Concept explainers

Videos

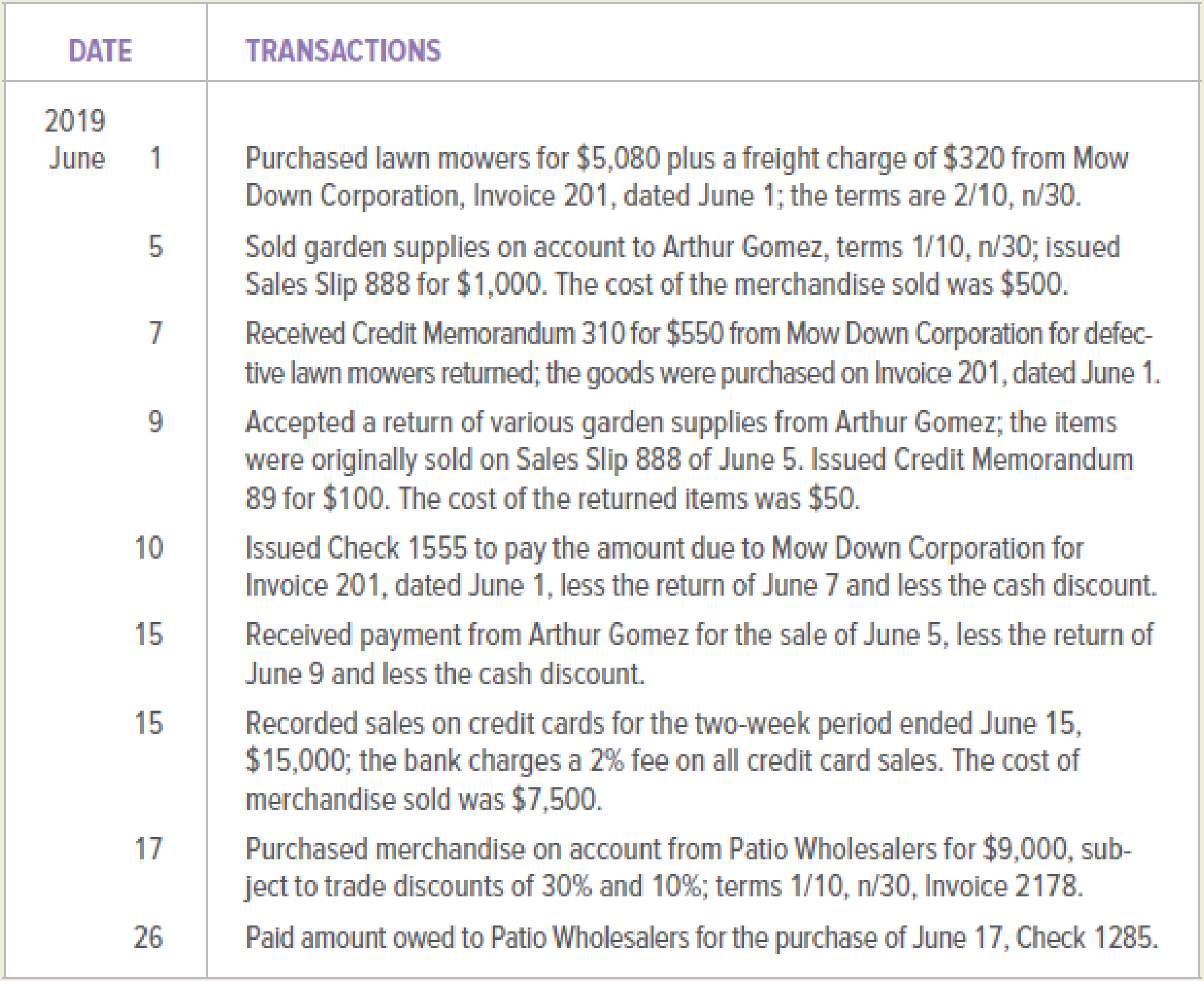

The following transactions took place at The Garden Center during June 2019. The Garden Center uses a perpetual inventory system. Record the transactions in a general journal. Use 10 as the page number for the general journal.

Analyze: Assume 20 lawn mowers were purchased from Mow Down Corporation on June 1. What was the average cost per lawn mower? (Hint: Include the freight charges as part of the cost of the lawn mowers.)

Post the transactions in the general journal using perpetual inventory system.

Explanation of Solution

Perpetual Inventory System:

The perpetual inventory systems are used for the management of the inventory which provides the latest information about inventory records. The transactions are recorded in inventory ledger correspondingly with each inventory purchase, inventory sale and inventory returns under the perpetual inventory system. The general ledger merchandise inventory account is also updated by the system.

The transactions are posted to general journal as follows:

Merchandise purchased on credit including freight charges:

| GENERAL JOURNAL | Page 10 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| June 1, 2019 | Merchandise inventory | 5,400 | ||

| Accounts payable/Company MDC | 5,400 | |||

| (to record the merchandise purchased on credit with 2/10, n/30 terms) | ||||

Table (1)

- • The merchandise inventory account is an asset account and the account balance is increasing. Therefore, it is debited. The freight charges are included within merchandise inventory account. No separate account is prepared for the freight charges under perpetual inventory system.

- • Accounts payable is liability and the account balance is increasing. Therefore, it is credited.

Recording of the merchandise sold:

| GENERAL JOURNAL | Page 10 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| June 5, 2019 | Accounts Receivable/ Company AG | 1000 | ||

| Sales | 1000 | |||

| (to record the merchandise sold on credit on terms 1/10,n/30) | ||||

Table (2)

- • The accounts receivables account is an asset account and the account balance is increasing. Therefore, the accounts receivables account is debited.

- • The sales account is credited. This because the sales account is identified as the revenue account and the revenue is generated from selling merchandise.

Recording of the cost of merchandise sold:

| GENERAL JOURNAL | Page 10 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| June 5, 2019 | Cost of goods sold | 500 | ||

| Merchandise inventory | 500 | |||

| (to record the cost of merchandise sold) | ||||

Table (3)

- • The cost of goods sold account is an expense account and the account balance is increasing. Therefore, the cost of goods sold account is debited.

- • The merchandise inventory account is an asset account and the account balance is increasing. Therefore, it is debited.

Record the receiving of credit memorandum and merchandise returned:

| GENERAL JOURNAL | Page 10 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| June 7, 2019 | Accounts payable/Company MDC | 550 | ||

| Merchandise inventory | 550 | |||

| (to record the merchandise returned and receiving credit memorandum) | ||||

Table (4)

- • Accounts payable is liability and the account balance is decreasing. Therefore, it is debited.

- • The merchandise inventory is an asset account and the account balance is decreasing. Therefore, its balance is credited.

Recording the returned merchandise sold and the credit memorandum:

| GENERAL JOURNAL | Page 10 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| June 9, 2019 | Sales returns and allowances | 100 | ||

| Accounts Receivable/ Company AG | 100 | |||

| (to record the merchandise returned plus sales tax) | ||||

Table (5)

- • The sales returns and allowances account is identified as contra revenue account with debit normal balance and increasing. Therefore, it is debited.

- • The account receivable account is an asset account and the account balance is decreasing. Therefore, the accounts payable account is credited.

Recording the cost of returned merchandise sold:

| GENERAL JOURNAL | Page 10 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| June 9, 2019 | Merchandise inventory | 50 | ||

| Cost of goods sold | 50 | |||

| (to record the cost of returned merchandise sold) | ||||

Table (6)

- • The merchandise inventory account is an asset account and the account balance is increasing. Therefore, it is debited.

- • The cost of goods sold is an expense account and the account balance is decreasing. Therefore, it is credited.

Recording the payment made with purchase discount:

| GENERAL JOURNAL | Page 10 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| June 10, 2019 | Accounts payable/Company MDC | 4,850 | ||

| Merchandise inventory | 90.6 | |||

| Cash | 4,759.4 | |||

| (to record the payment made and taking purchase discount ) | ||||

Table (7)

- • The accounts payable is liability and the account balance is decreasing. Therefore, accounts payable account is debited. The amount in accounts payable accounts is calculated after subtracting the purchase returns amount.

- • The purchase discount is received of the payment made and there is reduction is merchandise purchases cost. Therefore, merchandise inventory account is credited.

- • The cash account is an asset account and the account balance is decreasing. Therefore, it is credited.

Recording the payment received from the accounts receivable:

| GENERAL JOURNAL | Page 10 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| June 15, 2019 | Sales discount | 9 | ||

| Cash | 891 | |||

| Accounts Receivable/Company AG | 900 | |||

| (to record the payment received from the account receivable) |

Table (8)

- • The sales discount account is identified as contra revenue account and it has debit normal balance which is increasing. Therefore, it is debited.

- • The cash account is an asset account and the account balance is increasing. Therefore, the cash account is debited.

- • The accounts receivable account is asset account and the account balance is decreasing. Therefore, it is credited.

Recording of the merchandise sold using credit card:

| GENERAL JOURNAL | Page 10 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| June 15, 2019 | Credit card expense | 300 | ||

| Cash | 14,700 | |||

| Sales | 15,000 | |||

| (to record the merchandise sold on credit) | ||||

Table (9)

- • The credit card expense is the expense account which has normal debit balance. The balance is increasing. Therefore, it is debited.

- • The cash account is an asset account and the account balance is increasing. Therefore, the cash account is debited.

- • The sales account is identified as the revenue account and the revenue is generated from selling merchandise. Therefore, sales account is credited.

Recording of the cost of merchandise sold:

| GENERAL JOURNAL | Page 10 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| June 15, 2019 | Cost of goods sold | 7,500 | ||

| Merchandise inventory | 7,500 | |||

| (to record the cost of merchandise sold) | ||||

Table (10)

- • The cost of goods sold account is an expense account and the account balance is increasing. Therefore, the cost of goods sold account is debited.

- • The merchandise inventory account is an asset account and the account balance is decreasing. Therefore, it is credited.

Recording the purchases on credit:

| GENERAL JOURNAL | Page 10 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| June 17, 2019 | Merchandise inventory | 5,670 | ||

| Accounts payable/Company PW | 5,670 | |||

| (to record the inventory purchased on account with terms 1/10,n/30) | ||||

Table (11)

- • The merchandise inventory account is an asset account and the account balance is increasing. Therefore, it is debited.

- • Accounts payable is liability and account balance is increasing. Therefore, it is credited.

Recording the payment made with purchase discount:

| GENERAL JOURNAL | Page 10 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| June 26, 2019 | Accounts payable/Company PW | 5,670 | ||

| Merchandise inventory | 56.7 | |||

| Cash | 5,613.3 | |||

| (to record the payment made and taking purchase discount ) | ||||

Table (12)

- • The accounts payable is liability and the account balance is decreasing. Therefore, accounts payable account is debited. The amount in accounts payable accounts is calculated after subtracting the purchase returns amount.

- • The purchase discount is received of the payment made and there is reduction is merchandise purchases cost. Therefore, merchandise inventory account is credited.

- • The cash account is an asset account and the account balance is decreasing. Therefore, it is credited.

Calculations for determining the cost per item purchased from company MDC are as follows:

The total cost incurred on purchasing 20 items is given as $5,400 including freight charges.

The formula for calculating cost per item is as follows:

Substitute $5,400 for the total cost incurred on purchasing of items and 20 for number of items.

The cost per item is calculated as $270.

Working Note:

Calculating purchase discount:

Under the perpetual inventory system, the purchase discount is represented by the merchandise inventory account. The purchased discount is calculated on the merchandise purchases cost excluding purchase returns and the freight charges. The purchase discount is given as two percent of the merchandise purchase.

The amount of purchase discount would be $90.6.

Calculations for sales discount:

The sales discount is provided to the customer by the seller fulfilling the terms of making the payments as per 1/10, n/30 terms. The customer is entitled to receive the one percent of sales discount on the merchandise sold if the payment is made with ten days of invoice provided.

The amount calculated as per given information would be $9.

Calculations for the credit card expense:

The fee is charged for availing the services of credit card. The bank fee to be charged as credit card is given as two percent for all credit card sales.

The expense would amount to be $300.

Calculations for the purchases amount:

The seller provides the trade discount of thirty percent and the ten percent on the list price to the buyer. The purchases amount to be recorded by the buyer would be the invoice price.

The purchases amount that would be calculated is $5,670.

Calculating purchase discount:

Under the perpetual inventory system, the purchase discount is represented by the merchandise inventory account. The purchased discount is calculated on the merchandise purchases cost excluding trade discount. The purchase discount is given as one percent of the merchandise purchase.

The amount of purchase discount would be $56.7.

Want to see more full solutions like this?

Chapter 8 Solutions

COLLEGE ACCOUNTING

- On January 5, 2019, ShoeKing Corp. sells for cash 500 pairs of volleyball shoes to FootAction, a shoe retailer, for 70 each. FootAction has the right to return the shoes for any reason up to March 31, 2019, for a full refund. The cost of each pair of shoes is 32. ShoeKing predicts that it is probable that 40 pairs of the shoes will be returned. ShoeKing uses the perpetual method for inventory. Required: 1. Prepare ShoeKings journal entry on January 5, 2019, to account for this transaction. 2. Assume that FootAction returns 35 pairs of shoes on March 31, 2019. Prepare the journal entry to record this return.arrow_forwardThe moving average inventory cost flow assumption is applicable to which of the following inventory systems? Questions M7-6 and M7-7 are based on the following data: City Stationers Inc. had 200 calculators on hand on January 1, 2019, costing 18 each. Purchases and sales of calculators during the month of January were as follows: City uses a periodic inventory system. According to a physical count, 150 calculators were on hand at January 31, 2019.arrow_forwardReview the following transactions, and prepare any necessary journal entries for Renovation Goods. A. On May 12, Renovation Goods purchases 750 square feet of flooring (Flooring Inventory) at $3.00 per square foot from a supplier, on credit. Terms of the purchase are 2/10, n/30 from the invoice date of May 12. B. On May 15, Renovation Goods purchases 200 measuring tapes (Tape Inventory) at $5.75 per tape from a supplier, on credit. Terms of the purchase are 4/15, n/60 from the invoice date of May 15. C. On May 22, Renovation Goods pays cash for the amount due to the flooring supplier from the May 12 transaction. D. On June 3, Renovation Goods pays cash for the amount due to the tape supplier from the May 15 transaction.arrow_forward

- Palisade Creek Co. is a merchandising business that uses the perpetual inventory system. The account balances for Palisade Creek Co. as of May 1, 2019 (unless otherwise indicated), are as follows: During May, the last month of the fiscal year, the following transactions were completed: Instructions 1. Enter the balances of each of the accounts in the appropriate balance column of a four-column account. Write Balance in the item section and place a check mark () in the Posting Reference column. Journalize the transactions for May, starting on Page 20 of the journal. 2. Post the journal to the general ledger, extending the month-end balances to the appropriate balance columns after all posting is completed. In this problem, you are not required to update or post to the accounts receivable and accounts payable subsidiary ledgers. 3. Prepare an unadjusted trial balance. 4. At the end of May, the following adjustment data were assembled. Analyze and use these data to complete (5) and (6). 5. (Optional) Enter the unadjusted trial balance on a 10-column end-of-period spreadsheet (work sheet), and complete the spreadsheet. 6. Journalize and post the adjusting entries. Record the adjusting entries on Page 22 of the journal. 7. Prepare an adjusted trial balance. 8. Prepare an income statement, a statement of owners equity, and a balance sheet. 9. Prepare and post the closing entries. Record the closing entries on Page 23 of the journal. Indicate closed accounts by inserting a line in both Balance columns opposite the closing entry. Insert the new balance in the owners capital account. 10. Prepare a post-closing trial balance.arrow_forwardAllen Company is a wholesale distributor of automotive replacement parts. Initial amounts taken from Allens accounting records are as follows: Accounts payable at December 31, 2019: Additional information is as follows: 1. Parts held on consignment from Charlie to Allen, the consignee, amounting to 155,000 were included in the physical count of goods in Allens warehouse on December 31, 2019, and in accounts payable at December 31, 2019. 2. 22,000 of parts, which were purchased from Full and paid for in December 2019, were sold in the last week of 2019 and appropriately recorded as sales of 28,000. The parts were included in the physical count of goods in Allens warehouse on December 31, 2019, because the parts were on the loading dock waiting to be picked up by customers. 3. Parts in transit to customers on December 31, 2019, shipped FOB shipping point on December 28, 2019, amounted to 34,000. The customers received the parts on January 7, 2020. Sales of 40,000 to the customers for the parts were recorded by Allen on January 3, 2020. 4. Retailers were holding 210,000 at cost (250,000 at retail) of goods on consignment from Allen, the consignor, at their stores on December 31, 2019. 5. Goods were in transit from Greg to Allen on December 31, 2019. The cost of the goods was 25,000, and they were shipped FOB shipping point on December 29, 2019. 6. A quarterly freight bill in the amount of 2,000 specifically relating to merchandise purchases in December 2019, all of which was still in the inventory at December 31, 2019, was received on January 4, 2020. The freight bill was not included in either the inventory or in accounts payable at December 31, 2019. 7. All of the purchases from Baker occurred during the last 7 days of the year. These items have been recorded in accounts payable and accounted for in the physical inventory at cost before discount. Allens policy is to pay invoices in time to take advantage of all cash discounts, adjust inventory accordingly, and record accounts payable, net of cash discounts. Required: Prepare a schedule of adjustments to the initial amounts of inventory, accounts payable, and sales. Show the effect, if any, of each of the transactions separately and indicate if the transactions would have no effect on the amount.arrow_forwardOn April 5, a customer returns 20 bicycles with a sales price of $250 per bike to Barrio Bikes. Each bike cost Barrio Bikes $100. The customer had yet to pay on their account. The bikes are in sellable condition. Prepare the journal entry or entries to recognize this return if the company uses A. the perpetual inventory system B. the periodic inventory systemarrow_forward

