Videos

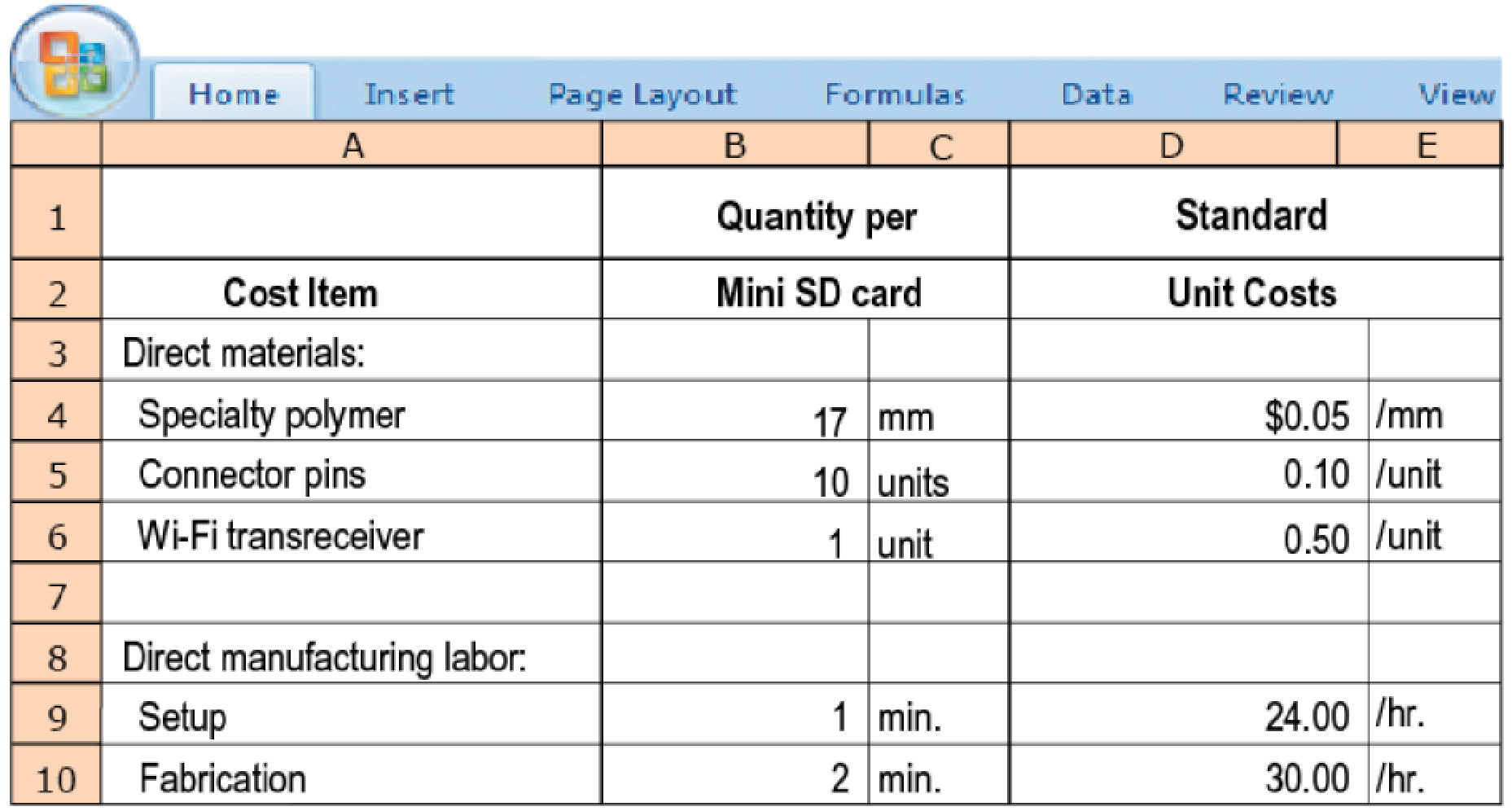

Direct-cost and selling price variances. MicroDisk is the market leader in the Secure Digital (SD) card industry and sells memory cards for use in portable devices such as mobile phones, tablets, and digital cameras. Its most popular card is the Mini SD, which it sells through outlets such as Target and Walmart for an average selling price of $8. MicroDisk has a standard monthly production level of 420,000 Mini SDs in its Taiwan facility. The standard input quantities and prices for direct-cost inputs are as follows:

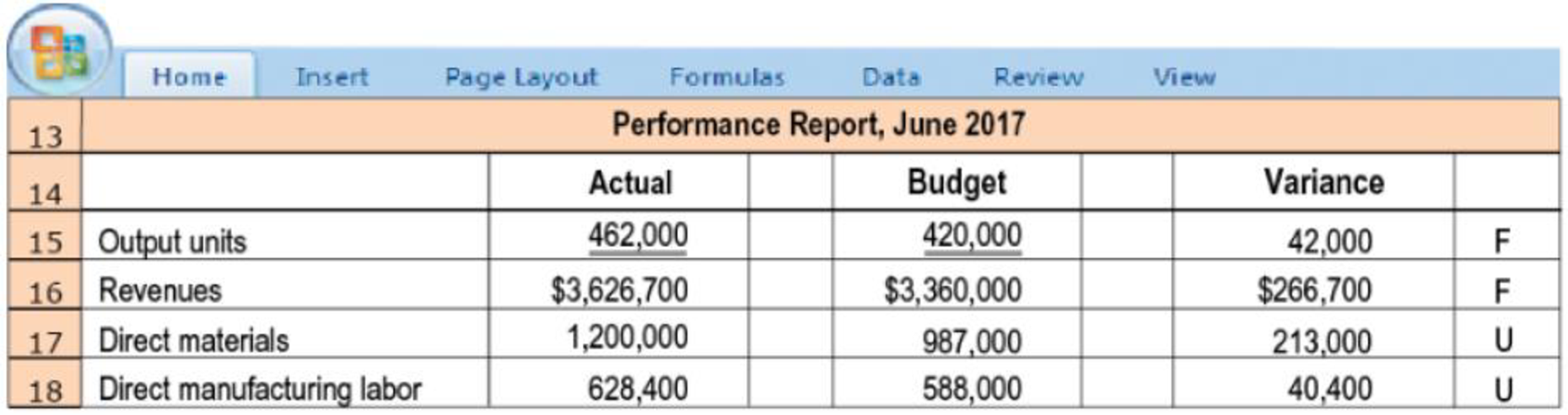

Phoebe King, the CEO, is disappointed with the results for June 2017, especially in comparison to her expectations based on the

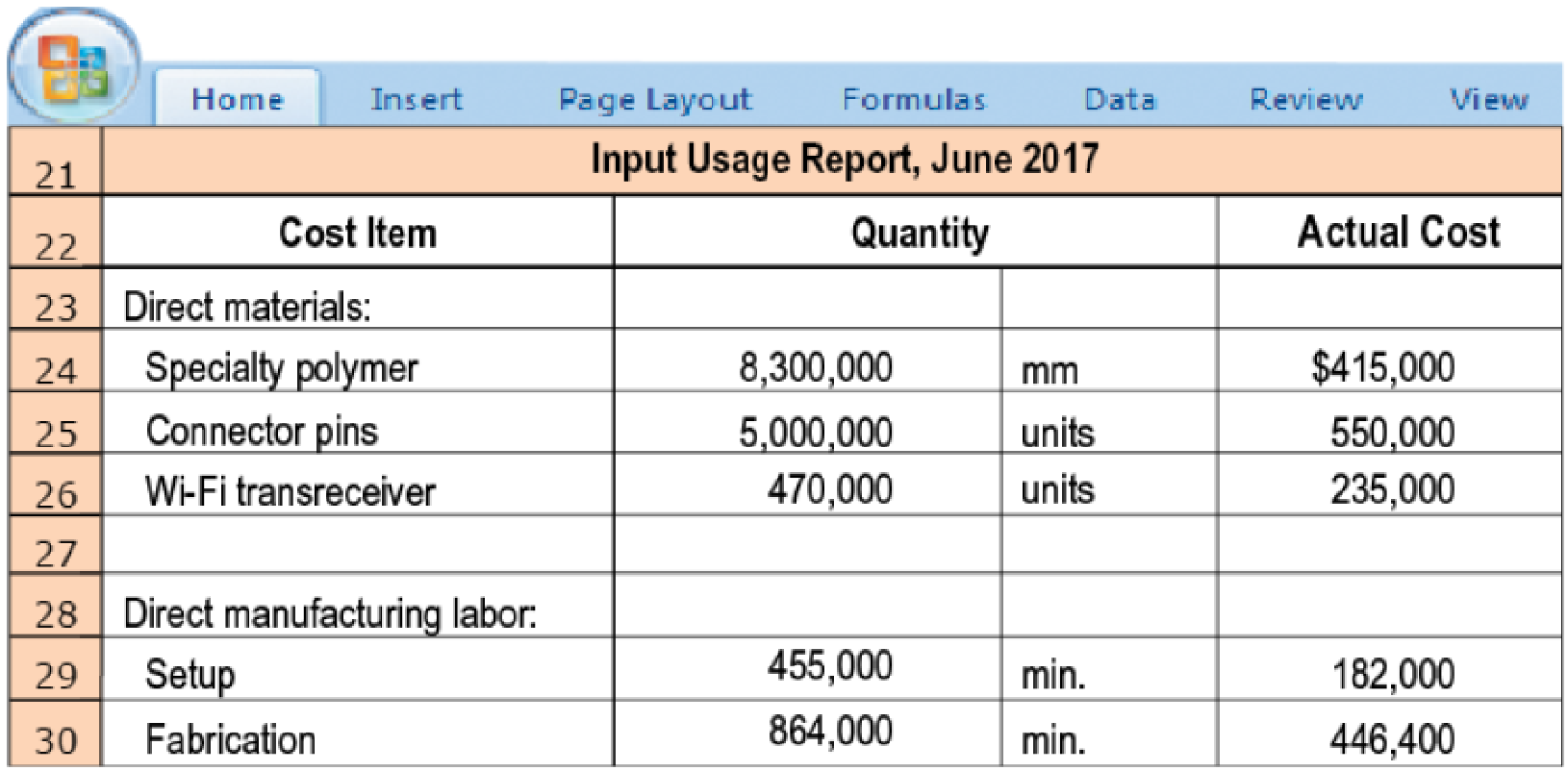

King observes that despite the significant increase in the output of Mini SDs in June, the product’s contribution to the company’s profitability has been lower than expected. She gathers the following information to help analyze the situation:

Calculate the following variances. Comment on the variances and provide potential reasons why they might have arisen, with particular attention to the variances that may be related to one another:

- 1. Selling-price variance

- 2. Direct materials price variance, for each category of materials

- 3. Direct materials efficiency variance, for each category of materials

- 4. Direct manufacturing labor price variance, for setup and fabrication

- 5. Direct manufacturing labor efficiency variance, for setup and fabrication

Want to see the full answer?

Check out a sample textbook solution

Chapter 7 Solutions

COST ACCOUNTING TTU >IC<

- Uchdorf Manufacturing just completed a study of its purchasing activity with the objective of improving its efficiency. The driver for the activity is number of purchase orders. The following data pertain to the activity for the most recent year: Activity supply: five purchasing agents capable of processing 2,400 orders per year (12,000 orders) Purchasing agent cost (salary): 45,600 per year Actual usage: 10,600 orders per year Value-added quantity: 7,000 orders per year Required: 1. Calculate the volume variance and explain its significance. 2. Calculate the unused capacity variance and explain its use. 3. What if the actual usage drops to 9,000 orders? What effect will this have on capacity management? What will be the level of spending reduction if the value-added standard is met?arrow_forwardThe production cost for UV protective sunglasses is $5.50 per unit and fixed costs are $19,400 per month. How much is the favorable or unfavorable variance if 14,000 units were produced for a total of $97,000?arrow_forwardLowell Manufacturing Inc. has a normal selling price of 20 per unit and has been selling 125,000 units per month. In November, Lowell Manufacturing decided to lower its price to 19 per unit expecting it can increase the units sold by 16%. a. Compute the normal revenue with a 20 selling price. b. Compute the planned revenue with a 19 selling price. c. Compute the actual revenue for November, assuming 135,000 units were sold in November at 19 per unit. d. Compute the revenue price variance, assuming 135,000 units were sold in November at 19 per unit. e. Compute the revenue volume variance, assuming 135,000 units were sold in November at 19 per unit. f. Analyze and interpret the lowering of the price to 19.arrow_forward

- Ed Co. manufactures two types of O rings, large and small. Both rings use the same material but require different amounts. Standard materials for both are shown. At the beginning of the month, Edve Co. bought 25,000 feet of rubber for $6.875. The company made 3,000 large O rings and 4,000 small O rings. The company used 14,500 feet of rubber. A. What are the direct materials price variance, the direct materials quantity variance, and the total direct materials cost variance? B. If they bought 10,000 connectors costing $310, what would the direct materials price variance be for the connectors? C. If there was an unfavorable direct materials price variance of $125, how much did they pay per toot for the rubber?arrow_forwardPrice and efficiency variances, benchmarking. Nantucket Enterprises manufactures insulated cold beverage cups printed with college and corporate logos, which it distributes nationally in lots of 12 dozen cups. In June 2017, Nantucket produced 5,000 lots of its most popular line of cups, the 24-ounce lidded tumbler, at each of its two plants, which are located in Providence and Amherst. The production manager, Shannon Bryant, asks her assistant, Joel Hudson, to nd out the precise per-unit budgeted variable costs at the two plants and the variable costs of a competitor, Beverage Mate, who offers similar-quality tumblers at cheaper prices. Hudson pulls together the following information for each lot:arrow_forwardCompuWorld sells two products, R66 and R100, and calculates sales variances using the CM. Info for the current year: Budgeted Actual R66 R100 R66 R-100 Selling Price $50 $160 $55 $155 VC per unit $40 $90 $43 $95 CM $10 $70 $12 $60 FC per unit $6 $30 $5 $25 Op Income $4 $40 $7 $35 Sales in units 1,200 400 1,000 1,000. What is R100 Sales Mix Variance? What is total sales volume variance? What is the R66 sales quantity variance?arrow_forward

- witter Company manufactures a remote control device for home theaters. The following data were from the operating period just completed: Actual market size (units) 21,000 Budgeted market size (units) 20,000 Actual market share 10 % Budgeted market share 7 % Budgeted selling price per unit $ 46 Actual selling price per unit $ 41 Budgeted variable cost per unit $ 21 Actual variable cost per unit $ 9 What is the firm's market size variance? Multiple Choice $1,750 favorable. $590 favorable. $3,700 favorable. $4,150 favorable. $4,450 favorable.arrow_forwardCT Co uses a standard absorption costing system and manufactures and sells a single product called the DG. The standards cost and selling price details for the DG are as follows. $ per unit Variable cost 12 Fixed cost 4 16 Standard profit 6 Standard selling price 22 The sales volume variance reported in June was $12,000 adverse. CT Co is considering using standard marginal costing as the basis for variance reporting in the future. (a) Calculate the sales volume variance that would be shown in a marginal costing operating statement for June.arrow_forwardWestern Company manufactures remote control devices for garage doors. The following information was collected during June: Actual market size (units) 10,000 Actual market share 32% Actual average selling price $10 Budgeted market size (units) 11,000 Budgeted market share 30% Budgeted average selling price $11 Budgeted contribution margin per composite unit for budgeted mix $5 What is the Western Company's sales-quantity variance?arrow_forward

- John Cush is a producer of knitted cricket jumpers. His most popular selling line is called the 'Billy Jean' and due to England's recent cricket success he has benefitted from an increase in sales in this product. After a successful year in terms of sales he has been informed by his accountant that he has made a loss. He has asked the accountant to investigate the variances as a matter of urgency.The budget for the previous year was as follows:Selling price per jumper - £70Material to produce one jumper - 3 metres of wool at £7 per metre.Labour to produce one jumper - 2 hours at £15 per hourVariable overheads - £3 per direct labour hour.Fixed overheads budget was £15,000The budget was to produce and sell 2,000 jumpers in the year.The actual information for the year is as follows:Production of jumpers totalled 3,000 units and all were sold for £216,000. Purchases of wool totalled 10,500 metres costing £84,000.A total of 7,500 hours of labour was worked, costing £112,500. Variable…arrow_forwardJohn Cush is a producer of knitted cricket jumpers. His most popular selling line is called the 'Billy Jean’ and due to England's recent cricket success he has benefitted from an increase in sales in this product. After a successful year in terms of sales he has been informed by his accountant that he has made a loss. He has asked the accountant to investigate the variances as a matter of urgency. The budget for the previous year was as follows: Selling price per jumper - £70Material to produce one jumper – 3 metres of wool at £7 per metre. Labour to produce one jumper – 2 hours at £15 per hourVariable overheads - £3 per direct labour hour.Fixed overheads budget was £15,000The budget was to produce and sell 2,000 jumpers in the year. The actual information for the year is as follows: Production of jumpers totalled 3,000 units and all were sold for £216,000. Purchases of wool totalled 10,500 metres costing £84,000.A total of 7,500 hours of labour was worked, costing £112,500.Variable…arrow_forwardScandia Scandia produces a product with three different levels of quality (deluxe, standard and basic). The budget for October showed the following; Deluxe Standard Basic Selling price (£) 10 6 4 Variable costs (£) 5 4 3 Sales volume 3,000 6,000 1,000 Actual results were: Deluxe Standard Basic Selling price (£) 9 7 4 Variable costs (£) 5 4 3 Sales volume 4,000 6,500 500 Calculate the individual sales price variances and sales volume variances and then split the volume variances into a sales mix and quantity variance.arrow_forward

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning