Concept explainers

Videos

PROBLEM 3-12 Predetermined Overhead Rate; Disposing of Under applied or over appliedoverhead

L03-4

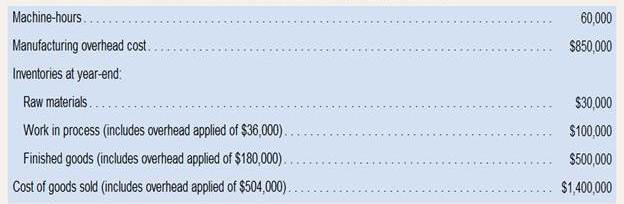

Luzadis Company makes furniture using the latest automated technology .The company uses a

During the year, a large quantity of furniture on the market resulted in cutting back production and a buildup of furniture in the company's warehouse. The company's cost records overhead the following actual cost Cid operating data for the year

Required:

1. Compute the under applied or over applied overhead.

2. Assume that the comp,' closes any under applied or over applied overhead to Cost of Goods Sold Prepare the appropriate

3. Assume that the company allocates under applied or over applied overhead proportionally to Work in Process, Finished Goods Cost of Goods Sold Prepare the appropriate journal

4 Finished Goods, Id Cost being closed to Cost of Goods Sold?

Want to see the full answer?

Check out a sample textbook solution

Chapter 3 Solutions

LSC BARUCH COLL COMBO LL INTRO MANAGERI

- Amounts for materials Big Timber Furniture Company manufactures furniture. Big Timber Furniture uses a job order cost system. Balances on June 1 from the materials ledger are as follows: The materials purchased during June are summarized from the receiving reports as follows: Materials were requisitioned to individual jobs as follows: The glue is not a significant cost, so it is treated as indirect materials (factory overhead). a.Determine the total purchase of materials in June. b.Determine the amounts of materials transferred to Work in Process and Factory Overhead during June. c.Determine the June 30 balances that would be shown in the materials ledger accounts.arrow_forwardOverhead application rate Roll Tide Manufacturing Inc. uses a job order cost system and standard costs. It manufactures one product, whose standard cost follows: The standards are based on normal capacity of 2,700 direct labor hours. Actual activity for March follows: Required: 1. Compute the variable and fixed factory overhead rates per unit. 2. Compute the variable and fixed overhead rates per direct labor hour. 3. Determine the total fixed factory overhead based on normal capacity.arrow_forwardPREDETERMINED FACTORY OVERHEAD RATE Marston Enterprises calculates a predetermined factory overhead rate so that factory overhead may be applied to production during the month. It calculates the overhead using three different methods and then decides which one to use. Total estimated factory overhead costs are 600,000. Total estimated direct labor hours are 30,000. Total estimated direct labor costs are 1,200,000. Total machine hours are estimated to be 200,000. Calculate the predetermined overhead application rates based on (1) direct labor hours, (2) direct labor costs, and (3) machine hours.arrow_forward

