Videos

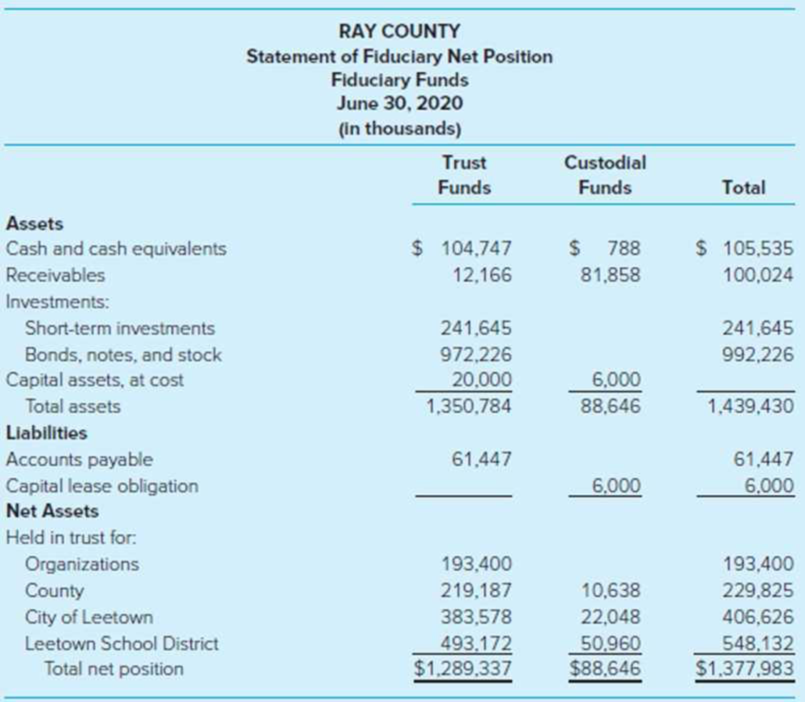

Fiduciary Financial Statements. (LO8-4) Ray County administers a tax custodial fund, an investment trust fund, and a private-purpose trust fund. The tax custodial fund acts as custodian for the county, a city within the county, and the school district within the county. Participants in the investment trust fund are the Ray County General Fund, the city, and the school district. The private-purpose trust is maintained for the benefit of a private organization located within the county. Ray County has prepared the following statement of fiduciary net position.

Required

The statement as presented is not in accordance with GASB standards. Using Illustration A2–10 (recall that the City and County of Denver statements use agency rather than custodial given they were issued prior to the change in terminology) and Illustration 8–6 as examples, identify the errors (problems) in the statement and explain how the errors should be corrected.

Want to see the full answer?

Check out a sample textbook solution

Chapter 8 Solutions

ACCOUNTING F/GOV.+..(LL)-W/CODE>CUSTOM<

- Required information [The following information applies to the questions displayed below.] The county collector of Sun County is responsible for collecting all property taxes levied by funds and governments within the boundaries of the county. To reimburse the county for estimated administrative expenses of operating the tax custodial fund, the custodial fund deducts 4 percent from the collections for the town, the school district, and the other towns. The total amount deducted is added to the collections for the county and remitted to the Sun County General Fund. The following events occurred during the year: 1. Current-year tax levies to be collected by the custodial fund were County General Fund Town of Bayshore Sun County Consolidated School District Total $10,473,000 4,910,000 6,620,000 $22,003,000 2. During the year, $13,840,000 of the current year's taxes was collected. 3. The 4 percent administrative collection fee was recorded. A schedule of amounts collected for each…arrow_forwardRequired information [The following information applies to the questions displayed below.] The county collector of Sun County is responsible for collecting all property taxes levied by funds and governments within the boundaries of the county. To reimburse the county for estimated administrative expenses of operating the tax custodial fund, the custodial fund deducts 4 percent from the collections for the town, the school district, and the other towns. The total amount deducted is added to the collections for the county and remitted to the Sun County General Fund. The following events occurred during the year: 1. Current-year tax levies to be collected by the custodial fund were County General Fund Town of Bayshore Sun County Consolidated School District Total $10,473,000 4,910,000 6,620,000 $22,003,000 2. During the year, $13,840,000 of the current year's taxes was collected. 3. The 4 percent administrative collection fee was recorded. A schedule of amounts collected for each…arrow_forwardWhich of the following is an example of activities that are likely to be accounted for in a government's general fund? a. sales taxes collected by a state on behalf of counties within the state b. donations that must be kept intact, but whose income must be used to beautify parks c. property taxes levied and collected. d. electricity utilities of government that are financed by user chargesarrow_forward

- Please help solve the below: see picture attached. The county collector of Sun County is responsible for collecting all property taxes levied by funds and governments within the boundaries of the county. To reimburse the county for estimated administrative expenses of operating the tax custodial fund, the custodial fund deducts 5 percent from the collections for the town, the school district, and the other towns. The total amount deducted is added to the collections for the county and remitted to the Sun County General Fund. The following events occurred during the year: Current-year tax levies to be collected by the custodial fund were County General Fund $ 10,443,000 Town of Bayshore 4,895,000 Sun County Consolidated School District 6,605,000 Total $ 21,943,000 During the year, $13,810,000 of the current year's taxes was collected. The 5 percent administrative collection fee was recorded. A schedule of amounts collected for…arrow_forwardThe city of Belle collects property taxes for other local governments—Beau County and the Landis Independent School District (LISD). The city uses a Property Tax Collection Custodial Fund to account for its collection of property taxes for itself, Beau County, and LISD.The following transactions and events occurred for Belle's Custodial Fund.1. Property taxes were levied for Belle ( $1,000,000), Beau County ( $500,000) andLISD ( $1,500,000). Assume taxes collected by the Custodial Fund will bepaid to Belle’s General Fund.2. Property taxes in the amount of $2,250,000 are collected. The percentage collectedfor each entity is in the same proportion as the original levy.3. The amounts owed to Beau County and LISD are recognized.4. The Custodial Fund distributes the amounts owed to the three governments.Prepare journal entries to record the above transactions and events for Belle’s Custodial Fund. If an entry affects more than one debit or credit account, enter the accounts in order of…arrow_forwardFor each of the following indicate the fund (or funds), if any, in which you think the activity should be accounted for and reported. If you think the fund should be a fiduciary fund, then indicate the type of fund; if a governmental or proprietary fund, then so state. Provide a brief explanation for your response. The Jackson School District holds all funds of the foundation that supports the Jackson High School football team. The foundation is governed by a board of advisors, the members of which are selected by a committee of other advisors. The District performs no administrative functions other than depositing the funds in a checking account and writing checks as directed by the foundation. Virginia State University requires that all cash collected by university‐sponsored clubs be held in university maintained accounts and that all disbursements be approved by the Assistant Dean of Students, consistent with policies and procedures established by the university. Using general…arrow_forward

- The city of Belle collects property taxes for other local governments—Beau County and the Landis Independent School District (LISD). The city uses a Property Tax Collection Custodial Fund to account for its collection of property taxes for itself, Beau County, and LISD. The following transactions and events occurred for Belle's Custodial Fund. 1. Property taxes were levied for Belle ( $1,500,000), Beau County ( $750,000) and LISD ( $2,250,000). Assume taxes collected by the Custodial Fund will be paid to Belle’s General Fund. 2. Property taxes in the amount of $3,375,000 are collected. The percentage collected for each entity is in the same proportion as the original levy. 3. The amounts owed to Beau County and LISD are recognized. 4. The Custodial Fund distributes the amounts owed to the three governments. Prepare journal entries to record the above transactions and events for Belle’s Custodial Fund. If an entry affects more than one debit or credit account, enter the accounts in…arrow_forwardChase City uses an internal service fund for its central motor pool. The assets and liabilities account balances for this fund that are not eliminated normally should be reported in the government-wide statement of net position as: Governmental activities. OBusiness-type activities. Fiduciary activities. Note disclosures only.arrow_forwardThe City of Sweetwater maintains in trust the Employees’ Retirement Fund, a single-employer defined benefit plan that provides annuity and disability benefits. The fund is financed by actuarially determined contributions from the city’s General Fund and by contributions from employees. Administration of the retirement fund is handled by General Fund employees, and the retirement fund does not bear any administrative expenses. The Statement of Fiduciary Net Position for the Employees’ Retirement Fund as of July 1, 2023, is shown here: CITY OF SWEETWATER Employees’ Retirement Fund Statement of Fiduciary Net Position As of July 1, 2023 Assets Cash $145,000 Accrued Interest Receivable 59,200 Investments, at Fair Value: Bonds 4,507,000 Common Stocks 1,313,000 Total Assets 6,024,200 Liabilities Accounts Payable and Accrued Expenses 384,000 Fiduciary Net Position Restricted for Pensions $5,640,200 During the year ended June 30, 2024, the following…arrow_forward

- Identification of activities with particular governmental-type funds Using only the governmental-type funds, indicate which would be used to record each of the following transactions and events. GF General Fund SRF Special Revenue Fund DSF Debt Service Fund CPF Capital Projects Fund PF Permanent Fund 1. Property taxes were received directly by the fund used to accumulate resources to pay bond principal and interest. 2. The city received its share of a state sales tax that is legally required to be used solely to finance library operations. 3. The city sent property tax bills to homeowners to help pay for day-to-day operating costs. 4. The city paid for five fire engines, using resources accumulated in a fund to pay for capital assets. 5. The city received a grant from the state to build an addition to the city hall. 6. The city received the proceeds of general obligation bonds to finance the construction of a new police station. 7. The mayor was paid his monthly…arrow_forwardProperty owners in the City of N e pay property taxes that are earmarked, in part, to provide debt service for the outstanding debt of the city. Property owners in the city also provide debt service support for a share of the outstanding debt of Center Township and Delaware County, proportionate to the ratio of the assessed valuation of property located within the city to that of all taxable property in the township and the county. The sum of the city's outstanding debt plus a proportionate share of the township and county's debt is referred to as: a. Total direct debt. b. Overlapping debt. c. Legal debt margin. d. Total general obligation debt outstanding. (ne)sarrow_forward1) State whether each of the following items should be classified as taxes, licences and permits, intergovernmental revenues, charges for services, fines and forfeits or miscellaneous revenue in a governmental fund. g) Charges to a local university for extra city police protection during sporting events. h) Barbers and hairdressers’ registration fees. i) Donation to government due to coronovirus. j) Parkingarrow_forward

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education