Videos

a

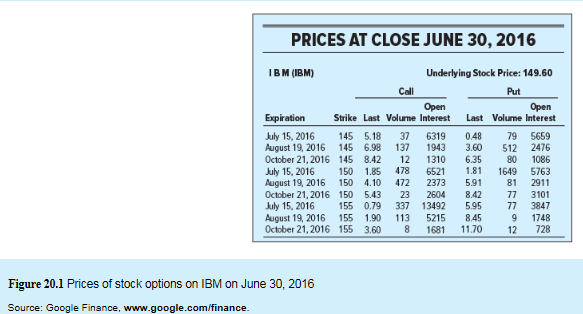

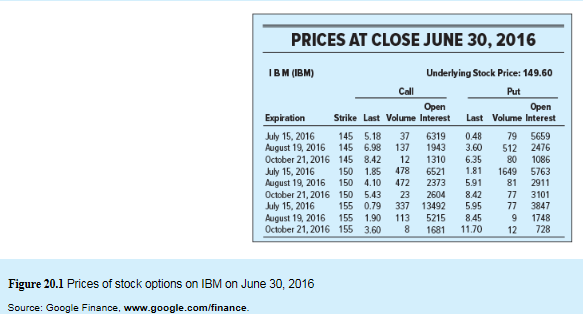

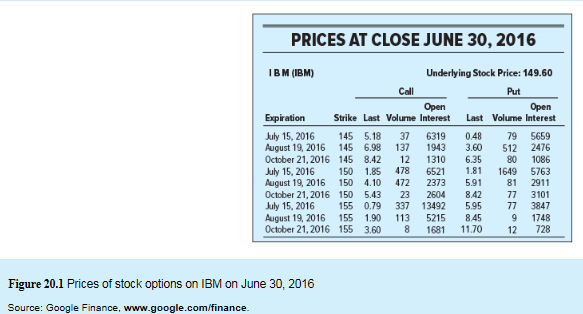

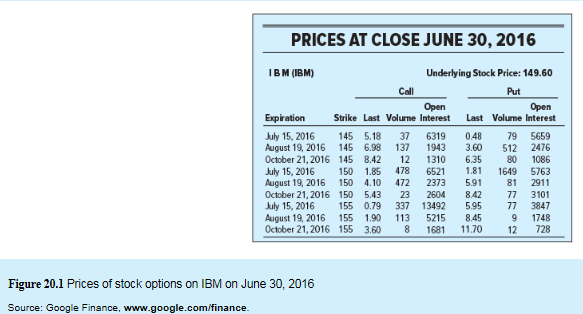

To compute: The payoff and the profit for investments when the call option’s exercise price X=$145 assuming that the stock price on the expiration date is $150.

Introduction:

Options: Options are the instruments used in financial transactions. These are derived based on the value of the underlying assets. Normally, the purpose of an option is to provide the buyer an opportunity to buy or sell the underlying asset depending upon the type of contract they possess. There are two types of options- Call option and put option.

a

Answer to Problem 5PS

The call buyer will incur loss of -$0.18 when the exercise price is $145.

Explanation of Solution

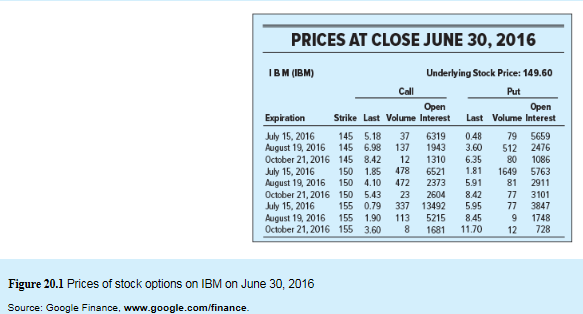

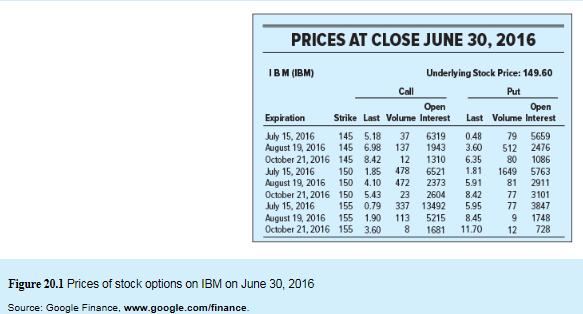

The information given to us is as follows:

Let us calculate the payoff when Call option X is $145 and stock price on expiry date is $150.

| Calculation of payoff in case of call option | ||

| Position | Stock price > X | Stock price is less than or equal to X |

| Payoff to call holder | Stock price -X | 0 |

| Payoff to call writer | -(Stock price -X) | 0 |

Stock price at expiration is $150.

Exercise or Strike price X=$145.

So, let us now substitute the values in the above table. We get

| Calculation of payoff in case of call option | ||

| Position | Stock price > X | Stock price is less than or equal to X |

| Payoff to call holder |  | 0 |

| Payoff to call writer |  | 0 |

By the above calculation, it is observed that the call writer is prepared to bear the risk in return of option premium as there is loss if stock price increases.

Calculation of profit for investment:

But as per the information given to us, the price of the call option is $5.18 at a strike price $145 on June 2016.

Therefore, the call buyer will incur loss of -$0.18.

b.

To compute: The payoff and the profit for investments when the put option’s exercise price X=$145 assuming that the stock price on the expiration date is $150.

Introduction:

Payoff: In financial terminology, payoff refers to the return on an investment.

b.

Answer to Problem 5PS

The loss incurred by the put buyer will be -$0.48 when the exercise price is $145.

Explanation of Solution

The information given to us is as follows:

Let us calculate the payoff when Put option X is $145 and stock price on expiry date is $150.

| Calculation of payoff in case of a put option | ||

| Position | If Stock price is less than X | If Stock price is greater or equal to X |

| Payoff to Put holder | X-Stock price | 0 |

| Payoff to Put writer | -(X-Stock price) | 0 |

Stock price at expiration is $150.

Exercise or Strike price X=$145.

So, let us now substitute the values in the above table. We get

| Calculation of payoff in case of a put option | ||

| Position | If Stock price is less than X | If Stock price is greater or equal to X |

| Payoff to Put holder | $0 | 0 |

| Payoff to Put writer | $0 | 0 |

But, we are informed that the put option is $0.48 at a strike price of $145 on June2016.

Therefore, the loss incurred by the buyer on put option will be -$0.48.

c

To compute: The payoff and the profit for investments when the call option’s exercise price X=$150 assuming that the stock price on the expiration date is $150.

Introduction:

Profit on investment: Investments are supposed to be considered as a monetary asset. Investments are done with an expectation to earn good income in future or to sell this asset at a higher price. If the purchase price of the asset is less than the sale price of the asset, it can be termed as profit on investment else it is loss on investment.

c

Answer to Problem 5PS

The call buyer will incur loss of -$1.85 when the exercise price is $150.

Explanation of Solution

The information given to us is as follows:

Let us calculate the payoff when Call option X is $150 and stock price on expiry date is $150.

| Calculation of payoff in case of call option: | ||

| Position | Stock price > X | Stock price is less than or equal to X |

| Payoff to call holder | Stock price -X | 0 |

| Payoff to call writer | -(Stock price -X) | 0 |

Stock price at expiration is $150.

Exercise or Strike price X=$150.

So, let us now substitute the values in the above table. We get

| Calculation of payoff in case of call option | ||

| Position | Stock price > X | Stock price is less than or equal to X |

| Payoff to call holder |  | 0 |

| Payoff to call writer |  | 0 |

By the above calculation, it is observed that the call writer is prepared to bear the risk in return of option premium as there is loss if stock price increases.

Calculation of profit for investment:

But as per the information given to us, the price of the call option is $1.85 at a strike price $150 on June 2016.

Therefore, the call buyer will incur loss of -$1.85.

d.

To compute: The payoff and the profit for investments when the put option’s exercise price X=$150 assuming that the stock price on the expiration date is $150.

Introduction:

Options: Options are the instruments used in financial transactions. These are derived based on the value of the underlying assets. Normally, the purpose of an option is to provide the buyer an opportunity to buy or sell the underlying asset depending upon the type of contract they possess. There are two types of options- Call option and put option.

d.

Answer to Problem 5PS

The incurred by the put buyer will be -$1.81 when the exercise price is $150.

Explanation of Solution

The information given to us is as follows:

Let us calculate the payoff when Put option X is $150 and stock price on expiry date is $150.

| Calculation of payoff in case of a put option | ||

| Position | If Stock price is less than X | If Stock price is greater or equal to X |

| Payoff to Put holder | X-Stock price | 0 |

| Payoff to Put writer | -(X-Stock price) | 0 |

Stock price at expiration is $150.

Exercise or Strike price X=$150.

So, let us now substitute the values in the above table. We get

| Calculation of payoff in case of a put option | ||

| Position | If Stock price is less than X | If Stock price is greater or equal to X |

| Payoff to Put holder | $0 | 0 |

| Payoff to Put writer | $0 | 0 |

But, we are informed that the put option is $1.81 at a strike price of $150 on June 2016.

Therefore, the loss incurred by the buyer on put option will be -$1.81.

e.

To compute: The payoff and the profit for investments when the call option’s exercise price X=$155 assuming that the stock price on the expiration date is $150.

Introduction:

Payoff: In financial terminology, payoff refers to the return on an investment.

e.

Answer to Problem 5PS

The loss incurred by the call buyer will be -$0.79 when the exercise price is $155.

Explanation of Solution

The information given to us is as follows:

Let us calculate the payoff when Call option X is $155 and stock price on expiry date is $150.

| Calculation of payoff in case of call option | ||

| Position | Stock price > X | Stock price is less than or equal to X |

| Payoff to call holder | Stock price -X | 0 |

| Payoff to call writer | -(Stock price -X) | 0 |

Stock price at expiration is $150.

Exercise or Strike price X=$155.

So, let us now substitute the values in the above table. We get

| Calculation of payoff in case of call option | ||

| Position | Stock price > X | Stock price is less than or equal to X |

| Payoff to call holder | 0 | 0 |

| Payoff to call writer | 0 | 0 |

By the above calculation, it is observed that the call writer is prepared to bear the risk in return of option premium as there is loss if stock price increases.

Calculation of profit for investment

But as per the information given to us, the price of the call option is $0.79 at a strike price $155 on June 2016.

Therefore, the call buyer will incur loss of -$0.79.

f.

To compute: The payoff and the profit for investments when the put option’s exercise price X=$155 assuming that the stock price on the expiration date is $150.

Introduction:

Loss on investment: Investments are supposed to be considered as a monetary asset. Investments are done with an expectation to earn good income in future or to sell this asset at a higher price. If the purchase price of the asset is less than the sale price of the asset, it can be termed as profit on investment else it is loss on investment.

f.

Answer to Problem 5PS

The loss incurred by the put buyer will be $-0.95 when the exercise price is $155.

Explanation of Solution

The information given to us is as follows:

Let us calculate the payoff when Put option X is $155 and stock price on expiry date is $150.

| Calculation of payoff in case of a put option | ||

| Position | If Stock price is less than X | If Stock price is greater or equal to X |

| Payoff to Put holder | X-Stock price | 0 |

| Payoff to Put writer | -(X-Stock price) | 0 |

Stock price at expiration is $150.

Exercise or Strike price X=$155.

So, let us now substitute the values in the above table. We get

| Calculation of payoff in case of a put option | ||

| Position | If Stock price is less than X | If Stock price is greater or equal to X |

| Payoff to Put holder |  | 0 |

| Payoff to Put writer |  | 0 |

But, we are informed that the put option is $5.95 at a strike price of $155 on June 2016.

Therefore, the loss incurred by the buyer on put option will be -0.95.

Want to see more full solutions like this?

Chapter 20 Solutions

INVESTMENTS (LOOSELEAF) W/CONNECT

- In 1973, Fischer Black and Myron Scholes developed the Black-Scholes option pricing model (OPM). (1) What assumptions underlie the OPM? (2) Write out the three equations that constitute the model. (3) According to the OPM, what is the value of a call option with the following characteristics? Stock price = 27.00 Strike price = 25.00 Time to expiration = 6 months = 0.5 years Risk-free rate = 6.0% Stock return standard deviation = 0.49arrow_forwardAn investor decides to implement a STRADDLE using put options using the following data . The price of stock today is $ 59 , time frame is 6months , the staddle is constructed using a put and a call option with a strike price of $ 61 . The call cost $ 4 and put costs $ 3 . a ) What is the profit ( % ) if in 6 months , if the stock price is at $ 70 b ) What is the profit ( % ) if in 6 months , if the stock price is at $ 60 c ) At what stock price in the future , the investor will make the least / min profit ? d ) Why do investors implement / use this strategy ? For what reason ?arrow_forwardAssume the following inputs for a call option: (1) current stock price is $23, (2) strike price is $28, (3) time to expiration is 5 months, (4) annualized risk-free rate is 5%, and (5) variance of stock return is 0.3. The data has been collected in the Microsoft Excel Online file below. Open the spreadsheet and perform the required analysis to answer the question below. Use the Black-Scholes model to find the price for the call option. Do not round intermediate calculations. Round your answer to the nearest cent.arrow_forward

- Consider the following options portfolio. You write an August expiration call option on IBM with exercise price $150. You write an August IBM put option with exercise price $145.a. Graph the payoff of this portfolio at option expiration as a function of IBM’s stock price at that time.b. What will be the profit/loss on this position if IBM is selling at $153 on the option expiration date? What if IBM is selling at $160? c. At what two stock prices will you just break even on your investment?d. What kind of “bet” is this investor making; that is, what must this investor believe about IBM’s stock price to justify this position?arrow_forwardConsider the following: your purchased a put option on JPM two months ago, with a strike price for the option of $138, and the option expires today. Suppose the stock price is $152. What is the exercise value?arrow_forwardYou have been given the following information on Claiborne Industries: Current stock price = $32 Option’s exercise price = $32 d1 = 0.1735 d2 = 0.02735 N(d)1 = 0.56960 N(d)2 = 0.51091 Time until expiration of option = 3 months, or 0.25 of a year Risk-free rate = 6% Variance of stock price = 0.09 Using the Black-Scholes Option Pricing Model, what would be the option’s value? Round intermediate calculations to 6 decimal places. Round your answer to two decimal places. $arrow_forward

- Call Options on a stock are available with strike prices of $35, $52.5 and $70, with the same expiration dates in 3 months. Their prices are $10, $5 and $1, respectively. Question Explain how the options can be used to create a Butterfly Spread. Show the graph with all details (premium, strike price, payoff line, etc).arrow_forwardSuppose you construct a strategy based on options on a stock that is currently selling for $100. The strategy is as follows: Buy one call option having an exercise price of $95. Sell two calls having an exercise price of $100. Buy one call option having an exercise price of $105. All of the options are written on the same stock and all have the same expiration date. Compute the payoff (the dollars you receive) from this strategy at the expiration date for each of the following alternative stocks prices: $90, $95, $98, $100, $102, $105, and $110. What additional information would be required to determine whether your strategy had been profitable? What is the name of this strategy?arrow_forwardThe Black-Scholes model is used by Bulldogs Inc. to value call options on the stock of National Inc. The following information was determined by the analyst:· The share price is P30.· The price of the option is at P32.· The risk-free rate is 3%.· The option matures in 6 monthsIn the formula of the current value of the call option under the Black-Scholes model, what is the exponent of “e” be?arrow_forward

- 1) Draw the binomial tree listing only the option prices at each node. Assume the following data on a 6-month call option, using 3-month intervals as the time period. K = $40, S = $37.90, r = 5.0%, σ = 0.35 2) Draw the binomial tree listing only the stock prices at each node. Assume the following data on a 6-month call option, using 3-month intervals as the time period. K = $70, S = $68.50, r = 6.0%, σ = 0.32 3) Draw the binomial tree listing only the option prices at each node. Assume the following data on a 6-month put option, using 3-month intervals as the time period. K = $40.00, S = $37.90, r = 5.0%, σ = 0.35 4) Using a binomial tree explanation, explain the situation in which an American option would alter the pricing of an option.arrow_forwardYou have the following information about LearnMore Inc.’s stock and a two-month call option with a strike price of $140.00. LearnMore Inc.’s current stock price is $100.00. You are using the multiperiod binomial option pricing model to find the value of the two-month option with two periods. ∏u∏u and ∏d∏d values given here apply to any period. Data Collected for LearnMore Inc. u 1.5032 d 0.5922 ∏u∏u 0.2357 ∏d∏d 0.3555 You work with a junior analyst to calculate the value of the option, and she submits her inferences to you. Which of the following points are true in the case of LearnMore Inc.’s stock options? Check all that apply. The option payoff if the stock goes up in two months will be $10.32. The value of the two-month call option with a strike price of $140.00 at the end of two months will be $2.43. The value of the call option will always remain $2.43, irrespective of the time until expiration. LearnMore Inc.’s stock price…arrow_forwardSuppose that both a call option and a put option have been written on a stock with an exerciseprice of $40. The current stock price is $42, and the call and put premiums are $3 and $0.75,respectively. Calculate the profit to positions of both the short call and the long put with an expiration day stock price of $43.arrow_forward

Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning

Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning