Concept explainers

Videos

Working with a Segmented Income Statement; Break-Even Analysis L07—4, L07—5

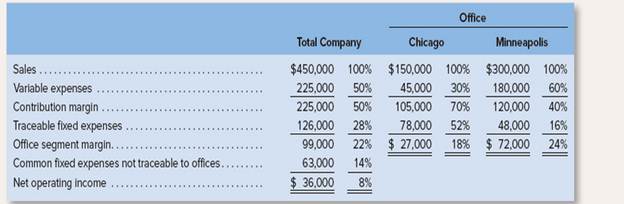

Raner, Harris & Chan is a consulting firm that specializes in information systems for medical and dental clinics. The firm has two offices—one in Chicago and one in Minneapolis. The firm classifies the direct costs of consulting jobs as variable costs. A contribution format segmented income statement for the company’s most recent year is given

Required:

1. Compute the companywide break-even point in dollar sales. Also, compute the break-even point for the Chicago office and for the Minneapolis office. Is the companywide break-even point greater than, less than, or equal to the sum of the Chicago and Minneapolis break-even points? Why?

2. By how much would the company’s net operating income increase if Minneapolis increased its sales by $75,000 per year? Assume no change in cost behavior patterns.

3. Refer to the original data. Assume that sales in Chicago increase by $50,000 next year and that sales in Minneapolis remain unchanged.

Assume no change in fixed costs.

a. Prepare a new segmented income statement for the company using the above format. Show both amounts and percentages.

b. Observe from the income statement you have prepared that the contribution margin ratio for Chicago has remained unchanged at 70% (the same as in the above data) but that the segment margin ratio has changed. How do you explain the change in the segment margin ratio?

Want to see the full answer?

Check out a sample textbook solution

Chapter 7 Solutions

Introduction To Managerial Accounting

- Raner, Harris & Chan is a consulting firm that specializes in information systems for medical and dental clinics. The firm has two offices—one in Chicago and one in Minneapolis. The firm classifies the direct costs of consulting jobs as variable costs. A contribution format segmented income statement for the company’s most recent year is given: Total Company Office Chicago Minneapolis Sales $ 508,500 100.00% $ 169,500 100.00% $ 339,000 100.00% Variable expenses 254,250 50.00% 50,850 30.00% 203,400 60.00% Contribution margin 254,250 50.00% 118,650 70.00% 135,600 40.00% Traceable fixed expenses 142,380 28.00% 88,140 52.00% 54,240 16.00% Office segment margin 111,870 22.00% $ 30,510 18.00% $ 81,360 24.00% Common fixed expenses not traceable to offices 71,190 14.00% Net operating income $ 40,680 8.00% rev: 06_09_2020_QC_CS-215744, 09_15_2020_QC_CS-220558, 11_04_2020_QC_CS-238526, 03_30_2021_QC_CS-258090 Exercise 6-17 (Algo) Working with…arrow_forwardRaner, Harris and Chan is a consulting firm specializing in information systems for medical and dental clinics. The firm has two offices—one in Chicago and one in Minneapolis. It classifies the direct costs of consulting jobs as variable costs. A contribution format segmented income statement for the company’s most recent year is given below: Total Company Office Chicago Minneapolis Sales $ 490,500 100.00% $ 163,500 100.00% $ 327,000 100.00% Variable expenses 245,250 50.00% 49,050 30.00% 196,200 60.00% Contribution margin 245,250 50.00% 114,450 70.00% 130,800 40.00% Traceable fixed expenses 137,340 28.00% 85,020 52.00% 52,320 16.00% Office segment margin 107,910 22.00% $ 29,430 18.00% $ 78,480 24.00% Common fixed expenses not traceable to offices 68,670 14.00% Net operating income $ 39,240 8.00% 2. How much would the company’s net operating income increase if Minneapolis increased its sales by $81,750 per year? Assume no change in cost behavior patterns.arrow_forwardRaner, Harris and Chan is a consulting firm specializing in information systems for medical and dental clinics. The firm has two offices—one in Chicago and one in Minneapolis. It classifies the direct costs of consulting jobs as variable costs. A contribution format segmented income statement for the company’s most recent year is given below: Total Company Office Chicago Minneapolis Sales $ 468,000 100.00% $ 156,000 100.00% $ 312,000 100.00% Variable expenses 234,000 50.00% 46,800 30.00% 187,200 60.00% Contribution margin 234,000 50.00% 109,200 70.00% 124,800 40.00% Traceable fixed expenses 131,040 28.00% 81,120 52.00% 49,920 16.00% Office segment margin 102,960 22.00% $ 28,080 18.00% $ 74,880 24.00% Common fixed expenses not traceable to offices 65,520 14.00% Net operating income $ 37,440 8.00% Exercise 6-17 (Algo) Working with a Segmented Income Statement [LO6-4] Assume Minneapolis’s sales by major market are: Minneapolis Market…arrow_forward

- Raner, Harris & Chan is a consulting firm that specializes in information systems for medical and dental clinics. The firm has two offices—one in Chicago and one in Minneapolis. The firm classifies the direct costs of consulting jobs as variable costs. A contribution format segmented income statement for the company’s most recent year is given: Office Total Company Chicago Minneapolis Sales $ 450,000 100 % $ 150,000 100 % $ 300,000 100 % Variable expenses 225,000 50 % 45,000 30 % 180,000 60 % Contribution margin 225,000 50 % 105,000 70 % 120,000 40 % Traceable fixed expenses 126,000 28 % 78,000 52 % 48,000 16 % Office segment margin 99,000 22 % $ 27,000 18 % $ 72,000 24 % Common fixed expenses not traceable to offices 63,000 14 % Net operating income $ 36,000 8 % 3. Assume that sales in Chicago increase by $50,000…arrow_forwardRaner, Harris & Chan is a consulting firm that specializes in information systems for medical and dental clinics. The firm has two offices—one in Chicago and one in Minneapolis. The firm classifies the direct costs of consulting jobs as variable costs. A contribution format segmented incomestatement for the company’s most recent year is given: Required:1. Compute the companywide break-even point in dollar sales. Also, compute the break-even point for the Chicago office and for the Minneapolis office. Is the companywide break-even point greater than, less than, or equal to the sum of the Chicago and Minneapolis break-evenpoints? Why?2. By how much would the company’s net operating income increase if Minneapolis increased its sales by $75,000 per year? Assume no change in cost behavior patterns.3. Refer to the original data. Assume that sales in Chicago increase by $50,000 next year and that sales in Minneapolis remain unchanged. Assume no change in fixed costs.a. Prepare a new…arrow_forwardRaner, Harris and Chan is a consulting firm that specializes in information systems for medical and dental clinics. The firm has two offices—one in Chicago and one in Minneapolis. The firm classifies the direct costs of consulting jobs as variable costs. A contribution format segmented income statement for the company’s most recent year is given: Total Company Office Chicago Minneapolis Sales $ 450,000 100% $ 150,000 100% $ 300,000 100% Variable expenses 225,000 50% 45,000 30% 180,000 60% Contribution margin 225,000 50% 105,000 70% 120,000 40% Traceable fixed expenses 126,000 28% 78,000 52% 48,000 16% Office segment margin 99,000 22% $ 27,000 18% $ 72,000 24% Common fixed expenses not traceable to offices 63,000 14% Net operating income $ 36,000 8% Assume that Minneapolis’ sales by major market are: Minneapolis Market Medical Dental Sales $ 300,000 100% $ 200,000 100% $ 100,000 100% Variable expenses 180,000 60% 128,000 64% 52,000 52% Contribution margin 120,000 40% 72,000 36% 48,000…arrow_forward

- Raner, Harris and Chan is a consulting firm that specializes in information systems for medical and dental clinics. The firm has two offices—one in Chicago and one in Minneapolis. The firm classifies the direct costs of consulting jobs as variable costs. A contribution format segmented income statement for the company’s most recent year is given: Total Company Office Chicago Minneapolis Sales $ 450,000 100% $ 150,000 100% $ 300,000 100% Variable expenses 225,000 50% 45,000 30% 180,000 60% Contribution margin 225,000 50% 105,000 70% 120,000 40% Traceable fixed expenses 126,000 28% 78,000 52% 48,000 16% Office segment margin 99,000 22% $ 27,000 18% $ 72,000 24% Common fixed expenses not traceable to offices 63,000 14% Net operating income $ 36,000 8% 2. By how much would the company’s net operating income increase if Minneapolis increased its sales by $75,000 per year? Assume no change in cost behavior patterns.arrow_forwardObjective: Consider that you are an analyst at Regeneron Pharmaceuticals. You need to decide how to allocate administrative overhead costs to Regeneron's main commercial products (Eylea, Dupixent, Kevzara and Praluent). Determine how to appropriately allocate the costs in the table below to each of the commercial products using an allocation methodology of your choice. Department2019 Annual Operating ExpenseTime spent supporting Commercial productsCommercial$200MM100%IT$100MM25%Facilities$150MM0%Finance$25MM20%Human Resources$75MM10% Use the supporting document Net Product Sales of REGN Products to facilitate your analysis. Provide a written summary of how you allocated the overhead costs to each product in an outline of no more than one page. As a starting point, it's recommended that you revisit the material we covered in Chapter 12. Guidance on calculations:Start off with Net Product Sales of REGN Products. Your objective pertains to 2019 expenses, so you should be reviewing 2019…arrow_forwardSpruce−Up Company provides cleaning services to commercial and residential customers. The commercial business segment provided services to 290 customers and the residential business segment provided services to 645 customers. Commercial Residential Total Service Revenue $93,000 $123,000 $216,000 Variable Costs 26,000 49,000 75,000 Fixed Costs 47,000 53,000 100,000 Operating Income $20,000 $21,000 $41,000 Identify the segment with the lower contribution margin ratio and show the amount of its contribution margin ratio. (Round your answer to two decimals.) A. Residential, 60.16% B. Residential, 39.84% C. Commercial, 21.51% D. Commercial, 44.96%arrow_forward

- Party Supply is trying to decide whether or not to continue its costume segment. The information shown is available for Party Supply’s business segments. Assume that neither the Direct fixed costs nor the Allocated common fixed costs may be eliminated, but will be allocated to the two remaining segments. Costumes PartySupplies FloralDecorations Sales $160,000 $111,000 $211,000 Variable costs 84,000 49,000 119,000 Contribution margin $76,000 $62,000 $92,000 Direct fixed costs 50,000 19,000 26,000 Allocated common fixed costs 30,000 26,000 30,000 Net income $(4,000) $17,000 $37,000 If costumes are dropped, what change will occur to profit? Profit will decrease by $????arrow_forward7. Party Supply is trying to decide whether or not to continue its costume segment. The information shown is available for Party Supply’s business segments. Assume that neither the Direct fixed costs nor the Allocated common fixed costs may be eliminated, but will be allocated to the two remaining segments. Costumers Party Supplies Floral Decorations Sales $160,000 $110,000 $210,000 Variable costs 84,000 50,000 120,000 Contribution margin 76,000 60,000 90,000 Direct fixed costs 50,000 20,000 25,000 Allocated common fixed costs. 30,000 25,000 30,000 Net income $…arrow_forwardStructuring a Keep-or-Drop Product Line Problem Shown below is a segmented income statement for Orzo Company's three laminated flooring product lines: Strip Plank Parquet Total Sales revenue $400,000 $200,000 $300,000 $900,000 Less: Variable expenses 225,000 120,000 250,000 595,000 Contribution margin $175,000 $ 80,000 $ 50,000 $305,000 Less direct fixed expenses: Machine rent (5,000) (20,000) (50,000) (75,000) Supervision (15,000) (10,000) (20,000) (45,000) Depreciation (35,000) (10,000) (25,000) (70,000) Segment margin $120,000 $ 40,000 $ (45,000) $115,000 Orzo's management is deciding whether to keep or drop the parquet product line. Orzo's parquet flooring product line has a contribution margin of $50,000 (sales of $300,000 less total variable costs of $250,000). All variable costs are relevant. Relevant fixed costs associated with this line include $30,000 in machine rent and $4,700 in supervision salaries. Required: 1. List…arrow_forward

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education