Concept explainers

Videos

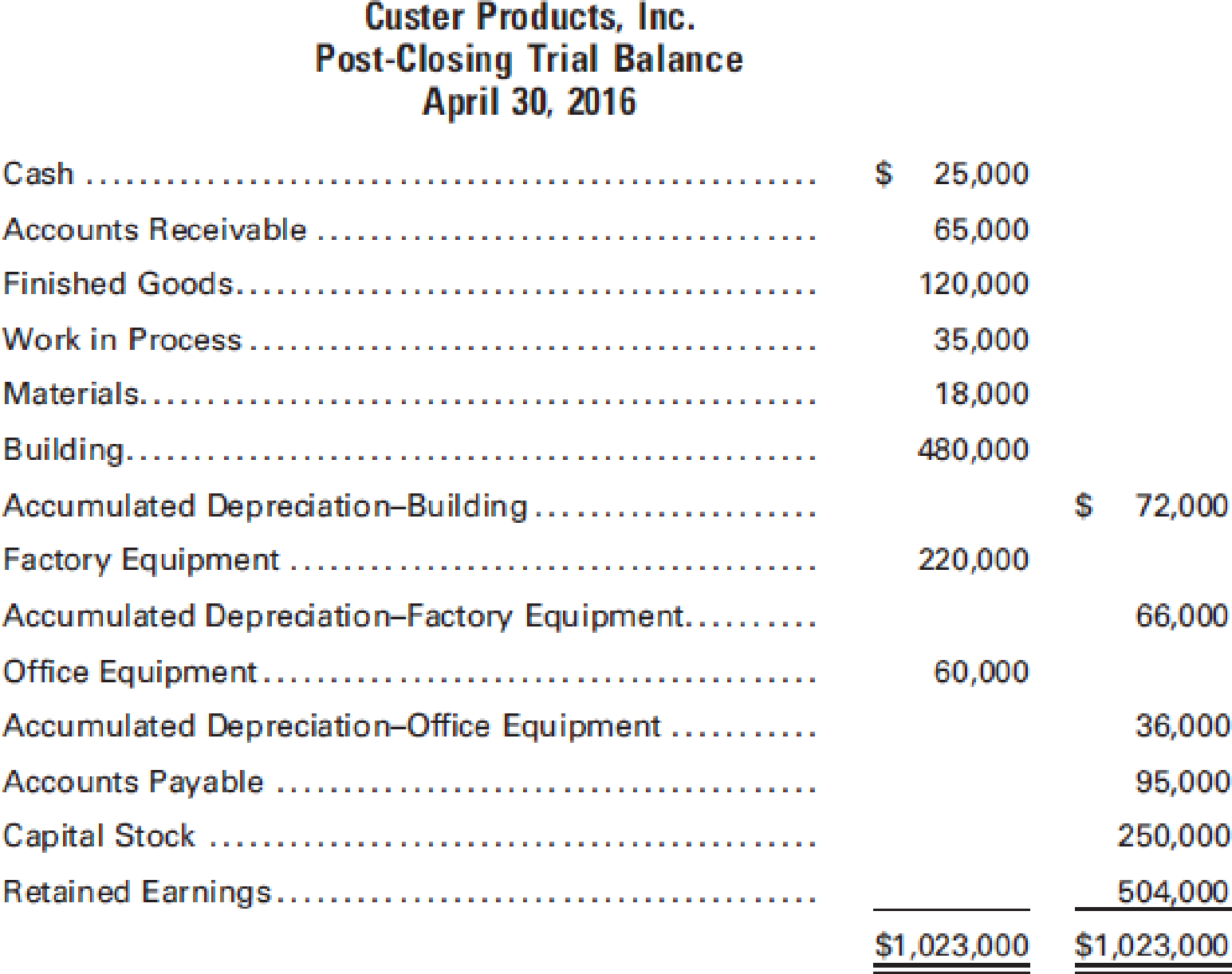

The post-closing

During May, the following transactions took place:

- a. Purchased raw materials at a cost of $45,000 and general factory supplies at a cost of $13,000 on account (recorded materials and supplies in the materials account).

- b. Issued raw materials to be used in production, costing $47,000, and miscellaneous factory supplies costing $15,000.

- c. Recorded the payroll and the payments to employees as follows: factory wages (including $12,000 indirect labor), $41,000; and selling and administrative salaries, $7,000. Additional account titles include Wages Payable and Payroll. (Ignore payroll withholdings and deductions.)

- d. Distributed the payroll in (c).

- e. Recognized

depreciation for the month at an annual rate of 5% on the building, 10% on the factory equipment, and 20% on the office equipment. The sales and administrative staff uses approximately one-fifth of the building for its offices. - f. Incurred other expenses totaling $11,000. One-fourth of this amount is allocable to the office function.

- g. Transferred total

factory overhead costs to Work in Process. - h. Completed and transferred goods with a total cost of $91,000 to the finished goods storeroom.

- i. Sold goods costing $188,000 for $362,000. (Assume that all sales were made on account.)

- j. Collected accounts receivable in the amount of $345,000.

- k. Paid accounts payable totaling $158,000.

Required:

- 1. Prepare

journal entries to record the transactions. - 2. Set up T-accounts. Post the beginning trial balance and the journal entries prepared in (1) to the accounts and determine the balances in the accounts on May 31.

- 3. Prepare a statement of cost of goods manufactured, an income statement, and a balance sheet. (Round amounts to the nearest whole dollar.)

1.

Prepare journal entry to record the given transactions.

Explanation of Solution

Prepare journal entry to record the given transactions.

| Date | Accounts title and explanation | Debit ($) | Credit ($) |

| a | Materials | 58,000 | |

| Accounts payable | 58,000 | ||

| (To record materials purchased on account) | |||

| b | Work in Process | 47,000 | |

| Factory overhead | 15,000 | ||

| Materials | 62,000 | ||

| (To record issue of direct materials and indirect materials) | |||

| c | Payroll | 48,000 | |

| Wages Payable | 48,000 | ||

| (To record factory wages and salaries) | |||

| Wages Payable | |||

| Cash | |||

| (To record the payment of factory wages and salaries) | |||

| d | Work in Process | 29,000 | |

| Factory overhead | 12,000 | ||

| Selling and Administrative Expenses (salaries) | 7,000 | ||

| Payroll | 48,000 | ||

| (To record the distribution of payroll) | |||

| e | Factory overhead (Depreciation of building) (1) | 1,600 | |

| Factory overhead (Depreciation of factory equipment) (3) | 1,833 | ||

| Selling and Administrative Expenses (Depreciation of building) (2) | 400 | ||

| Selling and Administrative Expenses (Depreciation of office equipment) (4) | 1,000 | ||

| Accumulated Depreciation - Building | 2,000 | ||

| Accumulated Depreciation – Factory Equipment | 1,833 | ||

| Accumulated Depreciation – Office Equipment | 1,000 | ||

| (To record depreciation on building, factory equipment, and office equipment) | |||

| f | Factory overhead(miscellaneous) | 8,250 | |

| Selling and Administrative expenses (miscellaneous) | 2,750 | ||

| Accounts payable | 11,000 | ||

| (To record factory overhead costs and selling and administrative expenses on account) | |||

| g. | Work in Process | 38,683 | |

| Factory Overhead | 38,683 | ||

| (To record transfer of factory overhead to Work-in process) | |||

| h. | Finished Goods | 91,000 | |

| Work in Process | 91,000 | ||

| (To record the transfer of cost of completed work to finished goods) | |||

| i | Accounts receivable | 362,000 | |

| Sales | 362,000 | ||

| (To record the sale made on account) | |||

| Cost of goods sold | 188,000 | ||

| Finished goods | 188,000 | ||

| (To record the cost of goods sold) | |||

| j. | Cash | 345,000 | |

| Accounts Receivable | 345,000 | ||

| (To record the receipt on accounts receivable) | |||

| k | Accounts Payable | ||

| Cash | |||

| (To record the payment of accounts payable) |

Table (1)

Working note 1: Calculate depreciation on buildings under factory overhead.

Working note 2: Calculate depreciation on buildings under selling and administrative expenses.

Working note 3: Calculate depreciation on factory equipment under factory overhead.

Working note 4: Calculate depreciation on factory equipment under selling and administrative expenses.

2

Prepare t-account and post the beginning trial balance and journal entries amount to the particular account and determine the ending balance in the account.

Explanation of Solution

Prepare t-account and post the beginning trial balance and journal entries amount to the particular account and determine the ending balance in the account.

| Cash | ||||

|

Beginning balance | 25,000 | (c) | 48,000 | |

| (j) | 345,000 | (k) | 158,000 | |

| Ending Balance | 164,000 | |||

| Accounts Receivable | ||||

|

Beginning balance | 65,000 | (j) | 345,000 | |

| (i) | 362,000 | |||

| Ending Balance | 164,000 | |||

| Finished Goods | ||||

|

Beginning balance | 120,000 | (i) | 188,000 | |

| (h) | 91,000 | |||

| Ending Balance | 23,000 | |||

| Work in Process | ||||

|

Beginning balance | 35,000 | (i) | 188,000 | |

| (h) | 91,000 | |||

| Ending Balance | 23,000 | |||

| Materials | ||||

|

Beginning balance | 18,000 | (b) | 62,000 | |

| (a) | 58,000 | |||

| Ending Balance | 14,000 | |||

| Building | ||||

|

Beginning balance | 480,000 | |||

| Ending Balance | 480,000 | |||

| Accumulated depreciation-Building | |||||||

|

Beginning balance (e) |

72,000 2,000 | ||||||

| Ending Balance | 74,000 | ||||||

|

Factory equipment | |||||||

|

Beginning balance | 220,000 | ||||||

| Ending Balance | 220,000 | ||||||

| Accumulated depreciation- Factory equipment | |||||||

|

Beginning balance (e) |

66,000 1,833 | ||||||

| Ending Balance | 67,833 | ||||||

|

Office equipment | |||||||

|

Beginning balance | 60,000 | ||||||

| Ending Balance | 60,000 | ||||||

| Accumulated depreciation- Office equipment | ||||

|

Beginning balance (e) |

36,000 1,000 | |||

| Ending Balance | 37,000 | |||

| Accounts Payable | ||||

|

(j) | 158,000 |

Beginning balance (a) (f) |

92,000 58,000 11,000 | |

| Ending Balance | 14,000 | |||

| Payroll | ||||

|

Beginning balance | 0 | |||

| (c) | 48,000 | (d) | 48,000 | |

| Ending Balance | 0 | |||

| Wages payable | ||||

|

Beginning balance | 0 | |||

| (c) | 48,000 | (c) | 48,000 | |

| Ending Balance | 0 | |||

| Capital Stock | ||||

|

Beginning balance | 250,000 | |||

| Ending Balance | 250,000 | |||

| Retained Earnings | ||||

|

Beginning balance | 504,000 | |||

| Ending Balance | 504,000 | |||

| Sales | |||||

| (i) | 362,000 | ||||

| Cost of goods sold | |||||

| (i) | 188,000 | ||||

| Factory Overhead | |||||

|

(b) (d) (e) (e) (f) |

15,000 12,000 1,600 1,833 8,250 | (g) | 38,683 | ||

| Selling and administrative expenses | |||||

|

(d) (e) (e) (f) |

7,000 400 1,000 2,750 | ||||

| Ending Balance | 11,150 | ||||

3.

Prepare Incorporation C’s statement of cost of goods manufactured, income statement, and balance sheet.

Explanation of Solution

Prepare Incorporation C’s statement of cost of goods manufactured for the month ended May 31, 2016.

| Incorporation C | ||

| Statement of cost of goods manufactured | ||

| For the month ended May 31, 2016 | ||

| Particulars | Amount ($) | Amount ($) |

| Direct materials: | ||

| Inventory, May 1 | 18,000 | |

| Add: Purchases | 58,000 | |

| Total cost of available materials | 76,000 | |

| Less: Inventory, May 31 | 14,000 | |

| Cost of materials used | 62,000 | |

| Less: Indirect materials used | 15,000 | |

| Cost of direct materials used in production | 47,000 | |

| Direct labor | 29,000 | |

| Factory Overhead: | ||

| Indirect materials | 15,000 | |

| Indirect labor | 12,000 | |

| Depreciation of building | 1,600 | |

| Depreciation of factory equipment | 1,833 | |

| Miscellaneous expenses | 8,250 | |

| Total factory overhead | 38,683 | |

| Total manufacturing cost | 114,683 | |

| Add: Work in process inventory, May 1 | 35,000 | |

| 149,683 | ||

| Less: work in process inventory, May 31 | 58,683 | |

| Cost of goods sold manufactured | 91,000 | |

Table (2)

Prepare Incorporation C’s income statement for the month ended May 31, 2016.

| Incorporation C | ||

| Income statement | ||

| For the month ended May 31, 2016 | ||

| Particulars | Amount ($) | Amount ($) |

| Sales | 362,000 | |

| Cost of goods sold: | ||

| Finished goods inventory, May 1 | 120,000 | |

| Add: Cost of goods manufactured | 91,000 | |

| Goods available for sale | 211,000 | |

| Less: Finished goods inventory , May 31 | 23,000 | 188,000 |

| Gross profit on sales | 174,000 | |

| Selling and administrative expenses | 11,150 | |

| Net income | 162,850 | |

Table (3)

Prepare Incorporation C’s balance sheet at May 31, 2016.

| Incorporation C | |||

| Balance Sheet | |||

| At May 31, 2016 | |||

| Particulars | Amount ($) | Amount ($) | |

| Current Assets: | |||

| Cash | 164,000 | ||

| Accounts receivable | 82,000 | ||

| Inventories: | |||

| Finished goods | 23,000 | ||

| Work in process | 58,683 | ||

| Materials | 14,000 | 95,683 | |

| Total current assets | 341,683 | ||

| Plant and equipment: | |||

| Building | 480,000 | ||

| Less: Accumulated depreciation | 74,000 | 406,000 | |

| Factory equipment | 220,000 | ||

| Less: Accumulated depreciation | 67,833 | 152,167 | |

| Office equipment | 60,000 | ||

| Less: Accumulated depreciation | 37,000 | 23,000 | |

| Total plant and equipment | 581,167 | ||

| Total assets | 922,850 | ||

| Liabilities and stockholder’s equity | |||

| Current liabilities: | |||

| Accounts payable | 6,000 | ||

| Stockholder’s equity: | |||

| Capital stock | 250,000 | ||

| Retained earnings (5) | 666,850 | ||

| Total Stockholder’s equity | 916,850 | ||

| Total liabilities and stockholder’s equity | 922,850 | ||

Table (4)

Working note 5:

Calculate the amount of retained earnings.

Want to see more full solutions like this?

Chapter 1 Solutions

Principles of Cost Accounting

- An examination of Buckhorn Fabricators records reveals the following transactions: a. On December 31, the physical inventory of raw material was 9,950 gallons. The book quantity, using the weighted average method, was 10,000 gal @ .52 per gal. b. Production returned to the storeroom materials that cost 775. c. Materials valued at 770 were charged to Factory Overhead (Repairs and Maintenance), but should have been charged to Work in Process. d. Defective material, purchased on account, was returned to the vendor. The material returned cost 234. e. Goods sold to a customer, on account, for 5,000 (cost 2,500) were returned because of a misunderstanding of the quantity ordered. The customer stated that the goods returned were in excess of the quantity needed. f. Materials requisitioned totaled 22,300, of which 2,100 represented supplies used. g. Materials purchased on account totaled 25,500. Freight on the materials purchased was 185. h. Direct materials returned to the storeroom amounted to 950. i. Scrap materials sent to the storeroom were valued at an estimated selling price of 685 and treated as a reduction in the cost of all jobs worked on during the period. j. Spoiled work sent to the storeroom valued at a sales price of 60 had production costs of 200 already charged to it. The cost of the spoilage is to be charged to the specific job worked on during the period. k. The scrap materials in (i) were sold for 685 cash. Required: Record the entries for each transaction.arrow_forwardThe following data summarize the operations during the year. Prepare a journal entry for each transaction. A. Purchase of raw materials on account: $1,500 B. Raw materials used by Job 1: $400 C. Raw materials used as indirect materials: $50 D. Direct labor for Job 1: $200 E. Indirect labor Incurred for Job 1: $30 F. Factory utilities Incurred on account: $500 G. Adjusting entry for factory depreciation: $200 H. Manufacturing overhead applied as percent of direct labor: 100% I. Job 1 is transferred to finished goods J. Job 1 is sold: $1,000 K. Manufacturing overhead is under applied: $100arrow_forwardThe adjusted trial balance for Appleton Appliances, Ltd. on June 30, the end of its first month of operation, is as follows: The general ledger reveals the following additional data: a. There were no beginning inventories. b. Materials purchases during the period were 23,000. c. Direct labor cost was 18,500. d. Factory overhead costs were as follows: Required: 1. Prepare a statement of cost of goods manufactured for June. 2. Prepare an income statement for June. (Hint: Check to be sure that your figure for Cost of Goods Sold equals the amount given in the trial balance.) 3. Prepare a balance sheet as of June 30. (Hint: Do not forget Retained Earnings.)arrow_forward

- A company has the following transactions during the week. Purchase of $3,000 raw materials inventory Assignment of $700 of raw materials inventory to Job 7 Payroll for 10 hours and $3,000 is assigned to Job 7 Factory depreciation of $1,750 Overhead applied at the rate of $200 per hour What is the cost assigned to Job 7 at the end of the week?arrow_forwardThe following data are taken from the general ledger and other records of Coral Park Production Co. on January 31, the end of the first month of operations in the current fiscal year: a. Prepare a statement of cost of goods manufactured. b. Prepare the cost of goods sold section of the income statement.arrow_forwardOn August 1, Cairle Companys work-in-process inventory consisted of three jobs with the following costs: During August, four more jobs were started. Information on costs added to the seven jobs during the month is as follows: Before the end of August, Jobs 70, 72, 73, and 75 were completed. On August 31, Jobs 72 and 75 were sold. Cairles selling and administrative expenses for August were 1,200. Required: Prepare an income statement for Cairle Company for August.arrow_forward

- On August 1, Cairle Companys work-in-process inventory consisted of three jobs with the following costs: During August, four more jobs were started. Information on costs added to the seven jobs during the month is as follows: Before the end of August, Jobs 70, 72, 73, and 75 were completed. On August 31, Jobs 72 and 75 were sold. Required: 1. Calculate the predetermined overhead rate based on direct labor cost. 2. Calculate the ending balance for each job as of August 31. 3. Calculate the ending balance of Work in Process as of August 31. 4. Calculate the cost of goods sold for August. 5. Assuming that Cairle prices its jobs at cost plus 20 percent, calculate Cairles sales revenue for August.arrow_forwardNelson Fabrication Inc. had a remaining credit balance of $20,000 in its under- and overapplied factory overhead account at year-end. The balance was deemed to be large and, therefore, should be closed to Work in Process, Finished Goods, and Cost of Goods Sold. The year-end balances of these accounts, before adjustment, showed the following: Determine the prorated amount of the overapplied factory overhead that is chargeable to each of the accounts. Prepare the journal entry to close the credit balance in Under-and Overapplied Factory Overhead.arrow_forwardDuring March, the following costs were charged to the manufacturing department: $14886 for materials; $14,656 for labor; and $13,820 for manufacturing overhead. The records show that 30,680 units were completed and transferred, while 2,400 remained in ending inventory. There were 33,080 equivalent units of material and 31,640 of conversion costs. Using the weighted-average method, what is the cost of inventory transferred and the balance in work in process inventory?arrow_forward

- Prepare the journal entry to record the factory wages of $25,000 incurred in the processing department and $15,000 incurred in the production department assuming payment will be made in the next pay period.arrow_forwardIssuance of materials On May 7, Bergan Company purchased on account 10,000 units of raw materials at 8 per unit. During May, raw materials were requisitioned for production as follows: 7,500 units for Job 200 at 8 per unit and 1,480 units for Job 305 at 5 per unit. Journalize the entry on May 7 to record the purchase and on May 31 to record the requisition from the materials storeroom.arrow_forwardLeMans Company produces specialty papers at its Fox Run plant. At the beginning of June, the following information was supplied by its accountant: During June, direct labor cost was 143,000, direct materials purchases were 346,000, and the total overhead cost was 375,800. The inventories at the end of June were: Required: 1. Prepare a cost of goods manufactured statement for June. 2. Prepare a cost of goods sold schedule for June.arrow_forward

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning