Videos

Suppose that your

a. Use the midpoint method to calculate your

b. Calculate your income elasticity of demand as your income increases from $20,000 to $24,000 if (i) the price is $12 and (ii) the price is $16.

Subpart (a):

Price elasticity of demand.

Explanation of Solution

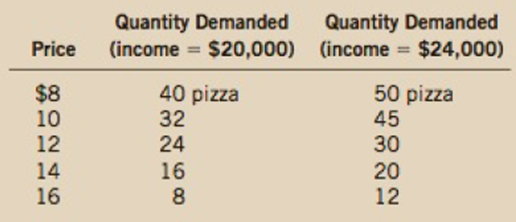

- (i) If the income is $20,000, then the price of pizza rises from $8 to $10, and the quantity demanded decreases from 40 to 32. By midpoint method, the price elasticity of demand is calculated as follows:

The price elasticity of demand for pizza is -1.

- (ii) If the income is $24,000, then the price of pizza rises from $8 to $10, and the quantity demanded decreases from 50 to 45. By midpoint method, the price elasticity of demand is calculated as follows:

The price elasticity of demand for pizza is -0.5.

Concept Introduction:

Price elasticity of demand: Price elasticity of demand refers to the percentage change in the demand for goods and services due to change occurred in the price level.

Subpart (b):

Income elasticity of demand.

Explanation of Solution

- (i) If the price is $12 and an income increases from $20,000 to $24,000, then the quantity demanded increases from 24 to 30. By midpoint method, the income elasticity of demand is calculated as follows:

The income elasticity of demand for pizza is 1.22.

- (ii) If the price is $12 and an income increases from $20,000 to $24,000, then the quantity demanded increases from 24 to 30. By midpoint method, the income elasticity of demand is calculated as follows:

The income elasticity of demand for pizza is 2.22.

Concept Introduction:

Income elasticity of demand: It measures how much quantity demanded of a good responds to the change in consumers’ income.

Want to see more full solutions like this?

Chapter 5 Solutions

Bundle: Essentials of Economics, Loose-leaf Version, 8th + Aplia, 1 term Printed Access Card

- (Other Elasticity Measures) Complete each of the following sentences: a. The income elasticity of demand measures, for a given price, the __________ in quantity demanded divided by the __________ income from which it resulted. b. If a decrease in the price of one good causes a decrease in demand for another good, the two goods are __________. c. If the value of the cross-price elasticity of demand between two goods is approximately zero, they are considered __________.arrow_forwardUsing the following equation for the demand for a good or service, calculate the price elasticity of demand (using the point form), cross-price elasticity with good x and income elasticity. Q=82P+0.10I+Px Q is quantity demanded, P is the product price. P1 is the price of a related good, and I is income. Assume that P= $10, I = 100, and Px = 20.arrow_forwardEconomists define normal goods as having a positive income elasticity. We can divide normal goods into two types: Those whose income elasticity is less than one and those whose income elasticity is greater than one. Think about products that would fall into each category. Can you come up with a name for each category?arrow_forward

- Plot the price and quantity data given in the demand schedule of exercise 1. Put price on the vertical axis and quantity on the horizontal axis. Indicate the price elasticity value at each quantity demanded. Explain why the elasticity value gets smaller as you move down the demand curve.arrow_forwardEstimates presented in Exhibit 5 show that Android users have a higher price elasticity of demand for apps in the Google Play Store than do iPhone users in the Apple App Store. Why might Android users tend to be more sensitive to app prices than iPhone users? What categories or types of apps (for example, games/social media) do you think have the highest price elasticities?arrow_forwardMaria has decided always to spend one third of her income on clothing. a. What is her income elasticity of clothing demand? b. What is her price elasticity of clothing demand? c. It Marias tastes change and she decides to spend only one fourth of her income on clothing, how does her demand curve change? What is her income elasticity and price elasticity now?arrow_forward

Essentials of Economics (MindTap Course List)EconomicsISBN:9781337091992Author:N. Gregory MankiwPublisher:Cengage Learning

Essentials of Economics (MindTap Course List)EconomicsISBN:9781337091992Author:N. Gregory MankiwPublisher:Cengage Learning Principles of MicroeconomicsEconomicsISBN:9781305156050Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of MicroeconomicsEconomicsISBN:9781305156050Author:N. Gregory MankiwPublisher:Cengage Learning