Concept explainers

Videos

Kelly Pitney began her consulting business, Kelly Consulting, on April 1, 2016. The accounting cycle for Kelly Consulting for April, including financial statements, was illustrated in this chapter. During May, Kelly Consulting entered into the following transactions:

May 3. Received cash from clients as an advance payment for services to be provided and recorded it as unearned fees, $4,500.

5. Received cash from clients on account, $2,450.

9. Paid cash for a newspaper advertisement, $225.

13. Paid Office Station Co. for part of the debt incurred on April 5, $640.

15. Recorded services provided on account for the period May 1–15, $9,180.

16. Paid part-time receptionist for two weeks' salary including the amount owed on April 30, $750.

17. Recorded cash from cash clients for fees earned during the period May 1–16, $8,360.

Record the following transactions on Page 6 of the journal:

20. Purchased supplies on account, $735.

21. Recorded services provided on account for the period May 16–20, $4,820.

25. Recorded cash from cash clients for fees earned for the period May 17–23, $7,900.

27. Received cash from clients on account, $9,520.

28. Paid part-time receptionist for two weeks' salary, $750.

30. Paid telephone bill for May, $260.

31. Paid electricity bill for May, $810.

31. Recorded cash from cash clients for fees earned for the period May 26–31, $3,300.

31. Recorded services provided on account for the remainder of May, $2,650.

31. Kelly withdrew $10,500 for personal use.

Instructions

1. The chart of accounts for Kelly Consulting is shown in Exhibit 9, and the post-closing

2. Post the journal to a ledger of four-column accounts.

3. Prepare an unadjusted trial balance.

4. At the end of May, the following adjustment data were assembled. Analyze and use these data to complete parts (5) and (6).

a. Insurance expired during May is $275.

b. Supplies on hand on May 31 are $715.

c.

d. Accrued receptionist salary on May 31 is $325.

e. Rent expired during May is $1,600.

f. Unearned fees on May 31 are $3,210.

5. (Optional) Enter the unadjusted trial balance on an end-of-period spreadsheet and complete the spreadsheet.

6. Journalize and post the

7. Prepare an adjusted trial balance.

8. Prepare an income statement, a statement of owner’s equity, and a balance sheet.

9. Prepare and

10. Prepare a post-closing trial balance.

(1)

Journal:

Journal is the book of original entry. Journal consists of the day-to-day financial transactions in a chronological order. The journal has two aspects; they are debit aspect and the credit aspect.

T-Accounts:

T-accounts are referred as T-account because its format represents the letter “T”. The T-accounts consists of the following:

- The title of accounts.

- The debit side (Dr) and,

- The credit side (Cr).

Adjusted trial balance:

The unadjusted trial balance is the summary of all the ledger accounts that appears on the ledger accounts before making adjusting journal entries.

Adjusting entries:

An adjusting entry is prepared when the trial balance is not up-to-date, and complete, and they are usually prepared at the end of the accounting period. This adjusting entry is essential for preparing the financial statements of the business.

Spreadsheet: A spreadsheet is a worksheet. It is used while preparing a financial statement. It is a type of form having multiple columns and it is used in the adjustment process. The use of a worksheet is optional for any organization. A worksheet can neither be considered as a journal nor a part of the general ledger.

Statement of owners’ equity:

This statement reports the beginning owner’s equity and all the changes, which led to ending owners’ equity. Additional capital, net income from income statement is added to and drawing is deducted from beginning owner’s equity to arrive at the end result, ending owner’s equity.

Income statement:

An income statement is one of the financial statements which shows the revenues, and expenses of the company. The income statement is prepared to ascertain the net income/loss of the company, by deducting the expenses from the revenues.

Balance sheet:

A balance sheet is a financial statement consists of the assets, liabilities, and the stockholder’s equity of the company. The balance of the assets account must be equal to that of the liabilities and the stockholder’s equity account.

Closing entries:

Closing entries are recorded in order to close the temporary accounts such as incomes and expenses by transferring them to the permanent accounts. It is passed at the end of the accounting period, to transfer the final balance.

Post-Closing Trial Balance:

After passing all the journal entries and the closing entries of the permanent accounts and then further posting them to each of the respective accounts, a post-closing trial balance is prepared which consists of a list of all the permanent accounts. A post-closing trial balance serves as an evidence to prove that the balance of the permanent accounts is equal.

To journalize: The transactions of May in a two column journal beginning on page 5.

Explanation of Solution

Journalize the transactions of May in a two column journal beginning on page 5.

| Journal Page 5 | |||||

| Date | Description | Post. Ref | Debit ($) | Credit ($) | |

| 2016 | 3 | Cash | 11 | 4,500 | |

| May | Unearned fees | 23 | 4,500 | ||

| (To record the cash received for the service yet to be provide) | |||||

| 5 | Cash | 11 | 2,450 | ||

| Accounts receivable | 12 | 2,450 | |||

| (To record the cash received from clients) | |||||

| 9 | Miscellaneousexpense | 59 | 225 | ||

| Cash | 11 | 225 | |||

| (To record the payment made for Miscellaneous expense) | |||||

| 13 | Accounts payable | 21 | 640 | ||

| Cash | 11 | 640 | |||

| (To record the payment made to creditors on account) | |||||

| 15 | Accounts receivable | 12 | 9,180 | ||

| Fees earned | 41 | 9,180 | |||

| (To record the revenue earned and billed) | |||||

| 14 | Salary Expense | 51 | 630 | ||

| Salaries payable | 22 | 120 | |||

| Cash | 11 | 750 | |||

| (To record the payment made for salary) | |||||

| Cash | 11 | 8,360 | |||

| 17 | Fees earned | 41 | 8,360 | ||

| (To record the receipt of cash) | |||||

Table (1)

| Journal Page 6 | |||||

| Date | Description | Post. Ref | Debit ($) | Credit ($) | |

| 2016 | 18 | Supplies | 14 | 735 | |

| May | Accounts payable | 21 | 735 | ||

| (To record the payment made for automobile expense) | |||||

| 21 | Accounts receivable | 12 | 4,820 | ||

| Fees earned | 41 | 4,820 | |||

| (To record the payment of advertising expense) | |||||

| 25 | Cash | 11 | 7,900 | ||

| Fees earned | 41 | 7,900 | |||

| (To record the cash received from client for fees earned) | |||||

| 27 | Cash | 11 | 9,520 | ||

| Accounts receivable | 12 | 9,520 | |||

| (To record the cash received from clients) | |||||

| 28 | Salary expense | 51 | 750 | ||

| Cash | 11 | 750 | |||

| (To record the payment of salary) | |||||

| 30 | Miscellaneous Expense | 59 | 260 | ||

| Cash | 11 | 260 | |||

| (To record the payment of telephone charges) | |||||

| 31 | Miscellaneous Expense | 59 | 810 | ||

| Cash | 11 | 810 | |||

| (To record the payment of electricity charges) | |||||

| 31 | Cash | 11 | 3,300 | ||

| Fees earned | 41 | 3,300 | |||

| (To record the cash received from client for fees earned) | |||||

| 31 | Accounts receivable | 12 | 2,650 | ||

| Fees earned | 41 | 2,650 | |||

| (To record the revenue earned and billed) | |||||

| 31 | Dividends | 33 | 10,500 | ||

| Cash | 11 | 10,500 | |||

| (To record the drawing made for personal use) | |||||

Table (2)

(2), (6) and (9)

To record: The balance of each accounts in the appropriate balance column of a four-column account and post them to the ledger.

Explanation of Solution

| Account: Cash Account no.11 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2016 | |||||||

| May | 1 |

|

✓ | 22,100 | |||

| 3 | 5 | 4,500 | 26,600 | ||||

| 5 | 5 | 2,450 | 29,050 | ||||

| 9 | 5 | 225 | 28,825 | ||||

| 13 | 5 | 640 | 28,185 | ||||

| 16 | 5 | 750 | 27,435 | ||||

| 17 | 5 | 8,360 | 35,795 | ||||

| 25 | 6 | 7,900 | 43,695 | ||||

| 27 | 6 | 9,520 | 53,215 | ||||

| 28 | 6 | 750 | 52,465 | ||||

| 30 | 6 | 260 | 52,205 | ||||

| 31 | 6 | 810 | 51,395 | ||||

| 31 | 6 | 3,300 | 54,695 | ||||

| 31 | 6 | 10,500 | 44,195 | ||||

Table (3)

| Account: Accounts Receivable Account no.12 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2016 | |||||||

| May | 1 |

|

✓ | 3,400 | |||

| 5 | 5 | 2,450 | 950 | ||||

| 15 | 5 | 9,180 | 10,130 | ||||

| 21 | 6 | 4,820 | 14,950 | ||||

| 27 | 6 | 9,520 | 5,430 | ||||

| 31 | 6 | 2,650 | 8,080 | ||||

Table (4)

| Account: Supplies Account no.14 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2016 | |||||||

| May | 1 |

|

✓ | 1,350 | |||

| 20 | 6 | 735 | 2,085 | ||||

| 30 | Adjusting | 7 | 1,350 | 715 | |||

Table (5)

| Account: Prepaid Rent Account no.15 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2016 | |||||||

| May | 1 |

|

✓ | 3,200 | |||

| 31 | Adjusting | 7 | 1,600 | 1,600 | |||

Table (6)

| Account: Prepaid Insurance Account no.16 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2016 | |||||||

| May | 1 |

|

✓ | 1,500 | |||

| 31 | Adjusting | 7 | 275 | 1,225 | |||

Table (7)

| Account: Office equipment Account no.18 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2016 | |||||||

| May | 1 |

|

✓ | 14,500 | |||

Table (8)

| Account: Accumulated Depreciation-Office equipment Account no.19 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2016 | |||||||

| May | 1 |

|

✓ | 330 | |||

| 31 | Adjusting | 7 | 330 | 660 | |||

Table (9)

| Account: Accounts Payable Account no.21 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2016 | |||||||

| May | 1 |

|

✓ | 800 | |||

| 13 | 5 | 640 | 160 | ||||

| 20 | 6 | 735 | 895 | ||||

Table (10)

| Account: Salaries Payable Account no.22 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2016 | |||||||

| May | 1 |

|

✓ | 120 | |||

| 16 | 5 | 120 | |||||

| 31 | Adjusting | 7 | 325 | 325 | |||

Table (11)

| Account: Unearned Fees Account no.23 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2016 | |||||||

| May | 1 |

|

✓ | 2,500 | |||

| 3 | 5 | 4,500 | 7,000 | ||||

| 31 | Adjusting | 7 | 3,790 | 3,210 | |||

Table (12)

|

Account: Common Stock Account no.31 |

|||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2016 | |||||||

| May | 1 |

|

✓ | 42,300 | |||

| 31 | Closing | 8 | 33,425 | 75,725 | |||

| 31 | Closing | 8 | 10,500 | 65,225 | |||

Table (13)

| Account: Dividends Account no.33 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2016 | |||||||

| May | 31 | 6 | 10,500 | 10,500 | |||

| 31 | Closing | 8 | 10,500 | ||||

Table (14)

| Account: Income Summary Account no.34 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2016 | |||||||

| May | 31 | Closing | 8 | 40,000 | 40,000 | ||

| 31 | Closing | 8 | 6,575 | 33,425 | |||

| 31 | Closing | 8 | 33,425 | ||||

Table (15)

| Account: Fees earned Account no.41 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2016 | |||||||

| May | 15 | 5 | 9,180 | 9,180 | |||

| 17 | 5 | 8,360 | 17,540 | ||||

| 21 | 6 | 4,820 | 22,360 | ||||

| 25 | 6 | 7,900 | 30,260 | ||||

| 31 | 6 | 3,300 | 33,560 | ||||

| 31 | 6 | 2,650 | 36,210 | ||||

| 31 | Adjusting | 7 | 3,790 | 40,000 | |||

| 31 | Closing | 8 | 40,000 | ||||

Table (16)

| Account: Salary expense Account no.51 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2016 | |||||||

| May | 16 | 5 | 630 | 630 | |||

| 28 | 6 | 750 | 1,380 | ||||

| 31 | Adjusting | 7 | 325 | 1,705 | |||

| 31 | Closing | 8 | 1,705 | ||||

Table (17)

| Account: Rent expense Account no.52 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2016 | |||||||

| May | 31 | Adjusting | 7 | 1,600 | 1,600 | ||

| 31 | Closing | 8 | 1,600 | ||||

Table (18)

| Account: Supplies expense Account no.53 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2016 | |||||||

| May | 31 | Adjusting | 7 | 1,370 | 1,370 | ||

| 31 | Closing | 8 | 1,370 | ||||

Table (19)

| Account: Depreciation expense Account no.54 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2016 | |||||||

| May | 31 | Adjusting | 7 | 330 | 330 | ||

| 31 | Closing | 8 | 330 | ||||

Table (20)

| Account: Insurance expense Account no.54 | |||||||

| Date | Item | PostRef. |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2016 | |||||||

| May | 31 | Adjusting | 7 | 275 | 275 | ||

| 31 | Closing | 8 | 275 | ||||

Table (21)

| Account: Miscellaneous expense Account no.59 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2016 | |||||||

| May | 9 | 5 | 225 | 225 | |||

| 30 | 6 | 260 | 485 | ||||

| 31 | 6 | 810 | 1,295 | ||||

| 31 | Closing | 8 | 1,295 | ||||

Table (22)

(3)

To prepare: The unadjusted trial balance of Consulting K at May, 31.

Explanation of Solution

Prepare an unadjusted trial balance of Consulting K for the month ended May, 31 as follows:

|

K Consulting Unadjusted Trial Balance May 31, 2016 |

|||

| Particulars | Account No. |

Debit $ | Credit $ |

| Cash | 11 | 44,195 | |

| Accounts receivable | 12 | 8,080 | |

| Supplies | 14 | 2,085 | |

| Prepaid rent | 15 | 3,200 | |

| Prepaid insurance | 16 | 1,500 | |

| Office Equipment | 18 | 14,500 | |

| Accumulated depreciation-Office equipment | 19 | 330 | |

| Accounts payable | 21 | 895 | |

| Salaries payable | 22 | 0 | |

| Unearned fees | 23 | 7,000 | |

| KP Capital | 31 | 42,300 | |

| KP Drawings | 33 | 10,500 | |

| Fees earned | 41 | 36,210 | |

| Salary expense | 51 | 1,380 | |

| Rent expense | 52 | 0 | |

| Supplies expense | 53 | 0 | |

| Depreciation expense | 54 | 0 | |

| Insurance expense | 55 | 0 | |

| Miscellaneous expense | 59 | 1,295 | |

| Total | $86,735 | $86,735 | |

Table (23)

The debit column and credit column of the unadjusted trial balance are agreed, both having balance of $86,735.

(5)

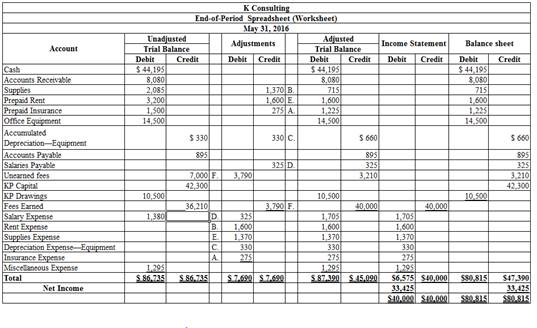

To enter: The unadjusted trial balance on an end-of-period spreadsheet.

Explanation of Solution

The unadjusted trial balance on an end-of-period spreadsheet is prepared as follows:

Table (24)

Hence, the unadjusted trial balance on an end-of-period spreadsheet is prepared and completed.

(6)

To Journalize: The adjusting entries of Consulting K for May 31.

Explanation of Solution

The adjusting entries of Consulting K for May 31, 2016are as follows:

| Date | Accounts title and explanation | Post Ref. | Debit ($) |

Credit ($) |

|

| 2016 | Insurance expense | 55 | 275 | ||

| May | 31 | Prepaid insurance | 16 | 275 | |

| (To record the insurance expense for May ) | |||||

| 31 | Supplies expense | 53 | 1,370 | ||

| Supplies | 14 | 1,370 | |||

| (To record the supplies expense) | |||||

| 31 | Depreciation expense | 54 | 330 | ||

| Accumulated Depreciation | 19 | 330 | |||

| (To record the depreciation and the accumulated depreciation) | |||||

| 31 | Salaries expense | 51 | 325 | ||

| Salaries payable | 22 | 325 | |||

| (To record the accrued salaries payable) | |||||

| 31 | Rent expense | 52 | 1,600 | ||

| Prepaid rent | 15 | 1,600 | |||

| (To record the rent expense for May ) | |||||

| 31 | Unearned fees | 23 | 3,790 | ||

| Fees earned | 41 | 3,790 | |||

| (To record the receipt of unearned fees) | |||||

Table (25)

Working notes:

(7)

To prepare: An adjusted trial balance of Consulting K for May 31, 2016.

Explanation of Solution

An adjusted trial balance of Consulting K for May 31, 2016 is prepared as follows:

|

K Consulting Adjusted Trial Balance May 31, 2016 |

|||

| Particulars | Account No. |

Debit $ | Credit $ |

| Cash | 11 | 44,195 | |

| Accounts receivable | 12 | 8,080 | |

| Supplies | 14 | 715 | |

| Prepaid insurance | 16 | 1,600 | |

| Prepaid rent | 15 | 1,225 | |

| Office Equipment | 18 | 14,500 | |

| Accumulated Depreciation-Office equipment | 19 | 660 | |

| Accounts payable | 21 | 895 | |

| Salaries payable | 22 | 325 | |

| Unearned fees | 23 | 3,210 | |

| Common stock | 31 | 30,000 | |

| Retained earnings | 32 | 12,300 | |

| Dividends | 33 | 10,500 | |

| Fees earned | 41 | 40,000 | |

| Salary expense | 51 | 1,705 | |

| Rent expense | 52 | 1,600 | |

| Supplies Expense | 53 | 1,370 | |

| Depreciation expense | 54 | 330 | |

| Insurance expense | 55 | 275 | |

| Miscellaneous expense | 59 | 1,295 | |

| Total | $87,390 | $87,390 | |

Table (25)

The debit column and credit column of the adjusted trial balance are agreed, both having balance of $87,390.

(8)

To Prepare: An income statement for the year ended May 31, 2016.

Answer to Problem 1CPP

| K Consulting | |||

| Balance Sheet | |||

| May 31, 2016 | |||

| Assets | |||

| Current Assets: | $ | $ | |

| Cash | 44,195 | ||

| Accounts Receivable | 8,080 | ||

| Supplies | 715 | ||

| Prepaid Rent | 1,600 | ||

| Prepaid Insurance | 1,225 | ||

| Total Current Assets | 55,815 | ||

| Property, plant and equipment: | |||

| Office Equipment | 14,500 | ||

| Less: Accumulated Depreciation | (660) | ||

| Total Plant Assets | 13,840 | ||

| Total Assets | $69,655 | ||

| Liabilities | |||

| Current Liabilities: | |||

| Accounts Payable | 895 | ||

| Salaries Payable | 325 | ||

| Unearned rent | 3,210 | ||

| Total Liabilities | $4,430 | ||

| Owners’ Equity | |||

| Capital | 65,225 | ||

| Total owners ‘equity | 65,225 | ||

| Total Liabilities and Owners’ Equity | $69,655 | ||

Table (28)

Explanation of Solution

An income statement for the year ended May 31, 2016 is as follows:

| K Consulting | ||

| Income Statement | ||

| For the year ended May 31, 2016 | ||

| Particulars | Amount ($) | Amount ($) |

| Revenues: | ||

| Fees Earned | 40,000 | |

| Expenses: | ||

| Salaries Expense | 1,705 | |

| Rent Expense | 1,600 | |

| Supplies Expense | 1,370 | |

| Depreciation Expense- Building | 330 | |

| Insurance Expense | 275 | |

| Miscellaneous Expense | 1,295 | |

| Total Expenses | 6,575 | |

| Net Income | $33,425 | |

Table (26)

Hence, the net income of K Consulting for the year ended May 31, 2016is $33,425.

(9)

To Journalize: The closing entries for K Consulting.

Answer to Problem 1CPP

Closing entry for revenue and expense accounts:

| Date | Accounts title and Explanation | Post Ref. | Debit ($) |

Credit ($) |

| May 31, 2016 | Fees earned | 41 | 40,000 | |

| Income summary | 34 | 40,000 | ||

| (To close the balances of revenue account) | ||||

| May 31, 2016 | Income summary | 34 | 6,575 | |

| Salary expense | 51 | 1,705 | ||

| Rent Expense | 52 | 1,600 | ||

| Supplies Expense | 53 | 1,370 | ||

| Depreciation Expense | 54 | 330 | ||

| Insurance Expense | 55 | 275 | ||

| Miscellaneous Expense | 59 | 1,295 | ||

| (To close the balances of expense account) | ||||

| July 31 | Income Summary | 33 | 33,425 | |

| KP Capital | 31 | 33,425 | ||

| (To close balance of income summary are transferred to owners’ capital account) | ||||

| July 31 | KP’s Capital | 31 | 10,500 | |

| KP’s Drawing | 32 | 10,500 | ||

| (To Close the capital and drawings account) | ||||

Table (29)

Explanation of Solution

- A Service fee earned is revenue account. Since the amount of revenue is closed and transferred to JH’s capital account. Here, G Consulting earned an income of $64,550, and $18,000. Therefore, it is debited.

- Salaries Expense, Rent Expense, Insurance Expense, Utilities Expense, Supplies Expense, Depreciation Expense, Advertising Expense, JH Capital, and Miscellaneous Expense are expense accounts. Since the amount of expenses are closed to Income Summary account. Therefore, it is credited.

- Owner’s capital is a component of owner’s equity. Thus, owners ‘equity is debited since the capital is decreased on owners’ drawings.

- Owner’s drawings are a component of owner’s equity. It is credited because the balance of owners’ drawing account is transferred to owners ‘capital account.

(10)

To Journalize: The closing entries for K Consulting.

Explanation of Solution

Prepare a post–closing trial balance of K Consulting for the month ended May 31, 2016 as follows:

|

Consulting K Post-closing Trial Balance May, 31, 2016 |

|||

| Particulars | Account Number | Debit $ | Credit $ |

| Cash | 11 | 44,195 | |

| Accounts receivable | 12 | 8,080 | |

| Supplies | 14 | 715 | |

| Prepaid rent | 15 | 1,600 | |

| Prepaid insurance | 16 | 1,225 | |

| Office Equipment | 18 | 14,500 | |

| Accumulated depreciation –Office Equipment | 19 | 660 | |

| Accounts payable | 21 | 895 | |

| Salaries payable | 22 | 325 | |

| Unearned rent | 23 | 3,210 | |

| Common stock | 31 | 30,000 | |

| Retained earnings | 32 | 35,225 | |

| Total | $70,315 | $70,315 | |

Table (30)

The debit column and credit column of the post–closing trial balance are agreed, both having balance of $70,315.

Want to see more full solutions like this?

Chapter 4 Solutions

Accounting (Text Only)

- Kelly Pitney began her consulting business, Kelly Consulting, on April 1, 2016. The accounting cycle for Kelly Consulting for April, including financial statements, was illustrated in this chapter. During May, Kelly Consulting entered into the following transactions: Instructions 1. The chart of accounts for Kelly Consulting is shown in Exhibit 9, and the post-closing trial balance as of April 30, 2016, is shown in Exhibit 17. For each account in the post-closing trial balance, enter the balance in the appropriate Balance column of a four-column account. Date the balances May 1, 2016, and place a check mark () in the Posting Reference column. Journalize each of the May transactions in a two column journal starting on Page 5 of the journal and using Kelly Consultings chart of accounts. (Do not insert the account numbers in the journal at this time.) 2. Post the journal to a ledger of four-column accounts. 3. Prepare an unadjusted trial balance. 4. At the end of May, the following adjustment data were assembled. Analyze and use these data to complete parts (5) and (6) a. Insurance expired during May is 275. b. Supplies on hand on May 31 are 715. c. Depreciation of office equipment for May is 330. d. Accrued receptionist salary on May 31 is 325. e. Rent expired during May is 1,600. f. Unearned fees on May 31 are 3,210. 5.(Optional) Enter the unadjusted trial balance on an end-of-period spreadsheet and complete the spreadsheet. 6.Journalize and post the adjusting entries. Record the adjusting entries on Page 7 of the journal. 7.Prepare an adjusted trial balance. 8.Prepare an income statement, a statement of owners equity, and a balance sheet. 9.Prepare and post the closing entries. Record the closing entries on Page 8 of the journal. (Income Summary is account #33 in the chart of accounts.) Indicate closed accounts by inserting a line in both the Balance columns opposite the closing entry. 10.Prepare a post-closing trial balance.arrow_forwardIn October, A. Nguyen established an apartment rental service. The account headings are presented below. Transactions completed during the month of October follow. a. Nguyen deposited 25,000 in a bank account in the name of the business. b. Paid the rent for the month, 1,200, Ck. No. 2015. c. Bought supplies on account, 225. d. Bought a truck for 18,000, paying 1,000 in cash and placing the remainder on account e. Bought Insurance for the truck for the yean 1,400, Ck. No. 2016. f. Sold services on account 5,000. g. Bought office equipment on account from Henry Office Supply, 2,300. h. Sold services for cash for the first half of the month, 6,050. i. Received and paid the bill for utilities, 150, Ck. No. 2017. j. Received a bill for gas and oil for the truck. 80. k. Paid wages to the employees, 1,400, Ck Nos. 20182020. l. Sold services for cash for the remainder of the month, 4,200. m. Nguyen withdrew cash for personal use, 2,000, Ck. No. 2021. Required 1. Record the transactions and the balance after each transaction. 2. Total the left side of the accounting equation (left side of the equal sign), then total the right side of the accounting equation (right side of the equal sign). If the two totals are not equal, check the addition and subtraction. If you still cannot find the error, reanalyze each transaction.arrow_forwardOn March 1 of this year, B. Gervais established Gervais Catering Service. The account headings are presented below. Transactions completed during the month follow. a. Gervais deposited 25,000 in a bank account in the name of the business. b. Bought a truck from Kelly Motors for 26,329, paying 8,000 in cash and placing the balance on account, Ck. No. 500. c. Bought catering equipment on account from Luigis Equipment, 3,795. d. Paid the rent for the month, 1,255, Ck. No. 501. e. Bought insurance for the truck for one year, 400, Ck. No. 502. f. Sold catering services for cash for the first half of the month, 3,012. g. Bought supplies for cash, 185, Ck. No. 503. h. Sold catering services on account, 4,307. i. Received and paid the heating bill, 248, Ck. No. 504. j. Received a bill from GC Gas and Lube for gas and oil for the truck, 128. k. Sold catering services for cash for the remainder of the month, 2,649. l. Gervais withdrew cash for personal use, 1,550, Ck. No. 505. m. Paid the salary of the assistant, 1,150, Ck. No. 506. Required 1. Record the transactions and the balance after each transaction. 2. Total the left side of the accounting equation (left side of the equal sign), then total the right side of the accounting equation (right side of the equal sign). If the two totals are not equal, check the addition and subtraction. If you still cannot find the error, re-analyze each transaction.arrow_forward

- Kelly Pitney began her consulting business, Kelly Consulting, on April 1, 2019. The accounting cycle for Kelly Consulting for April, including financial statements, was illustrated in this chapter. During May, Kelly Consulting entered into the following transactions: May 3. Received cash from clients as an advance payment for services to be provided and recorded it as unearned fees, 4,500. 5. Received cash from clients on account, 2,450. 9. Paid cash for a newspaper advertisement, 225. 13. Paid Office Station Co. for part of the debt incurred on April 5, 640. 15. Provided services on account for the period May 115, 9,180. 16. Paid part-time receptionist for two weeks' salary including the amount owed on April 30, 750. 17. Received cash from cash clients for fees earned during the period May 116, 8,360. Record the following transactions on Page 6 of the journal: 20. Purchased supplies on account, 735. 21. Provided services on account for the period May 1620, 4,820. 25. Received cash from cash clients for fees earned for the period May 1723, 7,900. 27. Received cash from clients on account, 9,520. 28. Paid part-time receptionist for two weeks' salary, 750. 30. Paid telephone bill for May, 260. 31. Paid electricity bill for May, 810. 31. Received cash from cash clients for fees earned for the period May 2631, 3,300. 31. Provided services on account for the remainder of May, 2,650. 31. Kelly withdrew 10,500 for personal use. Instructions 1.The chart of accounts for Kelly Consulting is shown in Exhibit 9, and the post-closing trial balance as of April 30, 2019, is shown in Exhibit 17. For each account in the post-closing trial balance, enter the balance in the appropriate Balance column of a four-column account. Date the balances May 1, 2019, and place a check mark () in the Posting Reference column Journalize each of the May transactions in a two column Journal starting on Page 5 of the journal and using Kelly Consulting's chart of accounts. (Do not insert the account numbers in the journal at this time.) 2.Post the journal to a ledger of four-column accounts. 3Prepare an unadjusted trial balance. 4.At the end of May, the following adjustment data were assembled. Analyze and use these data to complete parts (5) and (6). a.Insurance expired during May is 275. b.Supplies on hand on May 3 1 are 715. c.Depreciation of office equipment for May is 330. d.Accrued receptionist salary on May 31 is 325. e.Rent expired during May is 1,600. f.Unearned fees on May 31 are 3,210. 5.(Optional) Enter the unadjusted trial balance on an end-of-period spreadsheet and complete the spreadsheet. 6.Journalize and post the adjusting entries. Record the adjusting entries on Page 7 of the journal. 7.Prepare an adjusted trial balance. 8.Prepare an income statement, a statement of owner's equity, and a balance sheet. 9.Prepare and post the closing entries. Record the closing entries on Page 8 of the journal. Indicate closed accounts by inserting a line in both Balance columns opposite the closing entry. 10.Prepare a post-closing trial balance.arrow_forwardIn October, A. Nguyen established an apartment rental service. The account headings are presented below. Transactions completed during the month of October follow. a. Nguyen deposited 25,000 in a bank account in the name of the business. b. Paid the rent for the month, 1,200, Ck. No. 2015 (Rent Expense). c. Bought supplies on account, 225. d. Bought a truck for 18,000, paying 1,000 in cash and placing the remainder on account. e. Bought insurance for the truck for the year, 1,400, Ck. No. 2016. f. Sold services on account, 5,000 (Service Income). g. Bought office equipment on account from Henry Office Supply, 2,300. h. Sold services for cash for the first half of the month, 6,050 (Service Income). i. Received and paid the bill for utilities, 150, Ck. No. 2017 (Utilities Expense). j. Received a bill for gas and oil for the truck, 80 (Gas and Oil Expense). k. Paid wages to the employees, 1,400, Ck. Nos. 20182020 (Wages Expense). l. Sold services for cash for the remainder of the month, 4,200 (Service Income). m. Nguyen withdrew cash for personal use, 2,000, Ck. No. 2021. Required 1. In the equation, write the owners name above the terms Capital and Drawing. 2. Record the transactions and the balance after each transaction. Identify the account affected when the transaction involves revenues or expenses. 3. Write the account totals from the left side of the equals sign and add them. Write the account totals from the right side of the equals sign and add them. If the two totals are not equal, check the addition and subtraction. If you still cannot find the error, re-analyze each transaction.arrow_forwardJournal entries and trial balance On October 1, 20Y6, Jay Crowley established Affordable Realty, which completed the following transactions during the month: a. Jay Crowley transferred cash from a personal bank account to an account to be used for the business in exchange for common stock, 40,000. b. Paid rent on office and equipment for the month, 4,800. c. Purchased supplies on account, 2,150. d. Paid creditor on account, 1,100. e. Earned sales commissions, receiving cash, 18,750. f. Paid automobile expenses (including rental charge) for month, 1,580, and miscellaneous expenses, 800. g. Paid office salaries, 3,500. h. Determined that the cost of supplies used was 1,300. i. Paid dividends, 1,500. Instructions 1. Journalize entries for transactions (a) through (i), using the following account titles: Cash, Supplies, Accounts Payable, Common Stock, Dividends, Sales Commissions, Rent Expense, Office Salaries Expense, Automobile Expense, Supplies Expense, Miscellaneous Expense. Explanations may be omitted. 2. Prepare T accounts, using the account titles in (1). Post the journal entries to these accounts, placing the appropriate letter to the left of each amount to identify the transactions. Determine the account balances after all posting is complete. Accounts containing only a single entry do not need a balance. 3. Prepare an unadjusted trial balance as of October 31, 20Y6. 4. Determine the following: a. Amount of total revenue recorded in the ledger. b. Amount of total expenses recorded in the ledger. c. Amount of net income for October. 5. Determine the increase or decrease in retained earnings for October.arrow_forward

- In March, T. Carter established Carter Delivery Service. The account headings are presented below. Transactions completed during the month of March follow. a. Carter deposited 25,000 in a bank account in the name of the business. b. Bought a used truck from Degroot Motors for 15,140, paying 5,140 in cash and placing the remainder on account. c. Bought equipment on account from Flemming Company, 3,450. d. Paid the rent for the month, 1,000, Ck. No. 3001 (Rent Expense). e. Sold services for cash for the first half of the month, 6,927 (Service Income). f. Bought supplies for cash, 301, Ck. No. 3002. g. Bought insurance for the truck for the year, 1,200, Ck. No. 3003. h. Received and paid the bill for utilities, 349, Ck. No. 3004 (Utilities Expense). i. Received a bill for gas and oil for the truck, 218 (Gas and Oil Expense). j. Sold services on account, 3,603 (Service Income). k. Sold services for cash for the remainder of the month, 4,612 (Service Income). l. Paid wages to the employees, 3,958, Ck. Nos. 30053007 (Wages Expense). m. Carter withdrew cash for personal use, 1,250, Ck. No. 3008. Required 1. In the equation, write the owners name above the terms Capital and Drawing. 2. Record the transactions and the balance after each transaction. Identify the account affected when the transaction involves revenues or expenses. 3. Write the account totals from the left side of the equals sign and add them. Write the account totals from the right side of the equals sign and add them. If the two totals are not equal, check the addition and subtraction. If you still cannot find the error, re-analyze each transaction.arrow_forwardIn March, T. Carter established Carter Delivery Service. The account headings are presented below. Transactions completed during the month of March follow. a. Carter deposited 25,000 in a bank account in the name of the business. b. Bought a used truck from Degroot Motors for 15,140, paying 5,140 in cash and placing the remainder on account. c. Bought equipment on account from Flemming Company, 3,450. d. Paid the rent for the month, 1,000, Ck. No. 3001. e. Sold services for cash for the first half of the month, 6,927. f. Bought supplies for cash, 301, Ck. No. 3002. g. Bought insurance for the truck for the year, 1,200, Ck. No. 3003. h. Received and paid the bill for utilities, 349, Ck. No. 3004. i. Received a bill for gas and oil for the truck, 218. j. Sold services on account, 3,603. k. Sold services for cash for the remainder of the month, 4,612. l. Paid wages to the employees, 3,958, Ck. Nos. 30053007. m. Carter withdrew cash for personal use, 1,250, Ck. No. 3008. Required 1. Record the transactions and the balance after each transaction 2. Total the left side of the accounting equation (left side of the equal sign), then total the right side of the accounting equation (right side of the equal sign). If the two totals are not equal, check the addition and subtraction. If you still cannot find the error, re-analyze each transaction.arrow_forwardWyoming Tours Co. is a travel agency. The nine transactions recorded by Wyoming Tours during June 2016, its first month of operations, are indicated in the following T accounts: Indicate for each debit and each credit: (a) whether an asset, liability, owners equity, drawing, revenue, or expense account was affected and (b) whether the account was increased (+) or decreased (). Present your answers in the following form, with transaction (1) given as an example:arrow_forward

- For the past several years, Steffy Lopez has operated a part-time consulting business from his home. As of July 1, 2016, Steffy decided to move to rented quarters and to operate the business, which was to be known as Diamond Consulting, on a full-time basis. Diamond Consulting entered into the following transactions during July: Instructions 1.Journalize each transaction in a two-column journal starting on Page 1, referring to the following chart of accounts in selecting the accounts to be debited and credited. (Do not insert the account numbers in the journal at this time.) 2.Post the journal to a ledger of four-column accounts. 3.Prepare an unadjusted trial balance. 4.At the end of July, the following adjustment data were assembled. Analyze and use these data to complete parts (5) and (6). a. Insurance expired during July is 375. b. Supplies on hand on July 31 are 1,525. c. Depreciation of office equipment for July is 750. d. Accrued receptionist salary on July 31 is 175. e. Rent expired during July is 2,400. f. Unearned fees on July 31 are 2,750. 5.(Optional) Enter the unadjusted trial balance on an end-of-period spreadsheet and complete the spreadsheet. 6.Journalize and post the adjusting entries. Record the adjusting entries on Page 3 of the journal. 7.Prepare an adjusted trial balance. 8.Prepare an income statement, a statement of owners equity, and a balance sheet. 9.Prepare and post the closing entries. (Income Summary is account #33 in the chart of accounts.) Record the closing entries on Page 4 of the journal. Indicate closed accounts by inserting a line in both the Balance columns opposite the closing entry. 10.Prepare a post-closing trial balance.arrow_forwardJournal entries and trial balance On August 1, 20Y7, Rafael Masey established Planet Realty, which completed the following transactions during the month: a. Rafael Masey transferred cash from a personal bank account to an account to be used for the business in exchange for common stock, 17,500. b. Purchased supplies on account, 2,300. c. Earned sales commissions, receiving cash, 13,300. d. Paid rent on office and equipment for the month, 3,000. e. Paid creditor on account, 1,150. f. Paid dividends, 1,800. g. Paid automobile expenses (including rental charge) for month, 1,500, and miscellaneous expenses, 400. h. Paid office salaries, 2,800. i. Determined that the cost of supplies used was 1,050. Instructions 1. Journalize entries for transactions (a) through (i), using the following account titles: Cash, Supplies, Accounts Payable, Common Stock, Dividends, Sales Commissions, Rent Expense, Office Salaries Expense, Automobile Expense, Supplies Expense, Miscellaneous Expense. Journal entry explanations may be omitted. 2. Prepare T accounts, using the account titles in (1). Post the journal entries to these accounts, placing the appropriate letter to the left of each amount to identify the transactions. Determine the account balances, after all posting is complete. Accounts containing only a single entry do not need a balance. 3. Prepare an unadjusted trial balance as of August 31, 20Y7. 4. Determine the following: a. Amount of total revenue recorded in the ledger. b. Amount of total expenses recorded in the ledger. c. Amount of net income for August. 5. Determine the increase or decrease in retained earnings for August.arrow_forwardOn March 1 of this year, B. Gervais established Gervais Catering Service. The account headings are presented below. Transactions completed during the month follow. a. Gervais deposited 25,000 in a bank account in the name of the business. b. Bought a truck from Kelly Motors for 26,329, paying 8,000 in cash and placing the balance on account, Ck. No. 500. c. Bought catering equipment on account from Luigis Equipment, 3,795. d. Paid the rent for the month, 1,255, Ck. No. 501 (Rent Expense). e. Bought insurance for the truck for one year, 400, Ck. No. 502. f. Sold catering services for cash for the first half of the month, 3,012 (Catering Income). g. Bought supplies for cash, 185, Ck. No. 503. h. Sold catering services on account, 4,307 (Catering Income). i. Received and paid the heating bill, 248, Ck. No. 504 (Utilities Expense). j. Received a bill from GC Gas and Lube for gas and oil for the truck, 128 (Gas and Oil Expense). k. Sold catering services for cash for the remainder of the month, 2,649 (Catering Income). l. Gervais withdrew cash for personal use, 1,550, Ck. No. 505. m. Paid the salary of the assistant, 1,150, Ck. No. 506 (Salary Expense). Required 1. In the equation, write the owners name above the terms Capital and Drawing. 2. Record the transactions and the balance after each transaction. Identify the account affected when the transaction involves revenues or expenses. 3. Write the account totals from the left side of the equals sign and add them. Write the account totals from the right side of the equals sign and add them. If the two totals are not equal, check the addition and subtraction. If you still cannot find the error, re-analyze each transaction.arrow_forward

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning Corporate Financial AccountingAccountingISBN:9781305653535Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Corporate Financial AccountingAccountingISBN:9781305653535Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Financial & Managerial AccountingAccountingISBN:9781337119207Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial & Managerial AccountingAccountingISBN:9781337119207Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning

Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning College Accounting (Book Only): A Career ApproachAccountingISBN:9781305084087Author:Cathy J. ScottPublisher:Cengage Learning

College Accounting (Book Only): A Career ApproachAccountingISBN:9781305084087Author:Cathy J. ScottPublisher:Cengage Learning