COST ACCOUNTING

6th Edition

ISBN: 9781260951516

Author: LANEN/ANDERSON

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Concept explainers

Videos

Textbook Question

Chapter 7, Problem 38E

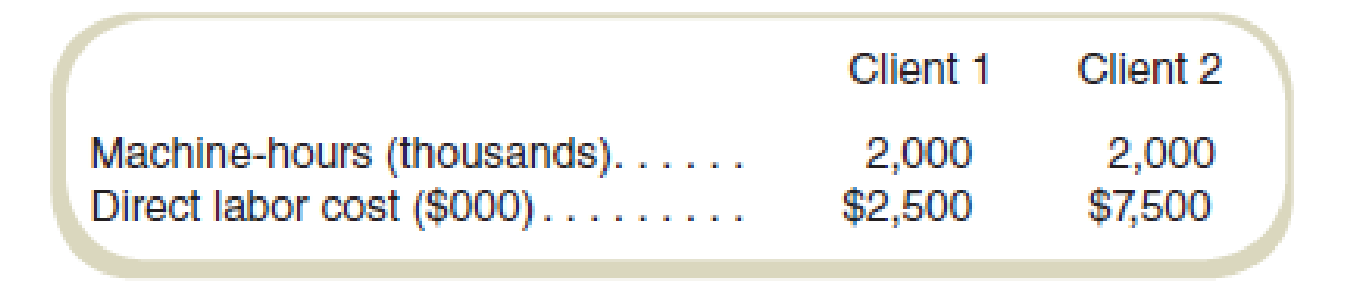

Predetermined Overhead Rates: Ethical Issues

Marine Components produces parts for airplanes and ships. The parts are produced to specification by their customers, who pay either a fixed price (the price does not depend directly on the cost of the job) or price equal to recorded cost plus a fixed fee (cost plus). For the upcoming year (year 2), Marine expects only two clients (client 1 and client 2). The work done for client 1 will all be done under fixed-price contracts while the work done for client 2 will all be done under cost-plus contracts.

Manufacturing overhead for year 2 is estimated to be $10 million. Other budgeted data for year 2 include:

Required

- a. Compute the predetermined rate assuming that Marine Components uses machine-hours to apply overhead.

- b. Compute the predetermined rate assuming that Marine Components uses direct labor cost to apply overhead.

- c. Which allocation base will provide higher income for Marine Components?

- d. Is it ethical to choose an allocation method based on which one leads to higher income for the firm?

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Students have asked these similar questions

A&R Quality Advisors is a small consulting firm offering quality audits and advising services to small and mid-sized

manufacturing firms. Quality audits entail reviewing, checking, and documenting quality practices within a firm.

Quality advising entails making recommendations for new or revised quality practices. Other firms in the area offer

one or both of these services, although the competition for quality audit jobs is stronger than for quality advising.

In addition to senior executives, A&R employees are either staff or managers. Staff employees are usually younger

with less experience. Managers, who oversee the staff on jobs, are more experienced. The average hourly wage is

$60 for staff and $150 for managers. (Both staff and managers are paid an annual salary; these hourly costs are

based on 2,000 average annual hours worked.) Staff are expected to spend at least 90 percent of their time on

billable work. Because of administrative work associated with supervising the staff and…

Angler Industries produces a product which goes through two operations, Assembly and Finishing, before it is ready to be shipped. Next year's expected

costs and activities are shown below.

Direct labor hours

Machine hours

Overhead costs

Multiple Choice

O $15.60.

O

Assume that the Assembly Department allocates overhead based on machine hours, and the Finishing Department allocates overhead based on direct

labor hours. How much total overhead will be assigned to a product that requires 1 direct labor hour and 3.4 machine hours in the Assembly Department,

and 4.0 direct labor hours and 0.6 machine hours in the Finishing Department?

$3.40

Assembly

190,000 DLH

390,000 MH

$16.10.

$ 390,000

Finishing)

149,000 DLH:

95,550 MH

$ 581,100

Using ABC in a service company

Blanchette Plant Service completed a special landscaping job for Kerry Company. Blanchette uses ABC and has the following predetermined overhead allocation rates:

The Kerry job included $750 in plants; $1,300 in direct labor; one design; and 30 plants.

Requirements

What is the total cost of the Kerry job?

If Kerry paid $3,540 for the job, what is the operating income or loss?

If Blanchette desires an operating income of 30% of cost, how much should the company charge for the Kerry job?

Chapter 7 Solutions

COST ACCOUNTING

Ch. 7 - What are characteristics of companies that are...Ch. 7 - Direct labor-hours and direct labor dollars are...Ch. 7 - What is the purpose of having two manufacturing...Ch. 7 - How does the accountant know what to record for...Ch. 7 - How is job costing in service organizations (for...Ch. 7 - What are the costs of a product using normal...Ch. 7 - Prob. 7RQCh. 7 - What are three common sources of improprieties in...Ch. 7 - In the context of job costing, what are projects?...Ch. 7 - Why do most companies use normal or standard...

Ch. 7 - Why is control of materials important from a...Ch. 7 - Worrying about the choice of an overhead...Ch. 7 - Prob. 13CADQCh. 7 - Interview the manager of a campus print shop or a...Ch. 7 - Would a dentist, an architect, a landscaper, and a...Ch. 7 - Consider two firms in the same industry. Is it...Ch. 7 - Prob. 17CADQCh. 7 - Assume that you have been asked to paint the...Ch. 7 - Prob. 19CADQCh. 7 - ABC Consultants works for only two clients: a...Ch. 7 - Prob. 21CADQCh. 7 - Assigning Costs to Jobs The following transactions...Ch. 7 - Assigning Costs to Jobs Sunset Products...Ch. 7 - Assigning Costs to Jobs Forest Components makes...Ch. 7 - Assigning Costs to Jobs Partially completed...Ch. 7 - Assigning Costs to Jobs Selected information from...Ch. 7 - Assigning Costs to Jobs Partially completed...Ch. 7 - Predetermined Overhead Rates Dixboro Company...Ch. 7 - Predetermined Overhead Rates Southern Rim Parts...Ch. 7 - Refer to the information in Exercise 7-29. Prepare...Ch. 7 - How much overhead was applied to each of the four...Ch. 7 - Refer to the information in Exercise 7-31. Prepare...Ch. 7 - Predetermined Overhead Rates Aspen Company...Ch. 7 - Prob. 34ECh. 7 - Applying Overhead Using a Predetermined Rate Marys...Ch. 7 - Applying Overhead Using a Predetermined Rate Turco...Ch. 7 - Calculating Over- or Underapplied Overhead Toms...Ch. 7 - Predetermined Overhead Rates: Ethical Issues...Ch. 7 - Compute the predetermined rate assuming that...Ch. 7 - Job Costing in a Service Organization At the...Ch. 7 - Job Costing in a Service Organization For August,...Ch. 7 - Job Costing in a Service Organization Allocation...Ch. 7 - Job Costing in a Service Organization TechMaster...Ch. 7 - Prob. 44ECh. 7 - Prob. 45ECh. 7 - Prob. 46PCh. 7 - Estimate Machine-Hours Worked from Overhead Data...Ch. 7 - Estimate Hours Worked from Overhead Data Capitol,...Ch. 7 - What will Wabash report as Cost of Goods Sold for...Ch. 7 - Assigning CostsMissing Data The following...Ch. 7 - Assigning Costs: Missing Data The following...Ch. 7 - Analysis of Overhead Using a Predetermined Rate...Ch. 7 - Analysis of Overhead Using a Predetermined Rate...Ch. 7 - Finding Missing Data A new computer virus...Ch. 7 - Cost Accumulation: Service Youth Athletic Services...Ch. 7 - Job Costs: Service Company For the month of July,...Ch. 7 - Job Costs in a Service Company On September 1, two...Ch. 7 - Tracing Costs in a Job Company The following...Ch. 7 - Cost Flows through Accounts Brighton Services...Ch. 7 - Show Flow of Costs to Jobs Kims Asphalt does...Ch. 7 - Reconstruct Missing Data A tornado struck the only...Ch. 7 - Find Missing Data IYF Corporation manufactures...Ch. 7 - Find Missing Data Accounting records for NIC...Ch. 7 - Incomplete Data: Job Costing Chelsea Household...Ch. 7 - Job Costing and Ethics Old Port Shipyards does...Ch. 7 - Job Costing and Ethics Chuck Moore supervises two...Ch. 7 - Job Costing and Ethics Global Partners is a...Ch. 7 - Prob. 68ICCh. 7 - What is the predetermined overhead rate for...

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Mary Manufacturing has four categories of overhead. The four categories and expected overhead costs for each category for next year are listed below: Maintenance 200,000.00 Material handling 32,000.00 Setups 100,000.00 Inspection 120,000.00 Currently, overhead is applied using a predetermined overhead rate, based on 80% of direct labor. The company has been asked to submit a bid for a proposed job. The plant manager feels that getting this job would result in new business in future years. Bids are based on full manufacturing cost plus 20 percent. Estimates for the proposed job are as follows: Direct materials 6,000.00 Direct labor (1k hours) 10,000.00 No. of materials moves 12.00 No. of inspections 10.00 No. of setups 2.00 No. of machine hours 500.00 In the past, full manufacturing cost has been calculated using normal costing. The plant manager has heard of a new way of applying overhead that…arrow_forwardMary Manufacturing has four categories of overhead. The four categories and expected overhead costs for each category for next year are listed below: Maintenance 200,000.00 Material handling 32,000.00 Setups 100,000.00 Inspection 120,000.00 Currently, overhead is applied using a predetermined overhead rate, based on 80% of direct labor. The company has been asked to submit a bid for a proposed job. The plant manager feels that getting this job would result in new business in future years. Bids are based on full manufacturing cost plus 20 percent. Estimates for the proposed job are as follows: Direct materials 6,000.00 Direct labor (1k hours) 10,000.00 No. of materials moves 12.00 No. of inspections 10.00 No. of setups 2.00 No. of machine hours 500.00 In the past, full manufacturing cost has been calculated using normal costing. The plant manager has heard of a new way of applying overhead that…arrow_forwardMary Manufacturing has four categories of overhead. The four categories and expected overhead costs for each category for next year are listed below: Maintenance 200,000.00 Material handling 32,000.00 Setups 100,000.00 Inspection 120,000.00 Currently, overhead is applied using a predetermined overhead rate, based on 80% of direct labor. The company has been asked to submit a bid for a proposed job. The plant manager feels that getting this job would result in new business in future years. Bids are based on full manufacturing cost plus 20 percent. Estimates for the proposed job are as follows: Direct materials 6,000.00 Direct labor (1k hours) 10,000.00 No. of materials moves 12.00 No. of inspections 10.00 No. of setups 2.00 No. of machine hours 500.00 In the past, full manufacturing cost has been calculated using normal costing. The plant manager has heard of a new way of applying overhead that…arrow_forward

- The management of Garn Corporation would like to investigate the possibility of basing its predetermined overhead rate on activity at capacity rather than on the estimated activity for the coming year. The Corporation's controller has provided an example to illustrate how this new system would work. In this example, the allocation base is machine-hours and the estimated activity for the upcoming year is 59,400 machine-hours. Capacity is 78,400 machine-hours. All of the manufacturing overhead is fixed and is $3,136,000 per year within the range of 59,400 to 78,400 machine-hours. If the Corporation bases its predetermined overhead rate on capacity but the actual level of activity for the year turns out to be 59,900 machine-hours, the cost of unused capacity shown on the income statement prepared for internal management purposes would be closest to: Multiple Choice $26.177 $766,177 $740,000 $26,397arrow_forwardMary Manufacturing has four categories of overhead. The four categories and expected overhead costs for each category for next year are listed below: Maintenance 200,000.00 Material handling 32,000.00 Setups 100,000.00 Inspection 120,000.00 Currently, overhead is applied using a predetermined overhead rate, based on 80% of direct labor. The company has been asked to submit a bid for a proposed job. The plant manager feels that getting this job would result in new business in future years. Bids are based on full manufacturing cost plus 20 percent. Estimates for the proposed job are as follows: Direct materials 6,000.00 Direct labor (1k hours) 10,000.00 No. of materials moves 12.00 No. of inspections 10.00 No. of setups 2.00 No. of machine hours 500.00 In the past, full manufacturing cost has been calculated using normal costing. The plant manager has heard of a new way of applying overhead that…arrow_forwardMary Manufacturing has four categories of overhead. The four categories and expected overhead costs for each category for next year are listed below: Maintenance 200,000.00 Material handling 32,000.00 Setups 100,000.00 Inspection 120,000.00 Currently, overhead is applied using a predetermined overhead rate, based on 80% of direct labor. The company has been asked to submit a bid for a proposed job. The plant manager feels that getting this job would result in new business in future years. Bids are based on full manufacturing cost plus 20 percent. Estimates for the proposed job are as follows: Direct materials 6,000.00 Direct labor (1k hours) 10,000.00 No. of materials moves 12.00 No. of inspections 10.00 No. of setups 2.00 No. of machine hours 500.00 In the past, full manufacturing cost has been calculated using normal costing. The plant manager has heard of a new way of applying overhead that…arrow_forward

- Carla Vista Limited is a company that produces machinery to customer orders, using a normal job-order cost system. It applies manufacturing overhead to production using a predetermined rate. This overhead rate is set at the beginning of each fiscal year by forecasting the year's overhead and relating it to direct labour costs. The budget for 2022 was as follows: Direct labour Manufacturing overhead $1,804,000 902,000 As at the end of the year, two jobs were incomplete. These were 1768B, with total direct labour charges of $113,600, and 1819C, with total direct labour charges of $390,100. Machine hours were 287 hours for 17688 and 647 hours for 1819C. Direct materials issued for 1768B amounted to $220,000, and for 1819C they amounted to $420,500. Total charges to the Manufacturing Overhead Control account for the year were $898,500, and direct labour charges made to all jobs amounted to $1,583,600, representing 247,500 direct labour hours. There were no beginning inventories. In…arrow_forwardXYZ Corporation has provided the following data concerning its overhead costs for the coming year: Wages and salaries Depreciation Rent Total The company has an activity-based costing system with the following three activity cost pools and estimated activity for the coming year: Activity Cost Pool Assembly Order processing Other Wages and salaries Depreciation $ 420,000 160,000 180,000 $760,000 Not Rent Total Activity 40,000 labor-hours 700 orders The Other activity cost pool does not have a measure of activity; it is used to accumulate costs of idle capacity and organization-sustaining costs. The distribution of resource consumption across activity cost pools is given below: applicable Assembly 35% 15% 35% Activity Cost Pools Order Processing 30% 45% 30% The activity rate for the Order Processing activity cost pool is closest to: Other 35% 40% 35% Total 100% 100% 100%arrow_forwardThe management of Garn Corporation would like to investigate the possibility of basing its predetermined overhead rate on activity at capacity rather than on the estimated activity for the coming year. The Corporation's controller has provided an example to illustrate how this new system would work. In this example, the allocation base is machine-hours and the estimated activity for the upcoming year is 69,000 machine-hours. Capacity is 85,000 machine-hours. AlIl of the manufacturing overhead is fixed and is $4,105,500 per year within the range of 69,000 to 85,000 machine-hours. If the Corporation bases its predetermined overhead rate on capacity but the actual level of activity for the year turns out to be 69,700 machine-hours, the cost of unused capacity shown on the income statement prepared for internal management purposes would be closest to: Multiple Choice $772,800 $780,640 $738,990 $41,650arrow_forward

- Blossom Limited is a company that produces machinery to customer orders, using a normal job-order cost system. It applies manufacturing overhead to production using a predetermined rate. This overhead rate is set at the beginning of each fiscal year by forecasting the year’s overhead and relating it to direct labour costs. The budget for 2022 was as follows: Direct labour $1,800,000 Manufacturing overhead 900,000 As at the end of the year, two jobs were incomplete. These were 1768B, with total direct labour charges of $110,000, and 1819C, with total direct labour charges of $390,000. Machine hours were 287 hours for 1768B and 647 hours for 1819C. Direct materials issued for 1768B amounted to $220,000, and for 1819C they amounted to $420,000.Total charges to the Manufacturing Overhead Control account for the year were $897,000, and direct labour charges made to all jobs amounted to $1,573,600, representing 247,200 direct labour hours.There were no beginning inventories. In…arrow_forwardCrane Limited is a company that produces machinery to customer orders, using a normal job-order cost system. It applies manufacturing overhead to production using a predetermined rate. This overhead rate is set at the beginning of each fiscal year by forecasting the year's overhead and relating it to direct labour costs. The budget for 2022 was as follows: Direct labour Manufacturing overhead $1,810,000 As at the end of the year, two jobs were incomplete. These were 1768B, with total direct labour charges of $111,000, and 1819C, with total direct labour charges of $390,800. Machine hours were 287 hours for 1768B and 647 hours for 1819C. Direct materials issued for 1768B amounted to $229,000, and for 1819C they amounted to $420,200. 905,000 Total charges to the Manufacturing Overhead Control account for the year were $902,500, and direct labour charges made to all jobs amounted to $1,582,600, representing 247,800 direct labour hours. There were no beginning inventories. In addition to…arrow_forwardWhen setting its predetermined overhead application race, Tasty Box Meals estimated its overhead would be $100,000 and would require 25,000 machine hours in the next year. At the end of the year. It found that actual overhead was $102,000 and required 26,000 machine hours. Determine the predetermined overhead rate. What is the overhead applied during the year? Prepare the journal entry to eliminate the under applied or over applied overhead.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Financial And Managerial Accounting

Accounting

ISBN:9781337902663

Author:WARREN, Carl S.

Publisher:Cengage Learning,

Managerial Accounting

Accounting

ISBN:9781337912020

Author:Carl Warren, Ph.d. Cma William B. Tayler

Publisher:South-Western College Pub

Cornerstones of Cost Management (Cornerstones Ser...

Accounting

ISBN:9781305970663

Author:Don R. Hansen, Maryanne M. Mowen

Publisher:Cengage Learning

Principles of Accounting Volume 2

Accounting

ISBN:9781947172609

Author:OpenStax

Publisher:OpenStax College

What is Cost Allocation? Definition & Process; Author: FloQast;https://www.youtube.com/watch?v=hLhvvHvZ3JM;License: Standard Youtube License