PRINCIPLES OF TAXATION F/BUS...(LL)

23rd Edition

ISBN: 9781260433197

Author: Jones

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Concept explainers

Videos

Textbook Question

Chapter 6, Problem 34AP

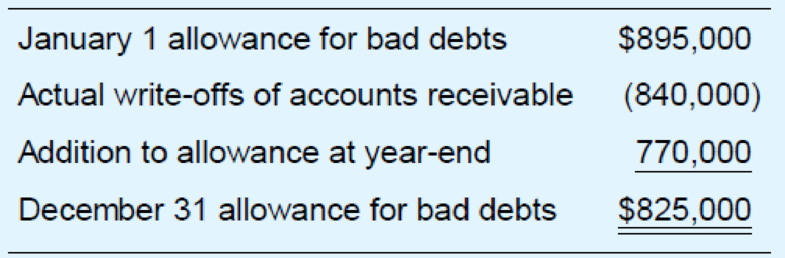

GK Company, a calendar year accrual basis taxpayer, made the following adjustments to its allowance for

- a. Compute GK’s bad debt expense for financial statement purposes.

- b. Compute GK’s tax deduction for bad debts.

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Students have asked these similar questions

Lindemax Inc. reports the following pretax income (loss) for both financial reporting purposes and tax purposes. (Assume the carryback provision is used for a net operating loss.)

The tax rates listed were all enacted by the beginning of 2018.

Instructions

a) Prepare the journal entries for the years 2018-2021 to record income tax expense (benefit) and income tax payable (refundable) and the tax effects of the loss carryback and carryforward, assuming that the end of 2020 it is probable that the benefits of the loss carryforward will be realized in the future.

(Accounting and Classification of Deferred Income Taxes)Part A: This year, Gumowski Company has each of the following items in its income statement.1. Gross profits on installment sales.2. Revenues on long-term construction contracts.3. Estimated costs of product warranty contracts.4. Premiums on officers’ life insurance policies with Gumowski as beneficiary.Instructions(a) Indicate where deferred income taxes are reported in the financial statements.(b) Specify when deferred income taxes would need to be recognized for each of the items above, and indicate the rationale for such recognition.

Part B: Gumowski Company’s president has heard that deferred income taxes can be classified in different ways in the balance sheet.

InstructionsIdentify the conditions under which deferred income taxes would be classified as a noncurrent item in the balance sheet. What justification exists for such classification?

The company incurred $800 of income tax but has made no tax payments this year. Record the transaction.

Chapter 6 Solutions

PRINCIPLES OF TAXATION F/BUS...(LL)

Ch. 6 - Prob. 1QPDCh. 6 - Prob. 2QPDCh. 6 - Prob. 3QPDCh. 6 - Prob. 4QPDCh. 6 - For many years, Mr. K, the president of KJ Inc.,...Ch. 6 - Prob. 6QPDCh. 6 - Prob. 7QPDCh. 6 - Firm NB, which uses the cash method of accounting,...Ch. 6 - Prob. 9QPDCh. 6 - Prob. 10QPD

Ch. 6 - Prob. 11QPDCh. 6 - Firms generally prefer to engage in transactions...Ch. 6 - Describe the contrasting treatment of prepaid...Ch. 6 - Net operating losses can be carried forward...Ch. 6 - Nello Company owed 23,400 overdue rent to its...Ch. 6 - For each of the following businesses, indicate the...Ch. 6 - Assuming a 21 percent marginal tax rate, compute...Ch. 6 - Prob. 4APCh. 6 - FruAgro Company has average annual gross receipts...Ch. 6 - Prob. 6APCh. 6 - Firm F is a cash basis legal firm. In 2018, it...Ch. 6 - Prob. 8APCh. 6 - Prob. 9APCh. 6 - Prob. 10APCh. 6 - Brillo Company uses the calendar year and the cash...Ch. 6 - NC Company, a retail hardware store, began...Ch. 6 - Prob. 13APCh. 6 - Warren Company is a calendar year, cash basis...Ch. 6 - Prob. 15APCh. 6 - Wahoo Inc., a calendar year taxpayer, leases...Ch. 6 - Prob. 17APCh. 6 - Using a 21 percent rate, compute the deferred tax...Ch. 6 - Prob. 19APCh. 6 - Prob. 20APCh. 6 - Prob. 21APCh. 6 - Prob. 22APCh. 6 - Prob. 23APCh. 6 - Prob. 24APCh. 6 - Prob. 25APCh. 6 - Prob. 26APCh. 6 - Prob. 27APCh. 6 - BZD, a calendar year corporation, made the...Ch. 6 - Prob. 29APCh. 6 - Prob. 30APCh. 6 - Prob. 31APCh. 6 - Prob. 32APCh. 6 - Prob. 33APCh. 6 - GK Company, a calendar year accrual basis...Ch. 6 - Prob. 35APCh. 6 - Prob. 36APCh. 6 - TRW Inc. began business in 2019 and incurred net...Ch. 6 - Prob. 38APCh. 6 - Prob. 39APCh. 6 - Margaret, a married taxpayer filing a joint...Ch. 6 - Prob. 41APCh. 6 - Prob. 1IRPCh. 6 - Corporation DS owns assets worth 550,000 and has...Ch. 6 - Two years ago, a professional theater company paid...Ch. 6 - Prob. 4IRPCh. 6 - Prob. 5IRPCh. 6 - Prob. 6IRPCh. 6 - Every December, Maxo Inc., an accrual basis,...Ch. 6 - Prob. 8IRPCh. 6 - Prob. 9IRPCh. 6 - Corporation WJ began business in 2019 and elected...Ch. 6 - Prob. 11IRPCh. 6 - Bontaine Publications, an accrual basis, calendar...Ch. 6 - Prob. 2RPCh. 6 - Prob. 3RPCh. 6 - Prob. 4RPCh. 6 - Company Y began business in February 2019. By the...Ch. 6 - Prob. 2TPC

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- A company has only one deductible temporary difference due to the use of the current expected credit loss method (CECL) of recognizing credit losses (ie, bad debts) for financial reporting purposes. The company is trying to determine how the resulting deferred tax asset will be reported on the balance sheet. Which section of the authoritative literature describes whether deferred tax assets and liabilities are classified as current or noncurrent? Enter your response in the answer fields below. Unless specifically requested, your response should not cite implementation guidance. Guidance on correctly structuring your response appears above and below the answer fields. Type the topic here. Correctly formatted FASB ASC topics are 3 digits. FASB ASCarrow_forwardRich Goma Corporation failed to file its income tax return for the fiscal year ending August 31, 2021. On June 6, 2022, it filed an income tax return with a basic tax still due and payable for the fiscal year amounting to P500,000. Compute the interest penalty to be imposed by the BIR. P28,603 P45,873 P28,438 P46,207arrow_forwardMs. Kirsten provided information to the BIR leading to the recovery of P8,000,000 unpaid taxes. Compute for a. Final withholding tax b. Net amount to be released to the tax informerarrow_forward

- Mini, Inc., earns pretax book net income of $1,828,000 in 2018. Mini deducted $190,400 in bad debt expense for book purposes. This expense is not yet deductible for tax purposes.Mini reports $1,919,400 of pretax book net income in 2019. Mini did not deduct any bad debt expense for book purposes in 2019 but did deduct $142,800 in bad debt expense for tax purposes. Mini reports no other temporary or permanent differences. Assuming that the pertinent U.S. Federal corporate income tax rate is 21%, and Mini earns an after-tax rate of return on capital of 8%. a. The 2019 end-of-year balance in Mini’s deferred tax asset and deferred tax liability balance sheet accounts. If an amount is zero, enter "0". If required, round your answer to nearest whole value. 2019 a. Deferred tax asset account balance ______ b. Deferred tax liability account balance ______ b. The cost to Mini of the deferral of the bad debt deduction, considering the time value of money. Mini earns an…arrow_forwardShear Co.'s Year 1 financial statements included profit from an installment sale of $2,600 that was recognized but not received and credit loss expenses of $1,400. No receivables were written off during the year. It is anticipated that both items will be recognized for tax purposes in Year 3. The enacted tax rates are 30% in Year 1 and 25% in Year 3. What amount should Shear report as deferred income tax expense in its Year 1 income statement? A. $300 B. $360 C. $420 D. $780arrow_forwardWhich of the following statements accurately describes the impact of accounting for bad debts on taxes? A) Accounting for bad debts increases taxable income in the period they are recognized. B) Accounting for bad debts decreases taxable income in the period they are recognized. C Accounting for bad debts has no impact on taxable income. D) Accounting for bad debts defers taxable income to future periods.arrow_forward

- Consider the following accounts and determine if the account is a current liability, a noncurrent liability, or neither. A. cash B. federal income tax payable this year C. long-term note payable D. current portion of a long-term note payable E. note payable due in four years F. interest expense G. state income taxarrow_forward2) X reported a pre-tax income of P5,000,000. The taxable income per tax code does not tally with the income per GAAP. The differences are the nontaxable income of P500,000, bad debts based on estimate amounting to P300,000, and accrued rent income of P500,000. For the first 3 quarters, X made a total tax payment of P1,205,000 at 35% of taxable income at that time, which is creditable against income tax due computed under tax code. X' net tax payable after tax credits is a. 1,505,000 b. 440,000 C. 370,000 4300,000 Carlota Company is determining the amount of its pretax financial income for 2005 by making adjustment to taxable income from the company's 2005 tax return. The tax return indicates taxable income of P15,000,000 on which a tax liability of P4,800,000 has been recognized. Following is a list of items that may be required to determine pretax financial income from the amount of taxable income. Accelerated depreciation for income tax purposes was P2,000,000 and straight line…arrow_forwardRich Goma Corporation failed to file its income tax return for the fiscal year ending August 31, 2021. On June 6, 2022, it filed an income tax return with a basic tax still due and payable for the fiscal year amounting to P500,000. Compute the total tax assessment to be paid, excluding compromise penalty. P653,603 P689,275 P653,438 P660,873arrow_forward

- Indicate whether the following statements are "True" or "False" regarding the statute of limitations. a. If no return is filed or a fraudulent return is filed, assessments can be made at any time. b. If a taxpayer omits an amount of gross income in excess of 25 percent of the gross income stated on the return, the statute of limitations does not apply. c. In general, any tax that is imposed must be assessed within three years of the later of (a) the filing date of the return or (b) the unextended due date of the return. d. The statute of limitations may be extended for a fixed period of time by mutual consent of the IRS and the taxpayer.arrow_forwardOn December 31, for GAAP purposes, Clubs Inc. reported a balance of $40,000 in a warranty liability for anticipated costs to satisfy future warranty claims. The tax basis for the warranty liability is zero. No claims were paid during the year. The increase to income tax payable on December 31 is $85,000, and the tax rate is 25%. Assume no other differences between the tax basis and GAAP basis of assets and liabilities, or any beginning balances in deferred tax accounts. Required a. Record the income tax journal entry on December 31. •Note: If a line in a journal entry isn't required for the transaction, in the last line of the journal entry, select "N/A" as the account name and leave the Dr. and Cr. answers blank (zero). Date Account Name Dec. 31 Income Tax Expense Deferred Tax Asset Income Tax Payable N/A To record income tax expense Dr. Cr. 0 10000 0 0 0 0 b. Assume that there was a January 1 beginning balance of $4,000 in the deferred tax asset account. How would your answer to part…arrow_forwardWhich of the following statements is false? Select one: O A. In general, individual taxpayers are required to file a tax return only if their gross income exceeds the standard deduction OB. The penalty for failure to file is more severe than the penalty for failure to pay OC. Taxpayers may file a tax return even when they are not required to do so to obtain a refund of income taxes withheld OD. Individual tax returns are always due on April 15 for calendar-year individualsarrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Chapter 19 Accounting for Income Taxes Part 1; Author: Vicki Stewart;https://www.youtube.com/watch?v=FMjwcdZhLoE;License: Standard Youtube License