Videos

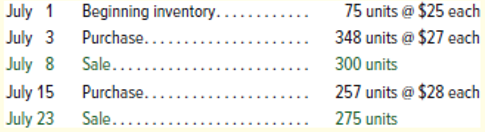

Use the following information from Marvel Company for the month of July to answer questions 1 through 4.

1. Perpetual: Assume that Marvel uses a perpetual FIFO inventory system. What is the dollar value of its ending inventory?

- $2,940

- $2,685

- $2,625

- $2,852

- $2,705

Perpetual Inventory System:

The perpetual inventory system is that system of accounting the inventory in which the inventory is verified physically. This is done so that the lost and misplaced items are also recorded. The entries are made through merchandise accounts.

The dollar value of the ending inventory using FIFO.

Explanation of Solution

Option a, $2,940 is correct.

Given,

The company uses perpetual FIFO inventory system.

Calculation of the value of ending inventory:

| Date | Goods purchased | Cost of goods sold | Inventory balance |

| July 1 | |||

| July 3 | 348 units | ||

| July 8 | |||

| July 15 | 257 units | ||

| July 23 | |||

| $15,527 | $2,940 |

The value of the ending inventory is $2,940.

Thus, option a is correct.

Want to see more full solutions like this?

Chapter 5 Solutions

Gen Combo Ll Financial Accounting Fundamentals; Connect Access Card

- Carla Company uses the perpetual inventory system. The following information is available for January of the current year when Carla sold 1,600 units of inventory on January 14. Using the FIFO method, calculate Carlas cost of goods sold for January and its January 31 inventory.arrow_forwardJessie Stores uses the periodic system of calculating inventory. The following information is available for December of the current year when Jessie sold 500 units of inventory. Using the FIFO method, calculate Jessies inventory on December 31 and its cost of goods sold for December.arrow_forwardJessie Stores uses the periodic system of calculating inventory. The following information is available for December of the current year when Jessie sold 500 units of inventory. Using the FIFO method, calculate Jessies inventory on December 31 and its cost of goods sold for December. RE7-11 Using the information from RE7-10, calculate Jessie Storess inventory on December 31 and its cost of goods sold for December using the LIFO method.arrow_forward

- Beginning inventory, purchases, and sales for Item Zebra 9x are as follows: Assuming a perpetual inventory system and using the last-in, first-out (LIFO) method, determine (a) the cost of merchandise sold on April 27 and (b) the inventory on April 30.arrow_forwardPERPETUAL: LIFO AND MOVING-AVERAGE Kelley Company began business on January 1, 20-1. Purchases and sales during the month of January follow. REQUIRED Calculate the total amount to be assigned to cost of goods sold for January and the ending inventory on January 31, under each of the following methods: 1. Perpetual LIFO inventory method. 2. Perpetual moving-average inventory method.arrow_forwardFIFO perpetual inventory The beginning inventory at Dunne Co. and data on purchases and sales for a three-month period ending June 30 are as follows: Instructions 1. Record the inventory, purchases, and cost of goods sold data in a perpetual inventory record similar to the one illustrated in Exhibit 3, using the first-in, first-out method. 2. Determine the total sales and the total cost of goods sold for the period. Journalize the entries in the sales and cost of goods sold accounts. Assume that all sales were on account. 3. Determine the gross profit from sales for the period. 4. Determine the ending inventory cost on June 30. 5. Based upon the preceding data, would you expect the ending inventory using the last-in, first-out method to be higher or lower?arrow_forward

- Beginning inventory, purchases, and sales for Item ProX2 are as follows: Assuming a perpetual inventory system and using the first-in, first-out (FIFO) method, determine (a) the cost of merchandise sold on January 25 and (b) the inventory on January 31.arrow_forwardAlternative Inventory Methods Park Companys perpetual inventory records indicate the following transactions in the month of June: Required: 1. Compute the cost of goods sold for June and the inventory at the end of June using each of the following cost flow assumptions: a. FIFO b. LIFO c. Average cost (Round unit costs to 3 decimal places and other amounts to the nearest dollar.) 2. Next Level Why are the cost of goods sold and ending inventory amounts different for each of the three methods? What do these amounts tell us about the purchase price of inventory during the year? 3. Next Level Which method produces the most realistic amount for net income? For inventory? Explain your answer. 4. Next Level If Park uses IFRS, which of the previous alternatives would be acceptable and why?arrow_forwardBeginning inventory, purchases, and sales for Item Foxtrot are as follows: Assuming a perpetual inventory system and using the last-in, first-out (LIFO) method, determine (a) the cost of merchandise sold on March 27 and (b) the inventory on March 31.arrow_forward

- LIFO perpetual inventory The beginning inventory for Dunne Co. and data on purchases and sales for a three-month period are shown in Problem 6-1B. Instructions 1. Record the inventory, purchases, and cost of goods sold data in a perpetual inventory record similar to the one illustrated in Exhibit 4, using the last-in, first-out method. 2. Determine the total sales, the total cost of goods sold, and the gross profit from sales for the period. 3. Determine the ending inventory cost on June 30.arrow_forwardBasga Company uses the periodic inventory system. Beginning inventory amounted to 241,072. A physical count reveals that the latest inventory amount is 256,339. Record the adjusting entries, using T accounts.arrow_forwardCalculate the cost of goods sold dollar value for A66 Company for the month, considering the following transactions under three different cost allocation methods and using perpetual inventory updating. Provide calculations for last-in, first-out (LIFO).arrow_forward

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub

College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning, Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning