Concept explainers

Videos

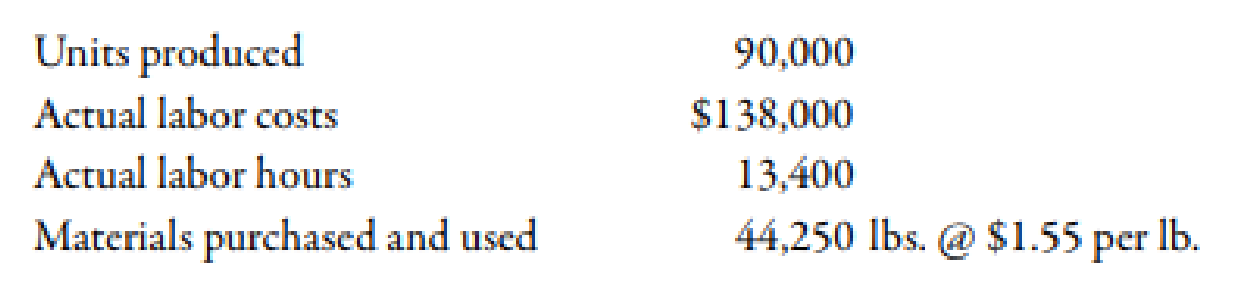

Phono Company manufactures a plastic toy cell phone. The following standards have been established for the toys materials and labor inputs:

During the first week of July, the company had the following results:

The purchasing agent located a new source of slightly higher-quality plastic, and this material was used during the first week in July. Also, a new manufacturing layout was implemented on a trial basis. The new layout required a slightly higher level of skilled labor. The higher-quality material has no effect on labor utilization. Similarly, the new manufacturing approach has no effect on material usage. (Note: Round all variances to the nearest dollar.)

Required:

- 1. CONCEPTUAL CONNECTION Compute the materials price and usage variances. Assuming that the materials variances are essentially attributable to the higher quality of materials, would you recommend that the purchasing agent continue to buy this quality, or should the usual quality be purchased? Assume that the quality of the end product is not affected significantly.

- 2. CONCEPTUAL CONNECTION Compute the labor rate and efficiency variances. Assuming that the labor variances are attributable to the new manufacturing layout, should it be continued or discontinued? Explain.

- 3. CONCEPTUAL CONNECTION Refer to Requirement 2. Suppose that the industrial engineer argued that the new layout should not be evaluated after only one week. His reasoning was that it would take at least a week for the workers to become efficient with the new approach. Suppose that the production is the same the second week and that the actual labor hours were 13,200 and the labor cost was $132,000. Should the new layout be adopted? Assume the variances are attributable to the new layout. If so, what would be the projected annual savings?

1.

Calculate the value of material price variance and material usage variance. Identify whether the plant manger could continue to purchase this quality product or purchase the usual quality.

Explanation of Solution

Variance:

The amount obtained when actual cost is deducted from budgeted cost is known as variance. Variance is calculated to find whether the cost is over applied or under applied.

Use the following formula to calculate material price variance:

Substitute $1.55 for actual price, 44,250 units for actual quantity and $1.50 for standard price in the above formula.

Therefore, the material price variance is $2,213(U).

Use the following formula to calculate material usage variance:

Substitute $1.50 for standard price, 44,250 units for actual quantity and 45,000 for standard quantity in the above formula.

Therefore, the material usage variance is $1,125(F).

The total variance is $1,088(U)

Working Note:

1. Calculation of standard quantity:

2.

Calculate the value of labor rate variance and labor efficiency variance. Identify whether the labor variances are attributable to the new manufacturing process should be continued or discontinued.

Explanation of Solution

Use the following formula to calculate labor rate variance:

Substitute $138,000 for actual cost, 10,800 hours for actual hours and $10 for standard rate in the above formula.

Therefore, the labor rate variance is $4,000(U).

Use the following formula to calculate labor efficiency variance:

Substitute $10.00 for standard rate, 13,400 hours for actual hours and 13,500 hours for standard hours in the above formula.

Therefore, the labor efficiency variance is $1,000(F).

The total labor variance is $3,000 (U)

Working Note:

1. Calculation of standard hours:

3.

Calculate the value of labor rate variance and labor efficiency variance. Identify whether the new process should be adopted.

Explanation of Solution

Use the following formula to calculate labor rate variance:

Substitute $132,000 for actual cost, 13,200 hours for actual hours and $10 for standard rate in the above formula.

Therefore, the labor rate variance is $0.

Use the following formula to calculate labor efficiency variance:

Substitute $10 for standard rate, 13,200 hours for actual hours and 13,500 hours for standard hours in the above formula.

Therefore, the labor efficiency variance is $3,000(F).

The total labor variance is $3,000 (F)

Working Note:

1. Calculation of standard hours:

Want to see more full solutions like this?

Chapter 10 Solutions

Bundle: Managerial Accounting: The Cornerstone of Business Decision-Making, Loose-Leaf Version, 7th + CengageNOWv2, 1 term (6 months) Printed Access Card

- Communications Jamarcus Bradshaw, plant manager of Georgia Paper Companys papermaking mill, was looking over the cost of production reports for July and August for the Papermaking Department. The reports revealed the following: Jamarcus was concerned about the increased cost per ton from the output of the department. As a result, he asked the plant controller to perform a study to help explain these results. The controller, Leann Brunswick, began the analysis by performing some interviews of key plant personnel in order to understand what the problem might be. Excerpts from an interview with Len Tyson, a paper machine operator, follow: Len: We have two papermaking machines in the department. I have no data, but I think paper machine No. 1 is applying too much pulp and, thus, is wasting both conversion and materials resources. We haven't had repairs on paper machine No. 1 in a while. Maybe this is the problem. Leann: How does too much pulp result in wasted resources? Len: Well, you see, if too much pulp is applied, then we will waste pulp material. The customer will not pay for the extra product; we just use more material to make the product. Also, when there is too much pulp, the machine must be slowed down in order to complete the drying process. This results in additional conversion costs. Leann: Do you have any other suspicions? Len: Well, as you know, we have two productsgreen paper and yellow paper. They are identical except for the color. The color is added to the papermaking process in the paper machine. I think that during August these two color papers have been behaving very differently. I don't have any data, but it just seems as though the amount of waste associated with the green paper has increased. Leann: Why is this? Len: I understand that there has been a change in specifications for the green paper, starting near the beginning of August. This change could be causing the machines to run poorly when making green paper. If this is the case, the cost per ton would increase for green paper. Leann also asked for a database printout providing greater detail on Augusts operating results. September 9 Requested by: Leann Brunswick Papermaking DepartmentAugust detail Prior to preparing a report, Leann resigned from Georgia Paper Company to start her own business. You have been asked to take the data that Leann collected, and write a memo to Jamarcus Bradshaw with a recommendation to management. Your memo should include analysis of the August data to determine whether the paper machine or the paper color explains the increase in the unit cost from July. Include any supporting schedules that are appropriate. Round any calculations to the nearest cent.arrow_forwardAnderson Company has the following departmental manufacturing structure for one of its products: After some study, the production manager of Anderson recommended the following revised cellular manufacturing approach: Required: 1. Calculate the total time it takes to produce a batch of 20 units using Andersons traditional departmental structure. 2. Using cellular manufacturing, how much time is saved producing the same batch of 20 units? Assuming the cell operates continuously, what is the production rate? Which process controls this production rate? 3. What if the processing times of molding, welding, and assembly are all reduced to six minutes each? What is the production rate now, and how long will it take to produce a batch of 20 units?arrow_forwardCalen Company manufactures and sells three products in a factory of three departments. Both labor and machine time are applied to the products as they pass through each department. The nature of the machine processing and of the labor skills required in each department is such that neither machines nor labor can be switched from one department to another. Calens management is attempting to plan its production schedule for the next several months. The planning is complicated by the fact that labor shortages exist in the community and some machines will be down several months for repairs. Following is information regarding available machine and labor time by department and the machine hours and direct labor hours required per unit of product. These data should be valid for at least the next six months. Calen believes that the monthly demand for the next six months will be as follows: Inventory levels will not be increased or decreased during the next six months. The unit cost and price data for each product are as follows: Required: 1. Calculate the monthly requirement for machine hours and direct labor hours for producing Products 401, 402, and 403 to determine whether or not the factory can meet the monthly sales demand. 2. Determine the quantities of 401, 402, and 403 that should be produced monthly to maximize profits. Prepare a schedule that shows the contribution to profits of your product mix. 3. Assume that the machine hours available in Department 3 are 1,500 instead of 2,700. Calculate the optimal monthly product mix using the graphing approach to linear programming. Prepare a schedule that shows the contribution to profits from this optimal mix. (CMA adapted)arrow_forward

- Big Mikes, a large hardware store, has gathered data on its overhead activities and associated costs for the past 10 months. Nizam Sanjay, a member of the controllers department, believes that overhead activities and costs should be classified into groups that have the same driver. He has decided that unloading incoming goods, counting goods, and inspecting goods can be grouped together as a more general receiving activity, since these three activities are all driven by the number of receiving orders. The 10 months of data shown below have been gathered for the receiving activity. Required: 1. Prepare a scattergraph, plotting the receiving costs against the number of purchase orders. Use the vertical axis for costs and the horizontal axis for orders. 2. Select two points that make the best fit, and compute a cost formula for receiving costs. 3. Using the high-low method, prepare a cost formula for the receiving activity. 4. Using the method of least squares, prepare a cost formula for the receiving activity. What is the coefficient of determination?arrow_forwardA local barbershop cuts the hair of 1,200 customers per month. The clients are men, and the barbers offer no special styling. During the month of May, 1,200 customers were serviced. The cost of haircuts includes the following: Required: 1. Explain why process costing is appropriate for this haircutting operation. 2. Calculate the cost per haircut. 3. Can you identify some possible direct materials used for this haircutting service? Is the usage of direct materials typical of services? If so, provide examples of services that use direct materials. Can you think of some services that would not use direct materials?arrow_forwardRIRA Company makes attachments such as backhoes and grader and bulldozer blades for construction equipment. The company uses a job order cost system. Management is concerned about cost performance and evaluates the job cost sheets to learn more about the cost effectiveness of the operations. To facilitate a comparison, the job cost sheets for Job 206 (for 50 backhoe buckets completed in October) and Job 228 (for 75 backhoe buckets completed in December) were pulled and presented as follows: Management is concerned about the increase in unit costs over the months from October to December. To understand what has occurred, management interviewed the purchasing manager and quality manager. Purchasing Manager: Prices have been holding steady for our raw materials during the first half of the year. I found a new supplier for our bulk steel that was willing to offer a better price than we received in the past. I saw these lower steel prices and jumped on them, knowing that a reduction in steel prices would have a very favorable impact on our costs. Quality Manager: Something happened around mid-year. All of a sudden, we were experiencing problems with respect to the quality of our steel. As a result, weve been having all sorts of problems on the shop floor in our foundry and welding operation. a. Analyze the two job cost sheets and identify why the unit costs have changed for the backhoe buckets. Complete the following schedule to help in your analysis: b. How would you interpret what has happened in light of your analysis and the interviews?arrow_forward

- Emery Manufacturing Company produces component parts for the farm equipment industry and has recently undergone a major computer system conversion. Jake Murray, the controller, has established a troubleshooting team to alleviate accounting problems that have occurred since the conversion. Jake has chosen Gus Swanson, assistant controller, to head the team that will include Linda Wheeler, cost accountant; Cindy Madsen, financial analyst; Randy Lewis, general accounting supervisor; and Max Crandall, financial accountant. The team has been meeting weekly for the last month. Gus insists on being part of all the team conversations in order to gather information, to make the final decision on any ideas or actions that the team develops, and to prepare a weekly report for Jake. He has also used this team as a forum to discuss issues and disputes about him and other members of Emerys top management team. At last weeks meeting, Gus told the team that he thought a competitor might purchase the common stock of Emery, because he had overheard Jake talking about this on the telephone. As a result, most of Emerys employees now informally discuss the sale of Emerys common stock and how it will affect their jobs. Required: Is Gus Swansons discussion with the team about the prospective sale of Emery unethical? Discuss, citing specific standards from the code of ethical conduct to support your position. (CMA adapted)arrow_forwardIngles Corporation is a manufacturer of tables sold to schools, restaurants, hotels, and other institutions. The table tops are manufactured by Ingles, but the table legs are purchased from an outside supplier. The Assembly Department takes a manufactured table top and attaches the four purchased table legs. It takes 16 minutes of labor to assemble a table. The company follows a policy of producing enough tables to ensure that 40 percent of next months sales are in the finished goods inventory. Ingles also purchases sufficient materials to ensure that materials inventory is 60 percent of the following months scheduled production. Ingless sales budget in units for the next quarter is as follows: Ingless ending inventories in units for July 31 are as follows: Required: 1. Calculate the number of tables to be produced during August. 2. Disregarding your response to Requirement 1, assume the required production units for August and September are 2,100 and 1,900, respectively, and the July 31 materials inventory is 4,000 units. Compute the number of table legs to be purchased in August. 3. Assume that Ingles Corporation will produce 2,340 units in September. How many employees will be required for the Assembly Department in September? (Fractional employees are acceptable since employees can be hired on a part-time basis. Assume a 40-hour week and a 4-week month.) (CMA adapted)arrow_forwardA company manufactures luxury watches made with high-end design materials. The company uses a traditional costing system in assigning overhead costs to the products on the basis of direct labour hours. However, the Production Manager seeks to replace the existing system with the Activity-based Costing (ABC) system to keep control over costs and offer more competitive pricing. After reviewing the existing costing system and interviewing the company’s personnel in relevant departments, the accountant compiled a report highlighting resources and costs involved in manufacturing watches per month: The following table lists out the overhead cost: Activity cost pool Overhead cost (£) Additional Notes Job-order set up 33,000 Procurement and placement 360,000 Installation of winding system 195,000 An auto winding system is fitted with every watch Quality inspection (machine) 60,000 Quality inspection (manual) 21,000 Finishing…arrow_forward

- Phono Company manufactures a plastic toy cell phone. The following standards have been established for the toy’s materials and labor inputs: During the first week of July, the company had the following results:Units produced 90,000Actual labor costs $138,000Actual labor hours 13,400Materials purchased and used 44,250 lbs. @ $1.55 per lb.The purchasing agent located a new source of slightly higher-quality plastic, and this materialwas used during the first week in July. Also, a new manufacturing layout was implemented ona trial basis. The new layout required a slightly higher level of skilled labor. The higher-qualitymaterial has no effect on labor utilization. Similarly, the new manufacturing approach has noeffect on material usage. (Note: Round all variances to the nearest dollar.)Required:1. CONCEPTUAL CONNECTION Compute the materials price and usage variances.Assuming that the materials variances are essentially attributable to the higher quality ofmaterials, would you recommend…arrow_forwardTaylor Inc. produces summer dresses for women. Their dresses are made of cotton fabrics. The line workers are paid an hourly wage and the production supervisor is paid an annual salary. The products are tested for quality control by an independent party which charges a set price per month and an additional charge for each item tested. The machineries are depreciated on a straight-line basis. Which of the following items should be classified as a mixed cost? Group of answer choices Quality control costs Depreciation of the machineries Production supervisor’s salary Cotton fabricsarrow_forwardGordon Company produces custom-made machine parts. A setup activity is required for the batches of parts that it produces. Activity output is measured using setup hours. The value-added standard (SQ) for this activity is zero. On July 1, at the beginning of the fiscal year, 10 setup hours were allowed and used per batch. The standard wage rate for setup labor is $20 per setup hour. During the first quarter of the new fiscal year, the company is planning to implement a new setup method developed by Gordon’s industrial engineers that is expected to reduce setup time by 40 percent. The new procedure was implemented during the first quarter and the improvement expected was realized. Required: 1. What is the setup standard for setup hours and the associated expected cost at the beginning of the first quarter? Setup standard fill in the blank 1 hours per batch Expected cost per batch $fill in the blank 2 The kaizen standard and expected associated cost? Kaizen standard fill in…arrow_forward

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,