Videos

Addison Parker (Social Security number 123-45-6785), single and age 32, lives at 3218 Columbia Drive, Spokane, WA 99210. She is employed as regional sales manager by VITA Corporation, a manufacturer and distributor of vitamins and food supplements. Addison is paid an annual salary of $83,000 and a separate travel allowance of $28,000. In order to access the travel allowance, VITA requires adequate accounting by Addison.

- Addison participates in VITA’s contributor)* health and § 401(k) plans. During 2019, she paid $4,500 for her share of the medical insurance and contributed $11,000 to the § 401(k) retirement plan.

- Addison uses her automobile 70% for business and 30% for personal. The automobile, a Toyota Avalon, was purchased new on June 30, 2017, for $37,000 (no trade-in was involved).

Depreciation has been claimed using the MACRS 200% declining-balance method, and no § 179 election was made in the year of purchase. (For depreciation information, see the IRS Instructions for Form 4562, Part V.) During 2019, Addison drove 15,000 miles and incurred and paid the following expenses relating to the automobile:

- Because VITA does not have an office in Spokane, the company expects Addison to maintain one in her home. Out of 1.500 square feet of living space in her apartment, Addison has set aside 300 square feet as an office. Expenses for 2019 relating to the office are listed below.

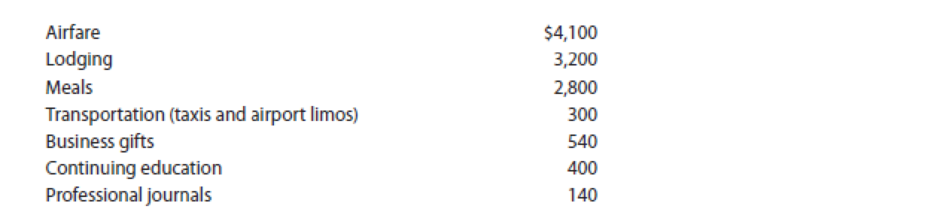

- Addison’s employment-related expenses (except for the trip to Korea) for 2019 are summarized below.

Most of Addison’s business trips involve visits to retail outlets in her region. Store managers and their key employees, as well as some suppliers, were the parties entertained. The business gifts were boxes of candy costing $30 ($25 each plus $5 for wrapping and shipping) sent to 18 store managers at Christmas. The continuing education was a noncredit course dealing with improving management skills that Addison took online.

- In July 2019, Addison traveled to Korea to investigate a new process that is being developed to convert fish parts to a solid consumable tablet form. She spent one week checking out the process and then took a one-week vacation tour of the country. The round-trip airfare was $3,600, and her expenses relating to business were $2,100 for lodging ($300 each night), $1,470 for meals, and $350 for transportation. Upon returning to the United States, Addison sent her findings about the process to her employer. VITA was so pleased with her report that it gave her an employee achievement award of $10,000. The award was sent to Addison in January 2020.

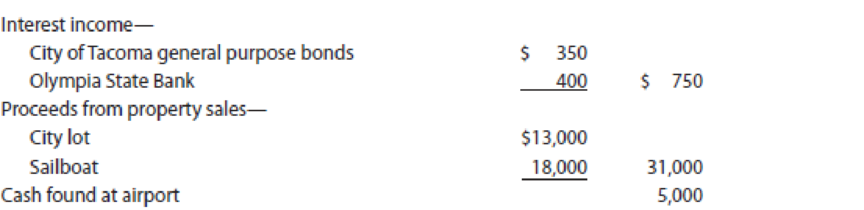

- Besides the items already mentioned, Addison had the following receipts in 2019:

Regarding the city lot (located in Vancouver), Addison purchased the property in 2004 for $16,000 and held it as an investment. Unfortunately, the neighborhood where the lot was located deteriorated, and property values declined. In 2019, Addison decided to cut her losses and sold the property for $13,000. The sailboat was used for pleasure and was purchased in 2015 for $16,500. Addison sold the boat because she purchased a new and larger model (see below). While at the Spokane airport, Addison found an unmarked envelope containing 55,000 in $50 bills. Because no mention of any lost funds was noted in the media, Addison kept the money.

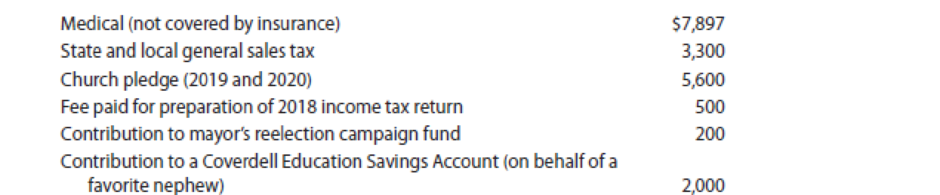

- Addison’s expenditures for 2019 (not previously noted) are summarized below.

Addison keeps careful records regarding sales taxes. In 2019, the sales tax total was unusually high due to the purchase of a new sailboat. In 2019, Addison decided to pay her church pledge for both 2019 and 2020. The insurance premium was on a policy covering her father’s life. (Addison is the designated beneficiary under the policy.)

Addison’s employer withheld $8,600 for Federal income tax purposes, and she applied her $800 overpayment for 2018 toward the 2019 tax liability.

Compute Addison’s Federal income tax payable (or refund) for 2019. In making the calculation, use the ‘Fax Rate Schedule and disregard the application of the alternative minimum tax (AMI*), which is not discussed until Chapter 12.

Calculate the Mrs. C’s federal income tax.

Explanation of Solution

Federal Income Tax: Federal income tax is the tax imposed by the federal government on the income of an individual and business organization. Federal income tax has a standard base for certain level of income.

Calculate the Mrs. C’s federal income tax.

| Particulars | Amount ($) | Amount ($) |

| Salary (Note 1) | 83,000 | |

| Expense allowance (Note 2) | 0 | |

|

Contribution to § 401 (k) retirement plan (Note 3) | (11,000) | |

| Interest income (Note 4) | 400 | |

| Treasure trove (Note 5) | 5,000 | |

| Property transactions (Note 6): | ||

| Loss on sale of lot | (3,000) | |

| Gain on boat | 1,500 | (1,500) |

| Adjusted gross income | 75,900 | |

| Itemized deductions: | ||

| Medical (Note 7) | 4,807 | |

| Sales tax (Note 8) | 3,300 | |

| Charitable contributions (Note 9) | 5,600 | |

| Campaign contribution (Note 10) | 0 | |

| Premium of life insurance (Note 11) | 0 | |

| Contribution to Coverdell education savings account (Note 12) | 0 | (13,707) |

| Taxable income | 62,193 | |

| Tax liability on taxable income of $62,193using the 2019 tax rate schedule for single taxpayers | 9,541 | |

| Less: | ||

| Withholding | 8,600 | |

| Overpayment from 2018 | 800 | (9,400) |

| Net tax due for 2019 | 141 |

Table (1)

Notes:

(1) Since it was not received in 2019, gross income does not include the achievement award $10,000. Mr. A does not recognize income until the year of its receipt, as cash basis taxpayer.

(2) Ms. A is required to provide an adequate accounting to VITA. Ms. A keeps records of her various expenses and submits them to VITA for reimbursement. Employee business expenses are considered as excess expenses.

Compute excess expenses.

| Particulars | Amount ($) | Amount ($) |

| Expense allowance | 28,000 | |

| Expenses: | ||

| Office in the home (Note 13) | 5,920 | |

| Business use of auto (Note 14) | 7,943 | |

| Employee expense (Note 15) | 4,985 | |

| Other employee expenses (Note 16) | 11,480 | |

| Total expenses | 30,328 | |

| Expense allowance used | (28,000) | |

| Excess expenses | 2,328 |

Table (2)

Expense allowance will effectively be offset by $28,000 of for AGI deductions; Since Mr. A provided adequate accounting to her employer. Expense allowance to Ms. A as income will not be reported as VITA. The excess expenses are miscellaneous itemized deductions, since Ms. A’s expenses exceeded her allowance. Congress suspended miscellaneous itemized deductions from 2018 through 2025 so, they are not deductible.

(3) In W–2 submitted by the employer is netted out from salary.

(4) The interest $350 on the City of Tacoma bonds is not subject to tax.

(5) Cash of $5,000 found by Ms. A is income.

(6) Gain on sales is $1,500 because gain on sale of personal use property is taxed. Since, Sale of the ATV is zero because Mr. C paid $14,000 as a result its $5,000 loss. Therefore, it is not deductible in case of personal losses. The result is a net long-term capital loss of $1,500, when offset against a long-term capital loss of $3,000.

(7) Compute medical expense after limitation.

| Particulars | Amount ($) |

| Medical expenses paid | 7,897 |

| Medical insurance premium | 4,500 |

| Total medical expenses | 12,397 |

| Less limitation | (7,590) |

| Medical expense after limitation | 4,807 |

Table (3)

(8) Since, Mr. A could justify a larger amount IRS sales tax tables did not have to be used.

(9) Charitable contributions are subject to deductions.

(10) Deduction is not subject to political contributions

(11) Premiums on personal life insurance policies are not subject to deduction.

(12) Contributions to Coverdell Education Savings Accounts (CESAs) are not subject to deduction. CESAs are subject to deduction from gross income.

(13) Percentage of office in the home business is 20% (300 sq. ft. /1,500 sq. ft.).

- Direct expense is $1,200.

- Indirect expenses are $4,720

(14) Compute the business use of auto.

| Particulars | Amount ($) |

| Gasoline | 3,100 |

| Depreciation | 3,050 |

| Insurance | 2,900 |

| Auto club dues | 240 |

| Interest on car loan | 0 |

| Repairs and maintenance | 1,200 |

| Total (a) | 10,490 |

| Business percentage (b) | 70% |

| Business portion (a x b) | 7,343 |

| Add: Business parking | 600 |

| Total auto deduction | 7,943 |

Table (4)

Traffic fines are not subject to deduction even during business use.

Regular depreciation for automobiles is $7,104 ($37,000 x 19.2%).

(15) Compute employee expenses:

| Particulars | Amount ($) | Amount ($) |

| Airfare | 1,800 | |

| Lodging | 2,100 | |

| Meals | 1,470 | |

| Less: 50% limit | (735) | 735 |

| Transportation | 350 | |

| Total | 4,985 |

Table (5)

(16) Compute other employee expenses:

| Particulars | Amount ($) |

| Airfare | 4,100 |

| Lodging | 3,200 |

| Meals | 2,800 |

| Transportation | 300 |

| Business gifts | 540 |

| Continuing education | 400 |

| Professional journals | 140 |

| Total | 11,480 |

Table (6)

Gift wrapping and shipping can be added to the $25 maximum allowed, since business gifts are allowed in full.

Want to see more full solutions like this?

Chapter 9 Solutions

Individual Income Taxes

- John Benson, age 40, is single. His Social Security number is 111-11-1111, and he resides at 150 Highway 51, Tangipahoa, LA 70465. John has a 5-year-old child, Kendra, who lives with her mother, Katy. As a result of his divorce in 2016, John pays alimony of 6,000 per year to Katy and child support of 12,000. The 12,000 of child support covers 65% of Katys costs of rearing Kendra. Kendras Social Security number is 123-45-6789, and Katys is 123-45-6788. Johns mother, Sally, lived with him until her death in early September 2019. He incurred and paid medical expenses for her of 15,588 and other support payments of 11,000. Sallys only sources of income were 5,500 of interest income on certificates of deposit and 5,600 of Social Security benefits, which she spent on her medical expenses and on maintenance of Johns household. Sallys Social Security number was 123-45-6787. John is employed by the Highway Department of the State of Louisiana in an executive position. His salary is 95,000. The appropriate amounts of Social Security tax and Medicare tax were withheld. In addition, 9,500 was withheld for Federal income taxes and 4,000 was withheld for state income taxes. In addition to his salary, Johns employer provides him with the following fringe benefits. Group term life insurance with a maturity value of 95,000; the cost of the premiums for the employer was 295. Group health insurance plan; Johns employer paid premiums of 5,800 for his coverage. The plan paid 2,600 for Johns medical expenses during the year. Upon the death of his aunt Josie in December 2018, John, her only recognized heir, inherited the following assets. Three months prior to her death, Josie gave John a mountain cabin. Her adjusted basis for the mountain cabin was 120,000, and the fair market value was 195,000. No gift taxes were paid. During the year, John reported the following transactions. On February 1, 2019, he sold for 45,000 Microsoft stock that he inherited from his father four years ago. His fathers adjusted basis was 49,000, and the fair market value at the date of the fathers death was 41,000. The car John inherited from Josie was destroyed in a wreck on October 1, 2019. He had loaned the car to Katy to use for a two-week period while the engine in her car was being replaced. Fortunately, neither Katy nor Kendra was injured. John received insurance proceeds of 16,000, the fair market value of the car on October 1, 2019. On December 28, 2019, John sold the 300 acres of land to his brother, James, for its fair market value of 160,000. James planned on using the land for his dairy farm. Other sources of income for John are: Potential itemized deductions for John, in addition to items already mentioned, are: Part 1Tax Computation Compute Johns net tax payable or refund due for 2019. Part 2Tax Planning Assume that rather than selling the land to James, John is considering leasing it to him for 12,000 annually with the lease beginning on October 1, 2019. James would prepay the lease payments through December 31, 2019. Thereafter, he would make monthly lease payments at the beginning of each month. What effect would this have on Johns 2019 tax liability? What potential problem might John encounter? Write a letter to John in which you advise him of the tax consequences of leasing versus selling. Also prepare a memo addressing these issues for the tax files.arrow_forwardMalin is a married taxpayer and has three dependent children. Malin's employer offers health insurance for employees and Malin takes advantage of the benefit for her entire family (her spouse's employer also offers health insurance but they opt out). During the year, Malin paid $ 1,200 toward her family's health insurance premiums through payroll deductions while the employer paid the remaining $ 9,200. Malin's family visited health care professionals numerous times during the year and made total copayments toward medical services of $280. Malin's daughter had knee surgery due to a soccer injury and the insurance company paid the hospital $ 6,700$ directly and reimbursed Malin $400 for her out-of-pocket health care expenses related to the surgery. How much gross income should Malin recognize related to her health insurance? $0 $ 9,200 14,020(9,200+6,7001,200280400) 8,000(9,2001,200) None of the abovearrow_forwardAbbe, age 56, is married and has two dependent children, one age 14, and the other a 21 -year-old full-time student. Abbe has one job, and her husband, age 58, is not employed. If she expects to earn wages of $50,000, file jointly, and take the standard deduction, how many allowances should Abbe claim on her Form W-4? 4 5 7 8 9arrow_forward

- Lance H. and Wanda B. Dean are married and live at 431 Yucca Drive, Santa Fe, NM 87501. Lance works for the convention bureau of the local Chamber of Commerce, and Wanda is employed part-time as a paralegal for a law firm. During 2018, the Deans had the following receipts: Wanda was previously married to John Allen. When they divorced several years ago, Wanda was awarded custody of their two children, Penny and Kyle. (Note: Wanda has never issued a Form 8332 waiver.) Under the divorce decree, John was obligated to pay alimony and child supportthe alimony payments were to terminate if Wanda remarried. In July, while going to lunch in downtown Santa Fe, Wanda was injured by a tour bus. Because the driver was clearly at fault, the owner of the bus, Roadrunner Touring Company, paid her medical expenses (including a one-week stay in a hospital). To avoid a lawsuit, Roadrunner also transferred 90,000 to her in settlement of the personal injuries she sustained. The Deans had the following expenditures for 2018: The life insurance policy was taken out by Lance several years ago and designates Wanda as the beneficiary. As a part-time employee, Wanda is excluded from coverage under her employers pension plan. Consequently, she provides for her own retirement with a traditional IRA obtained at a local trust company. Because the mayor is a member of the local Chamber of Commerce, Lance felt compelled to make the political contribution. The Deans household includes the following, for whom they provide more than half of the support: Penny graduated from high school on May 9, 2018, and is undecided about college. During 2018, she earned 8,500 (placed in a savings account) playing a harp in the lobby of a local hotel. Wayne is Wandas widower father who died on December 20, 2017. For the past few years, Wayne qualified as a dependent of the Deans. Federal income tax withheld is 4,200 (Lance) and 2,100 (Wanda). The proper amount of Social Security and Medicare tax was withheld. Determine the Federal income tax for 2018 for the Deans on a joint return by completing the appropriate forms. They do not want to contribute to the Presidential Election Campaign Fund. All members of the family had health care coverage for all of 2018. If an overpayment results, it is to be refunded to them. Suggested software: ProConnect Tax Online.arrow_forwardMargaret, age 65, and John, age 62, are married with a 23 -year-old daughter who lives in their home. They provide over half of their daughter's support, and their daughter earned $4,100 this year from a part-time job. Their daughter is not a full-time student. The daughter can/cannot be claimed as a dependent because: She cannot be claimed because she is over 19 and not a full-time student. She can be claimed because she is a qualifying child. She can be claimed because she is a qualifying relative. She cannot be claimed because she fails the gross income test.arrow_forward

Individual Income TaxesAccountingISBN:9780357109731Author:HoffmanPublisher:CENGAGE LEARNING - CONSIGNMENT

Individual Income TaxesAccountingISBN:9780357109731Author:HoffmanPublisher:CENGAGE LEARNING - CONSIGNMENT