The impact of the elasticity on the demand and supply of the agricultural products and on its quantity and price .

Explanation of Solution

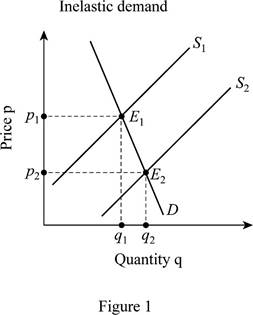

Due to the inelastic nature of the demand for the agricultural products, the shift in the supply curve of the agricultural products leads to a large change in the equilibrium prices with a small change in the

In Figure 1, the demand curve is relatively inelastic as compared to the supply curve. The new equilibrium (E2) shows that there has been a small change in the quantity of the demand with the drastic change in the price.

The volatile nature of the exports increases the instability of the demand for the agricultural products. The exports change from year to year; so, there is an increase in the instability for the demand of the agricultural products.

Concept Introduction

Supply and demand of the agricultural products: The demand for the agricultural products is inelastic in nature because a large change in the prices has a very small impact on the demand for the agricultural products. The supply of the agricultural products is elastic in nature.

Want to see more full solutions like this?

Chapter 22 Solutions

ECONOMICS W/CONNECT+20 >C<

- ADVANCED ANALYSIS Assume that demand for a commodity is represented by the equation P=80−2Qd.P=80−2Qd. Supply is represented by the equation P=−20+2Qs,P=−20+2Qs, where Qd and Qs are quantity demanded and quantity supplied, respectively, and P is price.Instructions: Round your answer for price to 2 decimal places and enter your answer for quantity as a whole number. Using the equilibrium condition Qs = Qd, solve the equations to determine equilibrium price and equilibrium quantity.arrow_forward1. Much of the demand for U.S. agricultural output comes from other countries. Suppose that the total demand for wheat in the U.S. wheat market is QDT = 3,244 – 283P, where P is the price measured in dollars per bushel and Q is the quantity of wheat expressed in millions of bushels per year. Of the total demand, total domestic demand was QD,US = 1,700 – 107P. Total supply of wheat in the U.S. market is QST = 1,944 + 207P. As a result of the ongoing trade war with China, suppose the export demand for wheat falls by 40 percent. a. U.S. farmers are concerned about this drop in export demand. How does this drop in export demand impact the market price of wheat in the U.S.? Do farmers have much reason to worry? Explain/support your answer. b. How does the reduction in export demand affect U.S. consumer surplus in the wheat market? Illustrate and explain. c. Now, suppose the U.S. government wants to buy enough wheat to raise the price to $3.50 per bushel. With the drop in export…arrow_forwardWill the equilibrium price of orange juice increase or decrease in each of the following situations? LO7a. A medical study reporting that orange juice reduces cancer is released at the same time that a freak storm destroys half of the orange crop in Florida. The prices of all beverages except orange juice fall in half while unexpectedly perfect weather in Florida results in an orange crop that is 20 percent larger than normal.arrow_forward

- Next, complete the following graph, labeled Scenario 2, by shifting the supply and demand curves in the same way that you did on the Scenario 1 graph. PRICE (Dollars per pen) 10 9 8 co LO 5 + 3 2 1 0 0 1 Price Quantity 2 Equilibrium Object True Scenario 2 3 False Supply 4 5 6 7 QUANTITY (Millions of pens) Demand Scenario 1 8 9 Compare both the Scenario 1 and Scenario 2 graphs. Notice that after completing both graphs, you can now see a difference between them that wasn't apparent before the shifts because each graph indicates different magnitudes for the supply and demand shifts in the market for pens. 10 Use the results of your answers on both the Scenario 1 and Scenario 2 graphs to complete the following table. Begin by indicating the overall change in the equilibrium price and quantity after the shift in demand or supply for each shift-magnitude scenario. Then, in the final column, indicate the resulting change in the equilibrium price and quantity when supply and demand shift in…arrow_forwardADVANCED ANALYSIS Assume that demand for a commodity is represented by the equation P = 80 – 2Qd. Supply is represented by the equation P = -20 + 2Qs, where Qgand Qg are quantity demanded and quantity supplied, respectively, and Pis price. Instructions: Round your answer for price to 2 decimal places and enter your answer for quantity as a whole number. Using the equilibrium condition Qs = Qd, solve the equations to determine equilibrium price and equilibrium quantity. Equilibrium price = $ Equilibrium quantity = unitsarrow_forwardADVANCED ANALYSIS Assume that demand for a commodity is represented by the equation P = 20 – 2Qd. Supply is represented by the equation P = -5 + 3Qs, where Qgand Qs are quantity demanded and quantity supplied, respectively, and Pis price. Instructions: Round your answer for price to 2 decimal places and enter your answer for quantity as a whole number. Using the equilibrium condition Qs= Qd solve the equations to determine equilibrium price and equilibrium quantity. Equilibrium price = $ Equilibrium quantity = unitsarrow_forward

- 4. How will each of the following changes in demand and/or supply affect equilibrium price and equilibrium quantity in a competitive market; that is, do price and quantity rise, fall, or remain unchanged, or are the answers indeterminate be- cause they depend on the magnitudes of the shifts? Use sup- ply and demand to verify your answers. LO3.5 a. Supply decreases and demand is constant. b. Demand decreases and supply is constant. c. Supply increases and demand is constant. d. Demand increases and supply increases. e. Demand increases and supply is constant. f. Supply increases and demand decreases.arrow_forwardThe data in the table below are for kilos of prawns. Price $24 26 28 30 32 34 36 Quantity Demanded 270 250 230 190 170 150 New equilibrium price: Quantity Supplied (before tax) LA 210 230 240 250 260 270 a) What is the present equilibrium price and quantity? Equilibrium price: $ Equilibrium quantity: b) Complete the Quantity Supplied (after tax) that results. c) What will be the new equilibrium price and quantity? New equilibrium quantity: Quantity Supplied (after tax) Suppose that the government Introduces a $6 excise tax on prawns. 4arrow_forward27) Of the collection of supply and demand diagrams in Figure 2.2, which one shows the result of a decrease in the price of a substitute for a good? Figure 2 P" P FE Q*Q® Q Qº Figure 3 Figure 4 S P₁ P P₁ p. P Figure 1 Q" Q Figure 2.2 A) Figure 1 B) Figure 2 C) Figure 3 D) Figure 4 18 Q't lö 27)arrow_forward

- A company was selling its product at a price of $8 a unit, and sold 18 units. Then they raised the price to $11 and sold 14 units. In this case, the lost revenue due to the quantity effect is _________ and the new revenue due to the price effect is $36.5; $44 O $36.5; $42 O $32; $42 $32; $44arrow_forward5. Show how a change in the price of one good affects the supply of another. Use the graph to show how an increase in the price of organic onions would shift the demand curve, supply curve, or both curves in the market for tomatoes. Assume that onions and tomatoes are neither complements nor substitutes. Market for Tomatoes 10 9. Supply 8 7 4 Demand 1 4 8 10 12 14 16 18 20 Quantity (Ibs) LO 3. 2. Price ($)arrow_forwardBy 2021, automobile market analysts expect that the demand for electric cars will increase as buyers become more attracted to cost-saving vehicles. However, the costs of producing electric cars may increase because of higher costs for inputs (e.g., machinery and labour costs elements). In your opinion, what will be the expected impact of these changes on the market equilibrium price and quantity for electric cars? Hint: Demand & Supply curves are normal in shape) O a. Unambiguously higher quantity, and equilibrium price may be higher or lower O b. Unambiguously higher price, and equilibrium quantity may be higher or lower O c. Unambiguously higher equilibrium price and quantity O d. We cannot form any unambiguous expectations for either price or quantityarrow_forward

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education