Concept explainers

Videos

Purchases and cash payments journals; accounts payable subsidiary and general ledgers

West Texas Exploration Co. was established on October 15 to provide oil-drilling services. West Texas uses field equipment (rigs and pipe) and field supplies (drill bits and lubricants) in its operations. Transactions related to purchases anti cash payments during the remainder of October are as follows:

| Oct. 16. | Issued Check No. 1 in payment of rent for the remainder of October, $7,000. |

| 16. | Purchased field equipment on account from Petro Services Inc., $32,600. |

| Oct.17. | Purchased field supplies on account from Midland Supply Co., $9,780. |

| 18. | Issued Check No. 2 in payment of field supplies, $4,570, and office supplies, $650. |

| 20. | Purchased office supplies on account from A-One Office Supply Co., $1,320. |

| Post the journals to the accounts payable subsidiary ledger. | |

| 24. | Issued Check No. 3 to Petro Services Inc., in payment of October 16 invoice. |

| 26. | Issued Check No. 4 to Midland Supply Co. in payment of October 17 invoice. |

| 28 | Issued Check No. 5 to purchase land, $240,000. |

| 28 | Purchased office supplies on account from A-One Office Supply Co., $3,670. |

| Post the journals to the accounts payable subsidiary ledger. | |

| 30 | Purchased the following from Petro Services Inc. on account: field supplies, $25,300 and office equipment, $5,500. |

| 30 | Issued Check No. 6 to A-One Office Supply Co. in payment of October 20 invoice. |

| 30 | Purchased field supplies on account from Midland Supply Co., $12,450. |

| 31 | Issued Check No. 7 in payment of salaries, $32,000. |

| 31 | Rented building for one year in exchange for field equipment having a cost of $15,000. |

| Post the journals to the accounts payable subsidiary ledger. | |

Instructions

1 Journalize the transactions for October. Use a purchases journal and a cash payments journal similar to those illustrated in this chapter and a two-column general journal. Set debit columns for Field Supplies, Office Supplies, and Other Accounts in the purchases journal. Refer to the following partial chart of accounts:

| 11. | Cash | 18 | Office Equipment |

| 14. | Field Supplies | 19 | Land |

| 15. | Office Supplies | 21 | Accounts Payable |

| 16. | Prepaid Rent | 61 | Salary Expense |

| 17. | Field Equipment | 71 | Rent Expense |

At the points indicated in the narrative of transactions, post to the following subsidiary accounts in the accounts payable ledger:

A-One Office Supply Co.

Midland Supply Co.

Petro Services Inc.

- 2.

Post the individual entries (Other Accounts columns of the purchases journal and the Cash payments journal; both columns of the general journal) to the appropriate general ledger accounts. - 3. Total each of the columns of the purchases journal and the cash payments journal, and post the appropriate totals to the general ledger. (Because the problem does not include transactions related to cash receipts, the cash account in the ledger will have a credit balance.)

- 4. Sum the balances of the accounts payable creditor balances.

- 5. Why might West Texas consider using a subsidiary ledger for the field equipment?

1.

General Ledger

General ledger refers to the ledger that records all the transactions of the business related to the company’s assets, liabilities, owners’ equities, revenues, and expenses. Each subsidiary ledger is represented in the general ledger by summarizing the account.

Accounts payable control account and subsidiary ledger:

Accounts payable account and subsidiary ledger is the ledger which is used to post the creditors transaction in one particular ledger account. It helps the business to locate the error in the creditor ledger balance. After all transactions of creditor accounts are posted, the balances in the accounts payable subsidiary ledger should be totaled, and compare with the balance in the general ledger of accounts payable. If both the balance does not agree, the error has been located and corrected.

Purchase journal:

Purchase journal refers to the journal that is used to record all purchases on account. In the purchase journal, all purchase transactions are recorded only when the business purchased the goods on account. For example, the business purchased cleaning supplies on account.

Cash payments journal:

Cash payments journal refers to the journal that is used to record all transaction which involves the cash payments. For example, the business paid cash to employees (salary paid to employees).

To Prepare: A single column revenue journal and cash receipt journal, and post the accounts in the accounts payable subsidiary ledger.

Explanation of Solution

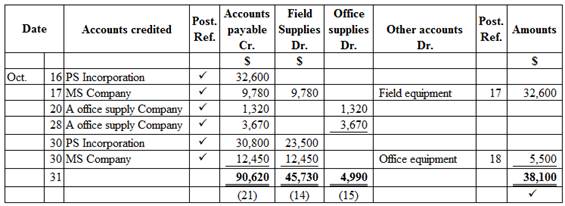

Purchase journal

Purchase journal of Company WTE in the month of October is as follows:

Figure (1)

Cash payment journal

Cash payment journal of Company WTE in the month of October is as follows:

Cash payment journal

| Date | Check No. | Account debited | Post Ref. | Other accounts Dr. | Accounts payable Dr. | Cash Dr. | |

| Oct. | 16 | 1 | Rent expense | 71 | 7,000 | 7,000 | |

| 18 | 2 | Field supplies | 14 | 4,570 | 4,570 | ||

| Office supplies | 15 | 650 | 650 | ||||

| 24 | PS Incorporation | ✓ | 32,600 | 32,600 | |||

| 26 | MS Company | ✓ | 9,780 | 9,780 | |||

| 28 | Land | 240,000 | 240,000 | ||||

| 30 | A Office supply Company | ✓ | 1,320 | 1,320 | |||

| 31 | Salary expense | 61 | 32,000 | 32,000 | |||

| 31 | 284,220 | 43,700 | 327,920 | ||||

| ✓ | (21) | (11) | |||||

Table (1)

Accounts payable subsidiary ledger

| Name: A Office supply Company | ||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) |

Balance ($) | |

| Oct. | 20 | P1 | 1,320 | 1,320 | ||

| 28 | P1 | 3,670 | 4,990 | |||

| 30 | CP1 | 1,320 | 3,670 | |||

Table (2)

| Name: MS Company | ||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) |

Balance ($) | |

| Oct. | 17 | P1 | 9,780 | 9,780 | ||

| 26 | CP1 | 9,780 | - | |||

| 30 | P1 | 12,450 | 12,450 | |||

Table (3)

| Name: PS Incorporation | ||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) |

Balance ($) | |

| Oct. | 16 | P1 | 32,600 | 32,600 | ||

| 24 | CP1 | 32,600 | - | |||

| 30 | P1 | 30,800 | 30,800 | |||

Table (4)

2. and 3.

To post: The individual entries to the appropriate general ledger accounts.

Explanation of Solution

Prepare the general ledger for given accounts as follows:

| Account: Cash Account no. 11 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| Oct. | 31 | CP1 | 327,920 | 327,920 | |||

Table (5)

| Account: Field supplies Account no. 14 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| Oct. | 18 | CP1 | 4,570 | 4,570 | |||

| 31 | P1 | 47,530 | 52,100 | ||||

Table (6)

| Account: Office supplies Account no. 15 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| Oct. | 18 | CP1 | 650 | 650 | |||

| 31 | P1 | 4,990 | 5,460 | ||||

Table (7)

| Account: Prepaid rent Account no. 16 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| Oct. | 31 | J1 | 15,000 | 15,000 | |||

Table (8)

| Account: Field equipment Account no. 17 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| Oct. | 16 | P1 | 32,600 | 32,600 | |||

| 31 | J1 | 15,000 | 17,600 | ||||

Table (9)

| Account: Office equipment Account no. 18 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 31 | P1 | 5,500 | 5,500 | ||||

Table (10)

| Account: Land Account no. 19 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| Oct. | 23 | CP1 | 240,000 | 240,000 | |||

Table (11)

| Account: Accounts payable Account no. 21 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| Oct. | 31 | P1 | 90,620 | 90,620 | |||

| 31 | CP1 | 43,700 | 46,920 | ||||

Table (12)

| Account: Salary expense Account no. 61 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| Oct. | 31 | CP1 | 32,000 | 32,000 | |||

Table (13)

| Account: Rent expense Account no. 71 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| Oct. | 16 | CP1 | 7,000 | 7,000 | |||

Table (14)

| Journal Page 01 | |||||

| Date | Description | Post. Ref | Debit ($) | Credit ($) | |

| Oct. | 31 | Prepaid rent | 16 | 15,000 | |

| Field equipment | 17 | 15,000 | |||

| (To record leasing of field equipment) | |||||

Table (15)

4.

To prepare: The accounts payable creditor balances.

Explanation of Solution

Accounts payable creditor balance

Accounts payable creditor balance is as follows:

| Company WTE | |

| Accounts payable creditor balances | |

| October 31 | |

| Amount ($) | |

| A Office supply Company | 3,670 |

| MS Company | 12,450 |

| PS Incorporation | 30,800 |

| Total accounts receivable | 46,920 |

Table (16)

Accounts payable controlling account

Ending balance of accounts payable controlling account is as follows:

| Company WTE | |

| Accounts payable (Controlling account) | |

| October 31 | |

| Amount ($) | |

| Opening balance | 0 |

| Add: | |

| Total credits (from purchase journal) | 90,620 |

| 90,620 | |

| Less: | |

| Total debits (from cash payment journal) | (43,700) |

| Total accounts payable | 46,920 |

Table (17)

Explanation:

In this case, accounts payable subsidiary ledger is used to identify, and locate the error by way of cross-checking the creditor balance and accounts payable controlling account. From the above calculation, we can understand that both balances of accounts payable is agree, hence there is no error in the recording and posing of transactions.

5.

To discuss: The reason for using subsidiary ledger for the field equipment.

Explanation of Solution

A subsidiary ledger for the field equipment helps the company to track the cost of each piece of equipment, location, useful life, and other necessary data. This information is used for safeguarding the equipment and determining depreciation of equipment.

Want to see more full solutions like this?

Chapter 5 Solutions

Accounting, Chapters 1-13

- Analyzing the Accounts The controller for Summit Sales Inc. provides the following information on transactions that occurred during the year: a. Purchased supplies on credit, $18,600 b. Paid $14,800 cash toward the purchase in Transaction a c. Provided services to customers on credit1 $46,925 d. Collected $39,650 cash from accounts receivable e. Recorded depreciation expense, $8,175 f. Employee salaries accrued, $15,650 g. Paid $15,650 cash to employees for salaries earned h. Accrued interest expense on long-term debt, $1,950 i. Paid a total of $25,000 on long-term debt, which includes $1.950 interest from Transaction h j. Paid $2,220 cash for l years insurance coverage in advance k. Recognized insurance expense, $1,340, that was paid in a previous period l. Sold equipment with a book value of $7,500 for $7,500 cash m. Declared cash dividend, $12,000 n. Paid cash dividend declared in Transaction m o. Purchased new equipment for $28,300 cash. p. Issued common stock for $60,000 cash q. Used $10,700 of supplies to produce revenues Summit Sales uses the indirect method to prepare its statement of cash flows. Required: 1. Construct a table similar to the one shown at the top of the next page. Analyze each transaction and indicate its effect on the fundamental accounting equation. If the transaction increases a financial statement element, write the amount of the increase preceded by a plus sign (+) in the appropriate column. If the transaction decreases a financial statement element, write the amount of the decrease preceded by a minus sign (-) in the appropriate column. 2. Indicate whether each transaction results in a cash inflow or a cash outflow in the Effect on Cash Flows column. If the transaction has no effect on cash flow, then indicate this by placing none in the Effect on Cash Flows column. 3. For each transaction that affected cash flows, indicate whether the cash flow would be classified as a cash flow from operating activities, cash flow from investing activities, or cash flow from financing activities. If there is no effect on cash flows, indicate this as a non-cash activity.arrow_forwardTransactions related to revenue and cash receipts completed by Sterling Engineering Services during the period June 230 are as follows: Instructions 1. Insert the following balances in the general ledger as of June 1: 2. Insert the following balances in the accounts receivable subsidiary ledger as of June 1: 3. Prepare a single-column revenue journal (p. 40) and a cash receipts journal (p. 36). Use the following column headings for the cash receipts journal: Fees Earned Cr., Accounts Receivable Cr., and Cash Dr. The Fees Earned column is used to record cash fees. Insert a check mark () in the Post. Ref. column when recording cash fees. 4. Using the two special journals and the two-column general journal (p. 1), journalize the transactions for June. Post to the accounts receivable subsidiary ledger and insert the balances at the points indicated in the narrative of transactions. Determine the balance in the customers account before recording a cash receipt. 5. Total each of the columns of the special journals and post the individual entries and totals to the general ledger. Insert account balances after the last posting. 6. Determine that the sum of the customer accounts agrees with the accounts receivable controlling account in the general ledger. 7. Why would an automated system omit postings to a control account as performed in step 5 for Accounts Receivable?arrow_forwardTransactions related to revenue and cash receipts completed by Crowne Business Services Co. during the period April 230 are as follows: Post revenue and collections to the accounts receivable subsidiary ledger. Instructions 1. Insert the following balances in the general ledger as of April 1: 2. Insert the following balances in the accounts receivable subsidiary ledger as of April 1: 3. Prepare a single-column revenue journal (p. 40) and a cash receipts journal (p. 36). Use the following column headings for the cash receipts journal: Fees Earned Cr., Accounts Receivable Cr., and Cash Dr. The Fees Earned column is used to record cash fees. Insert a check mark () in the Post. Ref. column when recording cash fees. 4. Using the two special journals and the two-column general journal (p. 1), journalize the transactions for April. Post to the accounts receivable subsidiary ledger, and insert the balances at the points indicated in the narrative of transactions. Determine the balance in the customers account before recording a cash receipt. 5. Total each of the columns of the special journals and post the individual entries and totals to the general ledger. Insert account balances after the last posting. 6. Determine that the sum of the customer balances agrees with the accounts receivable controlling account in the general ledger. 7. Why would an automated system omit postings to a controlling account as performed in step 5 for Accounts Receivable?arrow_forward

- Revenue and Cash Receipts Journals Lasting Summer Inc. has $2,360 in the October 1 balance of the accounts receivable account consisting of $1,090 from Champion Co. and $1,270 from Wayfarer Co. Transactions related to revenue and cash receipts completed by Lasting Summer Inc. during the month of October 20Y5 are as follows: Oct. 3. Issued Invoice No. 622 for services provided to Palace Corp., $2,480. 5. Received cash from Champion Co., on account, for $1,090. 8. Issued Invoice No. 623 for services provided to Sunny Style Inc., $4,270. 12. Received cash from Wayfarer Co., on account, for $1,270. 18. Issued Invoice No. 624 for services provided to Amex Services Inc., $3,000. 23. Received cash from Palace Corp. for Invoice No. 622 of October 3. 28. Issued Invoice No. 625 to Wayfarer Co., on account, for $2,530. 30. Received cash from Rogers Co. for services provided, $90. a. Prepare a single-column revenue journal to record these transactions.…arrow_forwardRevenue and cash receipts journals; accounts receivable subsidiary and general ledgers Transactions related to revenue and cash receipts completed by Crowne Business Services Co. during the period April 2–30 are as follows: Apr. 2. Issued Invoice No. 793 to Ohr Co., $7,120. Apr. 5. Received cash from Mendez Co. for the balance owed on its account. Apr. 6. Issued Invoice No. 794 to Pinecrest Co., $2,570. Apr. 13. Issued Invoice No. 795 to Shilo Co., $3,820. Post revenue and collections to the accounts receivable subsidiary ledger. Apr. 15. Received cash from Pinecrest Co. for the balance owed on April 1. Apr. 16. Issued Invoice No. 796 to Pinecrest Co., $7,980.Post revenue and collections to the accounts receivable subsidiary ledger. Apr. 19. Received cash from Ohr Co. for the balance due on invoice of April 2. Apr. 20. Received cash from Pinecrest Co. for balance due on invoice of April 6. Apr. 22. Issued Invoice No. 797 to Mendez Co.,…arrow_forwardRevenue and Cash Receipts Journals Lasting Summer Inc. has $1,840 in the October 1 balance of the accounts receivable account consisting of $850 from Champion Co. and $990 from Wayfarer Co. Transactions related to revenue and cash receipts completed by Lasting Summer Inc. during the month of October 20Y5 are as follows: Oct. 3. Issued Invoice No. 622 for services provided to Palace Corp., $1,930. 5. Received cash from Champion Co., on account, for $850. 8. Issued Invoice No. 623 for services provided to Sunny Style Inc., $3,330. 12. Received cash from Wayfarer Co., on account, for $990. 18. Issued Invoice No. 624 for services provided to Amex Services Inc., $2,340. 23. Received cash from Palace Corp. for Invoice No. 622 of October 3. 28. Issued Invoice No. 625 to Wayfarer Co., on account, for $1,970. 30. Received cash from Rogers Co. for services provided, $70. a. Prepare a single-column revenue journal to record these transactions. Enter…arrow_forward

- Transactions related to revenue and cash receipts completed by Crowne Business ServicesCo. during the period April 2–30 are as follows:Apr. 2. Issued Invoice No. 793 to Ohr Co., $4,680.5. Received cash from Mendez Co. for the balance owed on its account.6. Issued Invoice No. 794 to Pinecrest Co., $1,990.13. Issued Invoice No. 795 to Shilo Co., $3,450.Post revenue and collections to the accounts receivable subsidiary ledger.15. Received cash from Pinecrest Co. for the balance owed on April 1.16. Issued Invoice No. 796 to Pinecrest Co., $5,500.Post revenue and collections to the accounts receivable subsidiary ledger.19. Received cash from Ohr Co. for the balance due on invoice of April 2.20. Received cash from Pinecrest Co. for balance due on invoice of April 6.22. Issued Invoice No. 797 to Mendez Co., $7,470.25. Received $3,200 note receivable in partial settlement of the balance due on theShilo Co. account. Apr. 30. Received cash from fees earned, $12,890.Post revenue and collections…arrow_forwardThe transactions completed by Franklin Company during January, its first month of operations, are listed below. Assume that Franklin Company uses the following journals: cash payments (CP), purchases (P), and general (G). Assume that it uses accounts receivable and accounts payable subsidiary ledgers as well as a general ledger. Indicate by letters which journal would be used for each transaction and whether or not the entry requires a posting to a subsidiary ledger. Clear All P, subsidiary posting G, no subsidiary posting CP, no subsidiary posting CP, subsidiary posting Purchased supplies on account Purchased a computer for cash Recorded the adjustment for supplies used during the month Paid for the equipment purchased on accountarrow_forwardPurchases and Cash Payments Journals Transactions related to purchases and cash payments completed by Wisk Away Cleaning Services Inc. during the month of May 20Y5 are as follows: May 1. Issued Check No. 57 to Bio Safe Supplies Inc. in payment of account, $345. May 3. Purchased cleaning supplies on account from Brite N’ Shine Products Inc., $200. May 8. Issued Check No. 58 to purchase equipment from Carson Equipment Sales, $2,860. May 12. Purchased cleaning supplies on account from Porter Products Inc., $360. May 15. Issued Check No. 59 to Bowman Electrical Service in payment of account, $145. May 18. Purchased supplies on account from Bio Safe Supplies Inc., $240. May 20. Purchased electrical repair services from Bowman Electrical Service on account, $110. May 26. Issued Check No. 60 to Brite N’ Shine Products Inc. in payment of May 3 invoice. May 31. Issued Check No. 61 in payment of salaries, $5,600. Wisk Away Cleaning Services Inc. uses the…arrow_forward

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage

Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning