 2018arrow_forwardExercise 19-23 Spamela Hamderson Inc. reports the following pretax income (loss) for both financial reporting purposes and tax purposes. Year Pretax Income(Loss) Tax Rate 2018 $120,000 17 % 2019 90,000 17 % 2020 (280,000) 19 % 2021 300,000 19 % The tax rates listed were all enacted by the beginning of 2018. Assuming that at the end of 2020 the benefits of the loss carryforward are judged more likely than not to be realized in the future, prepare the income tax section of the 2020 income statement, beginning with the line “Operating loss before income taxes.” (Enter negative amounts using either a negative sign preceding the number e.g. -45 or parentheses e.g. (45).)arrow_forward

- Question 35 Armstrong Inc. is a calendar-year corporation. Its financial statements for the years ended 12/31/20 and 12/31/21 contained the following errors: 2020 2021 Ending inventory $50,000 overstatement $80,000 understatement Depreciation expense 20,000 understatement 40,000 overstatement Assume that the 2020 errors were not corrected and that no errors occurred in 2019. By what amount will 2020 income before income taxes be overstated or understated? $30,000 understatement $30,000 overstatement $70,000 overstatement $70,000 understatementarrow_forwardExercise 19-24 Beilman Inc. reports the following pretax income (loss) for both book and tax purposes. Year PretaxIncome (Loss) Tax Rate 2018 $120,000 20 % 2019 90,000 20 % 2020 (280,000) 25 % 2021 120,000 25 % The tax rates listed were all enacted by the beginning of 2018. A) Prepare the income tax section of the 2020 income statement beginning with the line “Operating loss before income taxes.” (Enter negative amounts using either a negative sign preceding the number e.g. -45 or parentheses e.g. (45).) B) Prepare the income tax section of the 2021 income statement beginning with the line “Income before income taxes.” (Enter negative amounts using either a negative sign preceding the number e.g. -45 or parentheses e.g. (45).)arrow_forward104-Principles of Management Acco y courses/ BUSS 104-2-20202 / TEST 2 SCHEDULED FOR 12TH APRIL 2021 IN CL The BCD Company had the following income statement on 31.12.2020 Deprecation 10000 Net income 190000 OMR The following accounts decreased during 2020: Accounts receivable 22000 inventory 15000 OMR. Rent payable 19000, Machinery 15000 OMR The following accounts increased during 2020:Notes receivable 14000 Accounts Payable 13000 long term Bonds payable 30000 OMR Calculate cash flows from operating activities Select one: O a. 245000 OMR O b. NONE OF THESE Oc. 217000 OMR O d. 249000 OMR Next page page s unit 4 Jump to.. nned in se Moor Rakhit Almaschani na utharrow_forward

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning Individual Income TaxesAccountingISBN:9780357109731Author:HoffmanPublisher:CENGAGE LEARNING - CONSIGNMENT

Individual Income TaxesAccountingISBN:9780357109731Author:HoffmanPublisher:CENGAGE LEARNING - CONSIGNMENT