- JOB ORDER COSTING WITH UNDER- AND OVERAPPLIED FACTORY OVERHEAD M. Evans Sons manufactures parts for radios. For each job order, it maintains ledger sheets on which it records direct labor, direct materials, and factory overhead applied. The factory overhead control account contains postings of actual overhead costs. At the end of the month, the under- or over applied factory overhead is charged to the cost of goods sold account. Factory overhead is applied on the basis of direct labor hours. For Job Nos. 101, 102,103, and 104, direct labor hours are 12, 000, 10,000, 11, 000, and 18,000, respectively. The overhead application rate is 1.20/direct labor hour. (a) Purchased raw materials on account, 50,000. (b) Issued direct materials: (c) Issued indirect materials to production, 8,000. (d) Incurred direct labor costs: (e) Charged indirect labor to production, 15,000. (f) Paid electricity bill, taxes, and repair fees for the factory and charged to production, 8,000. (g) Depreciation expense on factory equipment, 30,000. (h) Applied factory overhead to Job Nos. 101104 using the predetermined factory overhead rate (see above). (i) Finished Job Nos. 101103 and transferred to the finished goods inventory account as products N, O, and P. (j) Sold products N and for 50,000 and 45,400, respectively. (k) Transferred under- or over applied factory overhead balance to the cost of goods sold account. REQUIRED 1. Prepare general journal entries to record transactions (a) through (k). 2. Post the entries to the work in process and finished goods accounts only and determine the ending balances in these accounts. 3. Compute the balance in the job cost ledger and verify that this balance agrees with that in the work in process control account.arrow_forwardOverhead application rate Creole Manufacturing Inc. uses a job order cost system and standard costs. It manufactures one product, whose standard cost follows: The standards are based on normal capacity of 2,400 direct labor hours. Actual activity for October follows: Required: 1. Compute the variable and fixed factory overhead rates per unit. 2. Compute the variable and fixed overhead rates per direct labor hour. 3. Determine the total fixed factory overhead based on normal capacity.arrow_forwardUse the following information for Brief Exercises 4-27 and 4-28: Quillen Company manufactures a product in a factory that has two producing departments, Cutting and Sewing, and two support departments, S1 and S2. The activity driver for S1 is number of employees, and the activity driver for S2 is number of maintenance hours. The following data pertain to Quillen: Brief Exercises 4-27 (Appendix 4B) Assigning Support Department Costs by Using the Direct Method Refer to the information for Quillen Company above. Required: 1. Calculate the cost assignment ratios to be used under the direct method for Departments S1 and S2. (Note: Each support department will have two ratiosone for Cutting and the other for Sewing.) 2. Allocate the support department costs to the producing departments by using the direct method.arrow_forward

- JOB ORDER COSTING WITH UNDER- AND OVERAPPLIED FACTORY OVERHEAD M Evans Sons manufactures parts for radios. For each job order, it maintains ledger sheets on which it records direct labor, direct materials, and factory overhead applied. The factory overhead control account contains postings of actual overhead costs. At the end of the month, the under- or overapplied factory overhead is charged to the cost of goods sold account. Factory overhead is applied on the basis of direct labor hours. For Job Nos. 101, 102, 103, and 104, direct labor hours are 12,000, 10,000, 11,000, and 18,000, respectively. The overhead application rate is 1.20/direct labor hour (a) Purchased raw materials on account, 50,000. (b) Issued direct materials: (c) Issued indirect materials to production, 8,000. (d) Incurred direct labor costs: (e) Charged indirect labor to production, 15,000. (f) Paid electricity bill, taxes, and repair fees for the factory and charged to production, 8,000. (g) Depreciation expense on factory equipment, 30,000. (h) Applied factory overhead to Job Nos. 101-104 using the predetermined factory overhead rare (see above). (i) Finished Job Nos. 101-103 and transferred to the finished goods inventory account as products N, O, and P. (j) Sold products N and O for 50,000 and 45,400, respectively. (k) Transferred under- or overapplied factory overhead balance to the cost of goods sold account. REQUIRED 1. Prepare general journal entries to record transactions (a) through (k). Make compound entries for (b), (d), and (h), with separate debits for each job. 2. Post the entries to the work in process and finished goods T accounts only and determine the ending balances in these accounts. 3. Compute the balance in the job cost ledger and verify that this balance agrees with that in the work in process control account.arrow_forwardNEED A, B, C, D, E, AND F. Sorrento Products uses a job costing accounting system for its manufacturing costs. A predetermined overhead rate based on machine-hours is used to apply overhead to individual jobs. An estimate of overhead costs at different volumes was prepared for the current year as follows. Machine-hours 198,000 212,000 258,000 Variable overhead costs $ 752,400 $ 805,600 $ 980,400 Fixed overhead costs 1,780,800 1,780,800 1,780,800 Total overhead $ 2,533,200 $ 2,586,400 $ 2,761,200 The expected volume is 212,000 machine-hours for the entire year. The following information is for March, when Jobs 302 and 304 were completed: Inventories, March 1 Raw materials and supplies $ 92,900 Work in process (Job 302) 198,500 Finished goods 499,000 Purchases of raw materials and supplies Raw materials $ 1,363,400 Supplies 177,200 Materials and supplies requisitioned for production Job 302 $ 621,500 Job 304 526,300 Job 305…arrow_forwardQUESTION 10 Lawn and Order Company manufactures industrial sprinklers and uses an activity-based costing system to allocate overhead to its products. Each sprinkler consists of 6 separate parts totaling $3 in direct materials, $2 in direct labor and requires 1 hour of machine time to produce. Additional information follows Overhead Cost Pools Pre-determined Overhead Rate Materials handling Number of parts $0.40 per part Machining Machine hours $1.50 per machine hour Assembling Inspecting Number of parts $0.40 per part Number of finished units $0.30 per finished unit Determine the amount of overhead allocated to each sprìnkler. Round your answer to 2 decimal placesarrow_forward

- S Activity Cost Pool Labor-related Purchase orders Product testing Template etching General factory Activity Cost Pool Labor-related (DLHS) Activity Measure Direct labor-hours Number of orders Number of tests Number of templates Machine-hours Product A Product B Product C Product D Cost $ 19,250 $ 1,820 $ 6,320 $ 960 $ 68,600 Total Overhead Cost 2. The expected activity for the year was distributed among the company's four products as follows: Expected Activity 1,375 DLHS Expected Activity Product A Product B Product C Product D 300 650 125 300 20 65 180 190 Purchase orders (orders) Product testing (tests) 65 0 80 Template etching (templates) 250 0 26 10 4 General factory (MHs) 3,800 2,000 1,200 2,800 Using the ABC data, determine the total amount of overhead cost assigned to each product. 455 orders 395 tests 40 templates S 9,800 MHsarrow_forwardQuestion Content Area Blue Ridge Marketing Inc. manufactures two products, A and B. Presently, the company uses a single plantwide factory overhead rate for allocating overhead to products. However, management is considering moving to a multiple department rate system for allocating overhead. The following table presents information about estimated overhead and direct labor hours. Overhead DirectLabor Hours (dlh) Product A B Painting Dept. $248,000 10,000 dlh 16 dlh 4 dlh Finishing Dept. 72,000 10,000 4 16 Totals $320,000 20,000 dlh 20 dlh 20 dlh The overhead from both production departments allocated to each unit of Product A if Blue Ridge Marketing Inc. uses the multiple production department factory overhead rate method is a.$396.80 per unit b.$214.40 per unit c.$320.00 per unit d.$425.60 per unitarrow_forwardQUESTION 1C (TOPIC 3) North Network Sdn Bhd (NNSB) makes custom made furniture from quality woods. The company uses a job-order costing system and predetermined overhead rates to apply manufacturing overhead cost to jobs. Currently, NNSB uses a plantwide overhead rate based on direct labor costs in estimating the company manufacturing overhead. The following estimated data have been made by NNSB at the beginning of the year 2018: Department Costs Designing Machining Furnishing Direct labor hours 30,000 60,000 40,000 Machine hours 20,000 40,000 30,000 Direct labor costs RM150,000 RM100,000 RM200,000 Direct materials costs RM190,000 RM400,000 RM250,000 Manufacturing overhead costs RM270,000 RM400,000 RM50,000 Job 118 was started on 1 January 2018 and completed on 28 February 2018. NNSB’s cost records shown the following information on the Job 118: Department Costs Designing Machining…arrow_forward

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Survey of Accounting (Accounting I)AccountingISBN:9781305961883Author:Carl WarrenPublisher:Cengage Learning

Survey of Accounting (Accounting I)AccountingISBN:9781305961883Author:Carl WarrenPublisher:Cengage Learning College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning, College Accounting, Chapters 1-27 (New in Account...AccountingISBN:9781305666160Author:James A. Heintz, Robert W. ParryPublisher:Cengage Learning

College Accounting, Chapters 1-27 (New in Account...AccountingISBN:9781305666160Author:James A. Heintz, Robert W. ParryPublisher:Cengage Learning Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Financial & Managerial AccountingAccountingISBN:9781337119207Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial & Managerial AccountingAccountingISBN:9781337119207Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning