a)

To calculate: The following:

- Short-run supply curve for each snuffbox maker

- Short-run supply curve for the market as a whole

a)

Answer to Problem 9.8P

- Short-run supply curve for each snuffbox maker is

- Short-run supply curve for the market as a whole is

Explanation of Solution

Given:

Total identical firms

Short-run total cost

Short-run marginal cost

Explain:

- In the

perfect competition , supply curve for each firm will be equal to its short-run marginal cost. - As there are 100 firms in the industry thus industry supply is given as follows:

Thus, the short-run supply curve for each snuffbox market is

Introduction: One of the portion in the marginal cost that will appear above its

b)

To Calculate: The following:

- Equilibrium in the market

- Each firm’s total short-run profit

b)

Answer to Problem 9.8P

- Equilibrium in the market is

- Each firm’s total short-run profit is

Explanation of Solution

Given:

Explain:

a)

For equilibrium demand must be equal to its supply

Calculate the equilibrium as follows:

Set

b)

Calculate the equilibrium quantity as follows:

Substitute the value of P in the equation to get the value of Q.

Thus, the equilibrium quantity is

As there are 100 firms, each firm will produce

The formula for calculating total profit as follows:

Calculate TC as follows:

Thus, the firms total cost is

Calculate the firm’s total revenue as follows:

Thus, the total revenue is

Calculate the total profit as follows:

Thus, the firms total short run profit is

Introduction: Equilibrium is one of the market price where supplied goods is similar to the demanded goods. In this place only demand and supply curves in the market intersect. During

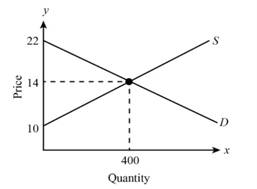

c)

To Graph: The market equilibrium and compute total

c)

Answer to Problem 9.8P

Total producer surplus is

Explanation of Solution

In the graph, quantity is represented on the horizontal axis and price on the vertical axis.

Equilibrium is at the point where demand and supply curve intersect each other.

Thus, the

Calculate the

Consumer surplus

Thus, the consumer surplus is

Calculate the producer surplus as follows:

Producer surplus

Thus, the Producer surplus is

Calculate the total surplus as follows:

Total surplus=Consumer surplus +Producer surplus

Thus, the total surplus is

Introduction: There is a great demand and equal supply, the markets are at equilibrium during summer. During post summer season, the supply will start falling and demand will remain the same. The corresponding price is the equilibrium price, also the quantity is the

d)

To Show: The calculated total producer surplus in part c is equal to total industry profits plus industry short-run fixed costs.

d)

Answer to Problem 9.8P

Total producer surplus is

Total industry profits and industry short-run fixed costs is

Therefore, the total industry profits plus industry short-run fixed cost is equal to producer’s surplus.

Explanation of Solution

Calculate the total profits of the industry as follows:

Total profit of the industry

Thus, the total profit of the industry is

Calculate the short run fixed costs as follows:

Thus, the short run fixed cost is

Because as per the equation,

Sum up both the total profit and short run fixed cost as follows:

Total profits+SRFC

Thus, it equals to

The producer surplus is

Introduction: Fixed costs are the expenditures that does not change based on the levels of production at least not in the short term. The fixed costs are same when the product will be produced a lot or little.

e)

To calculate: The tax change the market equilibrium when the government imposed a $3 tax on snuffboxes.

e)

Answer to Problem 9.8P

The market equilibrium price has declined from $14 to $13 and also the equilibrium quantity has declined by $100(from 400 to 300 units)

Explanation of Solution

Because of tariffs, new demand curve will be

Calculate the new equilibrium price as follows:

Thus, the equilibrium price is

Calculate the equilibrium quantity as follows:

Thus, the equilibrium quantity is

Introduction: Demanded quantity will be similar to the supplied quantity in a particular price is defined as Equilibrium. Suppose if the tax will be imposed by the government into the market, the tax imposed is to impact of the equilibrium. If the tax increases the price a buyer pays less than the tax.

f)

To Describe: The burden of the tax to be shared between snuffbox buyers and sellers.

f)

Answer to Problem 9.8P

Tax paid is

Consumers and producers will pay

Explanation of Solution

Calculate the tax paid as follows:

Tax paid

Introduction: Tax burden is divided between buyers and sellers. Suppose if the supply is more elastic than demand, buyers bear most of the tax burden. Otherwise, if the demand is more elastic than supply, producers bear most of the tax burden.

g)

To Calculate: The total loss of producer surplus as a result of the

g)

Answer to Problem 9.8P

The total loss of producer surplus as a result of the taxation of snuffboxes are

Explanation of Solution

Calculate the producer surplus as follows:

Produce surplus

Thus, the producer surplus is

Calculate the total loss of producer’s surplus as a result of the taxation of snuffboxes as follows:

Total loss

Introduction: The difference between prices is that Producers are willing to sell a product based on their costs within price and market equilibrium price is defined as produce surplus. Suppose if the economy produces the inefficient quantity, total surplus will occur. Deadweight is loss in the total producer.

Want to see more full solutions like this?

Chapter 9 Solutions

EBK INTERMEDIATE MICROECONOMICS AND ITS

Economics (MindTap Course List)EconomicsISBN:9781337617383Author:Roger A. ArnoldPublisher:Cengage Learning

Economics (MindTap Course List)EconomicsISBN:9781337617383Author:Roger A. ArnoldPublisher:Cengage Learning

Microeconomics: Private and Public Choice (MindTa...EconomicsISBN:9781305506893Author:James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. MacphersonPublisher:Cengage Learning

Microeconomics: Private and Public Choice (MindTa...EconomicsISBN:9781305506893Author:James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. MacphersonPublisher:Cengage Learning