Concept explainers

Videos

The following

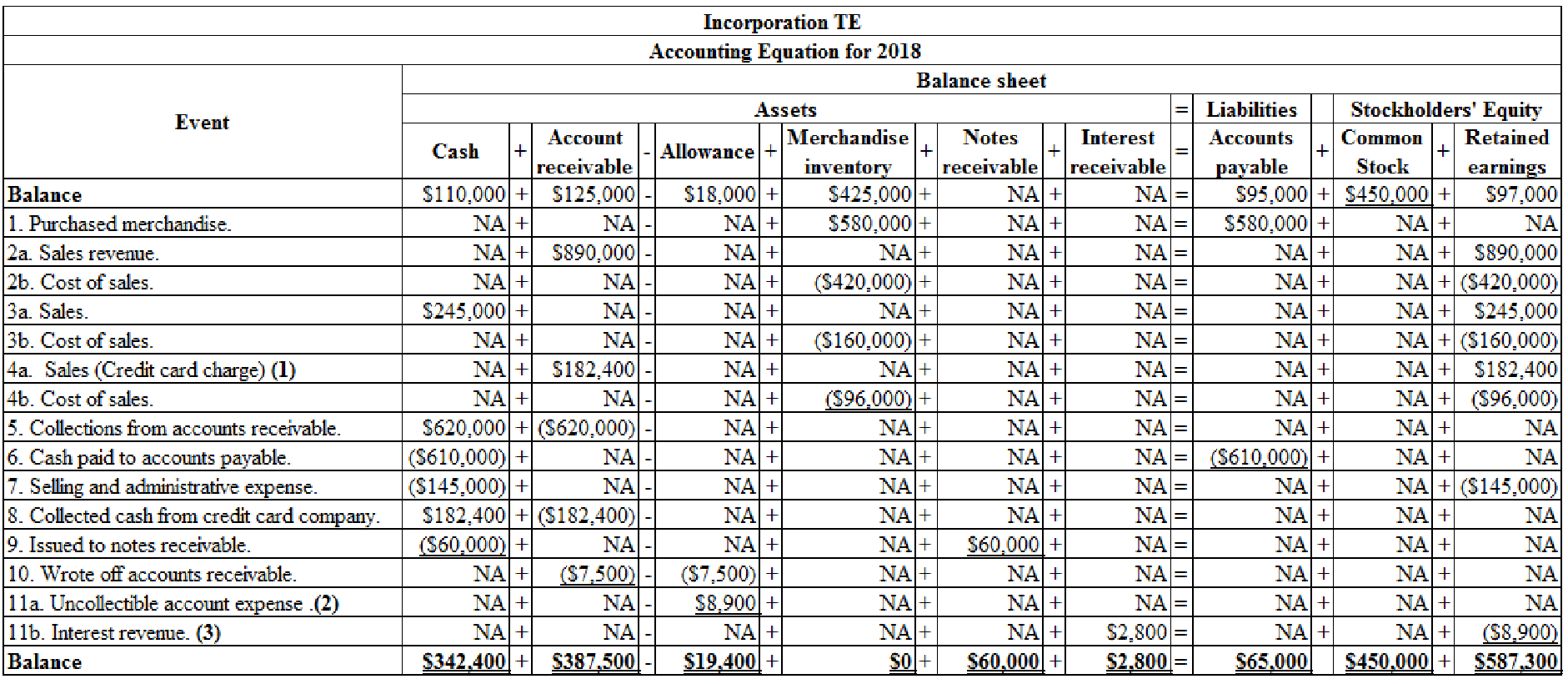

Tile, Etc. had the following transactions in 2018:

- 1. Purchased merchandise on account for $580,000.

- 2. Sold merchandise that cost $420,000 for $890,000 on account.

- 3. Sold for $245,000 cash merchandise that had cost $160,000.

- 4. Sold merchandise for $190,000 to credit card customers. The merchandise had cost $96,000. The credit card company charges a 4 percent fee.

- 5. Collected $620,000 cash from

accounts receivable . - 6. Paid $610,000 cash on accounts payable.

- 7. Paid $145,000 cash for selling and administrative expenses.

- 8. Collected cash for the full amount due from the credit card company (see item 4).

- 9. Loaned $60,000 to J. Parks. The note had an 8 percent interest rate and a one-year term to maturity.

- 10. Wrote off $7,500 of accounts as uncollectible.

- 11. Made the following

adjusting entries :- (a) Recorded uncollectible accounts expense estimated at 1 percent of sales on account.

- (b) Recorded seven months of accrued interest on the note at December 31, 2018 (see item 9).

Required

- a. Organize the transaction data in accounts under an

accounting equation. - b. Prepare an income statement, a statement of changes in stockholders’ equity, a

balance sheet , and a statement of cash flows for 2018.

a.

Organize the transaction data in accounts under an accounting equation.

Explanation of Solution

Percentage of sales method: Credit sales are recorded by debiting (increasing) accounts receivable account. The bad debts is a loss incurred out of credit sales, hence uncollectible accounts can be estimated as a percentage of credit sales or total sales.

It is a method of estimating the bad debts (expected loss on extending credit), by multiplying the expected percentage of uncollectible with the total amount of net credit sale (or total sales) for a specific period. Under percentage of sales method, estimated bad debts would be treated as a bad debt expense of the particular period.

Horizontal statements model: The model that represents all the financial statements, balance sheet, income statement, and statement of cash flows in one table in a horizontal form, is referred to as, horizontal statements model.

Organize the transaction data in accounts under an accounting equation.

Table (1)

Working note:

(1) Calculate the amount of credit card sales made to customers:

The merchandise sold to credit card customers for $190,000 and the company charges a fee of 4% on sales. So, the credit card expense is

(2) Calculate the amount for uncollectible accounts expense:

Calculate the amount of interest receivable:

Given: The loan amount is $60,000 and the rate of interest is 8%. So the total interest income is calculated as follows:

b.

Prepare an income statement, statement of changes in stockholders’ equity, a balance sheet, and a statement of cash flows for 2018.

Explanation of Solution

Income statement: The financial statement which reports revenues and expenses from business operations and the result of those operations as net income or net loss for a particular time period is referred to as income statement.

Prepare the income statement.

| Incorporation TE | ||

| Income statement | ||

| For the year ended December 31, 2018 | ||

| Particulars | Amount | Amount |

| Revenue | ||

| Sales revenue | $1,325,000 | |

| Less: Cost of goods sold | $676,000 | |

| Gross profit | $649,000 | |

| Less: Operating Expenses | ||

| Credit card expenses | $7,600 | |

| Selling and administrative expenses | $145,000 | |

| Uncollectible accounts expense | $8,900 | |

| Total operating income | ($161,500) | |

| Operating income | $487,500 | |

| Add: Non-operating items | ||

| Interest revenue | $2,800 | |

| Net income | $490,300 | |

Table (2)

Statement of changes in the stockholders’ equity: This statement reflects whether the components of stockholders’ equity have increased or decreased during the period.

Prepare the statement of changes in stockholders’ equity.

| Incorporation TE | ||

| Statement of changes in stockholders’ equity | ||

| For the year ended December 31, 2018 | ||

| Particulars | Amount | Amount |

| Beginning common stock | $450,000 | |

| Add: Common stocks issued | $0 | |

| Ending common stock | $450,000 | |

| Beginning retained earnings | $97,000 | |

| Add: Net income | $490,300 | |

| Less: Dividends | ($0) | |

| Ending retained earnings | $587,300 | |

| Total stockholders’ equity | $1,037,300 | |

Table (3)

Balance sheet: Balance Sheet is one of the financial statements that summarize the assets, the liabilities, and the Shareholder’s equity of a company at a given date. It is also known as the statement of financial status of the business.

Prepare the balance sheet.

| Incorporation TE | ||

| Balance sheet | ||

| As of December 31, 2018 | ||

| Particulars | Amount | Amount |

| Assets | ||

| Cash | $342,400 | |

| Accounts receivable | $387,500 | |

| Less: Allowance for doubtful accounts | $19,400 | $368,100 |

| Merchandise inventory | $329,000 | |

| Interest receivable | $2,800 | |

| Notes receivable | $60,000 | |

| Total assets | $1,102,300 | |

| Liabilities | ||

| Accounts payable | $65,000 | |

| Total liabilities | $65,000 | |

| Stockholders’ equity | ||

| Common stock | $450,000 | |

| Retained earnings | $587,300 | |

| Total stockholders' equity | $1,037,300 | |

| Total liabilities and stockholders' equity | $1,102,300 | |

Table (4)

Statement of cash flows: This statement reports all the cash transactions involves for inflow and outflow of cash, and the result of these transactions is reported as an ending balance of cash at the end of reported period.

Prepare the statement of cash flows.

| Incorporation TE | ||

| Statement of cash flow | ||

| For the year December 31, 2018 | ||

| Particulars | Amount | Amount |

| Cash flow from operating activities: | ||

| Inflow from customers (4) | $1,047,400 | |

| Outflow for inventory | ($610,000) | |

| Outflow for expenses | ($145,000) | |

| Net cash flow from operating activities | $292,400 | |

| Cash flow from investing activities | ||

| Outflow for notes receivable | ($60,000) | |

| Net cash flow from investing activities | ($60,000) | |

| Cash flow from financing activities | $0 | |

| Net change in cash | $232,400 | |

| Add: Beginning cash balance | $110,000 | |

| Ending cash balance | $342,400 | |

Table (5)

Working note:

(4) Calculate the amount of inflow from customers.

Want to see more full solutions like this?

Chapter 5 Solutions

Connect Access Card for Survey of Accounting

- The accounts and their balances in the ledger of Markeys Mountain Shop as of December 31, the end of its fiscal year, are as follows: Data for the adjustments are as follows. Assume that Markeys Mountain Shop uses the perpetual inventory system. a. Merchandise Inventory at December 31, 140,357. b. Store supplies inventory (on hand) at December 31, 540. c. Depreciation of building, 3,400. d. Depreciation of store equipment, 3,800. e. Salaries accrued at December 31, 1,250. f. Insurance expired during the year, 1,480. Required 1. Complete the work sheet after entering the account names and balances onto the work sheet. Ignore this step if using CLGL. 2. Journalize the adjusting entries. If using manual working papers, record adjusting entries on journal page 63.arrow_forwardOn January 1, Incredible Infants sold goods to Babies Inc. for $1,540, terms 30 days, and received payment on January 18. Which journal would the company use to record this transaction on the 18th? A. sales journal B. purchases journal C. cash receipts journal D. cash disbursements journal E. general journalarrow_forwardA firm is preparing to make adjusting entries at the end of the accounting period. The balance of the merchandise inventory account is 200,000. If the firm is using the periodic inventory system, what does this balance represent?arrow_forward

- The trial balance of Hadden Company as of December 31, the end of its current fiscal year, is as follows: Here are the data for the adjustments. ab.Merchandise Inventory at December 31, 64,742.80. c.Store supplies inventory (on hand), 420.20. d.Insurance expired, 738. e.Salaries accrued, 684.50. f.Depreciation of store equipment, 3,620. Required Complete the work sheet after entering the account names and balances onto the work sheet.arrow_forwardA firm is preparing to make adjusting entries at the end of the accounting period. The balance of the merchandise inventory account is 100,000. If the firm is using the perpetual inventory system, what does this balance represent?arrow_forwardPost the following November transactions to T-accounts for Accounts Payable and Inventory, indicating the ending balance (assume no beginning balances in these accounts). A. purchased merchandise inventory on account, $22,000 B. paid vendors for part of inventory purchased earlier in month, $14,000 C. purchased merchandise inventory for cash, $6,500arrow_forward

- On September 30, 2013, the general ledger of Leons Golf Shop, which uses the calendar year as its accounting period, showed the following year-to-date account balances: The merchandise inventory account had a 48,000 balance on January 1, 2013. The historical gross profit percentage is 40%. Leon prepares quarterly financial statements and takes physical inventory once a yearat the end of the accounting period. In order to prepare the financial statements for the third quarter, the store needs to have an estimate of ending inventory. You have been asked to use the gross profit method to estimate the ending inventory. Review the worksheet called GP. Study it carefully because it may have a solution format somewhat different from the one shown in your textbook.arrow_forwardThe balances of the ledger accounts of Beldren Home Center as of December 31, the end of its fiscal year, are as follows: Data for the adjustments are as follows: ab. Merchandise Inventory at December 31, 102,765. c. Wages accrued at December 31, 1,834. d. Supplies inventory (on hand) at December 31, 645. e. Depreciation of store equipment, 5,782. f. Depreciation of office equipment, 1,791. g. Insurance expired during the year, 845. h. Rent earned, 2,500. Required 1. Complete the work sheet after entering the account names and balances onto the work sheet. Ignore this step if using CLGL. 2. Journalize the adjusting entries. If using manual working papers, record adjusting entries on journal page 16.arrow_forwardPrepare journal entries to record the following transactions. Create a T-account for Accounts Payable, post any entries that affect the account, and calculate the ending balance for the account. Assume an Accounts Payable beginning balance of $7,500. A. May 12, purchased merchandise inventory on account. $9,200 B. June 10, paid creditor for part of previous months purchase, $11,350arrow_forward

- On December 31, the end of the year, the accountant for Fireside Magazine was called away suddenly because of an emergency. However, before leaving, the accountant jotted down a few notes pertaining to the adjustments. Journalize the necessary adjusting entries. Assume that Fireside Magazine uses the periodic inventory system. ab. A physical count of inventory revealed a balance of 199,830. The Merchandise Inventory account shows a balance of 202,839. c. Subscriptions received in advance amounting to 156,200 were recorded as Unearned Subscriptions. At year-end, 103,120 has been earned. d. Depreciation of equipment for the year is 12,300. e. The amount of expired insurance for the year is 1,612. f. The balance of Prepaid Rent is 2,400, representing four months rent. Three months rent has expired. g. Three days salaries will be unpaid at the end of the year; total weekly (five days) salaries are 4,000. h. As of December 31, the balance of the supplies account is 1,800. A physical inventory of the supplies was taken, with an amount of 920 determined to be on hand.arrow_forwardA partial work sheet for McKnight Music Store is presented here. The merchandise inventory at the beginning of the fiscal period was 48,473. W. J. McKnight, the owner, withdrew 40,000 during the year. Required 1. Prepare an income statement. 2. Journalize the closing entries. Check Figure Cost of Goods Sold, 192,521arrow_forwardA partial work sheet for The Fan Shop is presented here. The merchandise inventory at the beginning of the year was 52,300. P. G. Ochoa, the owner, withdrew 30,500 during the year. Required 1. Prepare an income statement. 2. Journalize the closing entries. Check Figure Cost of Goods Sold, 206,120arrow_forward

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub

College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning

Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning