Videos

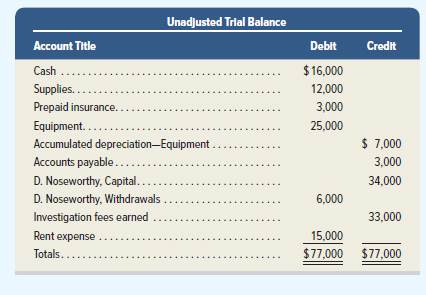

The unadjusted

Additional Year-End Information

1. Insurance that expired in the current period amounts to $2,200.

2. Equipment

3. Unused supplies total $5,000 at period-end.

4. Services in the amount of $800 have been provided but have not been billed or collected.

Responsibilities for Individual Team Members

1. Determine the accounts arid adjusted balances to be extended to the Balance Sheet columns of the work sheet for Noseworthy. Also

determine total assets and total liabilities.

2. Determine the adjusted revenue account balance and prepare the entry to close this account.

3. Determine the adjusted account balances for expenses and prepare the entry to dose these accounts.

4. Prepare T-accounts for both D. Noseworthy, Capital (reflecting the unadjusted trial balance amount) and Income Summary. Prepare the third

and fourth closing entries. Ask teammates assigned to parts 2 and 3 for the postings for Income Summary. Obtain amounts to complete the

third closing entry and post both the third and fourth closing entries. Provide the team with the ending capital account balance.

5. The entire team should prove the accounting equation using post-closing balances.

Want to see the full answer?

Check out a sample textbook solution

Chapter 4 Solutions

Fundamental Accounting Principles

- Frontland Advertising creates, plans, and handles advertising campaigns in three provinces. Recently, Frontland had to replace an inexperienced office worker in charge of bookkeeping because of some serious mistakes that had been uncovered in the accounting records. You have been hired to review these transactions to determine any corrections that might be necessary. In all cases, the bookkeeper made an accurate description of the transaction but did not correctly record the transaction in the journal. 1.For each of the preceding entries, indicate the effect of the error on cash, total assets, and net income. The answer for the first transaction has been provided as an example. Date Effect on Cash Effect on Total Assets Effect on Net IncomeMay 1 Understated $100 Overstated $100 Overstated $100 2.What is the correct balance of cash if the balance of cash on the books before correcting the preceding transactions was $6,400? 3.What is the correct amount of total assets…arrow_forwardyour line manager wants to assess your understanding and ability to prepare and produce the appropriate final accounts such as profit and loss account, owners’ equity statement, and balance sheet as well as how these accounts are differed under different forms and types of business. Produce the final accounts for a sole trader business (Software Programming Company) from task 1 including profit and loss account, owners’ equity statement, and balance sheet for the Period ended July 31st. using the trial balance that you have produced in problem 2/ task1 2) Make the adjustments entries for the following transactions before preparing the final accounts for LLC company: On the 20th of October 2019, the business purchased supplies for 8000 cash. On 31st of December, 2019 the business found out that the supplies still on hand were 4000 only. The business has a Equipment with book value of 17000, with annual depreciation rate of 10%. On the 1st of July the business purchased a…arrow_forwardErica Gray, CPA, is a sole practitioner. She has been practicing as an auditor for 10 years. Recently a long-standing audit client asked Gray to design and implement an integrated computer-based accounting information system. The fees associated with this additional engagement with the client are very attractive. However, Gray wonders if she can remain objective on subsequent audits in her evaluation of the client’s accounting system and its records if she was responsible for its design and implementation. Gray knows that professional auditing standards require her to remain independent in fact and appearance from her auditing clients. Required 1. What do you believe auditing standards are mainly concerned with when they require independence in fact? In appearance? 2. Why is it important that auditors remain independent of their clients? 3. Do you think Gray can accept this engagement and remain independent? Justify your response.arrow_forward

- Erica Gray, CPA, is a sole practitioner. She has been practicing as an auditor for 10 years. Recently a long-standing audit client asked Gray to design and implement an integrated computer-based accounting information system. The fees associated with this additional engagement with the client are very attractive. However, Gray wonders if she can remain objective on subsequent audits in her evaluation of the client’s accounting system and its records if she was responsible for its design and implementation. Gray knows that professional auditing standards require her to remain independent in fact and appearance from her auditing clients. Submit a substantive posting of at least 250 words that answers the questions Question 1: What do you believe auditing standards are mainly concerned with when they require independence in fact? In appearance? Question 2: Why is it important that auditors remain independent of their clients? Question 3: Do you think Gray can accept this engagement and…arrow_forwardAdjusting entries must be done to ensure that the adjusted trial balance: Select one: shows a more accurate picture of the business's activities. is before the income statement and after the adjustments column. is accurate in case of an audit. is different from the trial balance.arrow_forwardMabel, an accountant, discovers that an analyzed transaction has not been entered in to the books.mnat what step in the accounting cycle is she most likely to make the discoveryarrow_forward

- Your friend has come to you for advice on how to record a transaction in their accounting records for their proprietorship. 1) Use what you have learned in Chapter 4 to explain what is done at each step up to preparing the trial balance. 2) How would you go about detecting the error(s) if a trial balance resulted in total debits of $23,500 and total credits of $22,700arrow_forwardHoney Crunch Limited started business in 2018. It is now 2021 and the Board of Directors of Honey Crunch Limited hired Aegis Solutions to recommend how each of the following types of accounting changes or errors should be dealt with. As an audit assistant for Aegis, provide Honey Crunch with this information. For each issue write a note for the audit file (3-5 sentences) identify the type of accounting change or error, the appropriate accounting treatment, include amounts where applicable and how net income would be impacted if the issue needs correcting. 1. In early 2019, Honey Crunch changed its estimate from 5% to 4% of receivables on the amount of bad debt expense to be charged to operations. Bad debt expense for 2018, if a 4% rate had been used, would have been $8,000. The company adjusted Net Income in 2018 to reflect the change. 2. The company changed its method of inventory…arrow_forwardDescription and Instructions Suppose you are a part of a group of students from a prominent university and were sent out as a team to work with a leading merchandizing company as a part of a work experience program. The team having been introduced to the general manger was told that the Accountant who normally prepares the financial statements has suddenly resigned and there is no one available to prepare the company’s financial statements which are now due. As aspiring university students, you and your group members have expressed an interest in taking on the task. As a group, you are required to collaborate and analyse the problem at hand then apply the accrual basis of accounting in the preparation of the company’s financial statements. The problem to be resolved: The following trial balance was extracted from the books of Scholes Farm Ltd December 31, the end of the company’s financial year. The company is owned by Paul Scholes and is in the business of buying and farming…arrow_forward

- your line manager wants to assess your understanding and ability to prepare and produce the appropriate final accounts such as profit and loss account, owners’ equity statement, and balance sheet as well as how these accounts are differed under different forms and types of business 1 Produce the final accounts for a sole trader business (Software Programming Company) from task 1 including profit and loss account, owners’ equity statement, and balance sheet for the Period ended July 31st. using the trial balance that you have produced in problem 2/ task1. 2 Make the adjustments entries for the following transactions before preparing the final accounts for LLC company: On the 20th of October 2019, the business purchased supplies for 8000 cash. On 31st of December, 2019 the business found out that the supplies still on hand were 4000 only. The business has a Equipment with book value of 17000, with annual depreciation rate of 10%. On the 1st of July the business purchased a one-year…arrow_forwardIn your role as an accountant, conduct a comprehensive evaluation of the relationship between the journal, ledger, and trial balance. Furthermore, elaborate on the methods you would employ to identify errors within the trial balance as well as the subsequent process for rectifying those errors. Use relevant examples to substantiate your arguments.arrow_forward

Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning

Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning