Videos

Variance interpretation

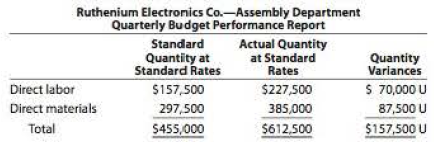

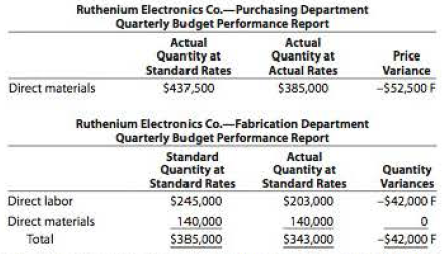

You have been asked to investigate some cost problems in the Assembly Department of Ruthenium Electronics Co., a consumer electronics company. To begin your investigation, you have obtained the following budget performance report for department for the last quarter:

The following reports were also obtained:

You also interviewed the Assembly Department supervisor. Excerpts from the interview follow:

Q: What explains the poor performance in your department?

A: Listen, you've got to understand what it's been like in this department recently. Lately, it seems no matter how hard we try, we can't seem to make the standards. I'm not sure what is going on, but we've been having a lot of problems lately.

Q: What kind of problems?

A: Well, for instance, all this quarter we've been requisitioning purchased parts from the material storeroom, and the pans just didn't fit together very well I'm not sure what is going on. but during most of this quarter we've had to scrap and sort purchased pans—just to get our assemblies put together. Naturally, all this takes time and material. And that's not all.

Q: Go on.

A: All this quarter, the work that we've been receiving from the Fabrication Department has been shoddy. I mean, maybe around 20% of the stuff that comes in from Fabrication just can't be assembled. The fabrication is all wrong. As a result, we've had to scrap and rework a lot of the stuff. Naturally, this has just shot our quantity variances.

Interpret the variance reports in light of the comments by the Assembly Department supervisor.

Trending nowThis is a popular solution!

Chapter 22 Solutions

Bundle: Financial & Managerial Accounting, Loose-leaf Version, 13th + CengageNOWv2, 1 term (6 months) Printed Access Card Corporate Financial ... Access Card for Managerial Accounting, 13th

- The controller for Muir Companys Salem plant is analyzing overhead in order to determine appropriate drivers for use in flexible budgeting. She decided to concentrate on the past 12 months since that time period was one in which there was little important change in technology, product lines, and so on. Data on overhead costs, number of machine hours, number of setups, and number of purchase orders are in the following table. Required: 1. Calculate an overhead rate based on machine hours using the total overhead cost and total machine hours. (Round the overhead rate to the nearest cent and predicted overhead to the nearest dollar.) Use this rate to predict overhead for each of the 12 months. 2. Run a regression equation using only machine hours as the independent variable. Prepare a flexible budget for overhead for the 12 months using the results of this regression equation. (Round the intercept and x-coefficient to the nearest cent and predicted overhead to the nearest dollar.) Is this flexible budget better than the budget in Requirement 1? Why or why not?arrow_forwardBusiness Decision Case Porter Corporation has just hired Bill Harlow as its new controller. Al- though Harlow has had little formal accounting training, he professes to be highly experienced, having learned accounting “the hard way” in the field. At the end of his first month’s work, Harlow prepared the following performance report: PORTER CORPORATION Performance Report for the Month of June, 2018 Total Actual Costs Total Budgeted Costs Variances Direct materials............................ $216,630 $237,600 $20,970 F Direct labor ............................... 119,340 132,000 12,660 F Variable overhead ......................... 63,000 66,000 3,000 F Fixed overhead............................ 184,000 184,000 $582,970 $619,600 $36,630 F In his presentation at Porter’s month-end management meeting, Harlow indicated that things were going “fantastically.” “The figures indicate,” he said, “that the firm is beating its budget in all cost categories.” This good news made everyone at the…arrow_forwardThink It Through: Don't "Skirt" the Issue E open You run a fabric store and order materials through a supplier. At the end of the month, you review your materials cost and discover that your direct materials price and quantity variances produced unfavorable results. What could be attributed to these unfavorable outcomes? How would these unfavorable outcomes impact the total direct materials variance?arrow_forward