- Review the following transactions, and prepare any necessary journal entries for Sewing Masters Inc. A. On October 3, Sewing Masters Inc. purchases 800 yards of fabric (Fabric Inventory) at $9.00 per yard from a supplier, on credit. Terms of the purchase are 1/5, n/40 from the invoice date of October 3. B. On October 8, Sewing Masters Inc. purchases 300 more yards of fabric from the same supplier at an increased price of $9.25 per yard, on credit. Terms of the purchase are 5/10, n/20 from the invoice date of October 8. C. On October 18, Sewing Masters pays cash for the amount due to the fabric supplier from the October 8 transaction. D. On October 23, Sewing Masters pays cash for the amount due to the fabric supplier from the October 3 transaction.arrow_forwardJohn Neff owns and operates Waikiki Surf Shop. A year-end trial balance is provided on page 561. Year-end adjustment data for the Waikiki Surf Shop are shown below. Neff uses the periodic inventory system. Year-end adjustment data are as follows: (a, b)A physical count shows that merchandise inventory costing 51,800 is on hand as of December 31, 20--. (c, d, e)Neff estimates that customers will be granted 2,000 in refunds of this years sales next year and the merchandise expected to be returned will have a cost of 1,200. (f)Supplies remaining at the end of the year, 600. (g)Unexpired insurance on December 31, 2,600. (h)Depreciation expense on the building for 20--, 5,000. (i)Depreciation expense on the store equipment for 20--, 3,000. (j)Wages earned but not paid as of December 31, 1,800. (k)Neff also offers boat rentals which clients pay for in advance. Unearned boat rental revenue as of December 31 is 3,000. Required 1. Prepare a year-end spreadsheet. 2. Journalize the adjusting entries. 3. Compute cost of goods sold using the spreadsheet prepared for part (1).arrow_forwardDick’s Sporting Goods is a large retailer based in Coraopolis, Pennsylvania. Given some indicators in fiscal year 2019-2020, we analyze its retail performance. The annual inventory holding cost rate is given in the table. The company carries a fishing rod at the unit cost of $105. To answer the question: (1) copy only Parts 2 and 3 onto your papers; (2) show numeric equations and final results; and (3) follow the units and decimal places specified.arrow_forward

- Coronado Machine Company maintains a general ledger account for each class of inventory, debiting such accounts for increases during the period and crediting them for decreases. The transactions below relate to the Raw Materials inventory account, which is debited for materials purchased and credited for materials requisitioned for use. 1. An invoice for $12,960, terms f.o.b. destination, was received and entered January 2, 2020. The receiving report shows that the materials were received December 28, 2019. 2. Materials costing $44,800, shipped f.o.b. destination, were not entered by December 31, 2019, “because they were in a railroad car on the company’s siding on that date and had not been unloaded.” 3. Materials costing $11,680 were returned to the supplier on December 29, 2019, and were shipped f.o.b. shipping point. The return was entered on that date, even though the materials are not expected to reach the supplier’s place of business until January 6, 2020. 4. An invoice for…arrow_forwardTracy Company, a manufacturer of air conditioners, sold 100 units to Thomas Company on November 17, 2021. The units have a list price of $500 each, but Thomas was given a 30% trade discount. The terms of the sale were 2/10, n/30. Thomas uses a perpetual inventory system. Prepare the following journal entries to record the purchase by Thomas on November 17 and payment on November 26, 2021 and December 15, 2021 using the net method of accounting for purchase discounts. Record the purchase of air conditioners. Record payment on November 26 using the net method of accounting for purchase discounts. Alternatively, record payment on December 15 using the net method of accounting for purchase discounts.arrow_forwardAll Things Auto are retailers who purchase and sell vehicle parts & accessories, including batteries. The business uses a perpetual inventory system and began the last quarter of 2020 with merchandise inventory of 10 batteries of the “DieHard” brand at a total cost of $168,200. The following transactions, relating to the “DieHard” brand were completed during the quarter:October 5: Purchased 15 batteries at a cost of $17,020 each.October 14: Sold 18 batteries at $22,250 per batteryOctober 22: Purchased 24 batteries at a cost of $18,175 each but the supplier gave a 4% quantity discount.November 10: Sold 15 batteries to Orion Auto Ltd and 10 batteries to Brown’s Auto Detailing at a price of $23,990 each.November 12: Owing to an increased demand for this brand of batteries, 30 batteries were purchased on account at a cost of $17,612 each. In addition, All Things Auto paid $288 in cash on eachbattery to have the inventory shipped from the vendor’s warehouse to their location.November…arrow_forward

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning, Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning