Videos

Accrual basis of accounting

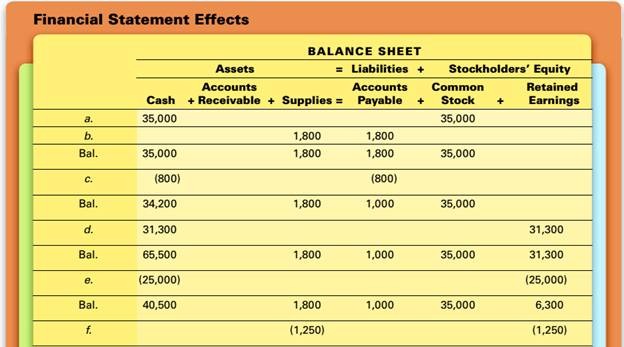

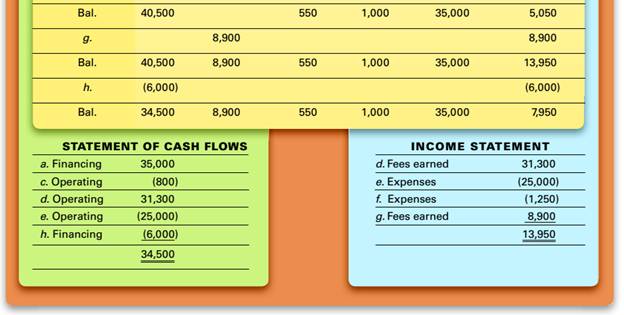

Margie Van Epps established Health Services, P.C., a professional corporation, in March of the current year, Health Services offers healthy living advice to its clients. The effect of each transaction on the balance sheet and the balances after each transaction for March are as follows. Each increase or decrease in

a. Describe each transaction.

b. What is the amount of the net income for March?

Trending nowThis is a popular solution!

Chapter 3 Solutions

Survey of Accounting (Accounting I)

Additional Business Textbook Solutions

Fundamentals of Cost Accounting

Advanced Financial Accounting

Horngren's Cost Accounting: A Managerial Emphasis (16th Edition)

Fundamentals Of Cost Accounting (6th Edition)

Intermediate Accounting

Managerial Accounting (5th Edition)

- Financial statements Seth Feye established Reliance Financial Services on July 1, 20Y2. Reliance Financial Services offers financial planning advice to its clients. The effect of each transaction and the balances after each transaction for July follow: Instructions 1. Prepare an income statement for the month ended July 31, 20Y2. 2. Prepare a statement of stockholders equity for the month ended July 31, 20Y2. 3. Prepare a balance sheet as of July 31, 20Y2. 4. (Optional) Prepare a statement of cash flows for the month ending July 31, 20Y2.arrow_forwardTransactions Interstate Delivery Service is owned and operated by Katie Wyer. The following selected transactions were completed by Interstate Delivery during May: 1. Received cash in exchange for common stock, 18,000. 2. Paid advertising expense, 4,850. 3. Purchased supplies on account, 2,100. 4. Billed customers for delivery services on account, 14,700. 5. Received cash from customers on account, 8,200. Indicate the effect of each transaction on the following accounting equation elements: Assets, Liabilities, Common Stock, Dividends, Revenue, and Expense. To illustrate, the answer to (1) follows: (1) Asset (Cash) increases by 18,000; Common Stock increases by 18,000.arrow_forwardEFFECTS OF TRANSACTIONS (BALANCE SHEET ACCOUNTS) Jon Wallace started a business. During the first month (March 20--), the following transactions occurred. Show the effect of each transaction on the accounting equation: Assets= Liabilities + Owners Equity. After each transaction, show the new account totals. (a) Invested cash in the business, 30,000. (b) Bought office equipment on account, 4,500. (c) Bought office equipment for cash, 1,600. (d) Paid cash on account to supplier in transaction (b), 2,000. EFFECTS OF TRANSACTIONS (REVENUE, EXPENSE, WITHDRAWALS) This exercise is an extension of Exercise 2-3B. Lets assume Jon Wallace completed the following additional transactions during March. Show the effect of each transaction on the basic elements of the expanded accounting equation: Assets = Liabilities + Owners Equity (Capital Drawing + Revenues Expenses). After transaction (k), report the totals for each element. Demonstrate that the accounting equation has remained in balance. (e) Performed services and received cash, 3,000. (f) Paid rent for March, 1,000. (g) Paid March phone bill, 68. (h) Jon Wallace withdrew cash for personal use, 800. (i) Performed services for clients on account, 900. (j) Paid wages to part-time employee, 500. (k) Received cash for services performed on account in transaction (i), 500.arrow_forward

- Trial Balance The following account titles, arranged in alphabetical order, are from the records of Hadley Realty Corporation. The balance in each account is the normal balance for that account. The balances are as of December 31, after adjusting entries have been made. Prepare an adjusted trial balance, listing the accounts in the following order: (1) assets; (2) liabilities; (3) stockholders equity accounts, including dividends; (4) revenues; and (5) expenses.arrow_forwardAccounts Used to Record Transactions A list of accounts, with an identifying number for each, is provided. Following the list of accounts is a series of transactions entered into by a company during its first year of operations. Required For each transaction, indicate the account or accounts that should be debited and credited. Cash Accounts Receivable Prepaid Insurance Office Supplies Automobiles Land Accounts Payable Income Taxes Payable Notes Payable Capital Stock Retained Earnings Service Revenue Wage and Salary Expense Utilities Expense Income Tax Expensearrow_forwardIdentify the financial statement on which each of the following accounts would appear: the income statement (IS), the retained earnings statement (RE), or the Balance Sheet (BS). A. Insurance Expense B. Accounts Receivable C. Office Supplies D. Sales Revenue E. Common Stock F. Notes Payablearrow_forward

- Transactions Interstate Delivery Service is owned and operated by Katie Wyer. The following selected transactions were completed by Interstate Delivery during May: 1. Received cash in exchange for common stock, 18,000. 2. Paid advertising expense, 4,850. 3. Purchased supplies on account, 2,100. 4. Billed customers for delivery services on account, 14,700. 5. Received cash from customers on account. 8,200. Indicate the effect of each transaction on the following accounting equation elements: Assets, Liabilities, Common Stock, Dividends, Revenue, and Expense. To illustrate, the answer to (1) follows: (1) Asset (Cash) increases by 18,000: Common Stock increases by 18,000.arrow_forwardPURPOSE OF ACCOUNTING Match the following users with the information needed. 1. Ownersa. Whether the firm can pay its bills on time 2. Managersb. Detailed, up-to-date information to measure business performance (and plan for future operations) 3. Creditorsc. To determine taxes to be paid and whether other regulations are met 4. Government agenciesd. The firms current financial conditionarrow_forwardCornerstone Exercise 1-15 Using the Accounting Equation At the beginning of the year, Morgan Company had total assets of 425,000 and total liabilities of 260,000. Required: Use the fundamental accounting equation to answer the following independent questions: What is total stockholders' equity at the beginning of the year? If, during the year, total assets increased by $73,000 and total liabilities increased by $32,000, what is the amount of total stockholders' equity at the end of the year? If, during the year, total assets decreased by $52,000 and total stockholders' equity increased by $35,000, what is the amount of total liabilities at the end of the year? If, during the year, total liabilities increased by $85,000 and total stockholders' equity decreased by $73,000, what is the amount of total assets at the end of the year?arrow_forward

Survey of Accounting (Accounting I)AccountingISBN:9781305961883Author:Carl WarrenPublisher:Cengage Learning

Survey of Accounting (Accounting I)AccountingISBN:9781305961883Author:Carl WarrenPublisher:Cengage Learning Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning

Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning