Subpart (a)

Calculate and illustrate the

Subpart (a)

Explanation of Solution

Given information:

The equilibrium for the market of DVD s is attained when the price is $4 and the quantity is 18 million.

The consumer surplus when the

Thus, the consumer surplus is $18.

The producer surplus when the equilibrium price is P and the quantity is Q is calculated using Equation (2) as shown below:

Thus, the producer surplus is $18.

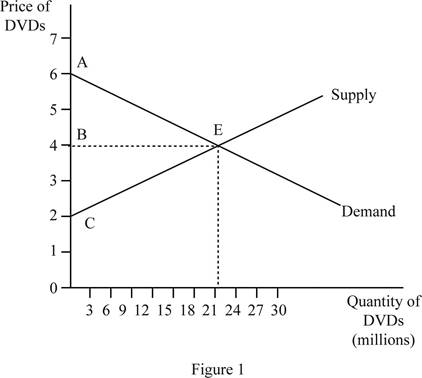

Figure 1 illustrates the consumer surplus and producer surplus.

Figure 1 shows the equilibrium where the quantity of DVDs is plotted along the horizontal axis and the price of DVDs is plotted along the vertical axis. The consumer surplus is obtained by the area of the triangle ABE and the producer surplus is obtained by the area of triangle CBE.

Consumer Surplus: The consumer surplus is defined as the difference between the maximum amount a person is willing to pay for consuming a commodity and the actual price the person pays for it.

Producer Surplus: The producer surplus is defined as the difference between the actual market price for which a commodity is sold and the minimum cost at which the producer is willing to sell the commodity. This minimum accepted price is usually the cost of production of the commodity.

Subpart (b)

The total consumer surplus, producer surplus, and dead weight loss when there is underproduction and show them on the graph.

Subpart (b)

Explanation of Solution

Given information:

The equilibrium for the market of DVD s is attained when the price is $4 and the quantity is 18 million. The underproduction leads to the production of 9 million DVDs.

When the production reduces to 9 million, the consumer surplus is calculated as follows:

Thus, the consumer surplus at underproduction of 9 million DVD s is $13.5 million.

When the production reduces to 9 million, the producer surplus is calculated as follows:

Thus, the producer surplus at underproduction of 9 million DVDs is $13.5 million.

The

Thus, the deadweight loss of underproduction is $9 million.

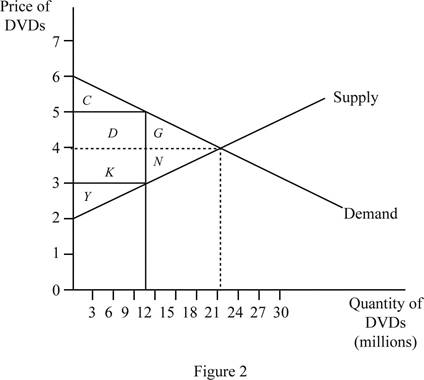

Figure 2 illustrates the deadweight loss.

Figure 2 shows the market for DVD s with underproduction. The horizontal axis measures the quantity of DVDs and the vertical axis measures the price of DVDs. The underproduction results in a deadweight loss which is shown by the area of G and N.

Consumer Surplus: The consumer surplus is defined as the difference between the maximum amount a person is willing to pay for consuming a commodity and the actual price the person pays for it.

Producer Surplus: The producer surplus is defined as the difference between the actual market price for which a commodity is sold and the minimum cost at which the producer is willing to sell the commodity. This minimum accepted price is usually the cost of production of the commodity.

Deadweight loss: The deadweight loss is defined as the loss of the total consumer surplus and producer surplus due to overproduction or underproduction.

Subpart (c)

The total consumer surplus, producer surplus, and dead weight loss when there is overproduction and show them on the graph.

Subpart (c)

Explanation of Solution

Given information:

The equilibrium for the market of DVD s is attained when the price is $4 and the quantity is 18 million. The overproduction leads to the production of 27 million DVDs.

When there is overproduction, the consumer surplus is calculated same as the consumer surplus at equilibrium.

Thus, the consumer surplus is $18.

The producer surplus of overproduction is same as the equilibrium producer surplus and is calculated using Equation (2) as follows:

Thus, the producer surplus is $18.

The deadweight loss of over production is equal to the area of the triangle EFG. It can be calculated as follows:

Thus, the deadweight loss of overproduction is $9 million.

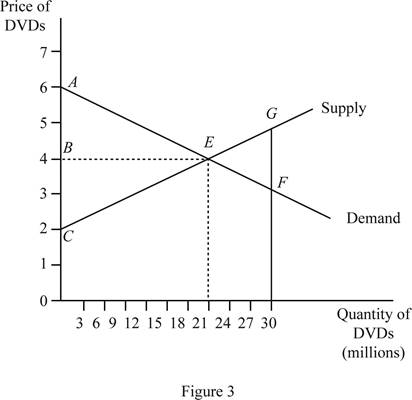

Figure 3 illustrates the deadweight loss.

Figure 3 shows the equilibrium where the quantity of DVDs is plotted along the horizontal axis and the price of DVDs is plotted along the vertical axis. The consumer surplus is obtained by the area of the triangle ABE and the producer surplus is obtained by the area of triangle CBE. Due to overproduction, there is a deadweight loss which is equal to the area of the triangle EFG.

Consumer Surplus: The consumer surplus is defined as the difference between the maximum amount a person is willing to pay for consuming a commodity and the actual price the person pays for it.

Producer Surplus: The producer surplus is defined as the difference between the actual market price for which a commodity is sold and the minimum cost at which the producer is willing to sell the commodity. This minimum accepted price is usually the cost of production of the commodity.

Deadweight loss: The deadweight loss is defined as the loss of the total consumer surplus and producer surplus due to overproduction or underproduction.

Want to see more full solutions like this?

Chapter 4 Solutions

PRINCIPLES OF MICROECONOMICS

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education