Concept explainers

Videos

Integration of financial statements; Chapters 3 and 4

• LO4–8

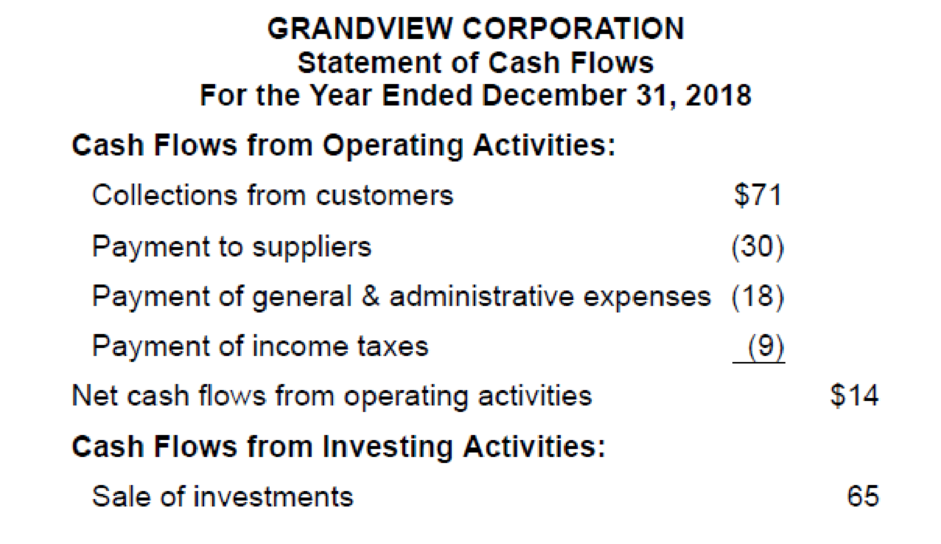

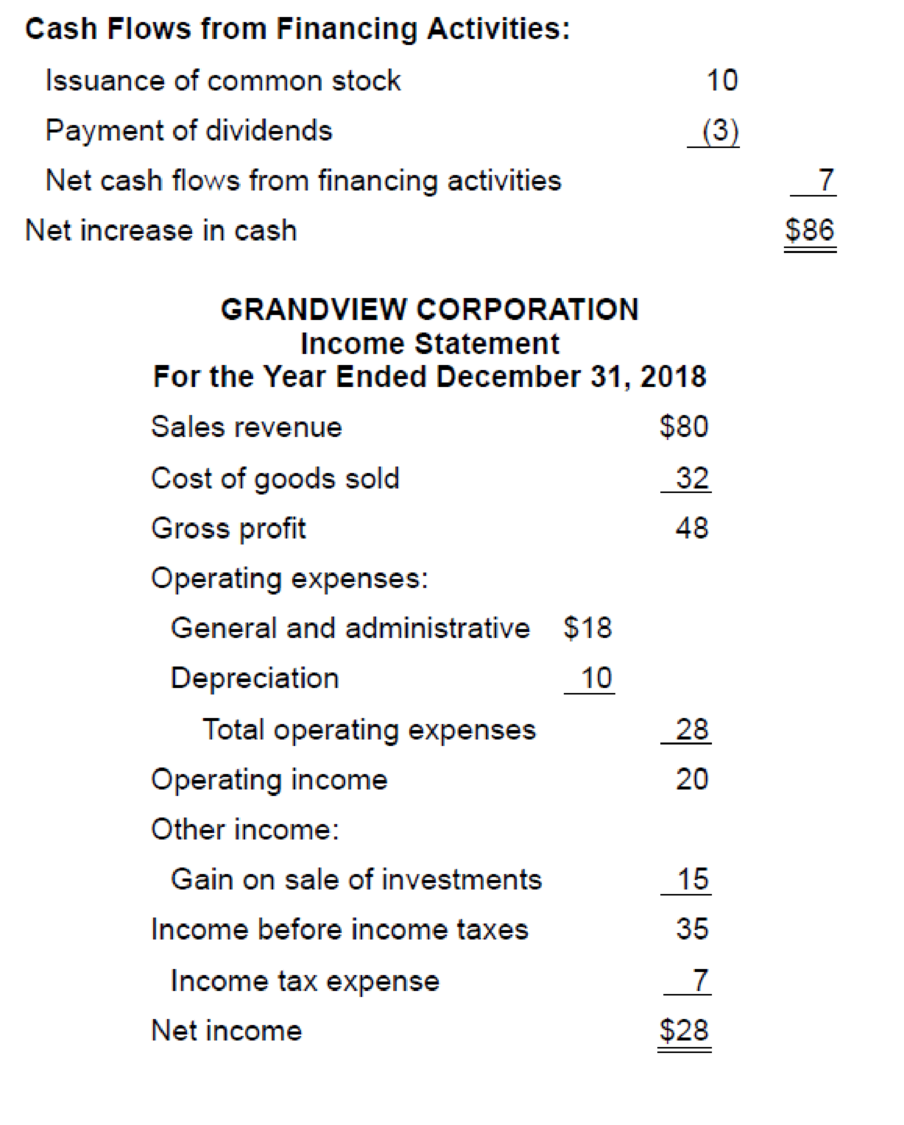

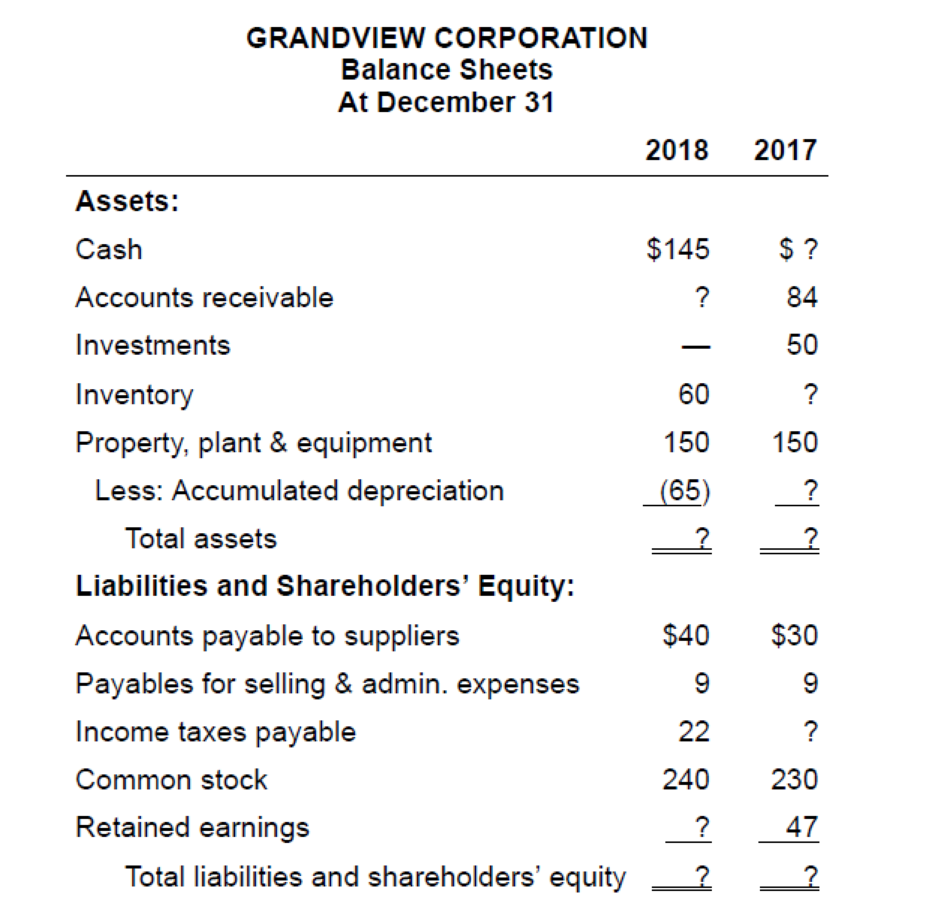

The chief accountant for Grandview Corporation provides you with the company’s 2018 statement of cash flows and income statement. The accountant has asked for your help with some missing figures in the company’s comparative balance sheets. These financial statements are shown next ($ in millions).

Required:

1. Calculate the missing amounts.

2. Prepare the operating activities section of Grandview’s 2018 statement of cash flows using the indirect method.

(1)

Financial statement:

A financial statement is the complete record of financial transactions that take place in a company at a particular point of time. It provides important financial information regardingthe assets, liabilities, revenues and expenses of the company to its internal and external users. It helps them to know the exact financial position of the company.

To calculate: the missing amounts.

Explanation of Solution

Calculate the missing amounts.

Cash Balance – 2017:

Accounts receivable-2018:

Inventory – 2018:

Calculate the purchase:

Calculate Inventory – 2017:

Accumulated Depreciation – 2017:

Calculate total assets:

| Total Assets | 2018($) | 2017($) |

| Cash | 145 | 59 |

| Accounts Receivable | 93 | 84 |

| Investments | - | 50 |

| Inventory | 60 | 52 |

| Property, plant, and equipment | 150 | 150 |

| Less: Accumulated Depreciation | (65) | (55) |

| Total Assets | $383 | $340 |

Table (1)

Calculate Income tax payable – 2017

Calculate retained earnings -2018:

Calculate total liabilities and shareholders’ equity:

| Total Liabilities and Stockholder’s Equity | 2018($) | 2017($) |

| Accounts payable to suppliers | 40 | 30 |

| Payables for selling and administrative expenses | 9 | 9 |

| Income taxes payable | 22 | 24 |

| Common stock | 240 | 230 |

| Retained earnings | 72 | 47 |

| Total Assets | $383 | $340 |

Table (2)

(2)

To prepare: Operating activities section of Corporation G’s cash flow statement using indirect method.

Explanation of Solution

Prepare the operating activities of Corporation G for 2018 statement of cash flows using indirect method.

| Corporation G | ||

| Statement of Cash Flows - Indirect Method (Partial) | ||

| For the Year 2018 | ||

| Particulars | Amount ($) | Amount ($) |

| Cash flows from Operating activities: | ||

| Net income | 28 | |

| Adjustments for noncash effects: | ||

| Depreciation expense | 10 | |

| Gain on sale of investments | (15) | |

| Changes in operating assets and liabilities | ||

| Increase in accounts receivable(1) | (9) | |

| Increase in inventory(2) | (8) | |

| Increase in accounts payable(3) | 10 | |

| Decrease in income taxes payable(4) | (2) | (14) |

| Net cash flows from operating activities | $14 | |

Table (3)

Working notes:

Determine changes of assets and liabilities:

Want to see more full solutions like this?

Chapter 4 Solutions

INTERMEDIATE ACCT.(LL)W/CONNECT ACCESS

- Statement of cash flows direct method The comparative balance sheet of Martinez Inc. for December 31, 20Y4 and 20Y3, is as follows: Dec. 31, 20Y4 Dec. 31, 20Y3 Assets Cash 661,920 683,100 Accounts receivable (net) 992,640 914,400 Inventories 1,394,400 1,363,800 Investments 0 432,000 Land 960,000 0 Equipment 1,224,000 984,000 Accumulated depreciationequipment (481,500) (368,400) Total assets 4,751,460 4,008,900 Liabilities and Stockholders' Equity Accounts payable (merchandise creditors) 1,080,000 966,600 Accrued expenses payable (operating expenses) 67,800 79,200 Dividends payable 100,800 91,200 Common stock, 5 par 130,000 30,000 Paid in capital: Excess of issue price over parcommon stock 950,000 450,000 Retained earnings 2,422,860 2,391,900 Total liabilities and stockholders' equity 4,751,460 4,008,900 The income Statement for the year ended December 51. 20Y3. is as follows: Sales 4,512,000 Cost of goods sold 2,352,000 Gross profit 2,160,000 Operating expenses: Depredation expense 113,100 Other operating expenses 1,344,840 Total operating expenses 1,457,940 Operating income 702,060 Other income: Gain on sale of investments 156,000 Income before income tax 858,060 Income tax expense 299,100 Net income 558,960 Additional data obtained from an examination of the accounts in the ledger for 20Y3 are as follows: A. Equipment and land were acquired for cash. B. There were no disposals of equipment during the year. C. The investments were sold for 588,000 cash. D. The common stock was issued for cash. E. There was a 528,000 debit to Retained Earnings for cash dividends declared. Instructions Prepare a statement of cash flows, using the direct method of presenting cash flows from operating activities.arrow_forwardStatement of cash flowsdirect method applied to PR 1618 The Comparative balance sheet of Merrick Equipment Co. for Dec. 31, 20Y9 and 20Y8, is as follows: Dec. 31, 20Y9 Dec. 31, 20Y8 Assets Cash.................................. 70,720 47,940 Accounts receivable (net).................................. 207,230 188,190 Inventories............................................... 298,520 289,850 Investments.............................................. 0 102,000 Land..................................................... 295,800 0 Equipment................................................ 438,600 358,020 Accumulated depreciationequipment.................... (99,110) (184,320) Total assets............................................ 1,211,760 901,680 Liabilities and Stockholders' Equity Accounts payable......................................... 205,700 194,140 Accrued expenses payable................................. 30,600 26,860 Dividends payable....................................... 25,500 20,400 Common stock, 1 par..................................... 202,000 102,000 Paid-in capital: Excess of issue price over parcommon stock...... 354,000 204,000 Retained earnings......................................... 393,960 354,280 Total liabilities and stockholders' equity.................. 1,211,760 901,680 The income statement for the year ended December 31. 20Y9, is as follows: Sales........................................... 2,023,898 Cost of merchandise sold........................ 1,245,476 Gross profit..................................... 778,422 Operating expenses: Depreciation expense........................ 14,790 Other operating expenses.................... 517,299 Total operating expenses.................. 532,089 Operating income............................... 246,333 Other expenses: Loss on sale of investments................... (10,200) Income before income tax....................... 236,133 Income tax expense............................. 94,453 Net income..................................... 141,680 Additional data obtained from an examination of the accounts in the ledger for 20Y9 are as follows: a. Equipment and land were acquired for cash. b. There were no disposals of equipment during the year. c. The investments were sold for 91,800 cash. d. The common stock was issued for cash. e. There was a 102,000 debit to Retained Earnings for cash dividends declared. Instructions Prepare a statement of cash flows, using the direct method of presenting cash flows from operating activities.arrow_forwardStatement of cash flowsdirect method The comparative balance sheet of Martinez Inc. for December 31, 20Y4 and 20Y3, is as follows: Dec 31, 20Y4 Dec. 31,20Y3 Assets Cash.................................. 661,920 683,100 Accounts receivable (net).................................. 992,640 0 914,400 Inventories............................................... 1,394,40 1,363,800 Investments.............................................. 0 432,000 Land..................................................... 960,000 0 Equipment................................................ 1,224,000 984,000 Accumulated depreciationequipment.................... (481,500) (368,400) Total assets............................................ 4,751,460 4,008,900 Liabilities and Stockholders' Equity Accounts payable......................................... 1,080,000 966,600 Accrued expenses payable................................ 67,800 79,200 Dividends payable.................................. 100,800 91,200 Common stock. S par .................................... 130,000 30,000 Paid in capital: Excess of issue price over parcommon stock...... 950,000 450,000 Retained earnings......................................... 2,422,860 2,391,900 Total liabilities and stockholders' equity.................. 4,751,460 4,008,900 The income statement for the year ended December 31, 20Y4, is as follows: Sales.......................................... 4,512,000 Cost of merchandise sold....................... 2,352,000 Gross profit.................................... 2,160,000 Operating expenses: Depreciation expense....................... 113,100 Other operating expenses................... 1,344,840 Total operating expenses................. 1,457,940 Operating income.............................. 702,060 Other income: Gain on sale of investments.................. 156,000 Income before income tax...................... 858,060 Income tax expense............................ 299,100 Net income.................................... 558,960 Additional data obtained from an examination of the accounts in the ledger for 20Y4 are as follows: a. Equipment and land were acquired for cash. b. There were no disposals of equipment during the year. c. The investments were sold for 588,000 cash. d. The common stock was issued for cash. e. There was a 528,000 debit to Retained Earnings for cash dividends declared. Instructions Prepare a statement of cash flows, using the direct method of presenting cash flows from operating activities.arrow_forward

- Statement of cash flowsindirect method The comparative balance sheet of Coulson, Inc. it December 31, 20Y2 and 20Y1, is as follows: Dec. 31, 20Y2 Dec. 31, 20Y1 Assets Cash 300,600 337,800 Accounts receivable (net) 704,400 609,600 Inventories 918,600 865,800 Prepaid expenses 18,600 26,400 Land 990,000 1,386,000 Buildings 1,980,000 990,000 Accumulated depreciationbuildings (397,200) (366,000) Equipment 660,600 529,800 Accumulated depreciationequipment (133,200) (162,000) Total assets 5,042,400 4,217,400 Liabilities and Stockholders' Equity Accounts payable 594,000 631,200 Income taxes payable 26,400 21,600 Bonds payable 330,000 0 Common stock, 20 par 320,000 180,000 Paid in capital: Excess of issue price over parcommon stock 950,000 810,000 Retained earnings 2,822,000 2,574,600 Total liabilities and stockholders' equity 5,042,400 4,217,400 The noncurrent asset, noncurrent liability, and stockholders equity accounts for 20Y2 are as follows: Instructions Prepare a statement of cash flows, using the indirect method of presenting cash flows from operating activities.arrow_forwardStatement of cash flowsdirect method applied to PR 131B The comparative balance sheet of Merrick Equipment Co. for Dec. 31, 20Y9 and 20Y8, is: Dec. 31, 20Y9 Dec. 31, 20Y8 Assets Cash 70,720 47,940 Accounts receivable (net) 207,230 188,190 Inventories 298,520 289,850 Investments 0 102,000 Land 295,800 0 Equipment 438,600 358,020 Accumulated depreciationequipment (99,110) (84,320) Total assets 1,211,760 901,680 Liabilities and Stockholders' Equity Accounts payable (merchandise creditors).................. 205,700 194,140 Accrued expenses payable (operating expenses) 30,600 26,860 Dividends payable 25,500 20,400 Common stock. 1 par 202,000 102,000 Paid-in capital: Excess of issue price over parcommon stock 354,000 204,000 Retained earnings 393,960 354,280 Total liabilities and stockholders' equity 1,211,760 901,680 The income statement for the year ended December 31,20Y9, is as fallow s: Sales 2,023,898 Cost of goods sold 1,245,476 Gross profit 778,422 Operating expenses: Depreciation expense 14,790 Other operating expenses 517,299 Total operating expenses 532,089 Operating income 246,333 Other expenses: Loss on sale of investments (10,200) Income before income tax 236,133 Income tax expense 94,453 Net income 141,680 Additional data obtained from an examination of the- accounts in the ledger for 20Y9 are as follows: A. Equipment and land were acquired for cash. B. There were no disposals of equipment during the year. C. The investments were sold for 91,800 cash. D. The common stock was issued for cash. E. There was a 102,000 debit to Retained Earnings for cash dividends declared. Instructions Prepare a statement of cash flows, using the direct method of presenting cash flows from operating activities.arrow_forwardStatement of cash flowsindirect method The comparative balance sheet of Harris Industries Inc. at December 31, 20Y4 and 20Y3, is as follows: Dec 31, 20Y4 Dec 31, 20Y3 Assets Cash 443,240 360,920 Accounts receivable (net) 665,280 592,200 Inventories 887,880 1,022,560 Prepaid expenses 31,640 25,200 Land 302,400 302,400 Buildings 1,713,600 1,134,000 Accumulated depreciationbuildings (466,200) (414,540) Machinery and equipment 781,200 781,200 Accumulated depreciationmachinery and equipment (214,200) (191,520) Patents 106,960 112,000 Total assets 4,251,800 3,724,420 Liabilities and Stockholders' Equity Accounts payable 837,480 927,080 Dividends payable 32,760 25,200 Salaries payable 78,960 87,080 Mortgage note payable, due in 10 years 224,000 0 Bonds payable 0 390,000 Common stock, S par 200,400 50,400 Paid-in capital: Excess of issue price over parcommon stock 366,000 126,000 Retained earnings 2,512,200 2,118,660 Total liabilities and stockholders' equity 4,251,800 3,724,420 An examination of the income statement and the accounting records revealed the following additional information applicable to 20Y4: a. Net income, 524,580. b. Depreciation expense reported on the income statement: buildings, 51,660; machinery and equipment, 22,680. c. Patent amortization reported on the income statement, 5,040. d. A building was constructed for 579,600. e. A mortgage note for 224,000 was issued for cash. f. 30.000 shares of common stock were issued at 13 in exchange for the bonds payable. g. Cash dividends declared, 131,040. Instructions Prepare a statement of cash flows, using the indirect method.arrow_forward

- Statement of cash flowsindirect method The comparative balance sheet of Whitman Co. at December 31, 20Y2 and 20Y1, is as follows: Dec. 31, 20Y2 Dec. 31, 20Y1 Assets Cash. 918,000 964,800 Accounts receivable (net) 828,900 761,940 Inventories 1,268,460 1,162,980 Prepaid expenses 29,340 35,100 Land 315,900 479,700 Buildings 1,462.500 900,900 Accumulated depreciationbuildings (408,00) (382,320) Equipment 512,280 454,680 Accumulated depreciationequipment (141,300) (158,760) Total assets 4,785,480 4,219,020 Liabilities and Stockholders' Equity Accounts payable (merchandise creditors) 922,500 958.320 Bonds payable 270,000 0 Common stock. 25 par 317,000 117,000 Paid-in capital: Excess of issue price over parcommon stock 758,000 558,000 Retained earnings 2,517,980 2,585,700 Total liabilities and stockholders' equity 4,785,480 4,219,020 The noncurrent asset, noncurrent liability, and stockholders' equity accounts for 20Y2 are as follows: Instructions Prepare a statement of cash flows, using the indirect method of presenting cash flows from operating activities.arrow_forwardEthics in Action Lucas Hunter, president of Simmons Industries Inc., believes that reporting operating cash flow per share on the income statement would be a useful addition to the companys just completed financial statements. The following discussion took place between Lucas Hunter and Simmons' controller, John Jameson, in January, after the close of the fiscal year: Lucas: Ive been reviewing our financial statements for the last year. I am disappointed that our net income per share has dropped by 10% from last year. This won't look good to our shareholders. Is there anything we can do about this? John. What do you means? The past is the past, and the numbers are in. There isnt much that can be done about it Our financial statements were prepared according to generally accepted accounting principles, and I dont see much leeway for significant change at this point. Lucan No, no. Ive not suggesting that we cook the books. But look at the cash flow from operating activities on the statement of cash flows. The cash flow from operating activities has increased by 20%. This is very good newsand. I might add, useful information. The higher cash flow from operating activities will give our creditors comfort. John. Well, the cash flow from operating activities is on the statement of cash flows, so I guess users will be able to see the improved cash flow figures there Lucas: This is true, but somehow I think this information should be given a much higher profile. I don't like this information being buried in the statement of cash flows. You know as well as I do that many users will focus on the income statement Therefore. I think we ought to include an operating cash flow per share number on the face of the income statementsomeplace under the earnings per share number In this way, users will get the complete picture of our operating performance. Yes, our earnings per share dropped this year, but our cash flow from operating activities improved! And all the information is in one place where users can see and compare the figures. What do you think? John I've never really thought about it like that before I guess we could put the operating cash flow per share on the income statement, underneath the earnings per share amount. Users would really benefit from this disclosure. Thanks for the ideaI'll start working on it. Lucas: Glad to be of service. How would you interpret this situation? Is John behaving in an ethical and professional manner?arrow_forwardStatement of cash flows direct method applied to PR 131A The comparative balance sheet of Livers Inc. for December 31, 20Y3 and 20Y2 is as follows: Dec. 31, 20Y3 Dec. 31, 20Y2 Assets Cash 155,000 150,000 Accounts receivable (net) 450,000 400,000 Inventories 770,000 750,000 Investments 0 100,000 Land 500,000 0 Equipment 1,400,000 1,200,000 Accumulated depreciationequipment (600,000) (500,000) Total assets Liabilities and Stockholders' Equity 2,675,000 2,100,000 Accounts payable (merchandise creditors) 340,000 300,000 Accrued expenses payable (operating expenses) 45,000 50,000 Dividends payable 30,000 25,000 Common stock, 4 par 700,000 600,000 Paid-in capital: Excess of issue price over parcommon stock 200,000 175,000 Retained earnings 1,360,000 950,000 Total liabilities and stockholders' equity 2,675,000 2,100,000 The income statement for the year ended December 31, 20Y3, is as follows: Sales 3,000,000 Cost of goods sold 1,400,000 Gross profit 1,600,000 Operating expenses: Depreciation expense 100,000 Other operating expenses. 950,000 Total operating expenses 1,050,000 Operating income 550,000 Gain on sale of investments 75,000 Income before income tax 625,000 Income tax expense 125,00 Net income 500,000 Additional data obtained from an examination of the accounts in the ledger for 20Y3 are as follows: A. The investments were sold for 175,000 cash. B. Equipment and land were acquired for cash. C. There were no disposals of equipment during the year. D. The common stock was issued for cash. E. There was a 90,000 debit to Retained Earnings for cash dividends declared. Instructions Prepare a .statement of cash flows, using the direct method of presenting cash flows from operating activities.arrow_forward

- Q 23.21: Last year, Alpha Corporation spent $250,000 to repurchase 15,000 shares of its own outstanding common stock. The company also paid $40,000 in interest on a construction loan that it had obtained from its bank. How should these transactions be reflected on Alpha’s annual statement of cash flows, and why? A : The two transactions should be reported in separate sections of the statement because one involves long-term assets while the other involves long-term liability. Specifically, Alpha should record a $250,000 cash outflow in the investing section and a $40,000 cash outflow in the financing section. B : The two transactions should be reported in separate sections of the statement because one involves a change in equity while the other involves a change in income. Specifically, Alpha should record a $250,000 cash outflow in the financing section and a $40,000 cash outflow in the operating section. C : Both transactions should be reported in the…arrow_forwardProblem 11-2A Classify items and prepare the statement of cash flows (LO11-1, 11-3, 11-4, 11-5) Seth Erkenbeck, a recent college graduate, has just completed the basic format to be used in preparing the statement of cash flows (indirect method) for ATM Software Developers. All amounts are in thousands (000s). ATM SOFTWARE DEVELOPERS Statement of Cash Flows For the year ended December 31, 2021 Cash Flows from Operating Activities Net income $ Adjustments to reconcile net income to net cash flows from operating activities: Net cash flows from operating activities Cash Flows from Investing Activities Net cash flows from investing activities Cash Flows from Financing Activities Net cash flows from financing activities Net increase (decrease) in cash $ 2,805 Cash at the beginning of the period 7,180 Cash at the end of the period $ 9,985 Listed below in random order are line items to be included in…arrow_forward

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning Corporate Financial AccountingAccountingISBN:9781305653535Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Corporate Financial AccountingAccountingISBN:9781305653535Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Financial & Managerial AccountingAccountingISBN:9781337119207Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial & Managerial AccountingAccountingISBN:9781337119207Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Corporate Financial AccountingAccountingISBN:9781337398169Author:Carl Warren, Jeff JonesPublisher:Cengage Learning

Corporate Financial AccountingAccountingISBN:9781337398169Author:Carl Warren, Jeff JonesPublisher:Cengage Learning