CORPORATE FINANCE-ACCESS >CUSTOM<

11th Edition

ISBN: 9781260170016

Author: Ross

Publisher: MCG CUSTOM

expand_more

expand_more

format_list_bulleted

Concept explainers

Videos

Textbook Question

Chapter 8, Problem 13CQ

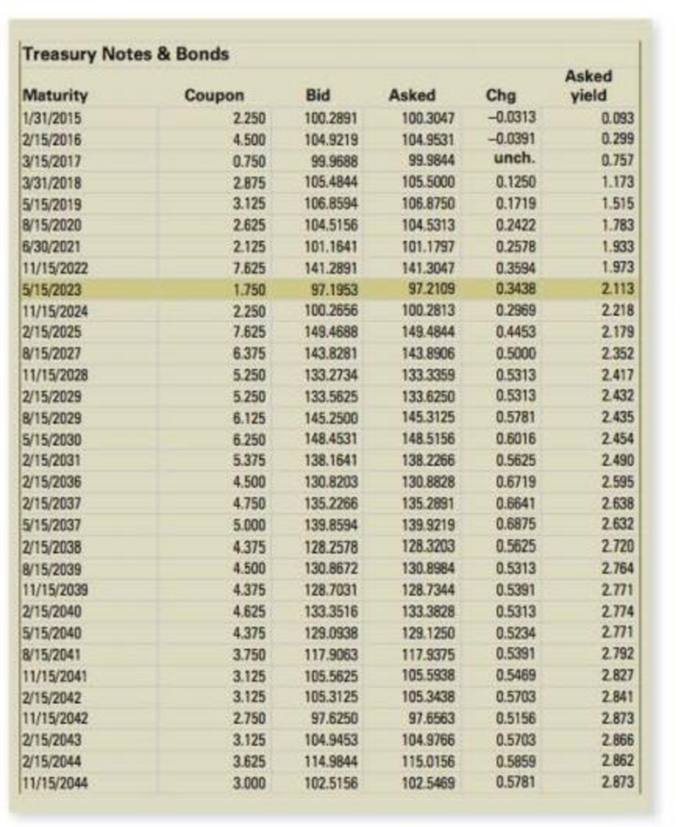

Treasury Market Take a look back at Figure 8.4. Notice the wide range of coupon rates. Why are they so different?

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Students have asked these similar questions

An investment Analysist provide the following data regarding the possible future returns on AmDa’s common stock

State of economy Probability ReturnRecession 0.25 -1.4%Normal 0.45 9.4%Boom 0.30 15.4%i. Compute the expected return on the security?

ii. Compute the standard deviation on the security?

iii. Compute the Coefficient of variation

Consider an economy with just two assets. The details of these are given below.

Number of Shares

Price

Expected Return

Standard Deviation

A

100

1.5

15

15

B

150

2

12

9

The correlation coefficient between the returns on the two assets is 1=3 and

there is also a risk-free asset. Assume the CAPM model is satisfied.

(1) What is the expected rate of return on the market portfolio?

(2) What is the standard deviation of the market portfolio?

(3) What is the beta of stock A?

(4) What is the risk-free rate of return?

What can you tell just by looking at the above yield curve?

Group of answer choices

An expectation of falling interest rates suggests trouble in the economy, a rise in bond prices, and a decline for stocks.

The economy is expected to do well in the short-run.

A correction in bond prices is expected.

Bond prices are expected to decline and so the stock market should do extremely well.

Chapter 8 Solutions

CORPORATE FINANCE-ACCESS >CUSTOM<

Ch. 8 - Prob. 1CQCh. 8 - Prob. 2CQCh. 8 - Prob. 3CQCh. 8 - Yield to Maturity Treasury bid and ask quotes are...Ch. 8 - Coupon Rate How does a bond issuer decide on the...Ch. 8 - Real and Nominal Returns Are there any...Ch. 8 - Prob. 7CQCh. 8 - Prob. 8CQCh. 8 - Term Structure What is the difference between the...Ch. 8 - Crossover Bonds Looking back at the crossover...

Ch. 8 - Municipal Bonds Why is it that municipal bonds are...Ch. 8 - Prob. 12CQCh. 8 - Treasury Market Take a look back at Figure 8.4....Ch. 8 - Prob. 14CQCh. 8 - Bonds as Equity The 100-year bonds we discussed in...Ch. 8 - Bond Prices versus Yields a. What is the...Ch. 8 - Interest Rate Risk All else being the same, which...Ch. 8 - Valuing Bonds What is the price of a 15-year, zero...Ch. 8 - Valuing Bonds Microhard has issued a bond with the...Ch. 8 - Prob. 3QPCh. 8 - Coupon Rates Rhiannon Corporation has bonds on the...Ch. 8 - Valuing Bonds Even though most corporate bonds in...Ch. 8 - Prob. 6QPCh. 8 - Zero Coupon Bonds You find a zero coupon bond with...Ch. 8 - Valuing Bonds Yan Yan Corp. has a 2,000 par value...Ch. 8 - Prob. 9QPCh. 8 - Prob. 10QPCh. 8 - Inflation and Nominal Returns Suppose the real...Ch. 8 - Prob. 12QPCh. 8 - Prob. 13QPCh. 8 - Prob. 14QPCh. 8 - Prob. 15QPCh. 8 - Prob. 16QPCh. 8 - Bond Price Movements Miller Corporation has a...Ch. 8 - Interest Rate Risk Laurel, Inc., and Hardy Corp....Ch. 8 - Interest Rate Risk The Faulk Corp. has a 6 percent...Ch. 8 - Bond Yields Hacker Software has 6.2 percent coupon...Ch. 8 - Prob. 21QPCh. 8 - Prob. 22QPCh. 8 - Prob. 23QPCh. 8 - Prob. 24QPCh. 8 - Prob. 25QPCh. 8 - Prob. 26QPCh. 8 - Prob. 27QPCh. 8 - Prob. 28QPCh. 8 - Prob. 29QPCh. 8 - Holding Period Yield The YTM on a bond is the...Ch. 8 - Prob. 31QPCh. 8 - Prob. 32QPCh. 8 - Prob. 33QPCh. 8 - Prob. 34QPCh. 8 - Real Cash Flows Paul Adams owns a health club in...Ch. 8 - FINANCING EAST COAST YACHTS'S EXPANSION PLANS WITH...Ch. 8 - Prob. 2MCCh. 8 - Prob. 3MCCh. 8 - Prob. 4MCCh. 8 - Prob. 5MCCh. 8 - Are investors really made whole with a make-whole...Ch. 8 - After considering all the relevant factors, would...

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- Suppose that many stocks are traded in the market and that it is possible to borrow at the risk-free rate, Rf. The characteristics of two of the stocks are as follows: Stock Expected ret Standard dev A 8% 40% B 13% 60% Correlation = -1 Could the equilibrium risk-free rate be greater than 10%? (HINT: Can a particular stock portfolio be substituted for the risk-free rate?)arrow_forwardIf the YTM is less than the coupon rate, wouldn't the bond price be higher?arrow_forwardAn investor is evaluating the common share of Bulldogs Inc. which has a beta of 1.8. The expected return for the securities market as a whole is 8%. The risk-free rate on a treasury bill is 2%. Based on the capital asset pricing model, what is the expected risk adjusted return of the Bulldogs Inc.’s common share?arrow_forward

- Suppose that the Treasury bill rate is 6% rather than 3%, as we assumed in Table 12.1, and the expected return on the market is 9%. Use the betas in that table to answer the following questions. a. When you assume this higher risk-free interest rate, what makes sense for how you should modify your assumption about the rate of return on the market portfolio? (Do not round intermediate calculations. Enter your answer as a percent rounded to 1 decimal place.) b. Recalculate the expected return on the stocks in Table 12.1. (Do not round intermediate calculations. Enter your answer as a percent rounded to 1 decimal place.) c. Suppose now that you continued to assume that the expected return on the market remained at 9%. Now what would be the expected returns on each stock? (Do not round intermediate calculations. Enter your answer as a percent rounded to 1 decimal place.)d. Ford offer a higher or lower expected return if the interest rate is 6% rather than 3%? e. Walmart offer a higher or…arrow_forwardExploring Finance: The Security Market Line and Inflation Changes Security Market Line: Inflation Changes Conceptual Overview: Explore how inflation changes the security market line. The Security Market Line defines the required rate of return for a security to be worth buying or holding. The line, depicted in blue in the graph, is the sum of the risk-free return (rf in the slider) and a risk premium determined by the market-risk premium (RPM) multiplied by the security's beta coefficient for risk. Drag the slider below the graph to change the amount of the risk-free return. These changes reflect changes in inflation. Drag left or right on the graph to move the cursor to evaluate securities with different beta coefficients. In this graph, the market-risk premium is fixed at 5%. r = r_{RF} + RP_M * beta = 6\% + 5\% * 1 = 6\% + 5.00\% = 11.00\%r=rRF+RPM∗beta=6%+5%∗1=6%+5.00%=11.00% 1. If the risk-free return were 4.0% and a security's beta coefficient were 2.0, what would be…arrow_forwardUsing the CAPM theory, if the Volatility of a stock is twice as great as the market, the market return on stocks in general (using the S&P 500 as a proxy) is 12 %, and treasury bills are yielding 2%, what is the return that investors in that security can expect? 12% 16% 20% 22%arrow_forward

- Suppose that there are many stocks in the security market and that the characteristics of stocks A and B are given as follows: Stock Expected Return Standard Deviation A 12 % 4 % B 19 12 Correlation = –1 Suppose that it is possible to borrow at the risk-free rate, rf. What must be the value of the risk-free rate? (Hint: Think about constructing a risk-free portfolio from stocks A and B.)arrow_forwardSuppose you observe the following situation on two securities:Security Beta Expected Return Pete Corp. 0.8 0.12 Repete Corp. 1.1 0.16 Assume these two securities are correctly priced. Based on the CAPM, what is the return on the market?arrow_forwardAssume that Temp Force has a beta coefficient of 1.2, that the risk-free rate (the yield on T-bonds) is 7.0%, and that the market risk premium is 5%. What is the required rate of return on the firms stock?arrow_forward

- In Chapter 7, we saw that if the market interest rate, rd, for a given bond increased, the price of the bond would decline. Applying this same logic to stocks, explain (a) how a decrease in risk aversion would affect stocks prices and earned rates of return, (b) how this would affect risk premiums as measured by the historical difference between returns on stocks and returns on bonds, and (c) what the implications of this would be for the use of historical risk premiums when applying the SML equation.arrow_forwardMarket equity beta measures the covariability of a firms returns with all shares traded on the market (in excess of the risk-free interest rate). We refer to the degree of covariability as systematic risk. The market prices securities so that the expected returns should compensate the investor for the systematic risk of a particular stock. Stocks carrying a market equity beta of 1.20 should generate a higher return than stocks carrying a market equity beta of 0.90. Nonsystematic risk is any source of risk that does not affect the covariability of a firms returns with the market. Some writers refer to nonsystematic risk as firm-specific risk. Why is the characterization of nonsystematic risk as firm-specific risk a misnomer?arrow_forwardWhat is the connection between the interest rate and the price of a fixed coupon bond? Why is this relationship still going strong?arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning

Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT

EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT Fundamentals of Financial Management, Concise Edi...FinanceISBN:9781285065137Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management, Concise Edi...FinanceISBN:9781285065137Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Fundamentals Of Financial Management, Concise Edi...FinanceISBN:9781337902571Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals Of Financial Management, Concise Edi...FinanceISBN:9781337902571Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Fundamentals of Financial Management, Concise Edi...FinanceISBN:9781305635937Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management, Concise Edi...FinanceISBN:9781305635937Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Intermediate Financial Management (MindTap Course...

Finance

ISBN:9781337395083

Author:Eugene F. Brigham, Phillip R. Daves

Publisher:Cengage Learning

EBK CONTEMPORARY FINANCIAL MANAGEMENT

Finance

ISBN:9781337514835

Author:MOYER

Publisher:CENGAGE LEARNING - CONSIGNMENT

Fundamentals of Financial Management, Concise Edi...

Finance

ISBN:9781285065137

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Fundamentals Of Financial Management, Concise Edi...

Finance

ISBN:9781337902571

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Fundamentals of Financial Management, Concise Edi...

Finance

ISBN:9781305635937

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Portfolio return, variance, standard deviation; Author: MyFinanceTeacher;https://www.youtube.com/watch?v=RWT0kx36vZE;License: Standard YouTube License, CC-BY