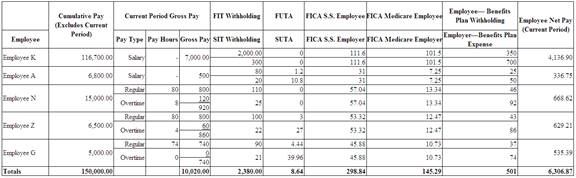

a.

Complete the payroll register by filling in all cells for the pay period ended August 31.

a.

Explanation of Solution

Payroll tax:

Payroll tax refers to the tax that are equally contributed by employees and

employer based on the salary and wages of an employee. Payroll tax includes taxes

like federal tax, local income tax, state tax, social security tax and federal and

state

(Table 1)

b.

Prepare

b.

Explanation of Solution

| Date | Account Titles and Explanation |

Debit (Amount in $) |

Credit (Amount in $) |

| August 31 | Salaries expense | 10,020.00 | |

| FICA - Social security taxes payable | 298.84 | ||

| FICA- Medicare taxes payable | 145.29 | ||

|

Federal income taxes payable- Employee | 2,380.00 | ||

|

State income taxes payable- Employee | 388.00 | ||

| Employee benefits plan payable | 501.00 | ||

| Salaries payable | 6306.87 | ||

| (To record the payroll for period) |

(Table 2)

- Salaries expense is a component of

stockholder’s equity and there is an increase in the value of expense. Hence, debit the salaries expense by $10,020.00 - FICA- Social security taxes payable is a liability and there is an increase in the value of liability. Hence, credit the FICA- social security taxes payable by $298.84.

- FICA- Medicare taxes payable is a liability and there is an increase in the value of liability. Hence, credit the FICA- Medicare taxes payable by $145.29

- Federal income taxes payable- employee is a liability and there is an increase in the value of liability. Hence, credit the federal income taxes payable by $2,380.00.

- State income taxes payable- employee is a liability and there is an increase in the value of liability. Hence, credit the state income taxes payable by $388.00.

- Employee benefits plan payable is a liability and there is an increase in the value of liability. Hence, credit the employee benefits plan payable by $501.00.

- Salaries payable is a liability and there is an increase in the value of liability. Hence, credit the salaries payable by $6,306.87.

c.

Prepare journal entry to record the employer’s cash payment of the net payroll of requirement b.

c.

Explanation of Solution

| Date | Account Titles and Explanation |

Debit (Amount in $) |

Credit (Amount in $) |

| August 31 | Salaries payable | 6,306.87 | |

| Cash | 6306.87 | ||

| (To record the payment of payroll) |

(Table 3)

- Salaries payable is a liability and there is a decrease in the value of liability. Hence, debit the salaries payable by $6,306.87.

- Cash is an asset and there is a decrease the value of an asset. Hence, credit the cash by $6,306.87.

d.

Prepare journal entry to record the employer’s payroll taxes including the contribution to the benefits plan.

d.

Explanation of Solution

| Date | Account Titles and Explanation |

Debit (Amount in $) |

Credit (Amount in $) |

| August 31 | Payroll tax expense | 530.53 | |

| FICA - Social security taxes payable | 298.84 | ||

| FICA- Medicare taxes payable | 145.29 | ||

| Federal unemployment taxes payable | 8.64 | ||

| State unemployment taxes payable | 77.76 | ||

| (To record the payroll taxes) |

(Table 4)

- Payroll tax expense is a component of stockholder’s equity and there is an increase in the value of expense. Hence, debit the payroll tax expense by $530.53.

- FICA- Social security taxes payable is a liability and there is an increase in the value of liability. Hence, credit the FICA- social security taxes payable by $298.84.

- FICA- Medicare taxes payable is a liability and there is an increase in the value of liability. Hence, credit the FICA- Medicare taxes payable by $145.29

- Federal unemployment taxes payable is a liability and there is an increase in the value of liability. Hence, credit the federal unemployment taxes payable by $8.64.

- State unemployment taxes payable is a liability and there is an increase in the value of liability. Hence, credit the state unemployment taxes payable by $77.76.

| Date | Account Titles and Explanation |

Debit (Amount in $) |

Credit (Amount in $) |

| August 31 | Employee benefits expense | 1,002.00 | |

| Employee benefits plan payable | 1,002.00 | ||

| (To record the cost of employee benefits) |

(Table 5)

- Employee benefits expense is a component of stockholder’s equity and there is an increase in the value of expense. Hence, debit the employee benefits expense by $1,002.00.

- Employee benefits plan payable is a liability and there is an increase in the value of liability. Hence, credit the employee benefits plan payable by $1,002.00.

e.

Prepare journal entry to record to pay all liabilities (except for the net payroll in requirement c) for this biweekly period.

e.

Explanation of Solution

| Date | Account Titles and Explanation |

Debit (Amount in $) |

Credit (Amount in $) |

| August 31 | FICA - Social security taxes payable | 597.68 | |

| FICA- Medicare taxes payable | 290.58 | ||

| Federal income taxes payable- employee | 2,380.00 | ||

| State income taxes payable- employee | 388.00 | ||

| Employee benefits plan payable | 1,503.00 | ||

| Federal unemployment taxes payable | 8.64 | ||

| State unemployment taxes payable | 77.76 | ||

| Cash | 5,245.66 | ||

| (To record payment of FICA, income taxes, SUTA, FUTA, and benefit plan contributions) |

(Table 6)

- FICA- Social security taxes payable is a liability and there is a decrease in the value of liability. Hence, debit the FICA- social security taxes payable by $597.68.

- FICA- Medicare taxes payable is a liability and there is a decrease in the value of liability. Hence, debit the FICA- Medicare taxes payable by $290.58.

- Federal income taxes payable- employee is a liability and there is a decrease in the value of liability. Hence, debit the federal income taxes payable by $2,380.00.

- State income taxes payable- employee is a liability and there is a decrease in the value of liability. Hence, debit the state income taxes payable by $388.00.

- Employee benefits plan payable is a liability and there is a decrease in the value of liability. Hence, debit the employee benefits plan payable by $1,503.00

- Federal unemployment taxes payable is a liability and there is a decrease in the value of liability. Hence, debit the federal unemployment taxes payable by $8.64.

- State unemployment taxes payable is a liability and there is a decrease in the value of liability. Hence, debit the state unemployment taxes payable by $77.76.

- Cash is an asset and there is a decrease the value of an asset. Hence, credit the cash by $5,245.66.

Want to see more full solutions like this?

Chapter 11 Solutions

Principles of Financial Accounting.

- Payroll Taxes Sids Grocery Store has 100 employees who earn a wage of $18.75 per hour. Each of Sids employees has worked a total of 160 hours over the month of July. At the time of recording Julys monthly payroll, the following amounts have been withheld: Also, the unemployment tax rate is 2% and applies to all but $30,000 of the gross payroll. Required: 1. What is the amount of net pay recorded by Sids? 2. Make the journal entries to record the payroll.arrow_forwardWages Payable Denton Corporation employs 50 workers in its plant. Each employee is paid $10 per hour and works seven hours per day, Monday through Friday. Employees are paid every Friday. The last payday was Friday, September 19. Required Compute the dollar amount of the weekly payroll. Prepare the journal entry on Friday, September 26, for the payment of the weekly payroll. Denton prepares monthly financial statements. Prepare the adjusting journal entry on Tuesday, September 30, the last day of the month. Prepare the journal entry on Friday, October 3, for the payment of the weekly payroll. Will net income for the month of September be understated or overstated if Denton doesnt bother with an adjusting entry on September 30? Explain your answer.arrow_forwardAn analysis of the payroll for the month of November for CinMar Inc. reveals the information shown: All regular time Andrews, Lomax, and Herzog are production workers, and Dimmick is the plant manager. Hendrick is in charge of the office. Cumulative earnings paid (before deductions) in this calendar year prior to the payroll period ending November 8 were as follows: Andrews, 21,200; Lomax, 6,800; Herzog, 11,500; Dimmick, 116,200; and Hendrick, 32,800. The solution to this problem requires the following forms, using the indicated column headings: 1. Prepare an employee earnings record for each of the five employees. 2. Prepare a payroll record for each of the four weeks. 3. Prepare a labor cost summary for the month. 4. Prepare journal entries to record the following: a. The payroll for each of the four weeks. b. The payment of wages for each of the four payrolls. c. The distribution of the monthly labor costs per the labor cost summary. d. The company's payroll taxes covering the four payroll periods.arrow_forward

- Accounting for bonus and vacation pay Cathy Muench a factory worker, earns 1,000 each week. In addition, she will receive a 4,000 bonus at year-end and a four-week paid vacation. Prepare the entry to record the weekly payroll and the costs and liabilities related to the bonus and the vacation pay, assuming that Muench is the only employee.arrow_forwardA weekly payroll summary made from labor time records shows the following data for Pima Company: Overtime is payable at one-and-a-half times the regular rate of pay and is distributed to all jobs worked on during the period. a. Determine the net pay of each employee. The income taxes withheld for each employee amount to 15% of the gross wages. b. Prepare journal entries for the following: 1. Recording the payroll. 2. Paying the payroll. 3. Distributing the payroll. (Assume that the overtime premium will be charged to all jobs worked on during the period.) 4. The employers payroll taxes. (Assume that none of the employees has achieved the maximum wage bases for FICA and unemployment taxes.)arrow_forwardIrina Company pays its employees weekly. The last pay period for 20-1 was on December 28. From December 28 through December 31, the employees earned 1,754, so the following adjusting entry was made: The first pay period in 20-2 was on Januar)-4. The totals line from Irina Companys payroll register for the week ended Januar)-4, 20-2, was as follows: REQUIRED 1. Prepare the journal entry for the payment of the payroll on January 4, 20-2. 2. Prepare T accounts for Wages and Salaries Expense and Wages and Salaries Payable showing the beginning balance, January 4, 20-2, entry, and aiding balance as of January 4, 20-2.arrow_forward

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning

Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning College Accounting, Chapters 1-27 (New in Account...AccountingISBN:9781305666160Author:James A. Heintz, Robert W. ParryPublisher:Cengage Learning

College Accounting, Chapters 1-27 (New in Account...AccountingISBN:9781305666160Author:James A. Heintz, Robert W. ParryPublisher:Cengage Learning College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub

College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning

Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning