Principles of Corporate Finance (Mcgraw-hill/Irwin Series in Finance, Insurance, and Real Estate)

12th Edition

ISBN: 9781259144387

Author: Richard A Brealey, Stewart C Myers, Franklin Allen

Publisher: McGraw-Hill Education

expand_more

expand_more

format_list_bulleted

Concept explainers

Videos

Textbook Question

Chapter 7, Problem 20PS

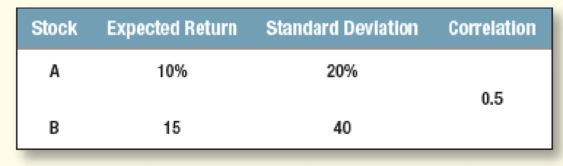

Portfolio risk You can form a portfolio of two assets, A and B, whose returns have the following characteristics:

If you demand an expected return of 12%, what are the portfolio weights? What is the portfolio’s standard deviation?

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Students have asked these similar questions

Using the following data:

Scenario Probability return K1 return K2

0.2

-10%

5%

W2

0.4

0%

30%

W3

0.4

20%

-5%

compute the weights in the portfolio with minimum risk. What are the expected return

and risk of this minimum risk portfolio?

Supposing the return from an investment has the following probability distribution

Return Probability

R (%)

8 0.2

10 0.2

12 0.5

14 0.1

Required:

What is the expected return of the investment?

What is the risk as measured by the standard deviation of expected returns?

Consider the following information: The possible rate of return for a portfolio for an investment is shown below.Probability Possible rate of return 0.25 0.09 0.25 0.11 0.25 0.13 0.25 0.16What is the expected rate of return for the investment?

Chapter 7 Solutions

Principles of Corporate Finance (Mcgraw-hill/Irwin Series in Finance, Insurance, and Real Estate)

Ch. 7 - Expected return and standard deviation A game of...Ch. 7 - Standard deviation of returns The following table...Ch. 7 - Average returns and standard deviation During the...Ch. 7 - Portfolio risk True or false? a. Investors prefer...Ch. 7 - Risk and diversification In which of the following...Ch. 7 - Portfolio risk To calculate the variance of a...Ch. 7 - Portfolio betas Suppose the standard deviation of...Ch. 7 - Portfolio betas A portfolio contains equal...Ch. 7 - Prob. 9PSCh. 7 - Prob. 10PS

Ch. 7 - Stocks vs. bonds Each of the following statements...Ch. 7 - Prob. 12PSCh. 7 - Prob. 13PSCh. 7 - Portfolio risk Hyacinth Macaw invests 60% of her...Ch. 7 - Portfolio risk a) How many variance terms and how...Ch. 7 - Portfolio risk Table 7.9 shows standard deviations...Ch. 7 - Portfolio risk Your eccentric Aunt Claudia has...Ch. 7 - Stock betas There are few, if any, real companies...Ch. 7 - Portfolio risk You can form a portfolio of two...Ch. 7 - Portfolio risk Here are some historical data on...Ch. 7 - Portfolio risk Suppose that Treasury bills offer a...Ch. 7 - Beta Calculate the beta of each of the stocks in...

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- You are given the following information concerning three portfolios, the market portfolio, and the risk-free asset: Portfolio Y Z Market Risk-free Rp 13.5% бр 35.00% 12.5 30.00 7.1 20.00 10.6 4.4 25.00 0 Вр 1.55 1.20 0.80 1.00 0 Assume that the correlation of returns on Portfolio Y to returns on the market is 0.70. What percentage of Portfolio Y's return is driven by the market? Note: Enter your answer as a decimal not a percentage. Round your answer to 4 decimal places. × Answer is complete but not entirely correct. R-squared 0.9785arrow_forwardWhich of the following measures the total risk of a portfolio? A. Standard Deviation B. Correlation Coefficient C. Beta D. Alphaarrow_forwardYou are given the following information concerning three portfolios, the market portfolio, and the risk-free asset: Portfolio X Y Z Market Risk-free Rp 14.0% 13.0 .8.5 12.0 7.2 Ор 39.00% 34.00 24.00 29.00 0 Bp 1.50 1.15 0.90 1.00 0 Assume that the correlation of returns on Portfolio Y to returns on the market is 0.90. What percentage of Portfolio Y's return is driven by the market? Note: Enter your answer as a decimal not a percentage. Round your answer to 4 decimal places. R-squaredarrow_forward

- An investor wants to determine the safest way to structure a portfolio from several investments, whose annual returns under different scenarios are as follows: Returns Scenario A B. D Probability 1. 0.11 -0.09 0.10 0.07 0.10 -0.11 0.12 0.14 0.06 0.10 3 0.09 0.15 0.11 0.08 0.10 4 0.25 0.18 0.33 0.07 0.30 0.18 0.16 0.1 0.06 0.40 9. Suppose the investor ignores the scenarios have different probabilities. If he has determined his risk aversion value is 0.75, what percentage of his portfolio should be invested in A? percent 2.arrow_forwardThe following portfolios are being considered for investment. During the period under consideration, RFR = 0.07.Portfolio Return Beta σiA 0.15 1.0 0.05B 0.20 1.5 0.10C 0.10 0.6 0.03D 0.17 1.1 0.06Market 0.13 1.0 0.04 a. Compute the Sharpe measure for each portfolio and the market portfolio. b. Compute the Treynor measure for each portfolio and the market portfolio. c. Rank the portfolios using each measure, explaining the cause for any differences you find in the rankings.arrow_forwardPortfolio Suppose rA ~ N (0.05, 0.01), rB ~ N (0.1, 0.04) with pA,B = 0.2 where rA and rB are CCR’s. a) Suppose you construct a portfolio with 50% for A and 50% for B. Find the variance of the portfolio CCR. b) Find the portfolio expected gross return. c) Find the expected portfolio CCR.arrow_forward

- You are given the following information concerning three portfolios, the market portfolio, and the risk-free asset: 8p 1.70 1.30 0.85 1.00 Portfolio X Y Z Market Risk-free Rp 11.5% 10.5 7.2 10.9 4.6 R-squared op 38.00% 33.00 23.00 28.00 0 Assume that the correlation of returns on Portfolio Y to returns on the market is 0.76. What percentage of Portfolio Y's return is driven by the market? Note: Enter your answer as a decimal not a percentage. Round your answer to 4 decimal places.arrow_forwardAn investiment portfolio consists of two securities, X and Y. The weight of X is 30%. Asset X's expected return is 15% and the standard deviation is 28%. Asset Y's expected return is 23% and the standard deviation is 33%. Assume the correlation coefficient between X and Y is 0.37. A. Calcualte the expected return of the portfolio. B. Calculate the standard deviation of the portfolio return. C. Suppose now the investor decides to add some risk free assets into this portfolio. The new weights of X, Y and risk free assets are 0.21, 0.49 and 0.30. What is the standard deviation of the new portfolio?arrow_forwardState the return rate (in %) for your optimal portfolio.arrow_forward

- Required: a) Calculate the expected return on this portfolio. b) What is the Beta of this portfolio? c) Does this portfolio have more or less systematic risk than an average asset?arrow_forwardUse the following CAPM equation for a portfolio to answer the questions that follow:E(RP) = RF + βP (RM – RF) = 1 + 0.8 (5 – 1) = 4.2% a) Is the portfolio defensive or aggressive. Why? b) If the actual portfolio return is 6%, what is the portfolio’s alpha?arrow_forwardShow detailed steps to solve the following question. Consider a portfolio comprised of three securities in the following proportions and with the indicated security beta. a.) What is the portfolios beta? b.) Wht is the portfolios expected return?arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education

Portfolio return, variance, standard deviation; Author: MyFinanceTeacher;https://www.youtube.com/watch?v=RWT0kx36vZE;License: Standard YouTube License, CC-BY