Concept explainers

Videos

Ledger accounts,

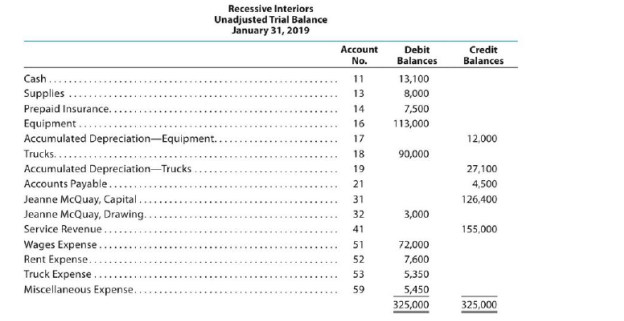

The unadjusted

The data needed to determine year-end adjustments are as follows:

- a. Supplies on hand at January 31 are $2,850.

- b. Insurance premiums expired during the year are $3,150.

- c.

Depreciation of equipment during the year is $5,250. - d. Depreciation of trucks during the year is $4,000.

- e. Wages accrued but not paid at January 31 are $900.

Instructions

- 1. For each account listed in the unadjusted trial balance, enter the balance in the appropriate Balance column of a four-column account and place a check mark (✓) in the Posting Reference column.

- 2. (Optional) Enter the unadjusted trial balance on an end-of-period spreadsheet and complete the spreadsheet. Add the accounts listed in part (3) as needed.

- 3. Journalize and post the adjusting entries, inserting balances in the accounts affected.

- a. Record the adjusting entries on Page 26 of the journal. The following additional accounts from Recessive Interiors' chart of accounts should be used: Wages Payable, 22; Depreciation Expense—Equipment, 54; Supplies Expense, 55; Depreciation Expense—Trucks, 56; Insurance Expense, 57.

- 4. Prepare an adjusted trial balance.

- 5. Prepare an income statement, a statement of owner's equity (no additional investments were made during the year), and a balance sheet.

- 6. Journalize and

post the closing entries. Record the closing entries on Page 27 of the journal. Indicate closed accounts by inserting a line in both Balance columns opposite the closing entry. - 7. Prepare a post-closing trial balance.

1, 3, and 6:

Journal:

Journal is the book of original entry. Journal consists of the day-to-day financial transactions in a chronological order. The journal has two aspects; they are debit aspect and the credit aspect.

T-Accounts:

T-accounts are referred as T-account because its format represents the letter “T”. The T-accounts consists of the following:

Ø The title of accounts.

Ø The debit side (Dr) and,

Ø The credit side (Cr).

Adjusted trial balance:

The unadjusted trial balance is the summary of all the ledger accounts that appears on the ledger accounts before making adjusting journal entries.

Adjusting entries:

An adjusting entry is prepared when the trial balance is not up-to-date, and complete, and they are usually prepared at the end of the accounting period. This adjusting entry is essential for preparing the financial statements of the business.

Spreadsheet:

A spreadsheet is a worksheet. It is used while preparing a financial statement. It is a type of form having multiple columns and it is used in the adjustment process. The use of a worksheet is optional for any organization. A worksheet can neither be considered as a journal nor a part of the general ledger.

Statement of owners’ equity:

This statement reports the beginning owner’s equity and all the changes, which led to ending owners’ equity. Additional capital, net income from income statement is added to and drawing is deducted from beginning owner’s equity to arrive at the end result, ending owner’s equity.

Income statement:

An income statement is one of the financial statements which shows the revenues, and expenses of the company. The income statement is prepared to ascertain the net income/loss of the company, by deducting the expenses from the revenues.

Balance sheet:

A balance sheet is a financial statement consists of the assets, liabilities, and the stockholder’s equity of the company. The balance of the assets account must be equal to that of the liabilities and the stockholder’s equity account.

Closing entries:

Closing entries are recorded in order to close the temporary accounts such as incomes and expenses by transferring them to the permanent accounts. It is passed at the end of the accounting period, to transfer the final balance.

Post-Closing Trial Balance:

After passing all the journal entries and the closing entries of the permanent accounts and then further posting them to each of the respective accounts, a post-closing trial balance is prepared which consists of a list of all the permanent accounts. A post-closing trial balance serves as an evidence to prove that the balance of the permanent accounts is equal.

To prepare: The T-accounts.