- Suppose for a moment that you are a production manager in a manufacturing company and you just received a poor performance rating for not meeting your budget. If you were slightly over budget, identify at least two possible reasons for the budget variance. Please provide specific examples.arrow_forwardPrepare a performance report that compares flexible budget and actual costs for the period just ended (i.e., the report that the general manager likely used when assessing Kellerman’s performance).arrow_forward1. Which is not the factor causing unfavourable direct material usage? Select one: a. Change in rate of utility costs b. Faulty machine used in the production process c. Ineffective supervision d. Inexperienced direct labour 2.A flexible budget is a budget that: Select one: a. contains only variable production costs. b. is updated with actual costs as they occur during the period. c. is prepared using a computer spreadsheet application. d. is updated to reflect the actual level of activity during the period.arrow_forward

- You work for a manufacturing company and have just completed the budget process for the upcoming business year. At the end of the first quarter, you take the actuals and compare them to the budget. You notice there are differences that need explanation and create the static and flexible budget variances. You present this to management and they request you to explain the variances in more detail. You go and create the Flexible Budget Performance Report and present this. You also need to explain the reasons for the variances and who is responsible. Explain the calculations used to create this report. Explain why the variances using standard costs better reflect the actual variance and how to determine who is responsible for each variancearrow_forwardStandard Costing; Variance Analysis; Strategic Considerations In a Wall Street Journalarticle, the author notes that various retailers in the United States (e.g., Meijer, Gap, and OfficeDepot) are turning to consulting firms, such as Accenture, to develop engineered labor standards forcashiers and other retail workers. Monitoring labor-hour consumption (i.e., labor efficiency) undersuch standards involves timing from the first scan of an item in a customer’s purchase to the production of a sales receipt for the customer. A commentator for Meijer states that the system now in usehas enabled the company to more efficiently staff stores while concomitantly increasing customerservice ratings. A representative from another client of Accenture states that the new system allowsthe retailer to determine how many workers to schedule at a given time, resulting in a labor-costreduction of approximately 8%. Engineered standards were developed many years ago in a manufacturing environment, at…arrow_forwardIn the book Advanced Managerial Accounting, Robert P. Magee discusses monitoring cost variances. A cost variance is the difference between a budgeted cost and an actual cost. Magee describes the following situation: Michael Bitner has responsibility for control of two manufacturing processes. Every week he receives a cost variance report for each of the two processes, broken down by labor costs, materials costs, and so on. One of the two processes, which we'll call process A , involves a stable, easily controlled production process with a little fluctuation in variances. Process B involves more random events: the equipment is more sensitive and prone to breakdown, the raw material prices fluctuate more, and so on. "It seems like I'm spending more of my time with process B than with process A," says Michael Bitner. "Yet I know that the probability of an inefficiency developing and the expected costs of inefficiencies are the same for the two processes. It's just the magnitude of…arrow_forward

- asked that you review the company's costing system and "do what you can to help us get better control of our manufacturing overhead costs." You find that the company has never used a flexible budget, and you suggest that preparing such a budget would be an excellent first step in overhead planning and control. After much effort and analysis, you determined the following cost formulas and gathered the following actual cost data for March: Utilities Maintenance Supplies Indirect labor Depreciation Cost Formula $16,000+ $0.19 per machine-hour $38,900 $1.30 per machine-hour $0.40 per machine-hour $94,000+ $1.20 per machine-hour $67,500 Actual Cost in March $ 22,390 Required: 1. Calculate the activity variances for March. 2. Calculate the spending variances for March. $60,000 $ 8,200 $120, 100 $ 69,200 During March, the company worked 19,000 machine-hours and produced 13,000 units. The company had originally planned to work 21,000 machine-hours during March.arrow_forward[1] The purpose of identifying manufacturing variances and assigning their responsibility to a person/department should be to A. Trace the variances to finished goods so that the inventory can be properly valued at year-end. B. Determine the proper cost of the products produced so that selling prices can be adjusted accordingly. C. Use the knowledge about the variances to promote learning and continuous improvement in the manufacturing process D. Pinpoint fault for operating problems in the organization.arrow_forwardPreparing a flexible budget performance report Murphy Company managers received the following incomplete performance report: Complete the performance report. Identify the employee group that may deserve praise and the group that may be subject to criticism. Give your reasoning.arrow_forward

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning