Accounting For Governmental & Nonprofit Entities

18th Edition

ISBN: 9781259917059

Author: RECK, Jacqueline L., Lowensohn, Suzanne L., NEELY, Daniel G.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Videos

Textbook Question

Chapter 7, Problem 12C

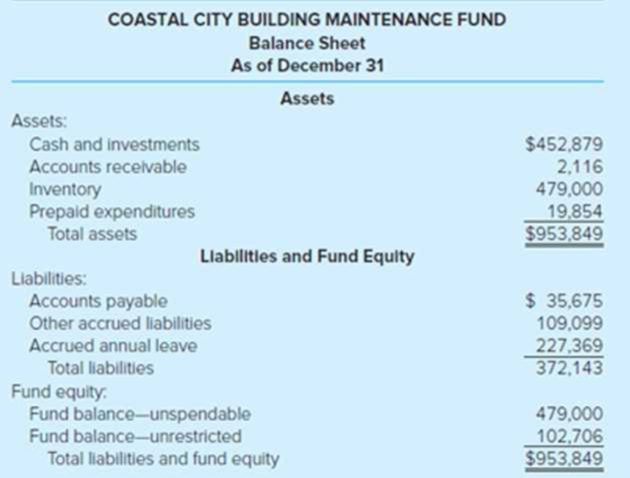

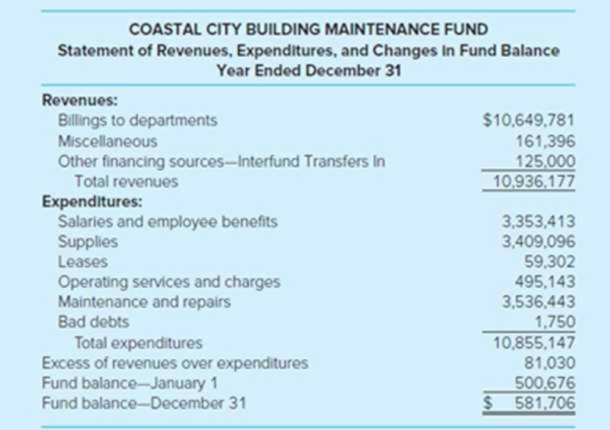

Internal Service Fund Reporting. (LO7-2) Financial statements for the Building Maintenance Fund, an internal service fund of Coastal City, are reproduced here. No further information about the nature or purposes of this fund is given in the annual report.

Required

- a. Assuming that the Building Maintenance Fund is an internal service fund, discuss whether the financial information is presented in accordance with GASB standards.

- b. If you were the manager of a city department that uses the services of the Building Maintenance Fund, what would you want to know in addition to the information disclosed in the financial statements?

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Students have asked these similar questions

The City of South Pittsburgh maintains its books so as to prepare fund accounting statements and records worksheet adjustments in order to prepare government-wide statements. You are to prepare, in journal form, worksheet adjustments for each of the following situations:

1. Deferred inflows of resources-property taxes of $69,400 at the end of the previous fiscal year were recognized as property tax revenue in the current yearAc€?cs Statement of Revenues, Expenditures, and Changes in Fund Balance.

2. The City levied property taxes for the current fiscal year in the amount of $10,000,000. When making the entries, it was estimated that 2 percent of the taxes would not be collected. At year-end, $600,000 of the taxes had not been collected. It was estimated that $320,000 of that amount would be collected during the 60-day period after the end of the fiscal year and that $80,000 would be collected after that time. The City had recognized the maximum of property taxes allowable under…

The City of South Pittsburgh maintains its books so as to prepare fund accounting statements and records worksheet adjustments in order to prepare government-wide statements. You are to prepare, in journal form, worksheet adjustments for each of the following situations:

1. Deferred inflows of resources-property taxes of $69,400 at the end of the previous fiscal year were recognized as property tax revenue in the current yearAc€?cs Statement of Revenues, Expenditures, and Changes in Fund Balance.

2. The City levied property taxes for the current fiscal year in the amount of $10,000,000. When making the entries, it was estimated that 2 percent of the taxes would not be collected. At year-end, $600,000 of the taxes had not been collected. It was estimated that $320,000 of that amount would be collected during the 60-day period after the end of the fiscal year and that $80,000 would be collected after that time. The City had recognized the maximum of property taxes allowable under…

A city constructs curbing in a new neighborhood and finances it as a special assessment. Under what condition should these transactions be recorded in an agency fund?

Never; the work is reported in the capital projects funds.

Only if the city is secondarily liable for any debt incurred to finance construction costs.

Only if the city is in no way liable for the costs of the construction.

In all cases.

Chapter 7 Solutions

Accounting For Governmental & Nonprofit Entities

Ch. 7 - Prob. 1QCh. 7 - Explain the reporting requirements for internal...Ch. 7 - A member of the city commission insists that the...Ch. 7 - Prob. 4QCh. 7 - What is the purpose of the Restricted Assets...Ch. 7 - Prob. 6QCh. 7 - Prob. 7QCh. 7 - When do GASB standards require interfund...Ch. 7 - Prob. 9QCh. 7 - What is meant by segment information for...

Ch. 7 - Prob. 11QCh. 7 - Internal Service Fund Reporting. (LO7-2) Financial...Ch. 7 - Proprietary Fund Operating Statement. (LO7-1)...Ch. 7 - Enterprise Fund Golf Course Management. (LO7-1)...Ch. 7 - Prob. 17.1EPCh. 7 - Which of the following would most likely be...Ch. 7 - Under GASB standards, the City of Parkview is...Ch. 7 - Prob. 17.4EPCh. 7 - Which of the following events would generally be...Ch. 7 - Proprietary funds a. Are permitted to integrate...Ch. 7 - Prob. 17.7EPCh. 7 - Prob. 17.8EPCh. 7 - Prob. 17.9EPCh. 7 - Prob. 17.10EPCh. 7 - The City of Tutland issued 10 million, 6 percent,...Ch. 7 - The City of Tutland issued 10 million, 6 percent,...Ch. 7 - Prob. 18EPCh. 7 - Prob. 19EPCh. 7 - Central Garage Internal Service Fund. (LO7-2) The...Ch. 7 - Internal Service Fund Statement of Cash Flows....Ch. 7 - Tribute Aquatic Center Enterprise Fund. (LO7-5)...Ch. 7 - Net Position Classifications. (LO7-5) During the...Ch. 7 - Central Station Enterprise Fund. (LO7-5) The Town...Ch. 7 - Enterprise Fund Journal Entries and Financial...Ch. 7 - Net Position Classifications. (LO7-5) The Village...Ch. 7 - Enterprise Fund Statement of Cash Flows. (LO7-5)...Ch. 7 - AppendixSolid Waste Enterprise Fund. (LO7-6) Brown...

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- A city constructs curbing in a new neighborhood and finances it as a special assessment. Under what condition should these transactions be recorded in an agency fund? Choose the correct.a. Never; the work is reported in the capital projects funds.b. Only if the city is secondarily liable for any debt incurred to finance construction costs.c. Only if the city is in no way liable for the costs of the construction.d. In all cases.arrow_forwardFor each of the following, indicate whether the statement is true or false and include a brief explanation for your answer.a. A pension trust fund appears in the government-wide financial statements but not in the fund financial statements.b. Permanent funds are included as one of the governmental funds.c. A fire department placed orders of $20,000 for equipment. The equipment is received but at a cost of $20,800. In compliance with requirements for fund financial statements, an encumbrance of $20,000 was recorded when the order was placed, and an expenditure of $20,800 was recorded when the order was received.d. The government reported a landfill as an enterprise fund. At the end of Year 1, the government estimated that the landfill will cost $800,000 to clean up when it is eventually full. Currently, it is 12 percent filled. At the end of Year 2, the estimation was changed to $860,000 when it was 20 percent filled. No payments are due for several years. Fund financial statements for…arrow_forward4. The City of Grinders Creek maintains its books in a manner that facilitates the preparation of fund accounting statements and uses worksheet adjustments to prepare government-wide statements. General fixed assets as of the beginning of the year, which had not been recorded, were as follows: Land $ 8,500,000 Buildings 27,600,000 Improvements Other Than Buildings 24,500,000 Equipment 11,690,000 Accumulated Depreciation, Capital Assets 25,800,000 During the year, expenditures for capital outlays amounted to $9,000,000. Of that amount, $4,800,000 was for buildings; the remainder was for improvements other than buildings. The capital outlay expenditures outlined in (2) were completed at the end of the year (and will begin to be depreciated next year). For purposes of financial statement presentation, all capital assets are depreciated using the straight-line method, with no estimated salvage value. Estimated lives are as follows: buildings, 40 years; improvements…arrow_forward

- 4. The City of Grinders Creek maintains its books in a manner that facilitates the preparation of fund accounting statements and uses worksheet adjustments to prepare government-wide statements. General fixed assets as of the beginning of the year, which had not been recorded, were as follows: Land $ 8,500,000 Buildings 27,600,000 Improvements Other Than Buildings 24,500,000 Equipment 11,690,000 Accumulated Depreciation, Capital Assets 25,800,000 During the year, expenditures for capital outlays amounted to $9,000,000. Of that amount, $4,800,000 was for buildings; the remainder was for improvements other than buildings. The capital outlay expenditures outlined in (2) were completed at the end of the year (and will begin to be depreciated next year). For purposes of financial statement presentation, all capital assets are depreciated using the straight-line method, with no estimated salvage value. Estimated lives are as follows: buildings, 40 years; improvements…arrow_forwardGeneral Fund, Debt Service Fund, General Fund, Capital Projects Fund, Special Revenue Fund, Capital Projects Fund, Enterprise Fund, Pension Trust Fund (Fiduciary), General Fund, Internal Service Fund, Permanent Fund. List the Appropriate Fund List the appropriate fund(s) that will be affected for each of the following transactions for Sienna City. Journal entries are not required. Bonds were issued to finance the construction of a new bridge. Sienna received a grant from the state to assist in financing the construction of a new bridge. Funds were set aside to pay of the principal and interest due on this year’s bonds. Land was received from a donor to be used as a park. It was stipulated by the donor that the land cannot be sold. Proceeds were collected from the sale of lottery tickets. By ordinance, these funds must be used for education and the school system. Construction on the new bridge was completed. The total cost was under budget and the excess funds were set aside to pay…arrow_forwardA city constructs a special assessment project (a sidewalk) for which it is secondarily liable. The city issues bonds of $90,000. It authorizes another $10,000 that is transferred out of the general fund. The sidewalk is built for $100,000. The citizens are billed for $90,000. They pay this amount and the debt is paid off. Where is the $100,000 expenditure for construction recorded? It is not recorded by the city. It is recorded in the agency fund. It is recorded in the general fund. It is recorded in the capital projects fund.arrow_forward

- A city constructs a special assessment project (a sidewalk) for which it is secondarily liable. The city issues bonds of $90,000. It authorizes another $10,000 that is transferred out of the general fund. The sidewalk is built for $100,000. The citizens are billed for $90,000. They pay this amount and the debt is paid off. Where is the $100,000 expenditure for construction recorded? Choose the correct.a. It is not recorded by the city.b. It is recorded in the agency fund.c. It is recorded in the general fund.d. It is recorded in the capital projects fund.arrow_forwardThe City of Southern Pines maintains its books so as to prepare fund accounting statements and records worksheet adjustments in order to prepare government-wide statements. As such, the City’s internal service fund, a motor pool fund, is included in the proprietary funds statements. Balance sheet asset accounts include: Cash, $87,000; Investments, $127,900; Due from the General Fund, $15,300; Inventories, $331,500; and Capital Assets (net), $979,200. Liability accounts include: Accounts Payable, $51,000; Long-Term Advance from Enterprise Fund, $612,000. The only transaction in the internal service fund that is external to the government is interest revenue in the amount of $2,900. Exclusive of the interest revenue, the internal service fund reported net income in the amount of $39,000. An examination of the records indicates that services were provided as follows: one-third to general government, one-third to public safety, and one-third to public works. Prepare necessary adjustments…arrow_forwardThe City of Soheil maintains its books so as to prepare fund accounting statements and prepares worksheet adjustments in order to prepare government-wide financial statements. Required: You are to prepare, in journal form, worksheet adjustments for each of the following situations. General fixed assets, as of the beginning of the year, which had not been recorded, were as follows: Land $ 96,000,000 Buildings 480,000,000 Improvements other than buildings 270,000,000 Equipment 60,000,000 Accumulated depreciation, capital assets 150,000,000 During the year, expenditures for capital outlays amounted to $22,700,000. Of that amount, $10,600,000 was for buildings; $8,300,000 was for improvements other than buildings, $95,000 was capitalized interest and the remainder was for land. The capital outlay expenditures outlined in (B) were completed at the end of the year (no depreciation until next year). For purposes of financial statement…arrow_forward

- Using the information below, what amount should be accounted for in a special revenue fund or funds? Warehouse equipment used to store supplies for delivery to all city departments and agencies on a cost-reimbursement basis $ 300,000 Equipment used for supplying electric power to residents $ 1,750,000 Receivables for completed sidewalks to be paid for in installments by affected property owners. Construction was financed by special assessment bonds for which the town has no liability $ 1,500,000 Cash received from federal government, dedicated to highway maintenance, that must be accounted for in a separate fund $ 1,800,000 Multiple Choice A. $1,800,000. B. $2,100,000. C. $5,350,000. D. $3,300,000.arrow_forwardIndicate (i) how each of the following transactions impacts the fund balance of the general fund, and its classifications, for fund financial statements and (ii) what impact each transaction has on the net position balance of the Government Activities on the government-wide financial statements.a. Issue a five-year bond for $6 million to finance general operations.b. Pay cash of $149,000 for a truck to be used by the police department.c. The fire department pays $17,000 to a government motor pool that services the vehicles of only the police and fire departments. Work was done on several department vehicles. d. Levy property taxes of $75,000 for the current year that will not be collected until four months into the subsequent year.e. Receive a grant for $7,000 that must be returned unless the money is spent according to the stipulations of the conveyance. That is expected to happen in the future.f. Businesses make sales of $20 million during the current year. The…arrow_forwardFor each of the following, indicate whether the statement is true or false and include a brief explanation for your answer. A pension trust fund appears in the government-wide financial statements but not in the fund financial statements. Permanent funds are included as one of the governmental funds. A fire department placed orders of $20,000 for equipment. The equipment is received but at a cost of $20,800. In compliance with requirements for fund financial statements, an encumbrance of $20,000 was recorded when the order was placed, and an expenditure of $20,800 was recorded when the order was received. The government reported a landfill as an enterprise fund. At the end of Year 1, the government estimated that the landfill will cost $800,000 to clean up when it is eventually full. Currently, it is 12 percent filled. At the end of Year 2, the estimation was changed to $860,000 when it was 20 percent filled. No payments are due for several years. Fund financial statements for Year 2…arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education

What is Fund Accounting?; Author: Aplos;https://www.youtube.com/watch?v=W5D5Dr0j9j4;License: Standard Youtube License