Explanation of Solution

Record the transactions directly in their respective T-accounts, and determine their balances.

| Account: Cash Account no. 11 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| January | 1 | Balance | ✓ | 13,100 | |||

| Account: Supplies Account no. 13 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| January | 31 | Balance | ✓ | 8,000 | |||

| 31 | Adjusting | 26 | 5,150 | 2,850 | |||

| Account: Prepaid Insurance Account no. 14 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| January | 31 | Balance | ✓ | 7,500 | |||

| 31 | Adjusting | 26 | 3,150 | 4,350 | |||

| Account: Equipment Account no. 16 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| January | 31 | Balance | ✓ | 113,000 | |||

| Account: Accumulated Depreciation-Office equipment Account no. 17 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| January | 31 | Balance | ✓ | 12,000 | |||

| 31 | Adjusting | 26 | 5,250 | 17,250 | |||

| Account: Trucks Account no. 18 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| January | 31 | Balance | ✓ | 90,000 | |||

| Account: Accumulated Depreciation- Truck Account no. 19 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| January | 31 | Balance | ✓ | 27,100 | |||

| 31 | Adjusting | 26 | 4,000 | 31,100 | |||

| Account: Accounts Payable Account no. 21 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| January | 31 | Balance | ✓ | 4,500 | |||

| Account: Wages Payable Account no. 22 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| January | 31 | Adjusting | 26 | 900 | 900 | ||

| Account: JM, Capital Account no. 31 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| January | 31 | Balance | ✓ 1 | 126,400 | |||

| 31 | Closing | 27 | 46,150 | 172,550 | |||

| 31 | Closing | 27 | 3,000 | 169,550 | |||

| Account: JM, Drawing Account no. 32 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| January | 31 | Balance | ✓ | 3,000 | |||

| 31 | Closing | 27 | 3,000 | ||||

| Account: Service revenue Account no. 41 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| January | 31 | Balance | ✓ | 155,000 | |||

| 31 | Closing | 27 | 155,000 | ||||

| Account: Wages expense Account no. 51 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| January | 1 | Balance | ✓ | 72,000 | |||

| 31 | Adjusting | 26 | 900 | 72,900 | |||

| 31 | Closing | 27 | 72,900 | ||||

| Account: Rent expense Account no. 52 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| January | 31 | Balance | ✓ | 7,600 | |||

| 31 | Closing | 27 | 7,600 | ||||

| Account: Truck Expense Account no. 53 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| January | 31 | Balance | ✓ | 5,350 | |||

| 31 | Closing | 27 | 5,350 | ||||

| Account: Depreciation Expense- Equipment Account no. 54 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| January | 31 | Adjusting | 26 | 5,250 | 5,250 | ||

| 31 | Closing | 27 | 5,250 | ||||

| Account: Supplies Expenses Account no. 55 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| January | 31 | Adjusting | 26 | 5,150 | 5,150 | ||

| 31 | Closing | 27 | 5,150 | ||||

| Account: Depreciation Expense- Trucks Account no. 56 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| January | 31 | Adjusting | 26 | 4,000 | 4,000 | ||

| 31 | Closing | 27 | 4,000 | ||||

| Account: Insurance expense Account no. 57 | ||||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | |||

| Debit ($) | Credit ($) | |||||||

| 2019 | ||||||||

| January | 31 | Adjusting | 26 | 3,150 | 3,150 | |||

| 31 | Closing | 27 | 3,150 | |||||

| Account: Miscellaneous expense Account no. 59 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| January | 1 | Balance | ✓ | 5,450 | |||

| 31 | Closing | 27 | 5,450 | ||||

2.

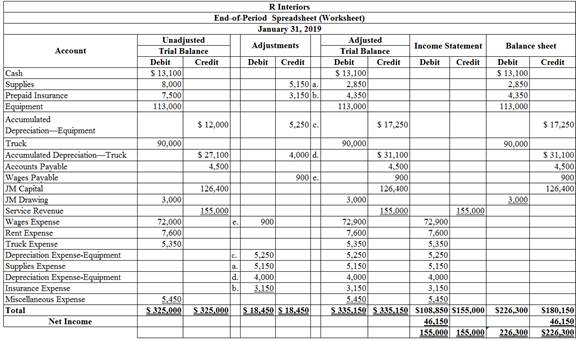

To enter: The unadjusted trial balance on an end-of-period spreadsheet, and complete the spreadsheet.

Explanation of Solution

The unadjusted trial balance on an end-of-period spreadsheet is prepared as follows:

Table (1)

Hence, the unadjusted trial balance on an end-of-period spreadsheet is prepared and completed.

3.

To Journalize and post: The adjusting entries.

Explanation of Solution

The adjusting entries are journalized as follows:

| Date | Description |

Post Ref. | Debit ($) | Credit ($) | |

| 2019 | Wages expense | 51 | 900 | ||

| January | 31 | Wages payable | 22 | 900 | |

| (To record the wages accrued) | |||||

Table (2)

Explanation:

- Wages expense is an expense account, and it is increased. Hence, debit the wages expense account by $900.

- Wages payable is a liability account, and it is increased. Hence, credit the wages payable account by $900.

| Date | Description |

Post Ref. | Debit ($) | Credit ($) | |

| 2019 | Depreciation expense-Equipment | 54 | 5,250 | ||

| January | 31 | Accumulated depreciation- Equipment | 17 | 5,250 | |

| (To record the equipment depreciation) | |||||

Table (3)

Explanation:

- Depreciation expense is an expense account, and it is increased. Hence, debit the wages expense account by $5,250.

- Accumulated depreciation is a contra asset account, and it is increased. Hence, credit the accumulated depreciation account by $5,250.

| Date | Description |

Post Ref. | Debit ($) | Credit ($) | |

| 2019 | Depreciation expense-Truck | 56 | 4,000 | ||

| January | 31 | Accumulated depreciation- Truck | 19 | 4,000 | |

| (To record the truck depreciation) | |||||

Table (4)

Explanation:

- Depreciation expense is an expense account, and it is increased. Hence, debit the wages expense account by $4,000.

- Accumulated depreciation is a contra asset account, and it is increased. Hence, credit the accumulated depreciation account by $4,000.

| Date | Description |

Post Ref. | Debit ($) | Credit ($) | |

| 2019 | Supplies expense | 55 | 5,150 | ||

| January | 31 |

Supplies

| 13 | 5,150 | |

| (To record the supplies expense) | |||||

Table (5)

Explanation:

- Supplies expense is an expense account, and it is increased. Hence, debit the supplies expense account by $5,150.

- Supplies are the asset account, and it is increased. Hence, credit the supplies account by $5,150.

| Date | Description |

Post Ref. | Debit ($) | Credit ($) | |

| 2019 | Insurance expense | 57 | 3,150 | ||

| January | 31 | Prepaid insurance | 14 | 3,150 | |

| (To record the insurance expense) | |||||

Table (6)

Explanation:

- Insurance expense is an expense account, and it is increased. Hence, debit the insurance expense account by $3,150.

- Prepaid insurance is an asset account, and it is decreased. Hence, credit the prepaid insurance account by $3,150.

4.

To prepare: An adjusted trial balance for R interiors, as of January 31, 2019.

Explanation of Solution

Prepare an adjusted trial balance for R interiors, as of January 31, 2019.

| R interiors | |||

| Adjusted Trial Balance | |||

| January 31, 2019 | |||

| Accounts | Account Number | Debit Balances | Credit Balances |

| Cash | 11 | 13,100 | |

| Supplies | 13 | 2,850 | |

| Prepaid Insurance | 14 | 4,350 | |

| Equipment | 16 | 113,000 | |

| Accumulated depreciation- Equipment | 17 | 17,250 | |

| Trucks | 18 | 90,000 | |

| Accumulated depreciation- Trucks | 19 | 31,100 | |

| Accounts payable | 21 | 4,500 | |

| Wages Payable | 22 | 900 | |

| JM, Capital | 31 | 126,400 | |

| JM, Drawing | 32 | 3,000 | |

| Service revenue | 41 | 155,000 | |

| Wages expense | 51 | 72,900 | |

| Rent expense | 52 | 7,600 | |

| Truck Expense | 53 | 5,350 | |

| Depreciation Expense- Equipment | 54 | 5,250 | |

| Supplies expense | 55 | 5,150 | |

| Depreciation Expense- Trucks | 56 | 4,000 | |

| Insurance Expense | 57 | 3,150 | |

| Miscellaneous Expense | 59 | 5,450 | |

| 335,150 | 335,150 | ||

Table (7)

The debit column and credit column of the adjusted trial balance are agreed, both having balance of $335,150.

5.

Explanation of Solution

The net income of R interiors for the month of January is $46,150.

| R interiors | ||

| Income Statement | ||

| For the year ended January 31, 2019 | ||

| Particulars | Amount ($) | Amount ($) |

| Revenue: | ||

| Laundry revenue | $155,000 | |

| Expenses: | ||

| Wages Expense | $72,900 | |

| Rent Expense | 7,600 | |

| Truck Expense | 5,350 | |

| Depreciation Expense-Equipment | 5,250 | |

| Supplies Expense | 5,150 | |

| Depreciation Expense-Trucks | 4,000 | |

| Insurance Expense | 3,150 | |

| Miscellaneous Expense | 5,450 | |

| Total Expenses | 108,850 | |

| Net Income | $46,150 | |

Table (8)

Hence, the net income of R interiors for the year ended January 31, 2019 is $46,150.

6.

To Journalize: The closing entries for R interiors.

Explanation of Solution

Closing entry for revenue and expense accounts:

| Date | Accounts title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| January 31, 2019 | Service Revenue | 41 | 155,000 | |

| Wages Expense | 51 | 72,900 | ||

| Rent Expense | 52 | 7,600 | ||

| Truck Expense | 53 | 5,350 | ||

| Depreciation Expense- Equipment | 54 | 5,250 | ||

| Supplies Expense | 55 | 5,150 | ||

| Depreciation Expense- Trucks | 56 | 4,000 | ||

| Insurance Expense | 57 | 3,150 | ||

| Miscellaneous Expense | 59 | 5,450 | ||

| JM, Capital | 31 | 46,150 | ||

| (To close the revenues and expenses account. Then the balance amount are transferred to owners’ capital account) | ||||

| January 31 | JM’s Capital | 31 | 3,000 | |

| JM’ Drawing | 32 | 3,000 | ||

| (To Close the capital and drawings account) | ||||

Table (11)

Explanation:

- Service revenue is revenue account. Since the amount of revenue is closed, and transferred to JM’s capital account. Here, R interiors earned an income of $155,000. Therefore, it is debited.

- Wages Expense, Rent Expense, Insurance Expense, Utilities Expense, Laundry Supplies Expense, Depreciation Expense, JM Capital, and Miscellaneous Expense are expense accounts. Since the amount of expenses are closed to Income Summary account. Therefore, it is credited.

- Owner’s capital is a component of owner’s equity. Thus, owners ‘equity is debited since the capital is decreased on owners’ drawings.

- Owner’s drawings are a component of owner’s equity. It is credited because the balance of owners’ drawing account is transferred to owners ‘capital account

7.

To prepare: The post–closing trial balance of R interiors for the month ended January 31, 2019.

Explanation of Solution

Prepare a post–closing trial balance of R interiors for the month ended January 31, 2019 as follows:

|

R interiors Post-closing Trial Balance January 31, 2019 | |||

| Particulars |

Account Number | Debit $ | Credit $ |

| Cash | 11 | 13,100 | |

| Supplies | 13 | 2,850 | |

| Prepaid insurance | 14 | 4,350 | |

| Equipment | 16 | 113,000 | |

| Accumulated depreciation- Equipment | 17 | 17,250 | |

| Trucks | 18 | 90,000 | |

| Accumulated depreciation- Trucks | 19 | 31,100 | |

| Accounts payable | 21 | 4,500 | |

| Wages payable | 22 | 900 | |

| JM’s Capital | 31 | 169,550 | |

| Total | 223,300 | 223,300 | |

Table (12)

The debit column and credit column of the post–closing trial balance are agreed, both having balance of $223,300.

Want to see more full solutions like this?

Chapter 4 Solutions

Bundle: Accounting, 27th + Working Papers, Chapters 1-17

- Adjusting entries for prepaid insurance Instructions Chart of Accounts Journal Instructions The balance in the prepaid insurance account, before adjustment at the end of the year, is $18,565. The year end is March 31. Journalize the March 31 adjusting entry required under each of the following alternatives for determining the amount of the adjustment: (a) the amount of insurance expired during the year is $14,135; (b) the amount of unexpired insurance applicable to future periods is $4,430. Refer to the Chart of Accounts for exact wording of account titles.arrow_forwardAdjusting entries for prepaid insuranceThe prepaid insurance account had a balance of $3,000 at the beginningof the year. The account was debited for $32,500 for premiums onpolicies purchased during the year. journalize the adjusting entry required under each of the following alternatives for determining theamount of the adjustment: (A) the amount of unexpired insuranceapplicable to future periods is $4,800; (B) the amount of insuranceexpired during the year is $30,700.arrow_forwardAdjusting Entries for Prepaid Insurance The balance in the prepaid insurance account, before adjustment at the end of the year, is $8,950. Journalize the adjusting entry required under each of the following alternatives for determining the amount of the adjustment: If an amount box does not require an entry, leave it blank. a. The amount of insurance expired during the year is $6,800. b. The amount of unexpired insurance applicable to future periods is $2,150.arrow_forward

- Prepare the adjusting journal entries as of Dec 31, 2019 for the following information gathered from the ledger of Flag Company : a.) Unexpired of the Prepaid Insurance account balance of P 42,500 was P 24,500. b.) Accrued Interest on Notes issued P 1,270. c.) Equipment acquired on March 31, 2019 at P 120,000, has a scrap value of P4,000 with estimated life of 10 years. d) Unrecorded unpaid taxes P 18,500. e.) Unpaid salaries P22,500. £.) Interest received and credited to Unearned Interest Income account was P 14,000 of which only P 12,000 was eamed. g.) Office supplies has a balance of P 8,000, Consumed as of Dec 31, 2019 was P 6,800. h.) Unearned Rent Income account has a balance of P 24,000 of which P 20,000 was rent earned. i.) Office Supplies balance was P5,600 of which P1,600 was consumed. Account Title Debit Credit a.) b.) e.) (P) e.) f.) g.) h.) i)arrow_forwardAdjusting Entries for Prepaid Insurance The balance in the prepaid insurance account, before adjustment at the end of the year, is $27,000. Journalize the adjusting entry required under each of the following alternatives for determining the amount of the adjustment: a. The amount of insurance expired during the year is $20,250. b. The amount of unexpired insurance applicable to future periods is $6,750.arrow_forwardAdjusting entries for prepaid insurance Instructions Chart of Accounts Journal Instructions The balance in the prepaid insurance account, before adjustment at the end of the year, is $18,135. Journalize the March 31 adjusting entry required under each of the following alternatives for determining the amount of the adjustment: (a) the amount of insurance expired during the year is $15,480; (b) the amount of unexpired insurance applicable to future periods is $2,655. Refer to the chart of accounts for the exact wording of the account titles. CNOW journals do not use lines for journal explanations. Every line on a journal page is used for debit or credit entries. CNOW journals will automatically indent a credit entry when a credit amount is entered. Chart of Accounts CHART OF ACCOUNTS General Ledger ASSETS 11 Cash 12 Accounts Receivable 13 Supplies 14 Prepaid Insurance 15 Land 16 Equipment 17…arrow_forward

- Tamarisk Company uses special strapping equipment in its packaging business. The equipment was purchased in January 2019 for $11,600,000 and had an estimated useful life of 8 years with no salvage value. At December 31, 2020, new technology was introduced that would accelerate the obsolescence of Tamarisk's equipment. Tamarisk's controller estimates that expected future net cash flows on the equipment will be $7,308,000 and that the fair value of the equipment is $6,496,000. Tamarisk intends to continue using the equipment, but it is estimated that the remaining useful life is 4 years. Tamarisk uses straight-line depreciation.arrow_forwardThe beginning balance represented the unexpired portion of a one-year policy On Nov. 30, 2019, the end of fiscal year, the following information is available to enable year were P45,260. The ending inventory revealed supplies on hand of P 13,970. Preparing the Adjusting Entries at Year-End a. The Supplies account showed a beginning balance of P21,740. Purchases during the you you to prepare Edgar Detoya Research and Development adjusting entries: b. The Prepaid Insurance account showed the following on November 30. Beginning balance July 1 P35,800 42,000 October 1 72,720 The beginning balance represented the unexpired portion of a one-yeal pand purchased in September 2018. The July 1 entry represented a new one-year policy, eme the Oct. 1 entry is additional coverage in the form of a three-year policy. c. The following table contains the cost and annual depreciation for buildings ana equipment, all of which the entity purchased before the current year: Annual Depreciation P145,000…arrow_forwardSafety First Company completed all of its October 31,2020 adjustments in preparation for preparing its financial statements which resulted in the following trial balance Other information: All accounts have normal balances $26,400 of the Notes payable balance is due by October 31, 2021 The final task in the year end process was to access the assets for impairment, which resulted in the following schedule Required: Prepare the entries to record any impairment losses at October 31, 2020. Assume the company recorded no impairment losses in the previous years Prepare a classified balance sheet at October 31, 2020 What is the impact on the financial statements of an impairment loss?arrow_forward

- Prepare an aging schedule to determine the total estimated uncollectibles at March 31,2018arrow_forwardAt the end of 2019, Framber Company received 8,000 as a prepayment for renting a building to a tenant during 2020. The company erroneously recorded the transaction by debiting Cash and crediting Rent Revenue in 2019 instead of 2020. Upon discovery of this error in 2020, what correcting journal entry will Framber make? Ignore income taxes.arrow_forwardAssume the following data for Casper Company before its year-end adjustments: Journalize the adjusting entries for the following:a. Estimated customer allowancesb. Estimated customer returnsarrow_forward

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning