a.

To determine: The futures price for contract maturity dates on February 14, 2016; May 21 2016 and November 18, 2016 assuming that the interest rate is 3% per year, stock index- 2,000, dividend yield of 2.0%.

Introduction:

Spot-futures parity relationship: It shows the relationship between the futures price andthe spot price. Sometimes, there is a difference between the futures price andthe spot price. It may be due to changes in interest rates, expiry time and dividends paid. So, this difference has to be equated. The mathematical equation which balances the underlying price and its future price may be termed as spot-future parity.

a.

Answer to Problem 17PS

The future prices as on maturity date is as follows:

| Current date January 1, 2016 | 2000.00 |

| February 14, 2016 | 2002.40 |

| May 21, 2016 | 2022.93 |

| November 18,2016 | 2051.71 |

Explanation of Solution

Current date= January 1, 2016

Interest rate per year = 3%

Stock index pay dividend of 2% at 2000

Dividend yield=2%

From the given information, let us calculate the future price.

The formula to be used here is:

Where,

Spot price= Price of the stock in cash market;

rf= Risk -free rate of interest;

D=Dividend paid by the company.

We should be aware of the fact that T-Bill or treasury bills and Government securities carry risk-free interest rate.

Since the future price expires in a short time, the above formula needs to be modified. The modified formula is as follows:

Where,

x= number of expiry days;

Spot price= Price of the stock in cash market;

rf= Risk -free rate of interest;

D=Dividend paid by the company.

So, let us now calculate the future prices:-

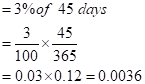

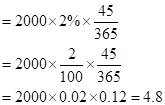

i) When the maturity date is February 14,2016

The risk-free interest rate is given for the whole year. Since we are given three different periods, we have to calculate number of days in each case.

In this case, Number of days= January 1,2016 to February 14, 2016

So now, we have to calculate the risk-free interest rate for 45 days.

In the same way, even the dividend date of 2% is given for the entire year.

So, the dividend earned for 45 days would be

So, let us now substitute the value in the given formula:

Hence the

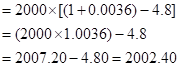

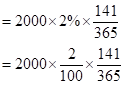

ii) When the maturity date is May 21,2016

In this case, Number of days= January 1,2016 to May 21, 2016

=January+February+March+April+21 days of May= 141 days

So now, we have to calculate the risk-free interest rate for 141 days.

In the same way, even the dividend date of 2% is given for the entire year.

So, the dividend earned for 141 days would be

So, let us now substitute the value in the given formula:

Hence the future value is 2022.932 when the maturity date is May 21, 2016.

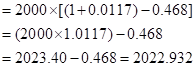

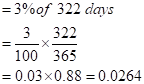

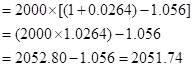

iii) When the maturity date is November 18, 2016.

In this case, Number of days= January 1,2016 to May 21, 2016

=January+February+March+April+May+June+July+August+September+October+18 days of November= 322 days

So now, we have to calculate the risk-free interest rate for 322 days.

In the same way, even the dividend date of 2% is given for the entire year.

So, the dividend earned for 322 days would be

So, let us now substitute the value in the given formula:

Hence the future value is 2051.74 when the maturity date is November 18, 2016.

b.

To determine: The term structure of future prices if the dividend yield is higher than the risk-free rate.

Introduction:

Dividend yield: It is supposed to be the amount of money paid by the company to its shareholders. Normally, dividend yield is calculated for one year of investment and is represented in terms of percentages.

b.

Answer to Problem 17PS

The future prices as on maturity date is as follows:

| February 14, 2016 | 1997.60 |

| May 21, 2016 | 2007.80 |

| November 18,2016 | 1982.40 |

Explanation of Solution

Current date= January 1, 2016

Interest rate per year = 3%

Stock index pay dividend of 2% at 2000

Dividend yield=2%

Let us consider the dividend yield to be 4%.

Let us now calculate the term structure of future prices if the dividend yield is 4%.

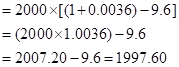

iv) When the maturity date is February 14,2016

The risk-free interest rate is given for the whole year. Since we are given three different periods, we have to calculate number of days in each case.

So now, we have to calculate the risk-free interest rate for 45 days.

From the above calculation now we are aware that number of days in this case =45 days and the risk-free interest rate for 45 days is 0.0036

The dividend date of 4% is given for the entire year.

So, the dividend earned for 45 days would be

So, let us now substitute the value in the given formula:

Hence the future value is 1997.60 when the maturity date is February 14, 2016.

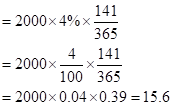

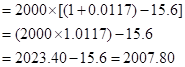

v) When the maturity date is May 21,2016

In this case, the number of days is 141 days and the risk-free interest rate for 141 days is 0.0117.

In the same way, even the dividend date of 4% is given for the entire year.

So, the dividend earned for 141 days would be

So, let us now substitute the value in the given formula:

Hence the future value is 2007.80 when the maturity date is May 21, 2016.

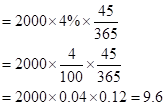

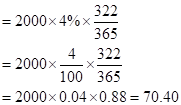

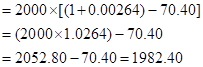

vi) When the maturity date is November 18, 2016.

In this case, the number of days is 322 days and the risk-free interest rate for 322 days is 0.0264.

In the same way, even the dividend date of 4% is given for the entire year.

So, the dividend earned for 322 days would be

So, let us now substitute the value in the given formula:

Hence the future value is 1982.40 when the maturity date is November 18, 2016.

We can conclude that an increase in dividend yield is showing a decrease in the future prices.

Want to see more full solutions like this?

Chapter 22 Solutions

INVESTMENTS (LOOSELEAF) W/CONNECT

- Suppose that, on 5 November 2020, you opened a short position in a two-year futures contract on the Tesla stock. The share price at the beginning of the contract was $146, and the initial futures price was equal to a theoretical two-year forward price. Assume the following: initial margin of 40% of the futures value, maintenance margin of 32% of the futures value, 3% flat interest rate, continuous compounding, no withdrawals of the excess margin. Next, suppose that, on 1 November 2022, the Tesla stock is priced at $228 per share, and it goes down by 1% daily over 2nd, 3rd and 4th November. Suppose further that, on 1 November 2022, you have received a margin call from your broker (this was your first margin call during this contract) and had to make an instant adjustment to your margin account. Your position in this contract is closed on 4 November 2022. How can you assess your overall profit or loss? Would your overall profit/loss from 1) change if, on 5 November 2020, you had…arrow_forwardSuppose that, on 5 November 2020, you opened a short position in a two-year futures contract on the Tesla stock. The share price at the beginning of the contract was $146, and the initial futures price was equal to a theoretical two-year forward price. Assume the following: initial margin of 40% of the futures value, maintenance margin of 32% of the futures value, 3% flat interest rate, continuous compounding, no withdrawals of the excess margin. Next, suppose that, on 1 November 2022, the Tesla stock is priced at $228 per share, and it goes down by 1% daily over 2nd, 3rd and 4th November. Suppose further that, on 1 November 2022, you have received a margin call from your broker (this was your first margin call during this contract) and had to make an instant adjustment to your margin account. Calculate the value of your position in this contract at a close of each day between 1-4 November 2022. Show and explain each step of your derivations.arrow_forwardSuppose that, on 5 November 2020, you opened a short position in a two-year futures contract on the Tesla stock. The share price at the beginning of the contract was $146, and the initial futures price was equal to a theoretical two-year forward price. Assume the following: initial margin of 40% of the futures value, maintenance margin of 32% of the futures value, 3% flat interest rate, continuous compounding, no withdrawals of the excess margin. Next, suppose that, on 1 November 2022, the Tesla stock is priced at $228 per share, and it goes down by 1% daily over 2nd, 3rd and 4th November. Suppose further that, on 1 November 2022, you have received a margin call from your broker (this was your first margin call during this contract) and had to make an instant adjustment to your margin account. Show how the balance on your margin account was changing over this period (i.e., 1-4 November 2022).arrow_forward

- Demonstrate how a Margin Account operates for both the Long and the Short futures position using the following information: The initial margin is R30. The initial Futures price is R100. On Day 1 the price drops to R90. On Day 2 the price rises to R95.arrow_forwardConsider Commodity Z, which has both exchange-traded futures and option contracts associated with it. As you look in today's paper, you find the following put and call prices for options that expire exactly six months from now: Exercise Price Put Price Call Price $ 40.00 $ 0.59 $ 8.73 $ 45.00 $ 1.93 $ - $ 50.00 $ - $ 2.47 a. Assuming that the futures price of a six-month contract on Commodity Z is Fo, 0.5 = $48, what must be the price of a put with an exercise price of $50 in order to avoid arbitrage across markets? Similarly, calculate the "no arbitrage" price of a call with an exercise price of $45. In both calculations, assume that the yield curve is flat and the annual risk-free rate is 6 percent. b. What is the "no arbitrage" price differential that should exist between the put and call options having an exercise price of $40? Is this…arrow_forwardAn index level of 1,000, what is the value of each contract? If a long stock index futures position on S& P 500 index futures at 1, 051 and has an index of 1, 058 at the settlement date, how much would be the trader’s gain? Complete Solution.arrow_forward

- You placed $120,000 in your future trading account have just bought your first HSI June 2023 futures contract today @ 19,652, at market close the HSI June 2023 future closed at 19,534. Currently the initial margin for HSI is $101,944, the maintenance margin is $81,555. HSI futures is $50 per index point. What is you margin account balance as of market closed today? Please write out the detailed calculation stepsarrow_forwardYou find the following information in December 2019. Assume the T-bill maturity and futures delivery are on the same day. Ignore transactions costs. Treasury Bill Maturity DTM Bid Asked Mar 20 90 1.19 1.18 Index Futures S&P 500 Index (CME) – 250 x index, cents per unit Open High Low Settle Mar 20 3324 3326 3320 3322 S&P 500 closed at $3329 on the same day. Suppose that if you buy one unit of S&P 500 index today, you will be entitled to a 2% dividend yield in March. Design a zero net investment arbitrage strategy involving: (1) buying the index for $3329, (2) shorting the futures for no cash now, (3) and borrowing $3329 at the spot rate. Show your profit per one futures contract (250 units of the index). a. $12,395 b. $10,114 c. $18,948 d. $11,639arrow_forwardA one-year gold futures contract is selling for $1,247. Spot gold prices are $1,200 and the one-year risk-free rate is 2%. a) According to spot-futures parity, what should be the futures price? b) What risk-free strategy can investors use to take advantage of the futures mispricing, and what would be the profits from that strategy?arrow_forward

- Consider the following prices, volume and open interest for gold futures contracts. Contract size: 100 oz Price units: $/oz (a) Which contract reached the highest price on this trading day? What was its contract value at that price? (b) Why is the high price equal to the low price for the contract expiring in October 2022?arrow_forwardIf the initial speculative margin of a futures contract is $2,000, the maintenance margin is $1,800 and your trading account balance has increased to $2,300, how much must you deposit to comply with your margin requirement?arrow_forwardSuppose the ASX200 Index is currently at 7,406, the expected dividend yield on the index is 2 percent per year, and the risk-free rate is 0.35%. Using the current price of ASX200 futures contracts that expire in six months recommend a program trading strategy for buying or selling the futures?arrow_forward