Videos

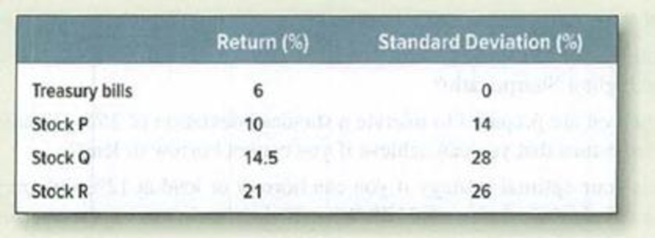

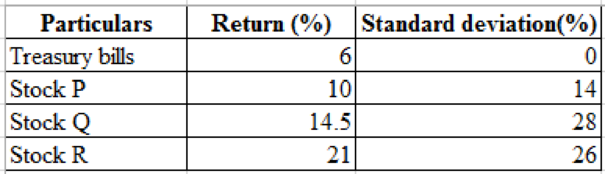

Portfolio risk and return* Here are returns and standard deviations for four investments.

Calculate the standard deviations of (the following portfolios.

- a. 50% in Treasury bills, 50% in stock P.

- b. 50% each in Q and R, assuming the shares have

- • Perfect positive correlation.

- • Perfect negative correlation.

- • No correlation.

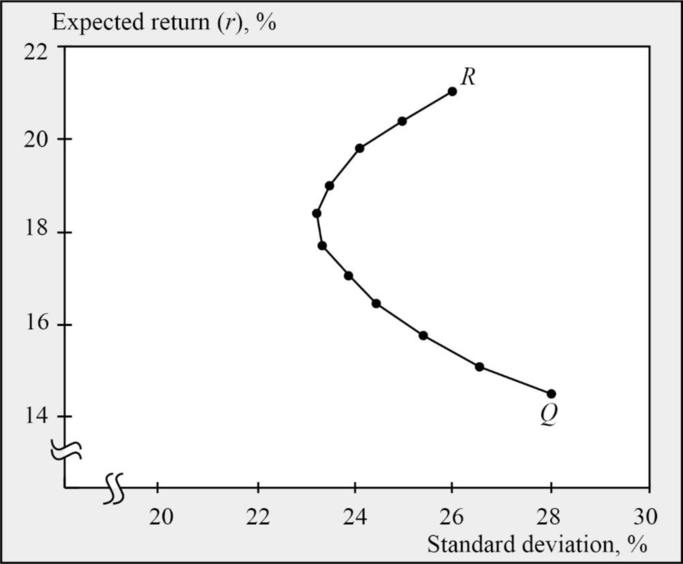

- c. Plot a figure like Figure 8.3 for Q and R, assuming a correlation coefficient of .5.

- d. Stock Q has a lower return than R but a higher standard deviation. Does that mean that Q’s price is too high or that R’s price is too low?

a)

To determine: Standard deviation of 50% Treasury bills and 50% in stock P.

Explanation of Solution

Given information:

Calculation of standard deviation:

Therefore, the standard deviation is 7%

b)

To determine: Standard deviation of 50% each in Q and R in the following situations.

Explanation of Solution

With a perfect positive correlation:

Therefore, the standard deviation in a perfect positive correlation is 27%

With a perfect negative correlation:

Therefore, the standard deviation in a perfect positive correlation is 1%

With no correlation:

Therefore, the standard deviation in a perfect positive correlation is 19.1%

c)

To graph: Figure showing the stocks of Q and R by assuming a correlation coefficient of 0.5

Explanation of Solution

d)

To discuss: If Q has a low return than R but with a higher standard deviation whether this mean that price of Q’s stock is too high or price of R’s stock is too low.

Explanation of Solution

When stock Q has lower return that stock R but, higher standard deviation, thus this doesn’t mean that price of Q’s stock is too high or price of R’s stock is too low. Because the risk factor is measured by beta not by the standard deviation.

Standard deviation measures the total risk whereas, beta measures non-diversifiable risk and inventors are solely compensated with a risk premium in holding the non-diversifiable risk.

Want to see more full solutions like this?

Chapter 8 Solutions

International Edition---principles Of Corporate Finance, 12th Edition

- Two-Asset Portfolio Stock A has an expected return of 12% and a standard deviation of 40%. Stock B has an expected return of 18% and a standard deviation of 60%. The correlation coefficient between Stocks A and B is 0.2. What are the expected return and standard deviation of a portfolio invested 30% in Stock A and 70% in Stock B?arrow_forwardYou have observed the following returns over time: Assume that the risk-free rate is 6% and the market risk premium is 5%. What are the betas of Stocks X and Y? What are the required rates of return on Stocks X and Y? What is the required rate of return on a portfolio consisting of 80% of Stock X and 20% of Stock Y?arrow_forwardThe standard deviation of stock returns for Stock A is 40%. The standard deviation of the market return is 20%. If the correlation between Stock A and the market is 0.70, then what is Stock A’s beta?arrow_forward

EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT

EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT

Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning

Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning