Microeconomics, Student Value Edition (2nd Edition)

2nd Edition

ISBN: 9780134461786

Author: Daron Acemoglu, David Laibson, John List

Publisher: PEARSON

expand_more

expand_more

format_list_bulleted

Question

Chapter 6, Problem 8Q

To determine

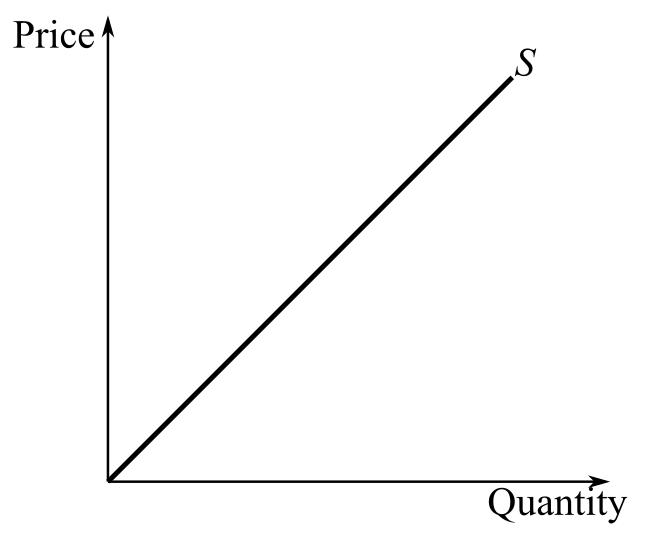

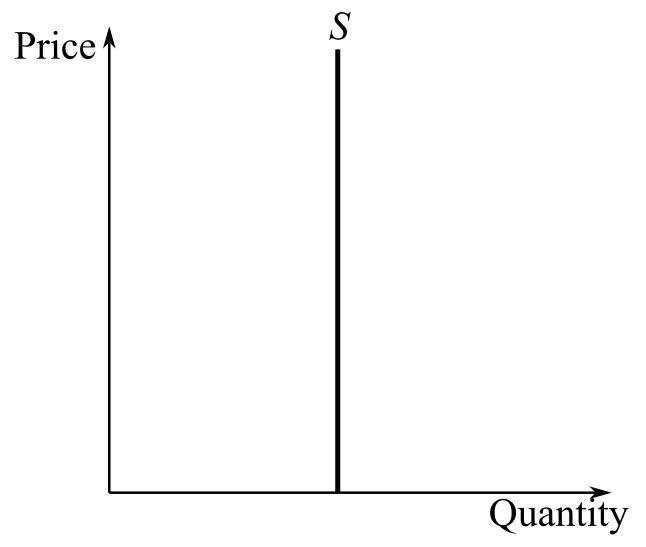

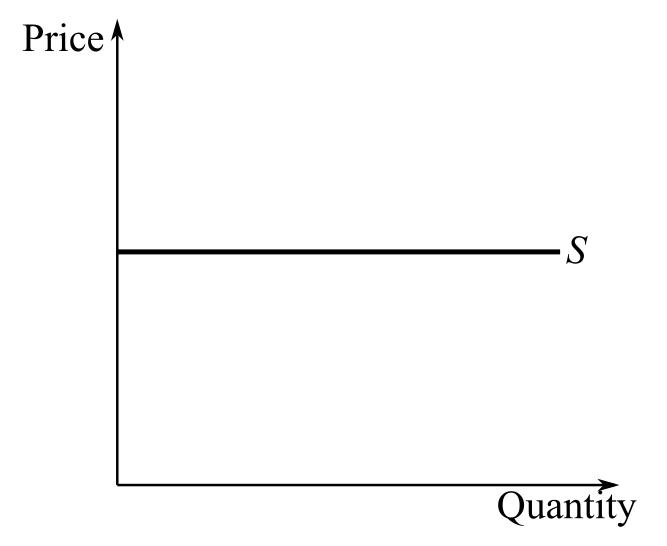

Elasticity of supply in the following curves:

(a)

(b)

(c)

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Students have asked these similar questions

Give three examples of goods with a vertical supply curve.

Explain how demand is seen by a purely competitive seller.

How is it possible for the elasticity of demand to change over time (in the long run)? Explain.

Chapter 6 Solutions

Microeconomics, Student Value Edition (2nd Edition)

Knowledge Booster

Similar questions

- The graph below shows the market supply and market demand curves for pencilsarrow_forwardComment on the following statement: “In the short run, Mr. Mohammed, a seller in the Fruit& Vegetable Market in Al-Aweer, faces a demand curve that is simply a horizontalline at themarket equilibrium price. In other words, competitive sellers, in this market, face perfectlyelastic demand in the short run.”arrow_forwardWhich of the following companies are most likely to face a nearly horizontal demand curve? Group of answer choices Companies (like Netflix) offering programs on television or computers Companies offering search engines on the Internet clothing retail stores offering their goods on the Internet The wholesale oil industry.arrow_forward

- Coca cola please Addressed in the Capstone Project: Analyze how demand and supply achieve an efficient market equilibrium and calculate various elasticities of demand and supply. Define and calculate the various economic costs of production in the short and long run.arrow_forwardJabari's HookNLadder is the only company selling fire engines in the fictional country of Alexandrina. Jabari initially produced four trucks, but then decided to increase production to five trucks. The following graph gives the demand curve faced by Jabari’s HookNLadder. As the graph shows, in order to sell the additional fire truck, Jabari must lower the price from $105,000 to $90,000 per truck. Notice that Jabari gains revenue from the sale of the additional engine, but at the same time, he loses revenue from the initial four engines because they are all sold at the lower price. Use the purple rectangle (diamond symbols) to shade the area representing the revenue lost from the initial four engines by selling at $90,000 rather than $105,000. Then use the green rectangle (triangle symbols) to shade the area representing the revenue gained from selling an additional engine at $90,000arrow_forwardShow that any linear inverse supply that passes through the origin (i.e., an inverse supply with the functional form p = c Q with c > 0) has a price elasticity of supply equal to one. Show that any linear inverse supply curve with a positive intercept (i.e., having the functional form p = k + c Q with c, k > 0) must be elastic.arrow_forward

- Which of the following would most likely be an example of elastic supply? Choose all that apply. A. luxury brand car B. gasoline C. a brand of jeans D. salt E. tap waterarrow_forwardDemand curve is perfectly elastic in case of which market structurearrow_forward(ALL OWNERSHIP GOES TO CENGAGE) The following graph plots a supply curve (orange line) for several sellers in the market for motor scooters in College Park, a university town in Maryland. Each seller has a single-motor scooter for sale. The market price of motor scooters is given by the horizontal black line at $70. Each rectangle on the graph corresponds to a particular seller in this market: blue (circle symbols) for Kevin, green (triangle symbols) for Maria, purple (diamond symbols) for Rajiv, tan (dash symbols) for Simone, and orange (square symbols) for Yakov. (Note: The name labels are to the right of the corresponding segment on the supply curve.) Use the rectangles to shade the areas representing producer surplus for each person who is willing to sell a motor scooter at a market price of $70. (Note: If a person will not sell a motor scooter at the market price, indicate this by leaving their rectangle in its original position on the palette.) Based on the information on…arrow_forward

- There are three sets of price and quantity below for a firm.P1 = $40 Q1 = 20P2 = $30 Q2 = 40 P1 = 30 Q1 = 40P2= 25 Q2 = 50 P1 = 25 Q1 = 50P2 = 20 Q2 = 60 Given the information above on the four sets of price and quantity 1. Using the price elasticity of demand (PED) formula (using the average formula),calculate the PED for each set of price and quantity demanded change, and determine inabsolute value the range of elasticity? 2. Using the information of above, calculate the total revenue (TR) for each and given theinformation from parts a, b and c, predict the price this firm will charge?arrow_forwardFor a firm with a downward-sloping demand curve, which of the following is true at the profit-maximizing level of output? For this case, let's assume that marginal costs are positive.a) demand is perfectly inelastic b) demand is inelastic but not perfectly inelastic c) demand is unit-elastic d) demand is elastic but not perfectly elastice) demand is perfectly elasticarrow_forwardThe elasticity of Supply is an important concept in Microeconomics as it relates to a business's ability to adjust its production and its production facility in response to market developments. Think of some examples of products and businesses that would have various degrees of Elasticity of Supply and share them here. For example, what would be the Elasticity of Supply for an original piece of art? What does this imply for the adjustment in this market to a change in Demand? How would you describe the Elasticity of Supply for a product such as peaches, plums, and other tree fruit? Consider first a brief period, such as weeks, and next a much longer period such as five years. How does the time horizon influence market adjustment when there is a change in Demand?arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Microeconomics: Private and Public Choice (MindTa...EconomicsISBN:9781305506893Author:James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. MacphersonPublisher:Cengage Learning

Microeconomics: Private and Public Choice (MindTa...EconomicsISBN:9781305506893Author:James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. MacphersonPublisher:Cengage Learning Economics: Private and Public Choice (MindTap Cou...EconomicsISBN:9781305506725Author:James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. MacphersonPublisher:Cengage Learning

Economics: Private and Public Choice (MindTap Cou...EconomicsISBN:9781305506725Author:James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. MacphersonPublisher:Cengage Learning

Microeconomics: Private and Public Choice (MindTa...

Economics

ISBN:9781305506893

Author:James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. Macpherson

Publisher:Cengage Learning

Economics: Private and Public Choice (MindTap Cou...

Economics

ISBN:9781305506725

Author:James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. Macpherson

Publisher:Cengage Learning